Global Dementia Treatment Market

Market Size in USD Billion

CAGR :

%

USD

19.98 Billion

USD

38.37 Billion

2025

2033

USD

19.98 Billion

USD

38.37 Billion

2025

2033

| 2026 –2033 | |

| USD 19.98 Billion | |

| USD 38.37 Billion | |

| % | |

|

Dementia Treatment Market Size

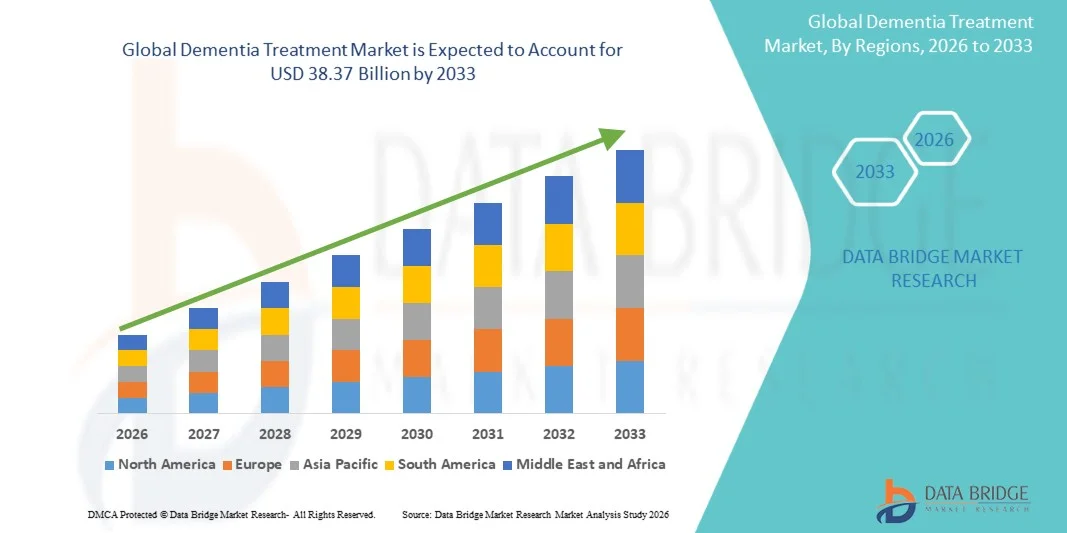

- The global dementia treatment market size was valued at USD 19.98 billion in 2025 and is expected to reach USD 38.37 billion by 2033, at a CAGR of 8.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of dementia and other cognitive disorders, along with a growing aging population worldwide, leading to higher demand for effective therapeutic interventions

- Furthermore, rising investments in research and development of innovative drugs, cognitive therapies, and personalized treatment approaches are accelerating the uptake of Dementia Treatment solutions, thereby significantly boosting the industry's growth

Dementia Treatment Market Analysis

- Dementia treatments, including pharmacological and non-pharmacological therapies, are increasingly vital components of modern healthcare for aging populations due to their potential to slow cognitive decline, manage symptoms, and improve quality of life

- The escalating demand for dementia treatments is primarily fueled by the growing prevalence of cognitive disorders, increasing awareness about early diagnosis, and rising investments in healthcare infrastructure for neurodegenerative diseases

- North America dominated the dementia treatment market with the largest revenue share of 38.7% in 2025, driven by a strong presence of leading pharmaceutical companies, well-established healthcare infrastructure, and increasing public awareness about dementia management

- Asia-Pacific is expected to be the fastest growing region in the dementia treatment market during the forecast period due to rising geriatric population, improving healthcare access, and expanding medical facilities, with a projected CAGR of 9.8%

- The Oral segment dominated the largest market revenue share of 61.4% in 2025, due to convenience, patient adherence, and availability of most dementia pharmacotherapies in tablet or capsule form

Report Scope and Dementia Treatment Market Segmentation

|

Attributes |

Dementia Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Eli Lilly and Company (U.S.) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Dementia Treatment Market Trends

“Rising Prevalence of Dementia and Growing Awareness Among Patients and Caregivers”

- The increasing global prevalence of dementia, particularly Alzheimer’s disease, is a primary driver for market growth. Aging populations in regions such as North America, Europe, and Asia-Pacific are contributing to a growing patient pool requiring effective treatment and care solutions

- For instance, in 2025, the U.S. Alzheimer’s Association reported that over 6.7 million Americans aged 65 and above are living with dementia, highlighting the urgent need for innovative therapeutic options and supportive care programs

- Increasing awareness among patients, caregivers, and healthcare professionals about early diagnosis, management, and available therapies is fueling the adoption of medications and therapy-based treatments. Early intervention programs and routine cognitive screening in hospitals and clinics are further supporting market expansion

- Furthermore, government and non-government initiatives aimed at improving dementia care, such as funding for research, public awareness campaigns, and patient assistance programs, are creating favorable conditions for market growth

- The rising focus on personalized and combination therapy approaches, including cognitive-enhancing drugs, symptomatic treatments, and lifestyle interventions, is boosting both the demand for medications and therapeutic services in hospitals, specialty clinics, and homecare settings

Dementia Treatment Market Dynamics

Driver

“Increasing Investments in Research and Development for Novel Therapies”

- The Dementia Treatment market is witnessing significant investment in research and development, particularly for disease-modifying therapies and innovative drug delivery methods. Pharmaceutical companies are prioritizing clinical trials to develop medications that slow disease progression and improve cognitive function

- For instance, in 2024, Biogen and Eisai expanded late-stage clinical trials for their Alzheimer’s disease therapies targeting amyloid plaques, demonstrating a strong industry focus on breakthrough treatments

- In addition, biotechnology advancements, including monoclonal antibodies and combination therapies, are contributing to a diversified treatment landscape and enabling tailored solutions for patients based on disease type (Amnestic and Non-Amnestic Dementia)

- Collaborations between academic institutions, biotech startups, and pharmaceutical giants are accelerating drug discovery, while increasing funding for dementia research supports continuous innovation and market expansion

- Healthcare providers are also integrating multidisciplinary treatment approaches combining medications with cognitive therapy, lifestyle management, and caregiver support programs, reflecting a holistic market trend

Restraint/Challenge

“High Treatment Costs and Limited Access in Emerging Regions”

- The high cost of novel dementia medications and long-term therapies poses a significant challenge to widespread adoption, particularly in developing countries and among uninsured or underinsured patients

- For instance, advanced Alzheimer’s drugs and combination therapy regimens can cost several thousand dollars per year, limiting access for patients without government or insurance coverage

- Unequal access to healthcare infrastructure, especially in rural and underserved areas, restricts timely diagnosis and treatment, further constraining market growth

- Additional challenges include the limited efficacy of existing treatments in halting disease progression and the need for ongoing monitoring and follow-up care, which require substantial healthcare resources

- Overcoming these restraints will require increased government funding, insurance coverage expansion, cost-effective generic formulations, and educational initiatives aimed at healthcare providers and caregivers to improve early diagnosis and adherence to treatment protocols

Dementia Treatment Market Scope

The market is segmented on the basis of type, drug class, therapy type, route of administration, and end-users.

• By Types

On the basis of types, the market is segmented into Alzheimer's Disease Dementia, Vascular Dementia, Dementia With Lewy Bodies (DLB), Parkinson's Disease Dementia, Mixed Dementia, Frontotemporal Dementia, and Others. The Alzheimer's Disease Dementia segment dominated the largest market revenue share of 38.6% in 2025, due to the high prevalence among elderly populations and established treatment protocols. Hospitals and specialty clinics prioritize Alzheimer’s therapies for early intervention and cognitive management. Government initiatives and awareness programs support diagnosis and treatment adoption. Clinical guidelines encourage pharmacological and non-pharmacological approaches. Patient adherence programs reinforce long-term therapy continuity. Hospital pharmacies ensure steady drug supply. Ongoing R&D in novel therapies drives physician confidence. Insurance coverage improves patient access. Homecare adoption complements hospital-based care. Public and private funding support early detection programs. Clinical trials and real-world studies validate treatment outcomes. Multidisciplinary care models enhance patient management.

The Vascular Dementia segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by increasing diagnosis of cerebrovascular-related cognitive impairments and rising adoption of cognitive therapies. Hospitals and homecare services integrate multidisciplinary care. Awareness campaigns enhance early screening. Specialty clinics implement therapy programs. Insurance coverage encourages patient access. Clinical evidence supports efficacy of pharmacological and non-pharmacological interventions. Emerging markets show adoption growth. Telemedicine and remote monitoring improve adherence. Caregiver education enhances patient outcomes. Pipeline developments in novel drugs expand options. Early intervention programs accelerate uptake. Home-based cognitive therapy adoption rises. Combination approaches with lifestyle interventions increase preference.

• By Drug Class

On the basis of drug class, the market is segmented into MAO Inhibitors, Glutamate Inhibitors, Cholinesterase Inhibitors, and Others. The Cholinesterase Inhibitors segment dominated the largest market revenue share of 42.7% in 2025, due to established efficacy in slowing cognitive decline in Alzheimer’s and related dementias. Hospitals and specialty clinics widely prescribe cholinesterase inhibitors for early- and mid-stage dementia. Insurance coverage supports access. Hospital pharmacies ensure steady supply and adherence monitoring. Clinical guidelines and physician preference reinforce adoption. Patient education enhances compliance. Combination therapies with cognitive stimulation improve outcomes. R&D pipeline continues for enhanced formulations. Homecare programs integrate oral therapies. Long-term therapy cycles maintain recurring demand. Government programs support early intervention.

The MAO Inhibitors segment is expected to witness the fastest CAGR of 7.1% from 2026 to 2033, driven by emerging evidence of their efficacy in Parkinson's Disease Dementia and Lewy Body Dementia. Hospitals and specialty clinics adopt MAO inhibitors in combination regimens. Homecare adoption of oral therapies improves adherence. Pipeline R&D supports novel formulations. Insurance coverage facilitates access. Awareness campaigns increase diagnosis and early treatment. Outpatient services and telemedicine integrate therapy management. Clinical trial data validate safety and efficacy. Specialty clinics expand treatment protocols. Multidisciplinary approaches enhance outcomes. Patient preference for targeted therapies supports growth. Emerging markets show increasing uptake. Combination with cognitive therapies improves functional outcomes.

• By Therapy Type

On the basis of therapy type, the market is segmented into Cognitive Stimulation Therapy and Cognitive Behavioral Therapy (CBT). The Cognitive Stimulation Therapy segment dominated the largest market revenue share of 46.3% in 2025, due to its established role in improving cognitive function and quality of life in dementia patients. Hospitals and specialty clinics implement structured therapy programs. Homecare providers integrate therapy into daily routines. Awareness campaigns improve patient and caregiver participation. Clinical guidelines support therapy for mild to moderate dementia. Patient adherence programs reinforce outcomes. Research demonstrates long-term cognitive benefits. Multidisciplinary teams facilitate therapy delivery. Government initiatives fund early intervention programs. Emerging clinics adopt therapy protocols. Digital platforms enable remote engagement. Insurance coverage supports therapy sessions. Combination with pharmacological treatment enhances efficacy.

The Cognitive Behavioral Therapy (CBT) segment is expected to witness the fastest CAGR of 7.5% from 2026 to 2033, driven by rising adoption for behavioral and psychological symptoms associated with dementia. Hospitals and specialty clinics increasingly implement CBT programs. Homecare providers integrate CBT into care routines. Telehealth and digital CBT platforms enhance accessibility. Clinical studies validate efficacy in reducing anxiety and depression in dementia patients. Patient and caregiver education promotes adherence. Insurance coverage supports outpatient therapy sessions. Emerging markets adopt CBT programs. Combination with cognitive stimulation therapies improves overall outcomes. Clinical guidelines increasingly recommend CBT. Research supports efficacy in Lewy Body and Frontotemporal Dementia. Home-based therapy adoption grows. Multidisciplinary management improves patient outcomes.

• By Route of Administration

On the basis of route of administration, the market is segmented into Oral and Parenteral. The Oral segment dominated the largest market revenue share of 61.4% in 2025, due to convenience, patient adherence, and availability of most dementia pharmacotherapies in tablet or capsule form. Hospitals and homecare services prioritize oral medications for long-term management. Specialty clinics prescribe oral drugs to maintain outpatient care efficiency. Insurance coverage supports patient access. Hospital pharmacies ensure immediate availability. Combination therapy with cognitive stimulation enhances outcomes. Physician familiarity and clinical guidelines reinforce oral drug adoption. Emerging markets adopt oral formulations. Research supports efficacy and safety. Long-term treatment cycles drive recurring demand. Telemedicine supports adherence monitoring. Homecare programs integrate oral therapy.

The Parenteral segment is expected to witness the fastest CAGR of 6.8% from 2026 to 2033, driven by novel injectable therapies under clinical evaluation for moderate-to-severe dementia. Hospitals administer parenteral formulations under controlled supervision. Specialty clinics adopt injections for specific indications. Homecare integration supports nurse-administered therapy. Pipeline R&D expands parenteral drug options. Insurance coverage facilitates access. Patient preference for fast-acting treatments drives uptake. Combination therapies with oral drugs enhance outcomes. Emerging markets show increasing adoption. Telemedicine supports therapy monitoring. Clinical guidelines promote parenteral therapy for select cases. Multidisciplinary oversight ensures safe administration.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Hospitals segment dominated the largest market revenue share of 63.2% in 2025, due to centralized care, access to specialists, and inpatient monitoring for dementia patients. Hospitals manage complex therapy combinations, adherence programs, and cognitive interventions. Insurance coverage supports patient access. Hospital pharmacies ensure availability of pharmacotherapies. Multidisciplinary teams deliver integrated care. Clinical guidelines reinforce hospital-based treatment. Long-term follow-up programs improve patient outcomes. Research and clinical trials support hospital dominance. Advanced infrastructure enables therapy delivery. Public awareness and early intervention programs drive adoption.

The Homecare segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, fueled by telemedicine services, remote monitoring, and patient preference for receiving care at home. Homecare providers integrate pharmacotherapy with cognitive stimulation therapy. Specialty clinics support home-based management. Insurance coverage improves adoption. Digital health platforms enhance adherence. Patient and caregiver education encourages participation. Early intervention and preventive care programs accelerate uptake. Emerging markets show increased homecare adoption. Outpatient therapy programs support growth. Combination therapy adoption rises. Multidisciplinary coordination ensures continuity of care.

Dementia Treatment Market Regional Analysis

- North America dominated the dementia treatment market with the largest revenue share of 38.7% in 2025, driven by a strong presence of leading pharmaceutical companies, well-established healthcare infrastructure, and increasing public awareness about dementia management

- The region benefits from extensive clinical research, advanced diagnostic facilities, and government-supported programs aimed at improving dementia care and early detection

- High healthcare expenditure, widespread availability of specialized clinics and hospitals, and supportive reimbursement policies for dementia medications are further accelerating market growth

U.S. Dementia Treatment Market Insight

The U.S. dementia treatment market captured the largest share within North America in 2025, fueled by high patient awareness and adoption of innovative therapeutic options. The country is a global hub for dementia research, with several key pharmaceutical companies actively investing in the development of disease-modifying therapies and symptomatic treatments. Extensive clinical trial activity, combined with strong regulatory support from the FDA, is enabling the faster introduction of new medications and therapeutic solutions. Public and private initiatives promoting early diagnosis, caregiver education, and patient assistance programs are expanding access to treatment, contributing to sustained market growth. The increasing prevalence of Alzheimer’s disease and other dementia types among the aging population is driving consistent demand for both medications and therapy-based interventions across hospitals, specialty clinics, and homecare settings.

Europe Dementia Treatment Market Insight

The Europe dementia treatment market is projected to grow at a substantial CAGR over the forecast period, primarily driven by increasing geriatric populations and rising healthcare awareness. Stringent healthcare policies, reimbursement schemes, and dementia management programs in countries such as Germany, France, and Italy are encouraging wider adoption of therapeutic solutions. Urbanization and increasing access to specialized hospitals and clinics are facilitating early diagnosis and treatment initiation. Growth is observed across multiple end users, including hospitals, specialty clinics, and homecare services, with a strong focus on personalized care plans and patient support initiatives.

U.K. Dementia Treatment Market Insight

The U.K. Dementia Treatment market is expected to expand at a notable CAGR during the forecast period. Rising prevalence of dementia, combined with government-backed healthcare initiatives such as the National Dementia Strategy, is promoting better diagnosis and treatment coverage. Increasing public awareness and caregiver support programs are enhancing adherence to treatment regimens and encouraging early intervention. Expansion in healthcare infrastructure and robust pharmaceutical presence ensures the availability of both branded and generic dementia medications.

Germany Dementia Treatment Market Insight

Germany’s dementia treatment market is projected to grow steadily, supported by strong healthcare infrastructure, well-developed geriatric care services, and increasing patient awareness. Emphasis on preventive care, early diagnosis, and ongoing cognitive therapy programs is driving the adoption of both medications and therapy-based interventions. Government initiatives promoting elderly care and specialized dementia clinics further strengthen market expansion. Growing R&D investments by domestic and international pharmaceutical companies are fostering the development of innovative therapies in the region.

Asia-Pacific Dementia Treatment Market Insight

The Asia-Pacific dementia treatment market is poised to grow at the fastest CAGR of 9.8% during the forecast period, driven by a rapidly aging population, increasing geriatric healthcare facilities, and rising awareness about cognitive disorders. Countries such as China, Japan, and India are witnessing increased public and private investment in dementia care infrastructure. Expanding healthcare access, improving affordability of medications, and rising number of specialty clinics and hospitals are boosting market penetration. Government-led initiatives, awareness campaigns, and training programs for healthcare professionals are enhancing early diagnosis and patient management.

Japan Dementia Treatment Market Insight

Japan’s dementia treatment market is growing steadily due to the country’s significant aging population and well-established healthcare system. Public health programs aimed at supporting dementia patients and caregivers are improving disease management and treatment adherence. The adoption of both pharmacological and non-pharmacological therapies is increasing, reflecting a holistic approach to cognitive care. Increasing research funding and clinical trial activities for novel dementia therapies are fostering innovation and expanding treatment options.

China Dementia Treatment Market Insight

China dementia treatment market accounted for the largest revenue share in Asia-Pacific in 2025, supported by rising elderly population, expanding healthcare facilities, and increasing government focus on geriatric and cognitive care. Rapid urbanization, rising disposable income, and growing health awareness among the elderly are driving demand for dementia treatments. Government initiatives promoting early diagnosis, patient support programs, and the expansion of specialized hospitals are creating favorable conditions for market growth. Both branded and generic medications are widely accessible, enhancing affordability and encouraging adoption across hospitals, specialty clinics, and homecare settings.

Dementia Treatment Market Share

The Dementia Treatment industry is primarily led by well-established companies, including:

• Eli Lilly and Company (U.S.)

• Roche Holding AG (Switzerland)

• Biogen Inc. (U.S.)

• AstraZeneca (U.K.)

• Novartis AG (Switzerland)

• ACADIA Pharmaceuticals Inc. (U.S.)

• Eisai Co., Ltd. (Japan)

• Axsome Therapeutics, Inc. (U.S.)

• Anavex Life Sciences Corp. (U.S.)

• Merck & Co., Inc. (U.S.)

• Sunovion Pharmaceuticals Inc. (U.S.)

• PharmaMar, S.A. (Spain)

• Valeant Pharmaceuticals (Canada)

• Gilead Sciences, Inc. (U.S.)

• Johnson & Johnson (U.S.)

• MediciNova, Inc. (U.S.)

• AC Immune SA (Switzerland)

• Cassava Sciences, Inc. (U.S.)

• Proteostasis Therapeutics, Inc. (U.S.)

• UCB S.A. (Belgium)

Latest Developments in Global Dementia Treatment Market

- In June 2021, the U.S. Food and Drug Administration (FDA) approved Aducanumab (Aduhelm), a monoclonal antibody therapy designed to reduce amyloid plaque in the brain and treat Alzheimer’s disease, marking the first new disease‑modifying dementia treatment approved in the U.S. in years

- In January 2023, the FDA granted accelerated approval to Lecanemab (Leqembi) — jointly developed by Eisai and Biogen — for treating early Alzheimer’s disease, showing slowed cognitive decline in patients with mild dementia or mild cognitive impairment

- In July 2023, Biogen and Eisai converted the accelerated approval of Leqembi (lecanemab) to traditional full FDA approval, solidifying its status as a disease‑modifying therapy for early Alzheimer’s and dementia progression

- In July 2024, the *FDA approved Donanemab (brand name Kisunla) — developed by Eli Lilly — for early‑stage Alzheimer’s disease and mild dementia, offering another anti‑amyloid treatment option that targets underlying disease pathology

- In May 2024, lecanemab (Leqembi) gained regulatory approval in South Korea, expanding access to this dementia therapy outside the U.S. market

- In April 2025, the European Commission granted marketing authorization for Leqembi (lecanemab) across the European Union, marking a key regulatory milestone for treating early Alzheimer’s disease and associated dementia

- In July 2025, the Saudi Food and Drug Authority (SFDA) approved Leqembi (lecanemab) as the first Alzheimer’s treatment available in Saudi Arabia, expanding dementia therapeutic options in the Middle East

- In September 2025, the Therapeutic Goods Administration (TGA) of Australia approved Leqembi (lecanemab) for treating early Alzheimer’s disease and mild dementia, after a review process that reversed an earlier decision

- In January 2025, the FDA granted Fast Track designation to Posdinemab, an investigational anti‑tau antibody therapy, streamlining its development and review for the treatment of Alzheimer’s‑related dementia

- In March 2025, Longeveron Inc. announced positive regulatory feedback from the FDA supporting advancement of laromestrocel (Lomecel‑BTM) into Phase II/III clinical trials as a potential cellular therapy for Alzheimer’s disease

- In February 2025, Merck triggered a USD 15 million milestone payment to Neuphoria Therapeutics upon initiating Phase II trials of MK‑1167, a novel α7 nicotinic acetylcholine receptor modulator for Alzheimer’s dementia symptom treatment

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.