Global Dental Membrane Bone Graft Substitute Market

Market Size in USD Billion

CAGR :

%

USD

1.22 Billion

USD

2.43 Billion

2025

2033

USD

1.22 Billion

USD

2.43 Billion

2025

2033

| 2026 –2033 | |

| USD 1.22 Billion | |

| USD 2.43 Billion | |

| % | |

|

Dental Membrane and Bone Graft Substitute Market Size

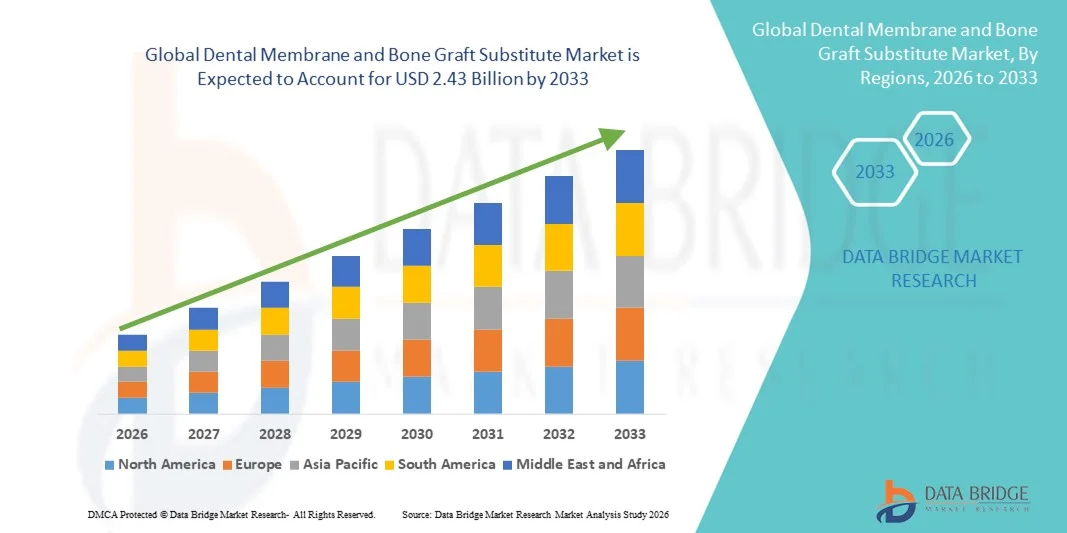

- The global dental membrane and bone graft substitute market size was valued at USD 1.22 billion in 2025 and is expected to reach USD 2.43 billion by 2033, at a CAGR of 9.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of dental diseases, rising demand for implantology and regenerative procedures, and the growing adoption of advanced biomaterials for oral care

- Furthermore, rising consumer awareness regarding aesthetic dentistry and minimally invasive treatments, along with technological advancements in membrane and bone graft substitute materials, is driving the uptake of Dental Membrane and Bone Graft Substitute solutions, thereby significantly boosting the industry's growth

Dental Membrane and Bone Graft Substitute Market Analysis

- Dental membranes and bone graft substitutes, offering advanced solutions for tissue regeneration and bone repair, are increasingly vital components of modern dental and oral surgery procedures in both hospitals and specialized dental clinics due to their enhanced biocompatibility, ease of use, and clinical effectiveness

- The escalating demand for dental membranes and bone graft substitutes is primarily fueled by the growing prevalence of dental implant procedures, increasing adoption of minimally invasive surgeries, and rising awareness among dental professionals and patients regarding periodontal regeneration and alveolar ridge preservation

- North America dominated the dental membrane and bone graft substitute market with the largest revenue share of 38.7% in 2025, supported by advanced dental care infrastructure, high adoption of implantology procedures, strong presence of leading biomaterial manufacturers, and favorable reimbursement frameworks

- Asia-Pacific is expected to be the fastest-growing region in the dental membrane and bone graft substitute market during the forecast period, expanding at a CAGR of 9.4% from 2026 to 2033, driven by rising investments in dental clinic modernization, growing patient awareness, and increasing demand for regenerative dental therapies

- The dental membranes segment dominated the largest market revenue share of 45.6% in 2025, primarily due to its extensive use in guided tissue regeneration (GTR) and guided bone regeneration (GBR) procedures

Report Scope and Dental Membrane and Bone Graft Substitute Market Segmentation

|

Attributes |

Dental Membrane and Bone Graft Substitute Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Dental Membrane and Bone Graft Substitute Market Trends

Increasing Prevalence of Dental Disorders and Implant Surgeries

- The rising prevalence of periodontal diseases, tooth loss, and alveolar bone deficiencies is driving the global market, as patients increasingly seek restorative solutions

- Expanding adoption of dental implants and oral reconstructive surgeries has intensified the demand for bone graft materials and barrier membranes

- For instance, in 2025, major dental chains in the U.S., such as Aspen Dental and Pacific Dental Services, reported a significant increase in implant procedures, with over 3.5 million dental implants performed in North America alone, significantly boosting the use of graft substitutes. Similarly, clinics in Germany and Japan are increasingly using xenograft and allograft materials for ridge augmentation and sinus lift procedures

- Continuous in biomaterial science, such as collagen-based and synthetic membranes, improve clinical outcomes, enhance graft stability, and reduce post-operative complications, thereby increasing clinician confidence

- The aging population globally is fueling demand, as older adults often require bone grafting for successful implant placement and oral rehabilitation

- Integration of regenerative dental techniques, such as guided bone regeneration (GBR) and socket preservation, into routine practice encourages broader adoption of specialized grafting products

- Increasing patient awareness regarding long-term oral health, functional restoration, and aesthetic outcomes is enhancing the market’s penetration, particularly in urban regions with advanced dental care infrastructure

Dental Membrane and Bone Graft Substitute Market Dynamics

Driver

Growing Adoption of Minimally Invasive and Regenerative Dental Procedures

- The global Dental Membrane and Bone Graft Substitute market is increasingly influenced by the adoption of minimally invasive and regenerative dental techniques, which reduce patient recovery times and improve surgical outcomes

- For instance, clinics such as Kuraray Noritake Dental in Japan and BioHorizons in the U.S. have incorporated advanced guided bone regeneration (GBR) protocols using resorbable collagen membranes and synthetic bone grafts. These procedures allow dentists to achieve predictable alveolar ridge preservation and sinus augmentation with minimal surgical trauma

- In addition, Straumann Group has reported a rising demand for its biomimetic graft materials in Europe, driven by dentists performing immediate implant placement combined with socket preservation techniques

- Technological innovations, such as 3D-printed bone scaffolds and injectable graft materials, are gaining traction, offering customized solutions that conform precisely to defect geometries

- The trend toward combining bone graft substitutes with growth factors, stem cells, or platelet-rich fibrin (PRF) is enabling enhanced osteogenesis and faster healing, further supporting adoption

- Increased integration of digital dentistry tools, including cone-beam computed tomography (CBCT) imaging and CAD/CAM surgical guides, allows precise planning and placement of membranes and grafts, reducing errors and improving clinical success

- Rising patient preference for procedures with minimal post-operative discomfort and better aesthetic outcomes continues to drive the adoption of advanced grafting techniques across private clinics, hospitals, and academic dental centers

Restraint/Challenge

High Costs and Limited Reimbursement Policies

- The relatively high cost of advanced dental membranes and bone graft substitutes remains a key challenge for widespread adoption, particularly in emerging markets and smaller dental practices. Premium materials such as cross-linked collagen membranes, synthetic hydroxyapatite granules, or xenografts can significantly increase treatment expenses compared to conventional bone grafting techniques

- For instance, in the U.S., products like Geistlich Bio-Gide and OsteoBiol® command high prices, making them less accessible for patients without comprehensive dental insurance coverage. Similarly, in India, private clinics report that the out-of-pocket cost for guided bone regeneration procedures using premium graft materials can deter middle-income patients from opting for advanced regenerative solutions

- Limited reimbursement under national or private dental insurance plans further constrains adoption, as many healthcare systems categorize advanced bone grafting procedures as elective rather than essential. In Europe, while countries like Germany provide partial coverage for GBR in implantology, other regions have inconsistent reimbursement policies, affecting treatment uptake

- Another challenge is the variability in clinical outcomes and practitioner expertise. Improper handling of membranes or grafts can lead to complications such as infection, graft exposure, or delayed healing, which may discourage both practitioners and patients from using these advanced products

- Educational gaps and limited training opportunities in regenerative dentistry also contribute to slow adoption in certain regions. For instance, smaller clinics in Southeast Asia and Latin America often lack access to hands-on workshops or certified training programs for complex grafting procedures

- Overcoming these restraints requires increased awareness, more cost-effective material options, and expanded insurance coverage, alongside continuous practitioner education to ensure predictable and safe clinical outcomes

Dental Membrane and Bone Graft Substitute Market Scope

The market is segmented on the basis of product type, material, application, and end use.

- By Product Type

On the basis of product type, the Dental Membrane and Bone Graft Substitute market is segmented into Dental Membranes and Dental Bone Grafts. The dental membranes segment dominated the largest market revenue share of 45.6% in 2025, primarily due to its extensive use in guided tissue regeneration (GTR) and guided bone regeneration (GBR) procedures. Dental membranes provide a barrier to prevent soft tissue ingrowth while enabling bone regeneration, making them a critical component in implantology and periodontal surgeries. Hospitals and dental clinics prefer these membranes for their predictable clinical outcomes and biocompatibility. Increasing adoption of implant-based restorative procedures across both developed and emerging markets significantly contributes to segment dominance. Technological innovations, such as resorbable collagen-based membranes and barrier membranes with enhanced handling properties, improve efficiency in clinical settings. Growing geriatric population and rising prevalence of periodontal diseases further drive usage. Dental education and training programs emphasize the use of membranes for regenerative procedures. Government healthcare initiatives and insurance coverage for dental treatments also support market growth. Rising awareness about oral health and aesthetic dentistry promotes adoption in private practices. Multi-specialty dental clinics are increasingly incorporating membranes in routine surgical protocols. Increasing collaborations between dental manufacturers and hospitals facilitate widespread availability. Rising patient demand for minimally invasive and faster-healing procedures strengthens the segment’s position.

The dental bone grafts segment is expected to witness the fastest CAGR of 12.3% from 2026 to 2033, driven by increasing demand for alveolar ridge augmentation, implant bone regeneration, and sinus lift procedures. Bone grafts, including autografts, allografts, and synthetic grafts, are widely preferred to restore bone volume and support successful implant integration. Rising dental implant surgeries globally significantly fuel segment growth. Innovations such as bioactive and composite bone grafts enhance bone regeneration and clinical predictability. Increasing prevalence of edentulism and trauma cases further drives demand. Advanced bone graft materials reduce patient morbidity and improve healing time, boosting adoption. Expansion of dental implant centers in emerging economies accelerates market penetration. Growing investment in dental research and regenerative materials strengthens technological advancements. Rising patient awareness regarding long-term implant success increases preference for grafts. Collaborations between manufacturers and dental clinics for clinical trials enhance trust and usage. Government support for oral healthcare infrastructure encourages adoption. The aesthetic and functional benefits of bone grafts in complex dental surgeries reinforce their fast-growing trajectory.

- By Material

On the basis of material, the market is segmented into Hydrogel, Collagen, Human Cell Source, Hydroxyapatite and Tricalcium Phosphate, and Polytetrafluoroethylene. The collagen segment dominated the largest market revenue share of 39.8% in 2025, driven by its superior biocompatibility, resorbability, and ability to support soft tissue healing. Collagen-based membranes and bone substitutes are widely preferred in both periodontal and implant surgeries. Hospitals and dental clinics prioritize collagen materials for predictable clinical outcomes. Increasing focus on minimally invasive procedures enhances segment adoption. Collagen products reduce postoperative complications, improving patient satisfaction. Regulatory approvals and established clinical protocols further strengthen usage. Technological advancements improving tensile strength and handling properties drive preference. Growth in aesthetic and implant dentistry boosts segment dominance. Rising geriatric population and prevalence of periodontitis drive increased procedure volumes. Dental education programs emphasize collagen-based regenerative techniques. Collaborations with research institutes accelerate innovation and adoption. Strong supply chain presence ensures availability across regions, supporting consistent market growth.

The human cell source segment is projected to witness the fastest CAGR of 13.7% from 2026 to 2033, fueled by increasing research and clinical adoption of autologous and stem cell-based grafting techniques. Human-derived materials improve bone regeneration, accelerate healing, and reduce immunogenic risks. Rising awareness about regenerative dentistry and personalized treatments drives adoption. Technological advancements in cell preservation, scaffold development, and bioactive coatings enhance performance. Hospitals and specialized dental clinics are increasingly investing in regenerative solutions for complex defects. Government funding for stem cell research promotes development and clinical implementation. Rising prevalence of alveolar bone loss and complex maxillofacial surgeries further fuels demand. Integration with advanced surgical navigation systems improves procedural accuracy. Growing patient preference for minimally invasive, natural tissue-based solutions accelerates adoption. Collaborations between biotech firms and dental research centers strengthen innovation pipelines. Expansion of dental regenerative therapy programs across academic and clinical institutions supports rapid market growth. Increasing clinical trials validating efficacy encourage widespread adoption.

- By Application

On the basis of application, the market is segmented into Ridge Augmentation, Socket Preservation, Periodontal Defect Regeneration, Implant Bone Regeneration, Sinus Lift, and Others. The implant bone regeneration segment dominated the largest market revenue share of 41.5% in 2025, driven by increasing global dental implant procedures. Bone grafts and membranes are critical for ensuring stable implant placement and long-term osseointegration. Rising aesthetic dentistry demand and restorative procedures across geriatric and adult populations support segment dominance. Hospitals and dental clinics prefer bone regenerative procedures for predictable outcomes. Technological advancements in graft materials, barrier membranes, and guided regeneration tools further enhance clinical adoption. Increasing training in implantology across dental schools strengthens segment utilization. Regulatory approvals for biocompatible grafts and membranes ensure clinical safety. Growing prevalence of edentulism and traumatic dental injuries increase procedural volume. Rising insurance coverage for dental implants encourages adoption. Development of specialized dental clinics focusing on implantology drives segment growth. Collaborative clinical research validates long-term efficacy and promotes market trust. Global expansion of dental healthcare infrastructure supports demand.

The ridge augmentation segment is expected to witness the fastest CAGR of 12.9% from 2026 to 2033, driven by the need to restore alveolar bone volume prior to implant placement and manage severe periodontal defects. Ridge augmentation procedures are increasingly preferred to improve implant success rates and esthetic outcomes. Rising dental implant adoption in emerging and developed markets significantly fuels segment growth. Advanced graft materials, including autografts, allografts, and synthetic composites, improve procedural outcomes and accelerate healing. Increasing prevalence of bone resorption due to aging and periodontal disease drives demand. Hospitals and dental clinics are adopting minimally invasive ridge augmentation techniques to reduce patient morbidity. Research and development in bioactive and composite grafts strengthen segment adoption. Collaboration between regenerative medicine firms and dental practices promotes usage. Training programs for oral surgeons emphasize ridge augmentation protocols. Government initiatives promoting oral health awareness further encourage adoption. Technological advancements in 3D-printed scaffolds enhance precision in ridge augmentation procedures. Expansion of dental specialty centers globally accelerates market penetration.

- By End Use

On the basis of end use, the market is segmented into Hospitals, Dental Clinics, and Ambulatory Surgical Centers. The dental clinics segment dominated the largest market revenue share of 46.2% in 2025, owing to the increasing number of private dental practices offering implantology and periodontal treatments. Clinics provide high procedural volumes with specialized care, supporting dominance. Rising patient preference for minimally invasive and cosmetic dental procedures enhances adoption. Clinics frequently utilize both membranes and bone graft substitutes for routine regenerative procedures. Technological adoption, including guided surgery and digital imaging, improves procedural efficiency. Insurance coverage for dental procedures in certain regions encourages patient uptake. Expansion of chain dental clinics in urban and semi-urban areas strengthens market reach. Continuing dental education programs promote use of advanced regenerative materials. Integration of clinics with laboratories ensures availability of high-quality graft materials. Patient awareness about esthetic and functional outcomes further drives segment demand. Rising prevalence of tooth loss and periodontal disease enhances procedural volumes. Government initiatives supporting oral healthcare access indirectly benefit clinic-based adoption.

The ambulatory surgical centers segment is projected to witness the fastest CAGR of 11.8% from 2026 to 2033, driven by growing outpatient surgical procedures and minimally invasive dental surgeries. Ambulatory centers offer cost-effective and convenient alternatives to hospital-based treatments, promoting adoption of membranes and bone graft substitutes. Rising dental tourism and specialized outpatient procedures boost segment growth. Advanced graft materials with rapid healing properties improve patient throughput. Expansion of outpatient surgical infrastructure globally accelerates adoption. Integration of regenerative dentistry techniques in outpatient centers enhances clinical offerings. Increasing patient demand for shorter recovery times and minimally invasive solutions strengthens market penetration. Collaboration with hospitals and dental manufacturers improves material availability. Government support for outpatient dental care programs promotes usage. Emerging economies are increasingly investing in ambulatory surgical centers to improve dental access. Technological advancements in guided bone regeneration improve procedural success. Rising prevalence of implant procedures in outpatient settings further fuels adoption.

Dental Membrane and Bone Graft Substitute Market Regional Analysis

- North America dominated the dental membrane and bone graft substitute market with the largest revenue share of 38.7% in 2025

- Supported by advanced dental care infrastructure, high adoption of implantology procedures, strong presence of leading biomaterial manufacturers, and favorable reimbursement frameworks

- The region benefits from a well-established network of dental clinics, growing awareness of regenerative dental therapies, and high patient acceptance of minimally invasive oral procedures

U.S. Dental Membrane and Bone Graft Substitute Market Insight

The U.S. dental membrane and bone graft substitute market accounted for a substantial share of North America’s revenue in 2025, fueled by increasing use of guided bone regeneration techniques, rising implant procedures, and continuous investments in dental research and innovation. Companies such as Geistlich Pharma AG and OsteoBiol are actively expanding product portfolios and promoting clinical adoption, while supportive insurance coverage enhances patient access to advanced graft and membrane solutions.

Europe Dental Membrane and Bone Graft Substitute Market Insight

The Europe dental membrane and bone graft substitute market is projected to expand at a significant CAGR during the forecast period, driven by high patient awareness, increasing dental implant penetration, and regulatory frameworks promoting biomaterial use. Countries such as Germany, France, and Italy are witnessing growing application of collagen-based membranes and xenograft substitutes for oral regenerative procedures.

U.K. Dental Membrane and Bone Graft Substitute Market Insight

The U.K. dental membrane and bone graft substitute market is expected to grow at a notable CAGR, supported by rising dental tourism, increasing adoption of regenerative therapies, and enhanced focus on periodontal and implant care. Modernization of dental clinics and accessibility to advanced biomaterials further bolster market expansion.

Germany Dental Membrane and Bone Graft Substitute Market Insight

The Germany dental membrane and bone graft substitute market is anticipated to expand steadily during the forecast period, fueled by technologically advanced dental practices, strong patient demand for oral reconstruction procedures, and reimbursement policies supporting biomaterial utilization. Training programs in implantology and regenerative dentistry contribute to higher adoption rates.

Asia-Pacific Dental Membrane and Bone Graft Substitute Market Insight

The Asia-Pacific dental membrane and bone graft substitute market is expected to be the fastest-growing globally, expanding at a CAGR of 9.4% from 2026 to 2033. Growth is driven by rising investments in dental clinic modernization, increasing patient awareness of oral health, and the growing demand for regenerative dental therapies. Rapid urbanization, expanding hospital and dental networks, and rising disposable incomes in countries such as China, Japan, and India are key factors supporting market expansion.

Japan Dental Membrane and Bone Graft Substitute Market Insight

The Japan dental membrane and bone graft substitute market is gaining traction due to a high-tech healthcare ecosystem, increasing geriatric population, and rising demand for cosmetic and restorative dental procedures. The adoption of modern regenerative techniques and high-quality biomaterials is fueling market growth.

China Dental Membrane and Bone Graft Substitute Market Insight

China dental membrane and bone graft substitute market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by the country’s expanding middle class, rapid urbanization, and growing awareness of dental care and oral health. The increasing number of dental clinics, investment in advanced implantology procedures, and availability of cost-effective biomaterials are key factors propelling market expansion.

Dental Membrane and Bone Graft Substitute Market Share

The Dental Membrane and Bone Graft Substitute industry is primarily led by well-established companies, including:

- Geistlich Pharma (Switzerland)

- BioHorizons (U.S.)

- Straumann (Switzerland)

- Dentsply Sirona (U.S.)

- Zimmer Biomet (U.S.)

- Medtronic (U.S.)

- OsteoBiol (Italy)

- Botiss Biomaterials (Germany)

- Collagen Matrix (U.S.)

- Novabone Products (U.S.)

- Curasan (Germany)

- HERAeus Kulzer (Germany)

- Bio-Oss (Switzerland)

- Alpha-Bio Tec (Israel)

- Osstem Implant (South Korea)

- Keystone Dental (U.S.)

- MIS Implants Technologies (Israel)

- Etex Group (Belgium)

- Osteogenics Biomedical (U.S.)

- Zimmer Dental (U.S.)

Latest Developments in Global Dental Membrane and Bone Graft Substitute Market

- In April 2023, ZimVie Inc. expanded its dental biomaterials portfolio by announcing the launch of RegenerOss CC Allograft Particulate and RegenerOss Bone Graft Plug, two collagen‑based bone graft products designed to support bone defect repair and serve implant procedures in the North American dental market. These product additions aim to enhance handling characteristics and clinical outcomes in guided bone regeneration procedures

- In May 2023, Biomatlante achieved Medical Device Regulation (MDR) certification in Europe for its established regenerative product lines — Bio‑Gide, Fibro‑Gide, and Mucograft membranes — confirming their compliance with stringent European regulations and enabling continued use in periodontal and bone regeneration surgeries across EU markets

- In September 2024, Regenity Biosciences received regulatory approval from China’s National Medical Products Administration (NMPA) for its innovative crosslinked, bioresorbable collagen dental membrane, Matrixflex, designed for use in oral surgical procedures. This marked Regenity’s first dental product approval in the Chinese market, expanding access to advanced membrane solutions in a key growth region

- In January 2025, NovaBone Products announced a major strategic distribution partnership with BEGO, a global provider of implantology solutions. Under the agreement, NovaBone’s advanced Dental Putty with Cartridge Dispenser will be introduced to the European market, broadening clinical access to bioactive synthetic bone graft substitutes

- In February 2025, Geistlich Holding announced a strategic investment in ReOss Ltd., securing global marketing and distribution rights for ReOss’ core products and pipeline technologies including the Yxoss CBR scaffold. This strategic move strengthens Geistlich’s leadership position in dental regenerative materials, particularly in advanced bone graft substitute technologies

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.