Global Diabetes Clinical Nutrition Market

Market Size in USD Billion

CAGR :

%

USD

5.97 Billion

USD

10.37 Billion

2025

2033

USD

5.97 Billion

USD

10.37 Billion

2025

2033

| 2026 –2033 | |

| USD 5.97 Billion | |

| USD 10.37 Billion | |

| % | |

|

Diabetes Clinical Nutrition Market Size

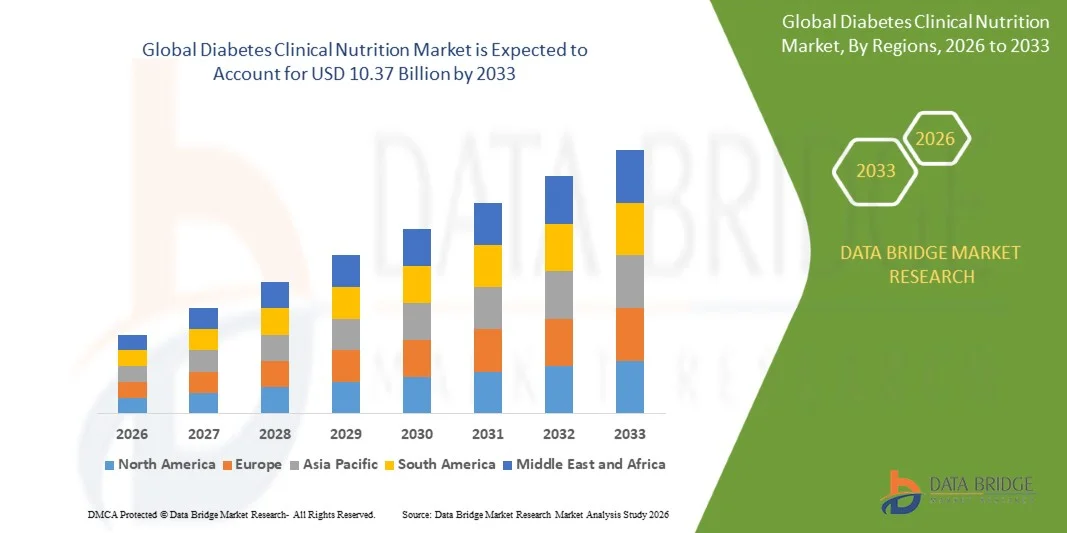

- The global Diabetes Clinical Nutrition market size was valued at USD 5.97 billion in 2025 and is expected to reach USD 10.37 billion by 2033, at a CAGR of 7.15% during the forecast period

- The market growth is largely fueled by the rising global prevalence of diabetes, increasing awareness regarding disease-specific nutritional management, and continuous advancements in specialized clinical nutrition products, leading to improved patient care across hospitals, clinics, and homecare settings

- Furthermore, growing demand for low-glycemic, high-protein, and balanced nutritional formulations, along with increasing focus on preventive healthcare and long-term blood glucose management, is establishing Diabetes Clinical Nutrition solutions as an essential component of modern diabetes care. These converging factors are accelerating the uptake of Diabetes Clinical Nutrition solutions, thereby significantly boosting the industry's growth

Diabetes Clinical Nutrition Market Analysis

- Diabetes Clinical Nutrition solutions, including diabetes-specific formulas, oral nutritional supplements, enteral nutrition products, and personalized dietary management solutions, are increasingly vital components of modern diabetes care across hospitals, clinics, long-term care centers, and homecare settings due to their role in supporting glycemic control and overall metabolic health

- The escalating demand for Diabetes Clinical Nutrition solutions is primarily fueled by the rising global prevalence of diabetes, growing awareness of nutrition-based disease management, increasing aging population, and rising preference for preventive healthcare and personalized nutritional support

- North America dominated the Diabetes Clinical Nutrition market with the largest revenue share of 41.5% in 2025, characterized by advanced healthcare infrastructure, high diabetes diagnosis rates, strong reimbursement support, and the presence of leading nutrition companies, with the U.S. experiencing substantial growth in home-based clinical nutrition adoption and hospital nutrition management programs

- Asia-Pacific is expected to be the fastest growing region in the Diabetes Clinical Nutrition market during the forecast period due to increasing urbanization, rising disposable incomes, growing diabetic population, expanding healthcare awareness, and improving access to specialized nutritional products across China, India, Japan, and Southeast Asia

- The Type 2 Diabetes segment held the largest market revenue share of 58.3% in 2025, driven by the high global prevalence of type 2 diabetes linked to obesity, sedentary lifestyles, and aging populations

Report Scope and Diabetes Clinical Nutrition Market Segmentation

|

Attributes |

Diabetes Clinical Nutrition Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Diabetes Clinical Nutrition Market Trends

“Enhanced Disease Management Through Personalized Nutrition and Digital Health Integration”

- A significant and accelerating trend in the global diabetes clinical nutrition market is the increasing adoption of personalized nutrition programs, continuous glucose monitoring (CGM)-linked dietary tools, and digital health platforms to improve glycemic control and long-term metabolic outcomes. These innovations are enhancing patient engagement and treatment effectiveness

- AI-powered nutrition platforms are increasingly being used to generate individualized meal plans based on glucose patterns, lifestyle habits, and medication schedules

- For instance, companies such as Abbott and Dexcom ecosystem partners are integrating CGM data with digital coaching applications to recommend food choices that help stabilize blood glucose levels

- The growing demand for diabetes-specific oral nutritional supplements and low-glycemic functional foods is also reshaping the market by providing convenient dietary support for patients with type 1, type 2, and gestational diabetes

- Another major trend is the expansion of tele-nutrition and remote dietitian consultation services, enabling patients to receive expert nutritional guidance without frequent clinic visits

- In addition, manufacturers are increasingly developing high-protein, fiber-enriched, and sugar-controlled formulas tailored for diabetic patients in hospitals, long-term care settings, and homecare environments

- This shift toward personalized, preventive, and digitally supported nutritional care is fundamentally transforming diabetes management and driving demand for evidence-based clinical nutrition solutions

Diabetes Clinical Nutrition Market Dynamics

Driver

“Rising Global Diabetes Prevalence and Growing Focus on Preventive Nutrition”

- The increasing global prevalence of diabetes, obesity, and prediabetes is a major driver for the Diabetes Clinical Nutrition market, as nutritional intervention remains a core component of blood glucose management and complication prevention

- Growing awareness regarding the role of diet in glycemic control is further accelerating market growth

- For instance, countries such as the U.S., India, China, and Saudi Arabia are expanding diabetes education programs that emphasize medical nutrition therapy and healthy dietary habits

- Rising healthcare expenditure and stronger physician recommendations for nutrition-based disease management are also supporting adoption of specialized diabetic formulas and supplements

- Furthermore, increasing hospitalization rates related to diabetes complications are driving demand for clinically formulated enteral and oral nutrition products in healthcare facilities

- The expansion of retail pharmacy, e-commerce, and direct-to-consumer channels is also improving access to diabetes nutrition products globally

Restraint/Challenge

“High Product Costs, Taste Preferences, and Limited Patient Adherence”

- One of the major challenges restraining the Diabetes Clinical Nutrition market is the relatively high cost of specialized diabetic nutrition formulas and premium low-glycemic products compared with conventional food alternatives

- Taste preferences and difficulty maintaining long-term dietary discipline can reduce patient adherence to prescribed nutrition plans

- For instance, some patients discontinue use of diabetes-specific meal replacement shakes or sugar-controlled supplements due to flavor fatigue or preference for regular foods

- Limited awareness in low-income and rural populations regarding the benefits of medical nutrition therapy also restricts broader market penetration

- In addition, reimbursement limitations for nutrition products in many healthcare systems may discourage sustained usage, especially for chronic patients requiring long-term support.

- Overcoming these barriers through affordable product innovation, better flavor profiles, stronger patient education, and expanded reimbursement support will be essential for sustained market growth

Diabetes Clinical Nutrition Market Scope

The market is segmented on the basis of product type, application, distribution channel, and end-user.

• By Product Type

On the basis of product type, the Diabetes Clinical Nutrition market is segmented into Oral Nutritional Supplements, Enteral Nutrition, Parenteral Nutrition, and Diabetes-Specific Formulas. The Diabetes-Specific Formulas segment dominated the largest market revenue share of 44.6% in 2025, driven by increasing preference for nutrition products specifically designed to manage glycemic response and improve metabolic control. These formulas contain slow-digesting carbohydrates, fiber blends, and balanced protein content that help stabilize blood sugar levels. Healthcare professionals increasingly recommend diabetes-specific formulas for hospitalized patients and outpatient nutritional support. Rising prevalence of diabetes globally has significantly increased demand for targeted nutritional interventions. Pharmaceutical and nutrition companies are expanding specialized product portfolios with clinically tested formulations. Growing consumer awareness regarding disease-specific dietary management is also contributing to segment growth. North America leads adoption due to advanced healthcare systems and strong reimbursement support. Europe follows with increasing use in elderly diabetic populations. Asia-Pacific is witnessing rapid uptake due to growing diabetic population. Continuous innovation in flavor, convenience packaging, and nutrient composition further strengthens demand. Overall, diabetes-specific formulas remain the leading product category in the market.

The Oral Nutritional Supplements segment is expected to witness the fastest CAGR of 22.1% from 2026 to 2033, fueled by growing consumer preference for convenient, ready-to-consume nutritional products. These supplements are widely used in outpatient care, elderly nutrition, and early diabetes management programs. Rising awareness regarding preventive healthcare and daily nutritional support is accelerating adoption. Patients prefer oral supplements due to ease of use compared to tube feeding or parenteral methods. Expanding e-commerce availability is improving accessibility across emerging markets. Manufacturers are introducing sugar-controlled, protein-rich, and plant-based formulations to attract broader consumers. Growing physician recommendations for nutritional supplementation in diabetic patients are also boosting demand. Asia-Pacific is emerging as a major growth hub due to rising incomes and healthcare awareness. Product innovation in sachets, powders, and ready-to-drink formats supports convenience-led growth. Increasing use in prediabetes management programs is another key factor. Strong marketing by global nutrition brands is enhancing market penetration. Overall, oral nutritional supplements are projected to be the fastest-growing product segment.

• By Application

On the basis of application, the Diabetes Clinical Nutrition market is segmented into Type 1 Diabetes, Type 2 Diabetes, Gestational Diabetes, and Prediabetes Management. The Type 2 Diabetes segment held the largest market revenue share of 58.3% in 2025, driven by the high global prevalence of type 2 diabetes linked to obesity, sedentary lifestyles, and aging populations. Clinical nutrition plays a critical role in blood glucose management, weight control, and reducing long-term complications in these patients. Healthcare providers strongly recommend tailored nutritional therapy alongside medication. Rising hospitalization rates among type 2 diabetic patients further support demand for enteral and oral nutritional products. Governments are promoting diabetes prevention and management programs, increasing awareness of medical nutrition therapy. North America dominates due to large diagnosed population and advanced care pathways. Europe is steadily expanding demand through preventive healthcare initiatives. Asia-Pacific contributes strongly because of growing urbanization and lifestyle-related diabetes incidence. Increasing use of diabetes-specific meal replacements also supports revenue growth. Product personalization based on patient needs is becoming common. Overall, type 2 diabetes remains the largest application segment.

The Prediabetes Management segment is expected to witness the fastest CAGR of 23.4% from 2026 to 2033, driven by rising awareness of early intervention to prevent progression to full diabetes. Increasing screening programs are identifying more prediabetic individuals globally. Consumers are actively seeking nutritional products for weight management and blood sugar stabilization. Healthcare systems are emphasizing preventive nutrition to reduce future treatment costs. Oral supplements and low-glycemic nutrition formulas are gaining strong traction in this category. Digital health coaching and wellness programs are encouraging nutritional compliance. Younger populations are increasingly adopting preventive lifestyle strategies. Asia-Pacific is expected to witness rapid growth due to urbanization and rising obesity rates. Retail and online pharmacy availability is improving product access. Growing corporate wellness initiatives also support demand. Product innovation focused on wellness consumers is accelerating adoption. Overall, prediabetes management is projected to be the fastest-growing application segment.

• By Distribution Channel

On the basis of distribution channel, the Diabetes Clinical Nutrition market is segmented into Hospital Pharmacy, Retail Pharmacy, Online Pharmacy, and Specialty Stores. The Hospital Pharmacy segment accounted for the largest market revenue share of 39.8% in 2025, driven by high demand for clinical nutrition products in inpatient diabetes management and critical care settings. Hospitals remain the primary channel for enteral and parenteral nutrition prescriptions. Physicians and dietitians frequently recommend diabetes-specific formulas during treatment and recovery periods. Increasing diabetic admissions and surgery-related nutrition support further strengthen demand. Strong institutional procurement systems ensure consistent product supply. North America leads this segment due to advanced hospital infrastructure. Europe follows with strong public healthcare systems. Asia-Pacific hospitals are expanding nutritional therapy services rapidly. Clinical supervision and trust in hospital dispensing channels remain key advantages. Rising adoption of integrated nutrition protocols also supports growth. Overall, hospital pharmacies remain the dominant distribution channel.

The Online Pharmacy segment is expected to witness the fastest CAGR of 24.2% from 2026 to 2033, fueled by increasing digital healthcare adoption and consumer preference for doorstep delivery. Patients increasingly purchase repeat-use nutritional products online for convenience and price discounts. Expanding internet penetration and smartphone use are accelerating e-pharmacy adoption globally. Subscription-based nutrition supply models are gaining popularity among chronic care patients. Manufacturers are partnering with digital platforms to improve direct-to-consumer sales. Asia-Pacific is emerging as a strong growth region due to rapid digitalization. Consumers benefit from broader product variety and easier comparison tools. Rising trust in licensed online healthcare platforms supports expansion. Promotional offers and home delivery convenience further boost sales. Increasing telehealth consultations also drive online prescriptions. Strong urban demand and recurring purchases strengthen this segment. Overall, online pharmacy is projected to be the fastest-growing channel.

• By End-User

On the basis of end-user, the Diabetes Clinical Nutrition market is segmented into Hospitals, Homecare Settings, Long-Term Care Facilities, and Clinics. The Hospitals segment dominated the largest market revenue share of 42.5% in 2025, driven by strong use of nutritional therapy in acute diabetic care, surgery recovery, and complication management. Hospitals manage large volumes of patients requiring monitored nutritional interventions. Enteral and parenteral nutrition products are widely utilized for critical patients unable to consume regular meals. Clinical dietitians play a major role in recommending specialized formulas. Rising diabetic complications such as kidney disease and wound healing issues support hospital demand. North America leads due to strong inpatient care infrastructure. Europe maintains high usage through structured public hospitals. Asia-Pacific hospitals are rapidly increasing nutrition support programs. Availability of multidisciplinary care teams strengthens adoption. Strong reimbursement for inpatient treatment also contributes to growth. Overall, hospitals remain the leading end-user segment.

The Homecare Settings segment is expected to witness the fastest CAGR of 22.8% from 2026 to 2033, driven by growing preference for cost-effective chronic disease management at home. Patients increasingly seek convenient nutritional support outside hospital environments. Oral supplements and home enteral nutrition are gaining popularity among elderly diabetic populations. Rising telehealth adoption enables professional monitoring of nutrition plans remotely. Healthcare systems encourage homecare to reduce hospitalization costs. Families prefer home-based management for long-term diabetic patients. Manufacturers are launching easy-to-use packaging and ready-to-drink products for home users. North America and Europe are leading adoption due to established homecare infrastructure. Asia-Pacific is witnessing rapid growth as healthcare access improves. Increasing caregiver awareness also supports demand. Better insurance support for homecare products is another key factor. Overall, homecare settings are projected to be the fastest-growing end-user segment.

Diabetes Clinical Nutrition Market Regional Analysis

- North America dominated the Diabetes Clinical Nutrition market with the largest revenue share of 41.5% in 2025, supported by advanced healthcare infrastructure, high diabetes diagnosis rates, favorable reimbursement frameworks, and the strong presence of leading clinical nutrition manufacturers. The region has also witnessed rising adoption of personalized nutrition solutions, home-based enteral nutrition support, and hospital-led diabetes management programs

- Consumers and healthcare providers in the region highly value evidence-based nutritional formulations designed for blood glucose management, weight control, and complication prevention. Increasing awareness regarding preventive healthcare and medically tailored nutrition plans continues to strengthen product demand

- This widespread adoption is further supported by high healthcare spending, strong physician recommendation rates, growing elderly populations, and increasing prevalence of Type 1 and Type 2 diabetes, establishing diabetes clinical nutrition products as an essential component of long-term disease management across hospitals, clinics, and homecare settings

U.S. Diabetes Clinical Nutrition Market Insight

The U.S. diabetes clinical nutrition market captured the largest revenue share in 2025 within North America, fueled by a high diabetic patient population, strong clinical awareness, and rapid adoption of specialized nutrition products in both acute care and homecare settings. Consumers are increasingly prioritizing medically supervised nutrition to support glycemic control and reduce diabetes-related complications. The growing preference for home-based nutritional therapy, combined with robust demand for ready-to-drink formulas, oral nutritional supplements, and digital health monitoring integration, further propels the market. Moreover, the expansion of hospital nutrition management programs and outpatient diabetes care services is significantly contributing to market growth.

Europe Diabetes Clinical Nutrition Market Insight

The Europe diabetes clinical nutrition market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising diabetes prevalence, aging demographics, and increasing focus on preventive healthcare. Strong healthcare systems and favorable regulatory standards are fostering the adoption of clinically validated nutrition products. European consumers are also drawn to products offering sugar control, balanced energy release, and cardiovascular health support. The region is experiencing notable growth across hospitals, elderly care centers, and home nutrition applications, with diabetes-focused nutrition increasingly incorporated into chronic disease management plans.

U.K. Diabetes Clinical Nutrition Market Insight

The U.K. diabetes clinical nutrition market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of diabetes prevention and the growing need for nutritional interventions in obesity and blood sugar management. In addition, expanding NHS support programs and rising consumer preference for convenient nutritional supplements are encouraging adoption. The country’s strong pharmacy, retail, and e-commerce networks are expected to further stimulate market growth.

Germany Diabetes Clinical Nutrition Market Insight

The Germany diabetes clinical nutrition market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of metabolic health, strong healthcare expenditure, and demand for scientifically formulated nutritional products. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and quality standards, promotes the adoption of diabetes clinical nutrition solutions in hospitals and outpatient care. Demand for clean-label, high-protein, and low-glycemic formulations is also increasing, aligning with local consumer preferences.

Asia-Pacific Diabetes Clinical Nutrition Market Insight

The Asia-Pacific diabetes clinical nutrition market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by increasing urbanization, rising disposable incomes, growing diabetic population, expanding healthcare awareness, and improving access to specialized nutritional products across China, India, Japan, and Southeast Asia. The region’s rising middle-class population and improving healthcare infrastructure are accelerating demand for preventive and therapeutic nutrition. Furthermore, local manufacturing capabilities and expanding pharmacy distribution networks are making diabetes nutrition products more affordable and accessible to a wider consumer base.

Japan Diabetes Clinical Nutrition Market Insight

The Japan diabetes clinical nutrition market is gaining momentum due to the country’s aging population, strong health consciousness, and demand for premium nutritional care solutions. The Japanese market places significant emphasis on preventive care, and adoption is driven by increasing need for blood sugar management among elderly consumers. Integration of clinical nutrition into hospital recovery programs and homecare settings is fueling growth. Moreover, demand for easy-to-consume liquid and functional nutrition products is expected to rise steadily.

China Diabetes Clinical Nutrition Market Insight

The China diabetes clinical nutrition market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding middle class, rapid urbanization, large diabetic population, and increasing health awareness. China stands as one of the largest markets for medical nutrition products, and diabetes-focused nutritional supplements are becoming increasingly popular across hospitals, pharmacies, and online retail channels. Government healthcare modernization initiatives, improving diagnosis rates, and the availability of affordable domestic products are key factors propelling market growth in China.

Diabetes Clinical Nutrition Market Share

The Diabetes Clinical Nutrition industry is primarily led by well-established companies, including:

- Abbott (U.S.)

- Nestlé Health Science (Switzerland)

- Danone S.A. (France)

- Fresenius Kabi AG (Germany)

- B. Braun SE (Germany)

- Mead Johnson Nutrition (U.S.)

- Baxter International Inc. (U.S.)

- Perrigo Company plc (Ireland)

- Glanbia plc (Ireland)

- Herbalife Ltd. (U.S.)

- Medtrition Inc. (U.S.)

- Kate Farms, Inc. (U.S.)

- Ajinomoto Co., Inc. (Japan)

- Otsuka Holdings Co., Ltd. (Japan)

- Reckitt Benckiser Group plc (U.K.)

- Arla Foods amba (Denmark)

- Hormel Health Labs (U.S.)

- DSM-Firmenich AG (Switzerland)

- Victus, Inc. (U.S.)

- Nutricia (Netherlands)

Latest Developments in Global Diabetes Clinical Nutrition Market

- In December 2021, Danone India introduced Protinex Diabetes Care, a specialized nutrition product formulated for individuals with diabetes. The product was developed with high protein and fiber content to support blood sugar management and meet daily nutritional requirements, reflecting rising demand for diabetes-specific clinical nutrition solutions in emerging markets

- In December 2021, Nestlé Health Science launched its first prediabetes program in Malaysia, featuring a novel food supplement designed to be sprinkled over meals to help maintain normal post-meal blood glucose levels. This initiative marked Nestlé’s expansion into early-stage metabolic health nutrition and preventive diabetes care

- In April 2022, Abbott reported continued growth of its Glucerna diabetes nutrition brand, with first-quarter global sales increasing on both reported and organic bases. The performance highlighted strong consumer and clinical demand for diabetes-focused oral nutritional supplements across international markets

- In August 2022, Lyons Magnus announced a voluntary recall of certain ready-to-drink Glucerna shakes manufactured for Abbott Nutrition due to potential microbial contamination risks. The action underscored the importance of supply chain quality assurance and product safety in the diabetes clinical nutrition market

- In June 2023, market analysts reported accelerating growth in the global diabetes clinical nutrition sector, driven by rising diabetes prevalence, increased physician adoption of disease-specific oral nutrition formulas, and expanding product availability through hospital and retail channels. Major participants identified included Abbott Nutrition, Nestlé Health Science, Danone Nutricia, and Otsuka Holdings

- In August 2024, Abbott highlighted new clinical findings showing that its Glucerna Protein Smart Shake stimulated GLP-1 release and reduced blood glucose response compared with a common breakfast option. The study reinforced growing interest in evidence-backed functional nutrition products for blood glucose management and weight control in people with diabetes

- In November 2025, Abbott announced the launch of a new and advanced formulation of Ensure Diabetes Care in India. The clinically proven formula featured higher myo-inositol content, a low glycemic index carbohydrate blend, high protein, and fiber to support blood glucose control, cholesterol reduction, and weight management. The launch demonstrated ongoing innovation in diabetes-focused medical nutrition products

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Diabetes Clinical Nutrition Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Diabetes Clinical Nutrition Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Diabetes Clinical Nutrition Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.