Global Diabetic Lancing Device Market

Market Size in USD Billion

CAGR :

%

USD

1.02 Billion

USD

2.23 Billion

2025

2033

USD

1.02 Billion

USD

2.23 Billion

2025

2033

| 2026 –2033 | |

| USD 1.02 Billion | |

| USD 2.23 Billion | |

| % | |

|

Diabetic Lancing Device Market Size

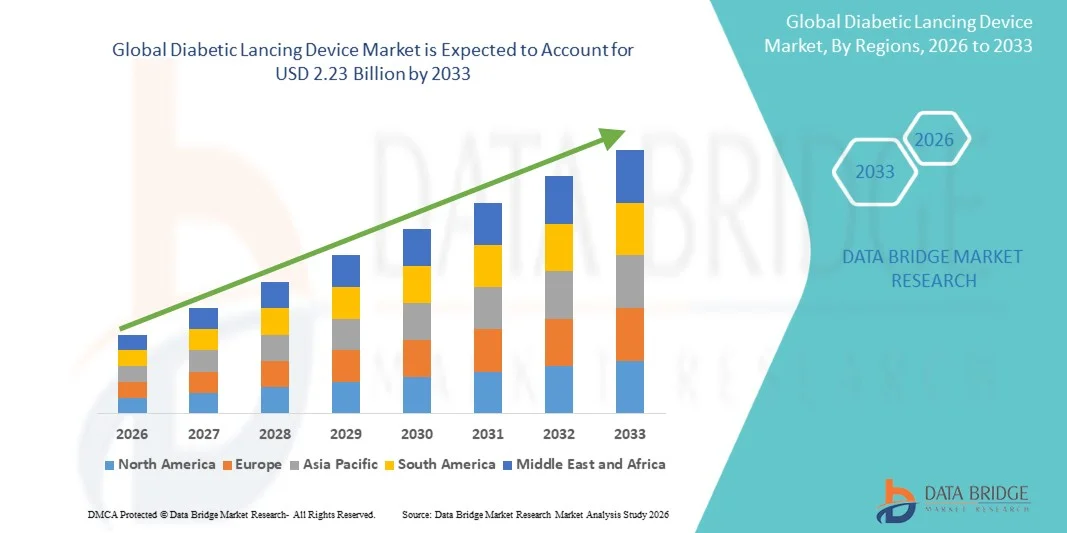

- The global diabetic lancing device market size was valued at USD 1.02 billion in 2025 and is expected to reach USD 2.23 billion by 2033, at a CAGR of 10.28% during the forecast period

- The market growth is largely fueled by the rising prevalence of diabetes worldwide, increasing frequency of blood glucose monitoring, and continuous technological advancements in diabetic lancing devices, leading to improved accuracy, reduced pain, and greater patient compliance in both homecare and clinical settings

- Furthermore, growing patient demand for safe, minimally painful, and easy-to-use blood sampling solutions, along with increasing adoption of self-monitoring of blood glucose (SMBG) and home-based diabetes management, is establishing advanced diabetic lancing devices as essential components of routine diabetes care. These converging factors are accelerating the uptake of diabetic lancing device solutions, thereby significantly boosting the industry’s growth

Diabetic Lancing Device Market Analysis

- Diabetic lancing devices, used for obtaining capillary blood samples for glucose monitoring, are essential components of diabetes management in both homecare and clinical settings due to their role in enabling frequent testing, improved patient compliance, and minimally painful blood sampling

- The escalating demand for diabetic lancing devices is primarily driven by the rising global prevalence of diabetes, increasing adoption of self-monitoring of blood glucose (SMBG), growing awareness about early disease management, and continuous product innovations focused on safety, comfort, and ease of use

- North America dominated the diabetic lancing device market with the largest revenue share of approximately 38.6% in 2025, supported by a high diabetes prevalence, strong reimbursement frameworks, widespread use of advanced glucose monitoring systems, and a well-established homecare ecosystem. The U.S. accounts for the majority of regional demand, driven by early adoption of safety lancets and growing preference for painless and reusable lancing solutions

- Asia-Pacific is expected to be the fastest growing region in the diabetic lancing device market during the forecast period, registering a CAGR of around 9.8%, driven by a rapidly expanding diabetic population, improving healthcare access, rising awareness of regular glucose monitoring, and increasing penetration of affordable lancing devices across emerging economies

- The safety lancets segment dominated the market in 2025, accounting for approximately 61.8% of total revenue, driven by growing emphasis on patient safety, infection control, and single-use medical devices

Report Scope and Diabetic Lancing Device Market Segmentation

|

Attributes |

Diabetic Lancing Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Diabetic Lancing Device Market Trends

“Advancements in Pain-Reduced and User-Friendly Lancing Technologies”

- A significant and accelerating trend in the global diabetic lancing device market is the growing emphasis on pain-reduction technologies and enhanced user comfort, driven by the need for frequent blood glucose monitoring among diabetic patients

- For instance, in 2023, Roche Diabetes Care introduced enhancements to its Accu-Chek lancing systems, focusing on ultra-thin needles and adjustable depth settings to minimize pain and skin trauma during routine glucose testing

- Manufacturers are increasingly incorporating ergonomic designs that improve grip, control, and ease of use, especially for elderly and pediatric patients

- The development of lancing devices with multiple depth settings allows users to personalize penetration based on skin thickness and sensitivity

- Single-use and disposable lancet systems are gaining traction due to improved hygiene and reduced infection risk

- There is a rising preference for devices that reduce visible blood sampling discomfort, improving long-term patient compliance

- Compact and portable lancing devices are being developed to support on-the-go glucose monitoring

- Innovation in spring-loaded mechanisms ensures consistent puncture force, reducing variability in blood sampling

- Manufacturers are focusing on quiet and vibration-free operation to enhance user experience

- The integration of lancing devices with broader glucose monitoring kits supports ease of daily diabetes management

- Increasing patient awareness regarding painless monitoring solutions is accelerating adoption globally

- This trend reflects a broader shift toward patient-centric diabetes care and improved quality of life

Diabetic Lancing Device Market Dynamics

Driver

“Rising Global Diabetes Prevalence and Increased Self-Monitoring Adoption”

- The rapidly increasing prevalence of diabetes worldwide is a major driver for the Diabetic Lancing Device market, as regular blood glucose monitoring remains a cornerstone of diabetes management

- For instance, in 2022, the International Diabetes Federation (IDF) reported a substantial rise in global diabetes cases, prompting healthcare providers to emphasize frequent self-monitoring, thereby increasing demand for lancing devices

- Growing awareness about early diagnosis and glycemic control is encouraging routine blood glucose testing among patients

- The expanding elderly population, which has a higher incidence of diabetes, further contributes to sustained demand

- Increasing adoption of home-based diabetes care solutions is driving the use of personal lancing devices

- Healthcare professionals strongly recommend self-monitoring for insulin-dependent and Type 2 diabetic patients

- Improved access to diabetes care products through retail pharmacies and online platforms supports market growth

- Government initiatives promoting diabetes screening and management programs are expanding device utilization

- The rising burden of diabetes-related complications is increasing the need for strict glucose monitoring routines. Advancements in glucose meters indirectly boost lancing device demand as complementary products

- Emerging markets are witnessing improved healthcare infrastructure, supporting wider adoption of lancing devices. Overall, the necessity for continuous glucose monitoring sustains long-term market expansion

Restraint/Challenge

“Pain Perception, Reusability Concerns, and Cost Sensitivity”

- Despite technological improvements, fear of pain and discomfort associated with finger-pricking remains a key challenge limiting frequent usage of diabetic lancing devices

- For instance, patient surveys published in 2021 highlighted that a significant proportion of diabetic patients avoid recommended testing frequency due to discomfort and needle anxiety, impacting consistent device usage

- Improper reuse of lancets due to cost concerns increases the risk of infection and skin damage. Price sensitivity in low- and middle-income regions limits access to high-quality lancing devices

- Lack of patient education regarding correct lancing techniques affects user experience and compliance

- Some patients prefer non-invasive glucose monitoring alternatives, which may reduce reliance on traditional lancing devices. Environmental concerns related to disposable lancet waste present sustainability challenges

- Variability in reimbursement policies across regions impacts affordability and adoption rates. Low awareness in rural areas regarding diabetes self-management tools restricts market penetration. Manual dexterity issues among elderly patients can hinder proper device usage

- Manufacturers face pressure to balance affordability with innovation and safety feature

- Addressing these challenges through patient education, cost-effective designs, and improved comfort will be critical for sustained market growth

Diabetic Lancing Device Market Scope

The market is segmented on the basis of type, gauge, penetration depth, and application.

- By Type

On the basis of type, the Global Diabetic Lancing Device market is segmented into safety lancets and standard lancets. The safety lancets segment dominated the market in 2025, accounting for approximately 61.8% of total revenue, driven by growing emphasis on patient safety, infection control, and single-use medical devices. Safety lancets are designed with retractable or shielded needles, significantly reducing the risk of accidental needle-stick injuries and cross-contamination. Their widespread adoption in hospitals, diagnostic centers, and homecare settings is supported by stringent regulatory guidelines and infection prevention protocols. Rising diabetes prevalence and increased frequency of blood glucose monitoring further contribute to the strong demand for safety lancets. In addition, the growing geriatric population and preference for painless, easy-to-use devices reinforce their dominance. Manufacturers are also focusing on ergonomic designs and ultra-thin needles to enhance patient comfort. The availability of safety lancets through institutional procurement channels strengthens their penetration. As a result, safety lancets remain the preferred choice across clinical and home-based testing environments.

The standard lancets segment is expected to witness the fastest growth, registering a CAGR of 8.6% from 2026 to 2033. This growth is driven by their lower cost, widespread availability, and compatibility with reusable lancing devices. Standard lancets are highly favored in cost-sensitive markets and among long-term diabetic patients who perform frequent self-monitoring. Emerging economies, where affordability plays a critical role, are witnessing increased adoption of standard lancets. The rising trend of home-based diabetes management further supports this segment’s growth. Improvements in needle sharpness and coating technologies are also enhancing user comfort. Online retail channels and bulk purchasing options contribute to market expansion. Consequently, standard lancets are expected to grow rapidly during the forecast period.

- By Gauge

On the basis of gauge, the market is segmented into 17/18g, 21g, 23g, 25g, 28g, 30g, and others. The 28g gauge segment dominated the market in 2025, holding approximately 29.4% of the total revenue share. This dominance is attributed to the optimal balance it offers between adequate blood flow and reduced pain during finger-prick testing. The 28g lancets are widely used across hospitals, diagnostic centers, and homecare settings due to their versatility and patient comfort. They are suitable for routine blood glucose monitoring and are compatible with most lancing devices. Increased awareness regarding painless sampling and patient-centric care has further boosted adoption. The rising diabetic population requiring frequent monitoring reinforces sustained demand. Manufacturers continue to standardize 28g lancets across product portfolios. This broad acceptance ensures their continued market leadership.

The 30g gauge segment is projected to grow at the fastest CAGR of 9.2% from 2026 to 2033. Ultra-thin 30g lancets are gaining popularity due to minimal pain perception and reduced skin trauma. They are particularly preferred by pediatric patients, elderly individuals, and users with sensitive skin. Advancements in needle manufacturing technologies have improved blood yield despite thinner gauges. The shift toward painless and patient-friendly testing solutions is accelerating adoption. Increased use in home diagnostics and continuous glucose monitoring support devices further drives growth. As comfort becomes a key purchasing factor, demand for 30g lancets is expected to rise significantly.

- By Penetration Depth

On the basis of penetration depth, the market is segmented into 0.8 mm to 1.0 mm, 1.0 mm to 1.5 mm, 1.6 mm to 2.0 mm, 2.1 mm to 2.5 mm, and 2.6 mm to 3.0 mm. The 1.0 mm to 1.5 mm penetration depth segment dominated the market in 2025, accounting for approximately 34.7% of revenue. This range provides sufficient blood volume while minimizing discomfort, making it suitable for most adult users. It is widely adopted in both clinical and homecare settings for routine glucose testing. Compatibility with adjustable lancing devices enhances its usability across patient groups. The segment benefits from standardized device settings recommended by healthcare professionals. Growing patient awareness about proper sampling techniques supports demand. Its balance of safety, comfort, and efficiency drives continued dominance.

The 0.8 mm to 1.0 mm penetration depth segment is expected to register the fastest CAGR of 9.0% from 2026 to 2033. This growth is fueled by increasing demand for minimally invasive blood sampling solutions. Shallow penetration depths are particularly preferred for frequent daily testing and among pediatric and elderly patients. Technological advancements enabling reliable blood collection at lower depths are accelerating adoption. The growing emphasis on pain reduction and skin protection supports this trend. Rising home-based testing further boosts growth. As user comfort becomes a priority, this segment is expected to expand rapidly.

- By Application

On the basis of application, the market is segmented into hospitals & clinics, home care & home diagnostics, diagnostic centers & medical institutions, research & academic laboratories, and others. The hospitals & clinics segment dominated the market in 2025, capturing approximately 38.9% of total revenue. This dominance is driven by high patient inflow, routine glucose monitoring, and strict adherence to safety protocols. Hospitals prefer single-use and safety lancets to minimize infection risks. The presence of trained healthcare professionals ensures standardized testing procedures. Increasing hospitalization rates for diabetes-related complications further support demand. Institutional procurement and bulk purchasing strengthen market penetration. As a result, hospitals and clinics remain the primary end users.

The home care & home diagnostics segment is expected to witness the fastest growth, registering a CAGR of 10.4% from 2026 to 2033. Rising awareness of self-monitoring of blood glucose and the growing diabetic population are key growth drivers. The shift toward remote patient monitoring and personalized healthcare accelerates adoption. User-friendly lancing devices and lancets designed for home use support expansion. Increasing availability through online and retail pharmacies further boosts growth. Aging populations and lifestyle-related diabetes prevalence contribute significantly. This segment is expected to emerge as a major growth engine over the forecast period.

Diabetic Lancing Device Market Regional Analysis

- North America dominated the diabetic lancing device market with the largest revenue share of approximately 38.6% in 2025, supported by a high prevalence of diabetes, strong reimbursement frameworks, widespread adoption of advanced glucose monitoring systems, and a well-established homecare ecosystem

- The region benefits from early adoption of safety lancets, growing preference for painless and reusable lancing devices, and strong patient awareness regarding regular blood glucose monitoring

- The presence of leading medical device manufacturers, favorable insurance coverage, and continuous innovation in minimally invasive lancing technologies further reinforce North America’s leading position across both clinical and homecare settings

U.S. Diabetic Lancing Device Market Insight

The U.S. diabetic lancing device market accounted for the majority share within North America in 2025, driven by a large diabetic population, high healthcare expenditure, and strong penetration of self-monitoring blood glucose (SMBG) devices. The growing shift toward home-based diabetes management, along with rising demand for safety-engineered and low-pain lancing solutions, is supporting sustained market growth. Additionally, widespread physician recommendation of regular glucose testing and favorable reimbursement policies continue to drive product adoption across hospitals, clinics, and homecare environments.

Europe Diabetic Lancing Device Market Insight

The Europe diabetic lancing device market is expected to expand at a steady CAGR during the forecast period, supported by increasing diabetes prevalence, rising geriatric population, and strong emphasis on preventive healthcare. Government-backed diabetes management programs, coupled with high adoption of safety lancets in clinical settings, are contributing to market growth. The region also benefits from strict medical device safety regulations, which encourage the use of single-use and safety-enabled lancing devices.

U.K. Diabetic Lancing Device Market Insight

The U.K. diabetic lancing device market is projected to grow at a notable CAGR, driven by increasing awareness of diabetes management, strong support from the National Health Service (NHS), and widespread availability of glucose monitoring supplies. The growing focus on home-based testing and patient-friendly lancing devices is further supporting demand across both adult and pediatric populations.

Germany Diabetic Lancing Device Market Insight

The Germany diabetic lancing device market is anticipated to witness consistent growth over the forecast period, supported by a well-developed healthcare infrastructure, high diagnostic standards, and strong adoption of technologically advanced medical devices. The demand for precision, safety, and reusable lancing systems is increasing across hospitals and outpatient care settings, aligning with Germany’s emphasis on quality healthcare delivery.

Asia-Pacific Diabetic Lancing Device Market Insight

The Asia-Pacific diabetic lancing device market is expected to be the fastest growing region during the forecast period, registering a CAGR of around 9.8%, driven by a rapidly expanding diabetic population, improving healthcare access, and rising awareness of routine blood glucose monitoring. Government initiatives aimed at strengthening diabetes care, along with increasing affordability of lancing devices, are accelerating market penetration across emerging economies.

Japan Diabetic Lancing Device Market Insight

The Japan diabetic lancing device market is witnessing steady growth due to the country’s aging population, high incidence of lifestyle-related disorders, and strong focus on regular health monitoring. Demand is particularly strong for low-pain, easy-to-use lancing devices suitable for elderly patients, supporting adoption across both homecare and clinical settings.

China Diabetic Lancing Device Market Insight

The China diabetic lancing device market held the largest revenue share within Asia-Pacific in 2025, driven by a rapidly growing diabetic population, expanding healthcare infrastructure, and rising awareness of early diagnosis and disease management. Increasing availability of cost-effective lancing devices and expanding access to primary healthcare facilities are key factors supporting market growth across urban and rural regions.

Diabetic Lancing Device Market Share

The Diabetic Lancing Device industry is primarily led by well-established companies, including:

- Roche Diabetes Care (Switzerland)

- Abbott (U.S.)

- BD (U.S.)

- Ascensia Diabetes Care (Switzerland)

- LifeScan (U.S.)

- Terumo Corporation (Japan)

- ARKRAY, Inc. (Japan)

- Ypsomed Holding AG (Switzerland)

- Owen Mumford Ltd. (U.K.)

- HTL-STREFA S.A. (Poland)

- Trividia Health, Inc. (U.S.)

- Nipro Corporation (Japan)

- Cardinal Health (U.S.)

- Impro Medical Devices Co., Ltd. (China)

- HMD Biomedical Inc. (Taiwan)

- Taidoc Technology Corporation (Taiwan)

- Beurer GmbH (Germany)

- i-SENS, Inc. (South Korea)

- Yuwell Medical (China)

- Omron Healthcare (Japan)

Latest Developments in Global Diabetic Lancing Device Market

- In March 2021, Roche Diabetes Care announced upgrades to its Accu-Chek lancing device portfolio, focusing on enhanced safety lancets with reduced penetration force and improved depth control. This development aimed to reduce pain during frequent blood glucose testing and improve user comfort, particularly for long-term diabetes patients who require multiple daily finger pricks

- In September 2022, Abbott expanded its diabetes care ecosystem by introducing next-generation disposable safety lancets compatible with its blood glucose monitoring systems. The company emphasized improved sterility, single-use safety mechanisms, and reduced risk of needle-stick injuries, supporting broader adoption in hospitals, clinics, and home-care environments

- In August 2023, F. Hoffmann-La Roche AG launched the Accu-Chek Pico disposable lancing device in Japan, designed specifically for elderly and first-time diabetes patients. The product features a simplified one-step activation mechanism and consistent shallow penetration, improving ease of use and adherence to routine glucose monitoring among aging populations

- In November 2023, several global manufacturers, including B. Braun and Terumo, introduced antimicrobial-coated lancets and ultra-thin gauge safety lancets across Asian and European markets. These innovations focused on minimizing infection risk and improving patient safety, particularly in high-volume clinical and diagnostic center settings

- In July 2024, Nipro Corporation announced the establishment of a new manufacturing facility in Greenville, North Carolina, dedicated to producing diabetic care products including lancing devices and lancets. This expansion was intended to strengthen supply chains in North America and meet rising demand from hospitals, diagnostic centers, and homecare providers

- In October 2024, Medisave officially launched an integrated blood glucose monitoring kit that included a redesigned lancing device, test strips, and lancets. The bundled solution was developed to improve affordability and convenience for home-based diabetes management and support growing retail and online distribution channels

- In February 2025, manufacturers introduced microneedle-based and ultra-low-pain lancing technologies aimed at significantly reducing discomfort during capillary blood sampling. These advancements align with the growing demand for patient-centric, minimally invasive diabetes monitoring solutions and are expected to support higher testing compliance rates

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.