Global Dna Sequencing And Next Generation Sequencing Market

Market Size in USD Billion

CAGR :

%

USD

26.29 Billion

USD

95.19 Billion

2025

2033

USD

26.29 Billion

USD

95.19 Billion

2025

2033

| 2026 - 2033 | |

| USD 26.29 Billion | |

| USD 95.19 Billion | |

| % | |

|

DNA Sequencing and Next-Generation Sequencing Market Size

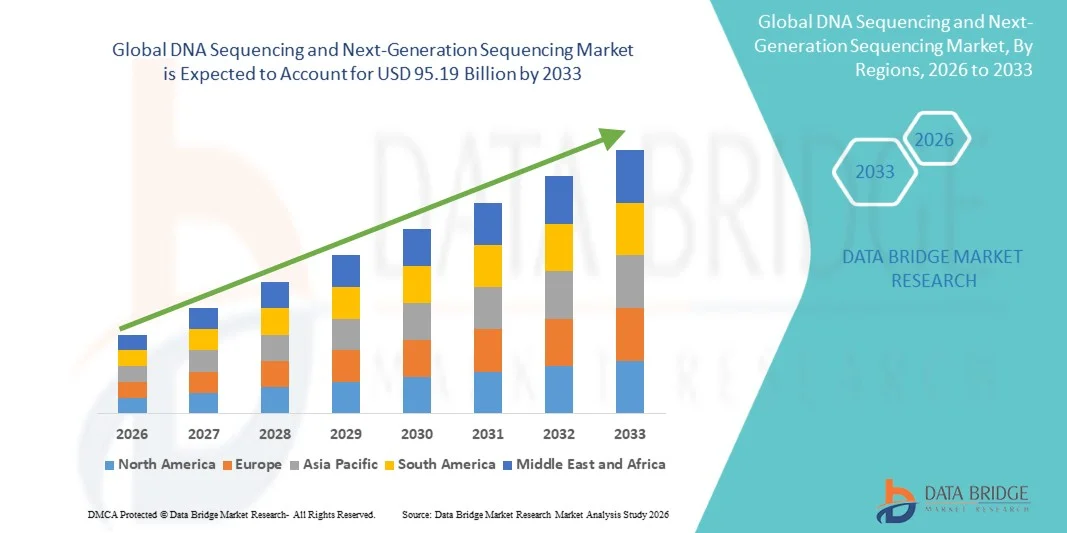

- The global DNA Sequencing and Next-Generation Sequencing market size was valued at USD 26.29 billion in 2025 and is expected to reach USD 95.19 billion by 2033, at a CAGR of 17.45% during the forecast period

- The market growth is largely fueled by rapid advancements in genomic technologies, increasing adoption of personalized medicine, and growing applications of DNA sequencing in diagnostics, drug discovery, and research, leading to higher demand for next-generation sequencing (NGS) solutions

- Furthermore, rising investments in genomics research, expanding applications in clinical diagnostics, oncology, and infectious disease testing, and the growing need for high-throughput, cost-effective, and accurate sequencing solutions are accelerating the uptake of DNA Sequencing and NGS technologies, thereby significantly boosting market growth

DNA Sequencing and Next-Generation Sequencing Market Analysis

- DNA sequencing and NGS solutions Smart sequencing technologies, offering high-throughput and precise genomic analysis, are increasingly vital components of modern research, clinical diagnostics, and personalized medicine due to their enhanced accuracy, speed, and integration with bioinformatics tools.

- The escalating demand for DNA sequencing and NGS solutions is primarily fueled by the widespread adoption of genomics in healthcare, biotechnology, and research, rising prevalence of genetic disorders, and a growing preference for cost-effective, high-throughput sequencing platforms

- North America dominated the DNA sequencing and next-generation sequencing market with the largest revenue share of 42.5% in 2025, characterized by advanced genomic research infrastructure, high healthcare expenditure, and a strong presence of key industry players. The U.S. is experiencing substantial growth in DNA sequencing installations, driven by innovations from established companies and startups in precision medicine, oncology, and infectious disease genomics

- Asia-Pacific is expected to be the fastest-growing region, with a CAGR-driven share of 28.7% during the forecast period, due to increasing investments in genomics research, rising healthcare infrastructure, and growing adoption of NGS technologies in emerging economies like China and India

- The Next-Generation Sequencing (NGS) platform dominated the market with a revenue share of 52.3% in 2025, due to its high throughput, cost-efficiency, and broad applicability

Report Scope and DNA Sequencing and Next-Generation Sequencing Market Segmentation

|

Attributes |

DNA Sequencing and Next-Generation Sequencing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

DNA Sequencing and Next-Generation Sequencing Market Trends

“Rising Demand for Advanced Genomic Research and Personalized Medicine”

- The global push for precision medicine and genomics-based research is fueling the adoption of DNA sequencing and next-generation sequencing (NGS) technologies. These platforms allow scientists and clinicians to identify genetic mutations, understand disease mechanisms, and tailor treatments to individual patients’ genetic profiles

- For instance, in 2025, Illumina, Inc. expanded its NovaSeq platform, offering faster genome sequencing at higher accuracy, enabling large-scale population studies and translational research in oncology and rare diseases. Such innovations are increasing demand for NGS platforms in research and clinical settings

- Growing awareness of hereditary disorders, cancer genomics, and personalized therapies is prompting hospitals and diagnostic laboratories to integrate sequencing technologies into routine clinical practice. This trend is particularly evident in oncology, where NGS aids in mutation profiling to guide targeted therapies

- Government initiatives and public-private partnerships are also acting as strong drivers. For example, the U.S. National Institutes of Health (NIH) has invested heavily in genome research projects like the All of Us Research Program, supporting the large-scale use of NGS platforms in population genomics studies

- The surge in biopharmaceutical R&D, especially in developing gene-based therapies and molecular diagnostics, has increased the need for high-throughput sequencing solutions that can accelerate drug discovery and clinical trials

- Increasing accessibility of cloud-based bioinformatics tools allows researchers to efficiently analyze complex genomic datasets, making DNA sequencing more viable for both large and small-scale studies

DNA Sequencing and Next-Generation Sequencing Market Dynamics

Driver

“Expansion in Emerging Markets and Growing Clinical Applications”

- Emerging economies in Asia-Pacific, Latin America, and the Middle East present lucrative opportunities due to rising healthcare spending, improving infrastructure, and increasing awareness of genomics-based healthcare solutions

- For instance, BGI Genomics has established multiple high-throughput sequencing centers across China and India, offering affordable sequencing solutions and supporting national research initiatives. This expansion is lowering cost barriers and enhancing market penetration in these regions

- The increasing applications of DNA sequencing in oncology, rare disease diagnosis, prenatal and neonatal screening, and infectious disease surveillance are driving market growth. Hospitals and clinics are adopting NGS as a routine diagnostic tool, enabling early detection and personalized interventions

- Collaborations between sequencing companies and pharmaceutical firms are creating new avenues for precision medicine and companion diagnostics. For example, Roche and Foundation Medicine have partnered to provide comprehensive genomic profiling for targeted cancer therapies

- Integration of NGS into large-scale epidemiological and population health studies offers additional opportunities. Countries investing in national genome projects are increasing demand for sequencing platforms to generate and analyze population-level genetic data

- Increasing availability of portable and benchtop sequencing instruments, such as Oxford Nanopore’s MinION, provides flexible solutions for clinical labs, research facilities, and field-based studies, opening markets previously inaccessible due to cost or infrastructure limitations

- Expansion in academic research and clinical trial applications is anticipated to further propel growth, as more studies utilize NGS to accelerate biomarker discovery, validate novel therapeutics, and enable precision medicine approaches globally

Restraint/Challenge

“High Cost of Sequencing Platforms and Limited Skilled Workforce”

- Despite technological advancements, the high initial investment required for NGS instruments, reagents, and maintenance limits adoption among smaller clinical labs and emerging-market institutions

- For instance, the cost of sequencing a single human genome using high-throughput platforms like PacBio Sequel II can still exceed tens of thousands of dollars, making it prohibitive for budget-conscious research facilities

- A significant challenge is the scarcity of trained professionals, including molecular biologists, bioinformaticians, and genetic counselors, who are essential for sequencing operation, data analysis, and interpretation

- The complexity of managing large genomic datasets requires robust computational infrastructure and expertise in bioinformatics pipelines, creating barriers for facilities without dedicated IT and genomics teams

- Regulatory and ethical concerns regarding genomic data privacy also pose challenges, as compliance with guidelines such as HIPAA (U.S.) or GDPR (Europe) requires secure data handling and storage systems, increasing operational costs

- Additional hurdles include the variability in reimbursement policies for sequencing-based diagnostics across different regions, which can limit clinical adoption despite proven utility in disease management

DNA Sequencing and Next-Generation Sequencing Market Scope

The market is segmented on the basis of product type, application, sequencing type, technology, platform, and end-user.

• By Product Type

On the basis of product type, the DNA Sequencing and Next-Generation Sequencing market is segmented into Instruments, Consumables, and Services. The Instruments segment dominated the largest market revenue share of 45.6% in 2025, driven by the adoption of high-performance sequencing platforms in research and clinical labs. Instruments provide high accuracy, scalability, and throughput, making them critical for genomics studies. Hospitals, pharmaceutical, and biotechnology companies prioritize acquisition of advanced sequencers. Academic institutes expand infrastructure for molecular biology and genomics research. Technological innovations and compact designs improve usability. Strong service networks enhance instrument reliability. Government funding and private investments boost procurement. Integration with multi-omics studies supports growth. Continuous R&D drives adoption of new instruments. The segment benefits from increasing global research funding. Overall, instruments remain the dominant product type.

The Consumables segment is expected to witness the fastest CAGR of 17.3% from 2026 to 2033, fueled by recurring demand for reagents, kits, and sequencing consumables. Consumables are critical for operating sequencing instruments and enable high-throughput experiments. Rising applications in diagnostics, drug discovery, and agricultural genomics boost consumption. Laboratories require continuous supply of high-quality reagents. Expansion of sequencing projects in emerging regions contributes to growth. Technological improvements in kits enhance accuracy and efficiency. Demand in pharmaceutical pipelines further accelerates adoption. Consumables are cost-effective for repeated experiments. Growth is supported by increasing research and clinical trials. Standardized protocols increase adoption in diagnostics and R&D. Overall, consumables emerge as the fastest-growing segment.

• By Application

On the basis of application, the market is segmented into Research, Diagnostic, Drug Discovery, Clinical, and Agriculture & Animal Research. The Research segment held the largest market revenue share of 48.2% in 2025, driven by growing genomics initiatives, government-funded programs, and academic research in molecular biology. Universities and research centers invest heavily in sequencing instruments and consumables. Collaboration with biotech firms accelerates adoption. Funding programs and grants further support research-focused sequencing. Sequencing provides insights into gene function, disease mechanisms, and personalized medicine development. High demand for multi-omics and population genomics drives growth. Educational initiatives promote NGS training. Overall, research dominates as the leading application.

The Diagnostic segment is expected to witness the fastest CAGR of 18.1% from 2026 to 2033, driven by adoption of sequencing for genetic testing, pathogen identification, and personalized treatment planning. Hospitals and clinical labs increasingly implement NGS for early disease detection. Rising incidence of genetic disorders and infectious diseases supports adoption. Regulatory approvals and insurance coverage enhance accessibility. Integration with clinical workflows improves patient outcomes. Emphasis on precision medicine and pharmacogenomics fuels demand. Diagnostics applications expand in oncology and rare disease testing. Rapid adoption in emerging regions contributes to growth. Overall, diagnostics emerges as the fastest-growing application.

• By Sequencing Type

On the basis of type, the market is segmented into Whole Genome Sequencing, Exome Sequencing, and Targeted Sequencing. Whole Genome Sequencing (WGS) dominated the largest revenue share of 46.7% in 2025, supported by comprehensive genomic analysis capability. WGS is widely used in research, clinical diagnostics, and population genomics. Rising projects in personalized medicine and oncology support adoption. Cost reductions and technological advancements enhance accessibility. Exome and targeted sequencing segments are gaining traction for focused applications. Academic, clinical, and industrial labs rely on WGS for detailed analysis. Integration with bioinformatics tools improves data interpretation. Government and private research funding accelerates WGS adoption. Overall, WGS remains dominant for large-scale studies.

Targeted Sequencing is expected to witness the fastest CAGR of 16.9% from 2026 to 2033, fueled by cancer panels, rare disease testing, and pharmacogenomics. Its cost-effectiveness and focused analysis suit clinical and drug discovery workflows. Growing adoption in diagnostics supports expansion. Increasing research funding and genomic initiatives drive growth. Focused sequencing panels reduce processing time and cost. Overall, targeted sequencing emerges as the fastest-growing type segment.

• By Technology

On the basis of technology, the DNA Sequencing and Next-Generation Sequencing market is segmented into Sequencing by Synthesis, Nanopore Sequencing, Sequencing by Ligation (SBL), Ion Semiconductor Sequencing, Pyrosequencing, Chain Termination Sequencing, Single-Molecule Real-Time Sequencing (SMRT), and Others. The Sequencing by Synthesis segment dominated the market with a revenue share of 44.8% in 2025. Its dominance is attributed to its high accuracy, scalability, and ability to process multiple samples simultaneously, which enhances laboratory productivity. Widely adopted in next-generation sequencing workflows, it supports diverse applications including research, clinical diagnostics, and pharmaceutical development. Technological advancements have improved read lengths, reduced errors, and increased reproducibility. Integration with automated systems further facilitates adoption in large academic and research institutes. High-throughput sequencing and workflow efficiency make it suitable for multi-sample and population-scale studies. Sequencing by Synthesis also benefits from robust software support for data analysis. Institutions prefer it for standardized, large-scale genomic studies. Its versatility across genomics, transcriptomics, and epigenetics ensures continued demand. The segment has become the backbone of modern sequencing laboratories.

The Nanopore Sequencing segment is expected to witness the fastest CAGR of 17.5% from 2026 to 2033, driven by its portability, rapid real-time analysis, and field-deployable applications. Nanopore devices enable sequencing outside traditional lab settings, facilitating on-site diagnostics and epidemiological studies. Its capacity for long-read sequencing improves genome assembly and structural variant detection. Lower capital costs and minimal infrastructure requirements accelerate adoption in emerging regions. Real-time data output allows faster decision-making in research and clinical applications. Growing demand in environmental genomics, infectious disease monitoring, and clinical research fuels market expansion. User-friendly interfaces and simplified workflows attract small-scale labs and mobile research units. Technological innovations continue to reduce error rates and improve throughput. Increasing collaborations with biotech firms and research institutes support market growth. Overall, Nanopore Sequencing is rapidly transforming portable and real-time sequencing applications worldwide.

• By Platform

On the basis of platform, the market is segmented into Sanger, Next-Generation Sequencing (NGS), qPCR, and Others. The Next-Generation Sequencing (NGS) platform dominated the market with a revenue share of 52.3% in 2025, due to its high throughput, cost-efficiency, and broad applicability. NGS enables large-scale genomics research, clinical diagnostics, and drug discovery with rapid turnaround. Its capability to process multiple samples simultaneously reduces per-base sequencing costs. Researchers and hospitals favor NGS for population genomics, precision medicine, and targeted therapies. Integration with bioinformatics pipelines facilitates comprehensive data analysis. NGS supports whole genome, exome, and targeted sequencing studies, making it versatile for various research and clinical applications. The platform’s scalability and adaptability attract academic, clinical, and pharmaceutical end-users. Sanger sequencing remains for validation or small-scale studies but NGS dominates enterprise-scale operations. Ongoing technological upgrades ensure sustained adoption. Overall, NGS is the most widely implemented sequencing platform globally.

The NGS platform is also expected to witness the fastest CAGR of 16.8% from 2026 to 2033, driven by expansion in clinical genomics, personalized medicine initiatives, and cost-effective high-throughput sequencing. Rising investment in genomics research and pharmaceutical R&D fuels rapid adoption. Increasing demand for early disease detection, biomarker discovery, and targeted therapies promotes growth. Enhanced data analysis software and automation improve efficiency and reduce turnaround time. Emerging markets are rapidly adopting NGS due to accessibility and reduced operational costs. Integration with multi-omics studies expands applications. Continuous improvements in sequencing chemistry and instrument throughput support faster adoption. Overall, NGS remains the dominant and fastest-growing platform simultaneously.

• By End-Users

On the basis of end-users, the market is segmented into Academic Institutes and Research Centers, Hospitals and Clinics, and Pharmaceutical and Biotechnology Companies. The Academic Institutes and Research Centers segment dominated with a revenue share of 50.1% in 2025, owing to extensive genomics research activities, government-funded initiatives, and collaborations with industry. These institutes invest heavily in sequencing instruments, consumables, and services to advance studies in genetics, molecular biology, and multi-omics. High-throughput sequencing enables large-scale research, population genomics, and epidemiological studies. Academic institutes benefit from access to grants, funding, and specialized facilities, encouraging adoption of cutting-edge technologies. Partnerships with pharmaceutical and biotech companies further accelerate use. They prioritize comprehensive sequencing workflows, robust data analysis, and reproducibility. Expansion of research programs in emerging regions supports market dominance. Integration with bioinformatics platforms enhances data interpretation and research efficiency. Overall, academic institutes lead as primary end-users globally.

The Pharmaceutical and Biotechnology Companies segment is expected to witness the fastest CAGR of 17.9% from 2026 to 2033, driven by the growing application of sequencing in drug discovery, biologics development, and precision medicine. Demand for genomics-driven therapeutics, target validation, and personalized treatment planning accelerates adoption. High-throughput sequencing supports preclinical and clinical trials. Strategic collaborations with academic institutes and CROs increase sequencing adoption. Investments in molecular diagnostics, biomarker discovery, and precision therapeutics promote growth. Emerging biotech hubs globally expand their sequencing infrastructure. Automation and advanced workflows improve operational efficiency and reduce costs. The pharma and biotech segment is rapidly increasing its market presence across global regions.

DNA Sequencing and Next-Generation Sequencing Market Regional Analysis

- North America dominated the DNA sequencing and next-generation sequencing market with the largest revenue share of 42.5% in 2025, characterized by advanced genomic research infrastructure, high healthcare expenditure, and a strong presence of key industry players

- The U.S. is experiencing substantial growth in DNA sequencing installations, driven by innovations from established companies and startups in precision medicine, oncology, and infectious disease genomics

- The region’s adoption is further supported by robust investments in clinical research, government initiatives for large-scale genome projects, and the increasing focus on personalized medicine, which require high-throughput sequencing platforms for accurate genetic analysis

U.S. DNA Sequencing and Next-Generation Sequencing Market Insight

The U.S. DNA sequencing and next-generation sequencing market accounted for the majority share of North America in 2025, driven by cutting-edge genomic research facilities, increasing clinical applications, and integration of sequencing in oncology, rare disease diagnostics, and prenatal screening. Growing investments in molecular diagnostics, coupled with the expanding number of precision medicine initiatives and collaborations between biotech firms and research institutions, are fueling market expansion. Moreover, government programs such as the NIH All of Us Research Program are accelerating the use of sequencing technologies for population genomics studies.

Europe DNA Sequencing and Next-Generation Sequencing Market Insight

The Europe DNA sequencing and next-generation sequencing market is projected to expand at a notable CAGR over the forecast period, supported by strong healthcare systems, increasing R&D in genomics, and favorable government funding for molecular diagnostics. Countries such as Germany, France, and the U.K. are adopting sequencing technologies in cancer genomics and infectious disease surveillance. The growing emphasis on personalized medicine, coupled with the presence of well-established biotechnology hubs, is driving clinical and research adoption across the region.

U.K. DNA Sequencing and Next-Generation Sequencing Market Insight

The U.K. DNA sequencing and next-generation sequencing market is expected to grow steadily during the forecast period, fueled by the national precision medicine initiative and the growing use of genomic sequencing in clinical settings. The adoption of next-generation sequencing is being encouraged by partnerships between healthcare providers, research institutions, and biotech companies, facilitating applications in oncology, rare disease research, and prenatal genetic testing. The increasing focus on academic research and clinical trials is also contributing to market expansion.

Germany DNA Sequencing and Next-Generation Sequencing Market Insight

Germany DNA sequencing and next-generation sequencing market is witnessing significant growth in the DNA sequencing and NGS market, driven by strong investments in genomic research infrastructure, technologically advanced laboratories, and increasing use of sequencing for diagnostic and therapeutic purposes. The country’s focus on innovation in healthcare, integration of genomics into clinical practice, and public-private partnerships are creating substantial opportunities for market players.

Asia-Pacific DNA Sequencing and Next-Generation Sequencing Market Insight

The Asia-Pacific DNA sequencing and next-generation sequencing market is expected to grow at the fastest CAGR of 28.7% from 2026 to 2033, driven by increasing investments in genomics research, expanding healthcare infrastructure, and rising demand for precision medicine in emerging economies such as China, India, and Japan. The region’s growing focus on infectious disease monitoring, government-backed genome initiatives, and the presence of cost-effective sequencing solutions are facilitating rapid adoption across research and clinical settings.

Japan DNA Sequencing and Next-Generation Sequencing Market Insight

Japan DNA sequencing and next-generation sequencing market is experiencing steady growth in the DNA sequencing market due to high investment in advanced healthcare technologies, a strong focus on precision medicine, and increasing adoption of NGS in oncology and rare disease research. Government support for genomics research and collaboration between academic and industrial players is further strengthening market expansion. The aging population is also driving demand for advanced genetic diagnostics and personalized therapies.

China DNA Sequencing and Next-Generation Sequencing Market Insight

China DNA sequencing and next-generation sequencing market accounted for the largest share of the Asia-Pacific market in 2025, supported by rapid urbanization, government initiatives for genomics research, and rising healthcare investments. The country is increasingly adopting NGS technologies in clinical diagnostics, population genomics, and precision medicine programs. The expansion of domestic sequencing companies and development of cost-efficient platforms are improving accessibility and affordability, further driving market growth.

DNA Sequencing and Next-Generation Sequencing Market Share

The DNA Sequencing and Next-Generation Sequencing industry is primarily led by well-established companies, including:

- Illumina (U.S.)

- Thermo Fisher Scientific (U.S.)

- BGI Genomics (China)

- Pacific Biosciences (U.S.)

- Oxford Nanopore Technologies (U.K.)

- QIAGEN (Germany)

- Roche (Switzerland)

- Agilent Technologies (U.S.)

- PerkinElmer (U.S.)

- GenapSys (U.S.)

- Novogene (China)

- Singlera Genomics (China)

- Element Biosciences (U.S.)

- Guardant Health (U.S.)

- NanoString Technologies (U.S.)

- Bio-Rad Laboratories (U.S.)

- Takara Bio (Japan)

- MGI Tech (China)

- Sophia Genetics (Switzerland)

- DNA Genotek (Canada)

Latest Developments in Global DNA Sequencing and Next-Generation Sequencing Market

- In June 2023, Illumina announced the launch of a new genomic sequencing AI neural network designed to accelerate interpretation of genomic data and integrate AI into sequencing workflows, marking a major step toward combining machine learning with high‑throughput DNA sequencing

- In May 2023, Revvity (formerly PerkinElmer Life Sciences & Diagnostics) began operations following its corporate spin‑out, positioning itself to expand global DNA sequencing applications — including newborn screening and multiomics workflows — as part of its strategy to push NGS technologies into broader clinical use

- In July 2025, scientists published the most comprehensive human genome map using advanced long‑read DNA sequencing technologies, sequencing over 1,000 genomes at high completeness and revealing previously hidden structural regions of the human genome, a milestone reflecting major technological progress in sequencing resolution and capability

- In December 2025, industry leaders including Illumina, Oxford Nanopore, Roche, and MGI announced expanded footprints in emerging genomics hubs in the Middle East and South Asia, establishing new partnerships and local sequencing capacity to support population‑scale genomic initiatives and clinical adoption of NGS technologies

- In September 2025, Element Biosciences filed antitrust and patent litigation against Illumina, alleging monopolistic practices and patent infringement in the gene‑sequencing market, a significant legal development highlighting competitive tensions and IP disputes within the NGS landscape

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.