Global Electric Mobility Market

Market Size in USD Billion

CAGR :

%

USD

206.50 Billion

USD

1,128.44 Billion

2025

2033

USD

206.50 Billion

USD

1,128.44 Billion

2025

2033

| 2026 - 2033 | |

| USD 206.50 Billion | |

| USD 1,128.44 Billion | |

| % | |

|

Electric Mobility Market Overview

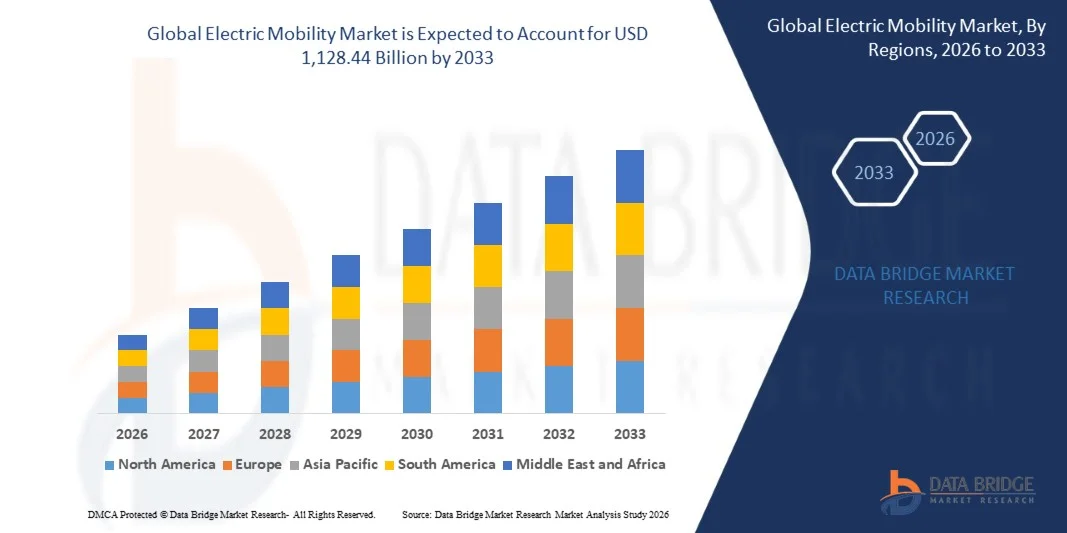

The Electric Mobility Market was valued at USD 206.50 billion in 2025 and is projected to reach USD 1,128.44 billion by 2033, growing at a CAGR of 23.65% from 2026 to 2033. The market is witnessing rapid expansion driven by accelerating adoption of electric vehicles, strong government incentives for clean transportation, and growing investments in charging infrastructure and battery technology across developed and emerging economies.

The increasing focus on reducing carbon emissions, rising fuel price volatility, and stringent global emission regulations are significantly accelerating the shift toward electric mobility solutions across passenger cars, two-wheelers, commercial vehicles, and shared mobility fleets. Continuous advancements in battery energy density, fast-charging technologies, and vehicle-to-grid integration are further enhancing adoption, while major automotive OEMs and new entrants are expanding electric vehicle portfolios to meet rising consumer demand for sustainable transportation alternatives.

Key Market Trends & Insights

- North America dominated the electric mobility market with the largest revenue share of approximately 42.8% in 2025, supported by strong EV adoption, expanding charging infrastructure, and favorable government incentives promoting zero-emission transportation.

- Asia-Pacific electric mobility market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, strong government EV policies, and expanding middle-class population in countries such as China, India, Japan, and South Korea.

- The Electric Car segment held the largest market revenue share of approximately 58.4% in 2025 driven by strong global adoption of passenger electric vehicles, expanding charging infrastructure, and aggressive OEM electrification strategies led by companies such as Tesla, BYD, and Volkswagen. Rising demand for long-range, high-performance EVs for personal and fleet applications is further strengthening segment dominance. Increasing government subsidies, tax incentives, and emission reduction mandates are also accelerating EV penetration across developed and emerging economies.

- The Electric Scooter segment is projected to register the fastest growth at a CAGR of 25.6% from 2026 to 2033, driven by rapid urbanization, rising last-mile connectivity demand, and increasing adoption of shared micro-mobility services across Asia-Pacific and Europe. Expanding ride-hailing integration and affordability compared to passenger EVs are further accelerating segment growth. Growing deployment of dockless scooter-sharing platforms and battery-swapping infrastructure is also supporting rapid adoption in congested urban centers.

- The Li-Ion segment held the largest market revenue share of approximately 87.2% in 2025 driven by its high energy density, lightweight structure, longer lifecycle, and widespread adoption across electric cars, scooters, and bicycles. Continuous advancements in lithium iron phosphate (LFP) and nickel manganese cobalt (NMC) chemistries are further strengthening dominance across all major EV categories. Rapid cost reduction in lithium-ion battery production and large-scale gigafactory expansion are also improving affordability and supply availability globally.

- The NiMH segment is projected to register moderate growth at a CAGR of 6.3% from 2026 to 2033, driven by its continued use in hybrid electric vehicles and certain low-cost mobility applications where cost stability and safety are prioritized over energy density. Ongoing utilization in legacy hybrid platforms, particularly in Japan and select North American models, continues to sustain steady demand.

- The Greater than 48V segment held the largest market revenue share of approximately 49.6% in 2025 driven by high adoption in electric cars, high-performance motorcycles, and advanced commercial EV platforms requiring higher power output and longer driving range. Increasing demand for fast acceleration, extended range, and improved energy efficiency is further supporting dominance of high-voltage systems.

- The 48V segment is projected to register the fastest growth at a CAGR of 24.1% from 2026 to 2033, driven by increasing adoption in mild-hybrid systems, electric scooters, and compact EV platforms offering improved efficiency and cost optimization for urban mobility solutions. Rising integration in automotive start-stop systems and hybrid electric architectures is also accelerating demand, particularly in Europe and Asia-Pacific markets where fuel efficiency regulations are stringent.

Market Size & Forecast

- Global Market Value (2025): USD 206.50 Billion

- Expected Market Value (2033): USD 1,128.44 Billion

- Forecast CAGR (2026–2033): 23.65%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Electric Mobility Market Segmentation

|

Attributes |

Electric Mobility Key Market Insights |

|

Segments Covered |

· By Product: Electric Scooter, Electric Bicycle, Electric Skateboard, Electric Motorcycle, Electric Car, and Electric Wheelchair · By Battery: Sealed Lead Acid, NiMH, and Li-Ion · By Voltage: 24V, Less than 24V, 36V, 48V, and Greater than 48V |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Tesla (U.S.) |

|

Market Opportunities |

• Expansion Of Ultra-Fast Charging Infrastructure Networks |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Electric Mobility Market Trends

Trend: Rapid Expansion Of Electrified Transportation And Smart Mobility Ecosystems

Increasing demand for low-emission transportation, government-backed electrification policies, and rising fuel price volatility are accelerating the shift toward electric mobility solutions across passenger vehicles, commercial fleets, and shared mobility platforms. Traditional internal combustion engine vehicles are being rapidly replaced by battery electric vehicles and plug-in hybrid models due to stricter emission regulations and long-term sustainability targets.

In modern automotive systems, manufacturers are integrating advanced lithium-ion and emerging solid-state battery technologies, for instance in vehicles such as Tesla Model Y and BYD Seal, to improve driving range, reduce charging time, and enhance energy efficiency. Expansion of ultra-fast charging networks capable of delivering 150–350 kW output is also supporting long-distance EV adoption, with operators in China and Europe deploying thousands of high-capacity charging stations in 2025 to reduce range anxiety and improve accessibility.

The rapid growth of shared mobility and electric public transportation is also increasing demand for fleet electrification across ride-hailing services, buses, and last-mile delivery vehicles, improving urban air quality and reducing operating costs. In addition, integration of vehicle-to-grid (V2G) technology and AI-based energy management systems is enabling two-way energy flow between EVs and power grids, with pilot projects in Europe demonstrating grid stabilization benefits of up to 10–15% during peak demand periods. Growing industry validation through large-scale EV deployment programs in 2025 across China and Europe is showing battery efficiency improvements of nearly 8–12% in optimized thermal and energy management conditions under real-world driving cycles.

Electric Mobility Market Dynamics

Key Market Driver: Strong Government Support And Rising Demand For Zero Emission Transportation

Governments worldwide are implementing strict emission regulations, tax incentives, and subsidy programs to accelerate electric vehicle adoption and reduce dependency on fossil fuels. Policies such as the European Union’s CO₂ emission targets and China’s New Energy Vehicle (NEV) mandates are significantly driving market expansion across passenger and commercial vehicle segments.

Automotive OEMs and fleet operators are increasingly shifting toward electrification to comply with regulatory frameworks and reduce long-term operational costs. For instance, EV penetration in Norway exceeded 80% of new car sales in 2024, reflecting strong policy effectiveness and consumer adoption. Similarly, major logistics companies in the U.S. and Europe are integrating electric delivery vans into urban supply chains to meet sustainability goals and reduce carbon footprints.

In addition, rising investment in renewable energy integration with EV charging infrastructure is strengthening the overall ecosystem, enabling cleaner and more efficient energy usage across transportation networks.

Key Restraint/Challenge: High Battery Costs And Charging Infrastructure Limitations

Despite strong growth, the electric mobility market is constrained by high battery manufacturing costs and limited availability of fast-charging infrastructure in developing regions. Lithium-ion battery packs remain a significant portion of total EV cost, impacting affordability for mass-market consumers, particularly in price-sensitive economies.

In addition, uneven charging infrastructure development across rural and semi-urban areas creates range anxiety and limits large-scale adoption. Charging time disparities compared to conventional refueling also continue to affect consumer preference, especially in long-distance and commercial applications.

Furthermore, supply chain dependencies on critical raw materials such as lithium, cobalt, and nickel pose risks of price volatility and geopolitical constraints, impacting production scalability and cost stability across global EV manufacturers.

Key Market Opportunity: Advancements In Battery Technology And Smart Mobility Integration

The growing focus on next-generation battery chemistries, including solid-state batteries and lithium iron phosphate (LFP) optimization, is creating significant opportunities for improving energy density, safety, and charging speed in electric vehicles. Continuous innovation in battery recycling and second-life applications is also enhancing sustainability across the EV value chain.

Automotive companies are increasingly integrating connected vehicle platforms, AI-driven energy optimization systems, and autonomous driving capabilities, for instance predictive energy management tools that improve driving range efficiency by up to 10–15% in real-world conditions.

In addition, expansion of smart city initiatives and electrified public transport networks across Asia-Pacific, Europe, and North America is further accelerating adoption. Large-scale electric bus deployments in cities such as Shenzhen, where full fleet electrification has already been achieved, demonstrate the scalability potential of electric mobility ecosystems in reducing urban emissions and improving transportation efficiency.

Electric Mobility Market Scope

The market is segmented on the basis of product, battery, and voltage.

- By Product

On the basis of product, the electric mobility market is segmented into Electric Scooter, Electric Bicycle, Electric Skateboard, Electric Motorcycle, Electric Car, and Electric Wheelchair. The Electric Car segment held the largest market revenue share of approximately 58.4% in 2025 driven by strong global adoption of passenger electric vehicles, expanding charging infrastructure, and aggressive OEM electrification strategies led by companies such as Tesla, BYD, and Volkswagen. Rising demand for long-range, high-performance EVs for personal and fleet applications is further strengthening segment dominance. Increasing government subsidies, tax incentives, and emission reduction mandates are also accelerating EV penetration across developed and emerging economies.

The Electric Scooter segment is projected to register the fastest growth at a CAGR of 25.6% from 2026 to 2033, driven by rapid urbanization, rising last-mile connectivity demand, and increasing adoption of shared micro-mobility services across Asia-Pacific and Europe. Expanding ride-hailing integration and affordability compared to passenger EVs are further accelerating segment growth. Growing deployment of dockless scooter-sharing platforms and battery-swapping infrastructure is also supporting rapid adoption in congested urban centers.

- By Battery

On the basis of battery, the market is segmented into Sealed Lead Acid, NiMH, and Li-Ion. The Li-Ion segment held the largest market revenue share of approximately 87.2% in 2025 driven by its high energy density, lightweight structure, longer lifecycle, and widespread adoption across electric cars, scooters, and bicycles. Continuous advancements in lithium iron phosphate (LFP) and nickel manganese cobalt (NMC) chemistries are further strengthening dominance across all major EV categories. Rapid cost reduction in lithium-ion battery production and large-scale gigafactory expansion are also improving affordability and supply availability globally.

The NiMH segment is projected to register moderate growth at a CAGR of 6.3% from 2026 to 2033, driven by its continued use in hybrid electric vehicles and certain low-cost mobility applications where cost stability and safety are prioritized over energy density. Ongoing utilization in legacy hybrid platforms, particularly in Japan and select North American models, continues to sustain steady demand.

- By Voltage

On the basis of voltage, the market is segmented into 24V, Less than 24V, 36V, 48V, and Greater than 48V. The Greater than 48V segment held the largest market revenue share of approximately 49.6% in 2025 driven by high adoption in electric cars, high-performance motorcycles, and advanced commercial EV platforms requiring higher power output and longer driving range. Increasing demand for fast acceleration, extended range, and improved energy efficiency is further supporting dominance of high-voltage systems.

The 48V segment is projected to register the fastest growth at a CAGR of 24.1% from 2026 to 2033, driven by increasing adoption in mild-hybrid systems, electric scooters, and compact EV platforms offering improved efficiency and cost optimization for urban mobility solutions. Rising integration in automotive start-stop systems and hybrid electric architectures is also accelerating demand, particularly in Europe and Asia-Pacific markets where fuel efficiency regulations are stringent.

Electric Mobility Market Regional Analysis

North America Electric Mobility Market Insight

North America dominated the electric mobility market with the largest revenue share of approximately 42.8% in 2025, supported by strong EV adoption, expanding charging infrastructure, and favorable government incentives promoting zero-emission transportation. The region benefits from high consumer purchasing power, advanced automotive manufacturing capabilities, and rapid integration of electric vehicles across passenger and commercial fleets. Increasing focus on reducing carbon emissions and strong presence of leading EV manufacturers further strengthen market leadership in the region.

U.S. Electric Mobility Market Insight

The U.S. electric mobility market captured the largest revenue share in North America in 2025, driven by rapid adoption of electric passenger vehicles, expansion of nationwide charging networks, and strong policy support through tax credits and emission regulations. The country is witnessing significant growth in EV manufacturing and battery production, supported by investments from major automakers such as Tesla, Ford, and General Motors. Increasing adoption of electric fleet vehicles in logistics and ride-hailing services is further accelerating market expansion.

Europe Electric Mobility Market Insight

The Europe electric mobility market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent carbon emission regulations, aggressive EV adoption targets, and strong government subsidies for electric vehicles and charging infrastructure. Countries such as Germany, France, Norway, and the Netherlands are leading EV penetration across passenger and commercial segments. Rising fuel prices, urban sustainability initiatives, and expansion of clean mobility zones are further supporting market growth across the region.

U.K. Electric Mobility Market Insight

The U.K. electric mobility market is expected to witness strong growth from 2026 to 2033, driven by increasing government mandates for zero-emission vehicles, rising consumer awareness of sustainable transport, and rapid expansion of public charging infrastructure. London and other major cities are witnessing strong adoption of EV taxis and delivery fleets. In addition, strong growth in home charging installations and rising availability of affordable electric models are further accelerating market penetration.

Germany Electric Mobility Market Insight

The Germany electric mobility market is expected to witness steady growth from 2026 to 2033, supported by strong automotive manufacturing base, increasing focus on sustainability, and rising demand for premium electric vehicles. Leading automakers such as Volkswagen, BMW, and Mercedes-Benz are heavily investing in EV platforms and battery technologies. Government incentives and strict emission regulations are further encouraging consumers to transition toward electric mobility, particularly in urban transportation systems.

Asia-Pacific Electric Mobility Market Insight

The Asia-Pacific electric mobility market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid urbanization, strong government EV policies, and expanding middle-class population in countries such as China, India, Japan, and South Korea. The region is also a major hub for EV manufacturing and battery production, significantly reducing costs and improving accessibility. Expansion of electric two-wheelers, three-wheelers, and shared mobility services is further accelerating adoption across densely populated urban centers.

Japan Electric Mobility Market Insight

The Japan electric mobility market is expected to witness steady growth from 2026 to 2033, driven by strong technological advancement, increasing environmental awareness, and government support for carbon neutrality goals. The country is focusing on hybrid and electric vehicle integration, with major automakers such as Toyota and Honda expanding EV portfolios. High urban density and advanced charging infrastructure are further supporting adoption, particularly in passenger cars and compact mobility solutions.

China Electric Mobility Market Insight

The China electric mobility market accounted for the largest revenue share in Asia-Pacific in 2025, supported by massive EV production capacity, strong government subsidies, and rapid urbanization. China remains the global leader in electric vehicle manufacturing and adoption, with strong dominance in electric cars, scooters, and buses. Companies such as BYD and NIO are driving innovation and large-scale deployment, while extensive charging infrastructure and smart city initiatives are further strengthening market growth in the country.

Electric Mobility Market Share

The Electric Mobility industry is primarily led by well-established companies, including:

• Tesla (U.S.)

• TOYOTA MOTOR CORPORATION (Japan)

• Nissan (Japan)

• Groupe Renault (France)

• Ford Motor Company (U.S.)

• General Motors (U.S.)

• AB Volvo (Sweden)

• BMW AG (Germany)

• Marshell Green Power (China)

• Daimler AG (Germany)

• MG Motor India Pvt. Ltd. (India)

• Honda Motor Co., Ltd (Japan)

• Tata Sons Private Limited (India)

• Mitsubishi Motors North America, Inc. (U.S.)

Latest Developments in Electric Mobility Market

- In December 2024, Rivian and Volkswagen (VW) formed a USD 5.8 billion joint venture to advance electric vehicle technology across multiple vehicle categories, integrating Rivian’s software capabilities with Volkswagen’s global manufacturing platform expertise. This collaboration is expected to accelerate EV innovation, reduce development costs, and strengthen competitiveness in the global electric vehicle market through scalable software-defined vehicle architecture.

- In October 2023, Stellantis N.V. entered a memorandum of understanding (MOU) to establish a joint venture focused on recycling end-of-life electric vehicle batteries and gigafactory scrap across Europe and North America. The initiative leverages Orano’s low-carbon technology to recover critical materials from lithium-ion batteries, including production of new cathode materials. This development is likely to support circular economy practices, reduce raw material dependency, and strengthen sustainability in the EV supply chain.

- In October 2023, Toyota Motor signed a supply agreement with LG Energy Solution for battery electric vehicles assembled in the U.S., under which LG Energy Solution will supply 20GWh of high-nickel NCMA battery modules annually starting from 2025. The company will invest approximately USD 3 billion in its Michigan facility to expand battery cell and module production for Toyota’s requirements. This partnership is expected to secure battery supply stability, enhance EV production capacity, and strengthen Toyota’s electrification strategy in the North American market.

- In February 2023, BYD announced new dealer partnerships in Europe, including Motor Distributors Ltd (MDL) in Ireland and RSA in Norway, expanding distribution across Finland and Iceland. This move supports BYD’s entry into multiple European markets with its electric vehicle lineup. The expansion is expected to improve market penetration, strengthen brand presence in Europe, and accelerate adoption of Chinese EV models in the region.

- In January 2024, Tesla announced plans to develop an affordable robotaxi and an entry-level USD 25,000 electric vehicle built on a shared vehicle architecture, targeted for launch around 2025. This strategy aims to position Tesla competitively against low-cost gasoline vehicles and emerging budget EV manufacturers such as BYD. The development is expected to expand EV accessibility, increase market competition in the entry-level segment, and accelerate adoption of autonomous mobility solutions.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.