Global Fixed Wing Vtol Uav Market

Market Size in USD Million

CAGR :

%

USD

801.42 Million

USD

3,354.71 Million

2025

2033

USD

801.42 Million

USD

3,354.71 Million

2025

2033

| 2026 –2033 | |

| USD 801.42 Million | |

| USD 3,354.71 Million | |

| % | |

|

What is the Global Fixed-wing VTOL UAV Market Size and Growth Rate?

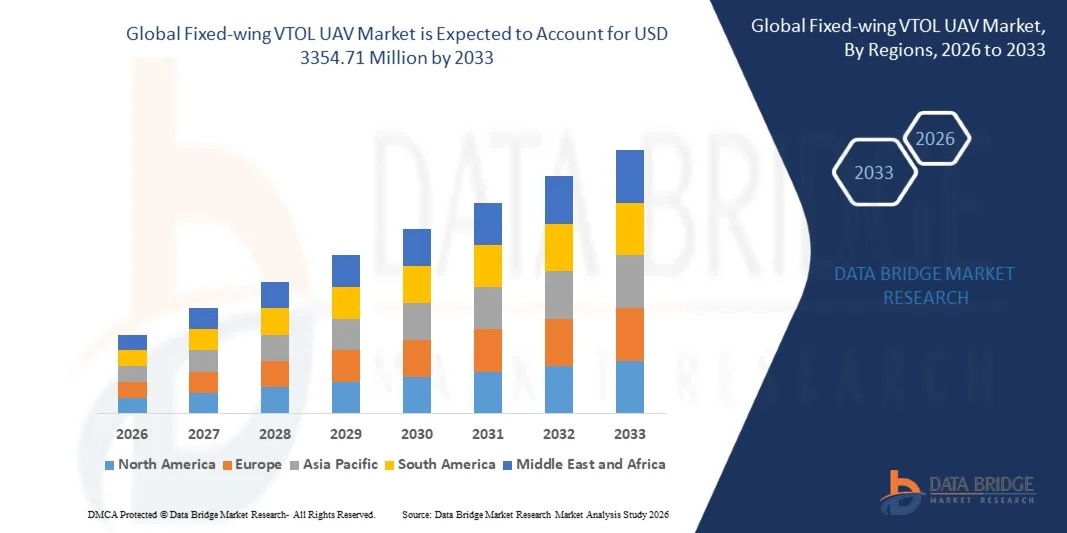

- The global Fixed-wing VTOL UAV market size was valued at USD 801.42 million in 2025 and is expected to reach USD 3354.71 million by 2033, at a CAGR of19.60% during the forecast period

- The increase in use of fixed-wing VTOL UAVs in military applications acts as one of the major factors driving the growth of the fixed-wing VTOL UAV market

- The rise in deployment of fixed-wing VTOL UAVs to carry out aerial remote sensing, and increase in popularity of fixed-wing VTOL UAVs in military applications accelerate the market growth

What are the Major Takeaways of Fixed-wing VTOL UAV Market?

- The rise in the popularity of fixed-wing VTOL UAVs in life-threatening military missions, and use of fixed-wing VTOL UAVs in advanced patrolling of marine borders further influence the market

- In addition, growth of the heavy engineering industry, use of fixed-wing VTOL UAVs in life-threatening military missions, rapid urbanization and use of modern warfare techniques positively affect the fixed-wing VTOL UAV market

- Furthermore, use of fixed-wing VTOL UAVs for cargo delivery in military and commercial applications, and technological developments in the field of drone payloads extend profitable opportunities to the market players

- North America dominated the Fixed-wing VTOL UAV market with a 43.2% revenue share in 2025, driven by strong defence modernization programs, increasing investments in unmanned aerial systems, and rising adoption of advanced surveillance technologies across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 10.58% from 2026 to 2033, driven by increasing defence modernization programs, expanding surveillance infrastructure, and rising adoption of UAV technologies across China, Japan, India, South Korea, and Southeast Asia

- The Visual Line of Sight (VLOS) segment dominated the market with a 44.6% share in 2025, as it remains widely adopted for short-distance surveillance, inspection, and monitoring missions where operators maintain direct visual contact with the UAV

Report Scope and Fixed-wing VTOL UAV Market Segmentation

|

Attributes |

Fixed-wing VTOL UAV Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the Fixed-wing VTOL UAV Market?

“Growing Adoption of Hybrid VTOL Platforms for Long-Endurance and Multi-Mission Operations”

- The Fixed-wing VTOL UAV market is witnessing rising adoption of hybrid aerial platforms that combine vertical take-off capability with fixed-wing cruise efficiency, enabling long-endurance missions and flexible deployment without the need for runways

- Manufacturers are increasingly developing lightweight composite airframes, advanced propulsion systems, and autonomous flight control technologies to improve flight stability, endurance, and operational range

- Growing demand for versatile UAV platforms capable of operating in remote, confined, and infrastructure-limited environments is accelerating adoption across defence, surveillance, mapping, and disaster monitoring applications

- For instance, companies such as AeroVironment, Northrop Grumman, Israel Aerospace Industries, and Elbit Systems are introducing advanced fixed-wing VTOL UAVs with improved endurance, payload capacity, and autonomous navigation capabilities

- Increasing integration of AI-based navigation, high-resolution sensors, and real-time communication systems is enhancing mission efficiency and enabling advanced aerial intelligence capabilities

- As defence agencies and commercial operators demand long-range UAVs with flexible deployment capabilities, fixed-wing VTOL platforms are expected to play a critical role in next-generation aerial surveillance and monitoring systems

What are the Key Drivers of Fixed-wing VTOL UAV Market?

- Rising demand for long-endurance UAVs capable of vertical take-off and efficient forward flight is driving adoption across defence surveillance, border security, environmental monitoring, and infrastructure inspection operations

- For instance, in 2025, companies such as Boeing, Lockheed Martin, and Saab expanded their UAV portfolios by introducing advanced fixed-wing VTOL platforms designed for extended surveillance and tactical reconnaissance missions

- Increasing use of UAVs for military intelligence, mapping, disaster management, and agricultural monitoring is creating strong demand for highly efficient hybrid aerial systems worldwide

- Advancements in electric propulsion systems, battery technology, autonomous flight software, and lightweight composite materials are improving UAV endurance, payload capability, and operational efficiency

- Rising investments in defence modernization programs, border surveillance systems, and smart infrastructure monitoring are further accelerating the adoption of advanced VTOL UAV platforms globally

- Supported by continuous innovation in aerospace engineering, sensor integration, and AI-enabled flight control, the Fixed-wing VTOL UAV market is expected to witness strong long-term growth

Which Factor is Challenging the Growth of the Fixed-wing VTOL UAV Market?

- High development and manufacturing costs associated with advanced propulsion systems, composite airframes, and integrated avionics limit adoption among smaller commercial operators and startups

- For instance, during 2024–2025, increasing costs of aerospace-grade materials, high-performance batteries, and advanced sensor systems raised production expenses for several UAV manufacturers

- Regulatory challenges related to airspace integration, flight permissions, and UAV certification requirements continue to restrict large-scale deployment in many regions

- Technical complexities in maintaining stable vertical-to-horizontal flight transitions, payload balancing, and long-range communication systems require advanced engineering expertise and testing

- Competition from multi-rotor drones and conventional fixed-wing UAV platforms, which may offer lower costs or simpler operations, also creates market adoption challenges

- To overcome these issues, companies are focusing on cost-efficient designs, improved autonomous flight systems, and regulatory collaboration, which will help expand the global adoption of fixed-wing VTOL UAV platforms

How is the Fixed-wing VTOL UAV Market Segmented?

The market is segmented on the basis of range, MTOW, propulsion, endurance, mode of operation, application, and vertical.

• By Range

On the basis of range, the Fixed-wing VTOL UAV market is segmented into Visual Line of Sight (VLOS), Extended Visual Line of Sight (EVLOS), and Beyond Line of Sight (BLOS). The Visual Line of Sight (VLOS) segment dominated the market with a 44.6% share in 2025, as it remains widely adopted for short-distance surveillance, inspection, and monitoring missions where operators maintain direct visual contact with the UAV. VLOS operations are commonly used in infrastructure inspection, agricultural monitoring, and local security operations due to their lower regulatory requirements, operational simplicity, and reduced communication system complexity. These UAVs are easier to deploy and require minimal infrastructure, making them popular among commercial operators and small defence units.

The Beyond Line of Sight (BLOS) segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for long-distance surveillance, border monitoring, maritime patrol, and large-area mapping operations. Advancements in satellite communication, autonomous navigation, and long-range data links are enabling UAVs to perform complex missions beyond direct operator visibility.

• By MTOW

On the basis of maximum take-off weight (MTOW), the market is segmented into <25 Kilograms, 25–170 Kilograms, and >170 Kilograms. The <25 Kilograms segment dominated the market with a 41.8% share in 2025, supported by strong demand for lightweight UAV platforms used in surveillance, mapping, environmental monitoring, and infrastructure inspection. These UAVs are easier to transport, deploy quickly, and require lower operational costs compared to heavier systems. Their compact size and efficient VTOL capabilities make them ideal for commercial applications, law enforcement, and small tactical military missions. In addition, favourable regulatory frameworks in many countries for lightweight UAVs further support their adoption.

The 25–170 Kilograms segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for medium-endurance UAVs capable of carrying advanced payloads such as electro-optical sensors, communication relays, and surveillance equipment. These UAVs offer a balance between payload capacity, endurance, and operational flexibility, making them suitable for defence and large-scale monitoring missions.

• By Propulsion

On the basis of propulsion, the Fixed-wing VTOL UAV market is segmented into Electric, Hybrid, and Gasoline. The Electric propulsion segment dominated the market with a 46.3% share in 2025, due to its lower operating costs, reduced noise levels, and improved energy efficiency compared to conventional fuel-powered systems. Electric propulsion systems are widely used in commercial UAVs for applications such as mapping, inspection, and environmental monitoring. Improvements in battery technology, energy density, and lightweight electric motors are enhancing UAV performance while reducing maintenance requirements. Electric VTOL UAVs are also gaining popularity due to their environmentally friendly operation and simplified mechanical design.

The Hybrid propulsion segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by the need for longer endurance, higher payload capacity, and extended operational range. Hybrid propulsion systems combine electric motors with fuel-powered generators, enabling UAVs to perform longer missions while maintaining efficient energy consumption.

• By Endurance

On the basis of endurance, the Fixed-wing VTOL UAV market is segmented into <5 hours, 5–10 hours, and >10 hours. The 5–10 hours segment dominated the market with a 38.7% share in 2025, as it provides an optimal balance between flight time, operational cost, and mission flexibility. UAVs with this endurance range are widely used in defence surveillance, infrastructure inspection, environmental monitoring, and mapping applications. These platforms can cover large operational areas while maintaining stable flight performance and reliable data transmission. Their moderate endurance allows operators to conduct extended missions without requiring complex fuel systems or heavy battery packs.

The >10 hours segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for long-duration surveillance missions, maritime monitoring, border patrol, and large-scale disaster management operations. Increasing adoption of hybrid propulsion systems and high-capacity energy storage technologies is enabling UAVs to achieve extended flight endurance.

• By Mode of Operation

On the basis of mode of operation, the Fixed-wing VTOL UAV market is segmented into Remotely Piloted, Optionally Piloted, and Fully Autonomous. The Remotely Piloted segment dominated the market with a 48.9% share in 2025, as most UAV operations currently rely on trained operators to control flight paths, monitor payload systems, and ensure mission safety. Remotely piloted systems offer high reliability and allow operators to adapt quickly to changing mission requirements. These UAVs are widely used in defence, border surveillance, disaster monitoring, and infrastructure inspection where human oversight remains critical.

The Fully Autonomous segment is expected to grow at the fastest CAGR from 2026 to 2033, supported by rapid advancements in artificial intelligence, autonomous navigation systems, and machine learning-based flight control technologies. Autonomous UAVs can conduct complex missions with minimal human intervention, improving operational efficiency and enabling large-scale UAV deployments.

• By Application

On the basis of application, the Fixed-wing VTOL UAV market is segmented into Border Management, Traffic Monitoring, Firefighting & Disaster Management, Search & Rescue, Police Operations & Investigations, and Maritime Security. The Border Management segment dominated the market with a 34.2% share in 2025, driven by increasing demand for persistent aerial surveillance to monitor large and remote border regions. Fixed-wing VTOL UAVs provide long-range monitoring capabilities, real-time video surveillance, and rapid deployment, making them highly effective for border patrol missions. Governments and defence agencies are increasingly deploying UAVs to enhance national security and reduce reliance on manned aircraft.

The Search & Rescue segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising use of UAVs for disaster response, emergency monitoring, and rapid victim location. Equipped with thermal cameras and advanced sensors, these UAVs significantly improve rescue efficiency during natural disasters and emergency operations.

• By Vertical

On the basis of vertical, the Fixed-wing VTOL UAV market is segmented into Military and Commercial. The Military segment dominated the market with a 55.4% share in 2025, driven by growing defence investments in advanced unmanned aerial systems for surveillance, intelligence gathering, and tactical reconnaissance. Fixed-wing VTOL UAVs are increasingly used by military forces due to their ability to operate without runways while providing long-endurance flight capabilities. These UAVs support missions such as border security, battlefield surveillance, communication relay, and reconnaissance in remote environments.

The Commercial segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by expanding use of UAVs in infrastructure inspection, agriculture, environmental monitoring, logistics, and mapping applications. Increasing adoption of smart monitoring technologies and UAV-based data analytics solutions is further accelerating the commercialization of fixed-wing VTOL UAV platforms.

Which Region Holds the Largest Share of the Fixed-wing VTOL UAV Market?

- North America dominated the Fixed-wing VTOL UAV market with a 43.2% revenue share in 2025, driven by strong defence modernization programs, increasing investments in unmanned aerial systems, and rising adoption of advanced surveillance technologies across the U.S. and Canada. Fixed-wing VTOL UAVs are increasingly deployed for border security, intelligence gathering, maritime patrol, and disaster monitoring missions. Their ability to combine vertical take-off capability with long-endurance fixed-wing flight makes them highly effective for tactical and long-range operations across military and security agencies

- Leading aerospace and defence companies in North America are focusing on developing high-endurance UAV platforms with advanced sensors, autonomous navigation systems, and secure communication technologies, strengthening the region’s technological leadership in unmanned aviation. Continuous investment in artificial intelligence, satellite communication systems, and integrated ISR (Intelligence, Surveillance, and Reconnaissance) capabilities further supports market growth

- Strong defence infrastructure, presence of major UAV manufacturers, and growing adoption of advanced aerial surveillance solutions continue to reinforce North America’s leadership in the Fixed-wing VTOL UAV market

U.S. Fixed-wing VTOL UAV Market Insight

The U.S. represents the largest contributor in North America, supported by extensive defence spending and continuous technological innovation in unmanned aerial systems. Increasing deployment of fixed-wing VTOL UAVs for border monitoring, military reconnaissance, coastal surveillance, and disaster response operations is driving market growth. Defence agencies and homeland security organizations are investing in advanced UAV platforms equipped with high-resolution cameras, thermal imaging sensors, and real-time communication systems. In addition, the presence of leading aerospace companies and strong R&D capabilities in autonomous flight technologies continue to strengthen the country’s market leadership.

Canada Fixed-wing VTOL UAV Market Insight

Canada contributes significantly to regional growth due to increasing use of UAVs for environmental monitoring, border surveillance, resource exploration, and disaster management operations. The country’s vast geographical landscape and remote regions create strong demand for UAV platforms capable of long-range monitoring and vertical take-off in infrastructure-limited environments. Government initiatives supporting defence modernization and technological innovation further accelerate the adoption of fixed-wing VTOL UAV systems across military and civil applications.

Asia-Pacific Fixed-wing VTOL UAV Market

Asia-Pacific is projected to register the fastest CAGR of 10.58% from 2026 to 2033, driven by increasing defence modernization programs, expanding surveillance infrastructure, and rising adoption of UAV technologies across China, Japan, India, South Korea, and Southeast Asia. Governments across the region are investing heavily in border security, maritime monitoring, disaster response, and infrastructure inspection, creating strong demand for advanced unmanned aerial systems. Rapid advancements in UAV manufacturing, sensor integration, and autonomous flight technologies are enabling the development of high-performance fixed-wing VTOL platforms across the region. Growing defence budgets, expanding drone startups, and increasing investments in aerospace innovation continue to accelerate regional market growth.

China Fixed-wing VTOL UAV Market Insight

China is the largest contributor to the Asia-Pacific market due to its strong UAV manufacturing ecosystem and significant investments in defence and surveillance technologies. The country is actively developing advanced fixed-wing VTOL UAVs for military reconnaissance, border security, industrial monitoring, and smart city surveillance. Strong government support and large-scale drone production capabilities further strengthen China’s position in the global UAV industry.

Japan Fixed-wing VTOL UAV Market Insight

Japan demonstrates steady growth driven by increasing adoption of UAVs for disaster response, infrastructure inspection, coastal monitoring, and environmental research. The country’s focus on advanced robotics, autonomous systems, and precision engineering supports the development of reliable and high-performance fixed-wing VTOL UAV platforms.

India Fixed-wing VTOL UAV Market Insight

India is emerging as a key growth hub due to rising investments in defence modernization, border surveillance technologies, and domestic drone manufacturing initiatives. Government programs promoting indigenous UAV development and increasing demand for aerial monitoring across agriculture, infrastructure inspection, and disaster management sectors are accelerating the adoption of fixed-wing VTOL UAV platforms.

South Korea Fixed-wing VTOL UAV Market Insight

South Korea contributes significantly to regional market expansion due to strong defence technology development and increasing demand for advanced surveillance systems. The country is actively investing in autonomous drone technologies, AI-enabled aerial monitoring, and next-generation unmanned aircraft systems. Strong aerospace manufacturing capabilities and growing innovation in drone technologies continue to support sustained market growth.

Which are the Top Companies in Fixed-wing VTOL UAV Market?

The Fixed-wing VTOL UAV industry is primarily led by well-established companies, including:

- General Atomics (U.S.)

- Northrop Grumman Corporation (U.S.)

- Israel Aerospace Industries Ltd. (Israel)

- AeroVironment, Inc. (U.S.)

- Lockheed Martin Corporation (U.S.)

- Boeing (U.S.)

- Aeronautics Ltd. (Israel)

- Saab AB (Sweden)

- Thales Group (France)

- DJI (China)

- Parrot Drone SAS (France)

- 3D Robotics (3DR) (U.S.)

- Textron Systems (U.S.)

- BAE Systems (U.K.)

- Raytheon Company (U.S.)

- EHang (China)

- ECA Group (France)

- Yuneec International (China)

- Microdrones (Germany)

- Elbit Systems Ltd. (Israel)

What are the Recent Developments in Global Fixed-wing VTOL UAV Market?

- In March 2025, Lockheed Martin Corporation (U.S.), through its Sikorsky division, introduced the Nomad™ program, aimed at developing scalable fixed-wing VTOL drones designed for long-endurance missions. The initiative was launched in collaboration with the U.S. Air Force Research Laboratory to advance autonomous logistics operations and intelligence, surveillance, and reconnaissance (ISR) capabilities. This development strengthens the evolution of next-generation autonomous UAV platforms for advanced military operations

- In September 2024, UKRSPECSYSTEMS (Ukraine) announced a strategic manufacturing collaboration with a U.K.-based defence consortium to produce the PD-2 fixed-wing VTOL UAV within the United Kingdom. The initiative focuses on strengthening regional production capacity, improving supply chain resilience, and expanding export opportunities across European defence markets. This partnership supports the growth of localized UAV manufacturing and strengthens defence technology cooperation in Europe

- In June 2024, Textron Systems (U.S.) partnered with the U.S. Navy’s Naval Air Systems Command to expand the deployment and capabilities of its Aerosonde family of fixed-wing VTOL UAVs. The collaboration includes improvements in maritime endurance performance, enhanced data-link connectivity, and operational support for naval intelligence, surveillance, and reconnaissance missions. This collaboration enhances the operational capability of VTOL UAV systems for advanced maritime defence applications

- In May 2024, AeroVironment Inc. (U.S.) signed a memorandum of understanding with the National Chung-Shan Institute of Science and Technology (Taiwan) to co-develop advanced fixed-wing VTOL UAV platforms. The partnership aims to expand manufacturing capacity and integrate hybrid-electric propulsion technologies for next-generation reconnaissance systems. This initiative accelerates innovation in high-performance UAV technologies for modern surveillance operations

- In February 2024, AeroVironment Inc. (U.S.) entered into a strategic partnership with Korean Air (South Korea) to jointly develop and customize the JUMP 20 fixed-wing VTOL UAV system for regional defence applications. The collaboration focuses on technology transfer, platform adaptation, and advanced payload integration to support tactical surveillance and border monitoring missions in Korea. This partnership strengthens international collaboration in the development of advanced defence UAV platforms

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.