Global Food Allergens And Intolerance Testing Market

Market Size in USD Million

CAGR :

%

USD

784.28 Million

USD

1,462.45 Million

2025

2033

USD

784.28 Million

USD

1,462.45 Million

2025

2033

| 2026 –2033 | |

| USD 784.28 Million | |

| USD 1,462.45 Million | |

| % | |

|

Food Allergens and Intolerance Testing Market Size

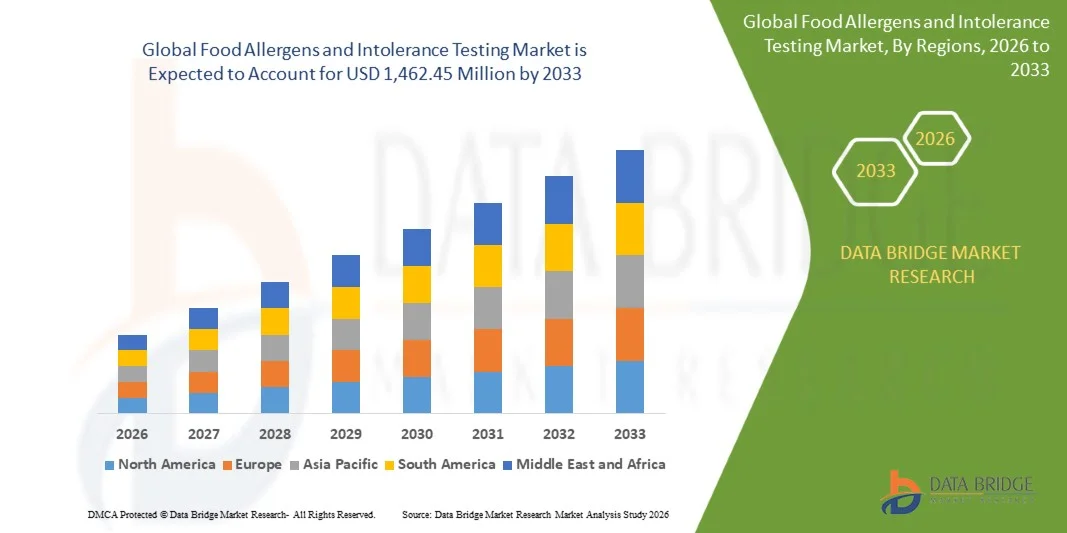

- The global food allergens and intolerance testing market size was valued at USD 784.28 million in 2025 and is expected to reach USD 1,462.45 million by 2033, at a CAGR of 8.10% during the forecast period

- The market growth is largely fuelled by the increasing prevalence of food allergies and intolerances along with rising consumer awareness regarding food safety and health

- Growing demand for accurate diagnostic solutions and stringent food labeling regulations are further supporting market expansion

Food Allergens and Intolerance Testing Market Analysis

- The market is experiencing steady growth driven by advancements in diagnostic technologies such as immunoassays and molecular testing, enabling faster and more reliable detection of allergens

- Increasing focus on preventive healthcare, coupled with rising adoption of personalized nutrition and dietary management, is encouraging the use of food allergen and intolerance testing solutions

- North America dominated the food allergens and intolerance testing market with the largest revenue share in 2025, driven by the high prevalence of food allergies and strong awareness regarding early diagnosis and preventive healthcare

- Asia-Pacific region is expected to witness the highest growth rate in the global food allergens and intolerance testing market, driven by increasing urbanization, expanding healthcare infrastructure, and growing awareness regarding food safety and preventive healthcare

- The allergen testing segment held the largest market revenue share in 2025 driven by the increasing prevalence of food allergies and the growing need for accurate identification of allergenic substances. Allergen testing is widely adopted in clinical and laboratory settings due to its ability to provide reliable and standardized results, supporting effective diagnosis and management of allergic conditions. Increasing regulatory emphasis on food safety and labeling standards is further strengthening demand for allergen testing solutions. In addition, advancements in immunoassay and molecular diagnostic technologies are improving testing accuracy and efficiency. Growing collaboration between healthcare providers and diagnostic laboratories is also supporting wider adoption across developed and emerging markets

Report Scope and Food Allergens and Intolerance Testing Market Segmentation

|

Attributes |

Food Allergens and Intolerance Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• SGS SA (Switzerland) |

|

Market Opportunities |

• Increasing Adoption Of At-Home Testing Kits |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Food Allergens and Intolerance Testing Market Trends

“Rising Demand For Accurate And Rapid Food Allergy Diagnostics”

• The increasing prevalence of food allergies and intolerances is significantly shaping the global food allergens and intolerance testing market, as consumers and healthcare providers increasingly seek reliable and timely diagnostic solutions. Advanced testing methods are gaining traction due to their ability to deliver precise results, support early diagnosis, and improve patient outcomes. This trend is strengthening adoption across clinical laboratories, hospitals, and at-home testing environments, encouraging manufacturers to develop innovative and user-friendly testing kits

• Growing awareness regarding health, nutrition, and preventive care has accelerated the demand for food allergen and intolerance testing across diverse population groups. Consumers are actively seeking personalized dietary solutions based on test results, prompting healthcare providers and diagnostic companies to expand service offerings. This has also led to collaborations between diagnostic laboratories and nutrition experts to enhance the effectiveness of testing and dietary management programs

• Technological advancements are influencing purchasing decisions, with manufacturers emphasizing rapid testing, high sensitivity, and ease of use. These factors are helping companies differentiate their offerings while improving accessibility and efficiency in diagnostics. Increasing integration of digital health platforms and telemedicine is also enabling remote consultations and test result management, enhancing overall patient experience

• For instance, in 2024, companies such as Thermo Fisher Scientific and Eurofins Scientific expanded their testing portfolios by introducing advanced allergen detection kits and laboratory services. These solutions were designed to improve diagnostic accuracy and turnaround time, with availability across hospitals, clinics, and online platforms. The services were also marketed as essential tools for managing food allergies and improving quality of life, strengthening consumer trust and adoption

• While demand for food allergen and intolerance testing is growing, sustained market expansion depends on improving affordability, increasing awareness in developing regions, and ensuring regulatory compliance. Companies are focusing on expanding testing capabilities, enhancing accuracy, and developing cost-effective solutions to support broader adoption

Food Allergens and Intolerance Testing Market Dynamics

Driver

“Increasing Prevalence Of Food Allergies And Intolerances”

• Rising incidence of food allergies and intolerances is a major driver for the global food allergens and intolerance testing market. Healthcare providers are increasingly recommending diagnostic testing to identify allergens and manage dietary risks effectively. This trend is also encouraging research into advanced diagnostic technologies and novel biomarkers for improved detection

• Expanding applications across hospitals, diagnostic laboratories, and home testing kits are influencing market growth. Testing solutions help identify specific allergens, support personalized nutrition plans, and reduce health complications, enabling better patient care and management. The increasing adoption of preventive healthcare practices further reinforces this trend

• Diagnostic companies are actively promoting testing solutions through product innovation, partnerships, and awareness campaigns. These efforts are supported by rising consumer interest in health monitoring and personalized nutrition, encouraging collaborations between healthcare providers and testing laboratories to improve service delivery

• For instance, in 2023, companies such as Abbott Laboratories and Danaher Corporation reported increased demand for allergy and intolerance testing solutions across clinical and home settings. This expansion followed growing consumer awareness and rising cases of food-related sensitivities, driving repeat usage and service expansion. Both companies also emphasized accuracy, speed, and accessibility to strengthen market positioning

• Although increasing prevalence supports market growth, wider adoption depends on improving cost efficiency, expanding healthcare access, and ensuring standardization of testing methods. Investment in research, infrastructure, and education will be critical for sustaining long-term market growth

Restraint/Challenge

“High Cost And Limited Awareness In Emerging Markets”

• The relatively high cost of advanced food allergen and intolerance testing remains a key challenge, limiting accessibility for price-sensitive consumers. Expenses associated with laboratory testing, equipment, and skilled professionals contribute to higher costs, restricting widespread adoption. In addition, lack of insurance coverage in certain regions further impacts affordability

• Consumer and healthcare awareness remains uneven, particularly in developing regions where diagnostic infrastructure is still evolving. Limited understanding of testing benefits and dietary management restricts adoption across certain population groups. This also leads to delayed diagnosis and underreporting of food allergies and intolerances

• Regulatory complexities and lack of standardized testing protocols also impact market growth, as variations in testing methods and certification requirements can create inconsistencies in results. Companies must ensure compliance with regulatory guidelines and maintain quality standards to build trust and reliability

• For instance, in 2024, several diagnostic providers in emerging markets reported slower adoption of advanced testing solutions due to high costs and limited awareness among consumers and healthcare professionals. Infrastructure limitations and lack of trained personnel further restricted market expansion, affecting service availability and utilization

• Overcoming these challenges will require cost-effective testing solutions, expanded healthcare infrastructure, and targeted awareness initiatives. Collaboration between governments, healthcare providers, and diagnostic companies will be essential to improve accessibility, standardize testing procedures, and support long-term market growth

Food Allergens and Intolerance Testing Market Scope

The market is segmented on the basis of testing type, method, and end user.

• By Testing Type

On the basis of testing type, the global food allergens and intolerance testing market is segmented into Allergen Testing and Intolerance Testing. The allergen testing segment held the largest market revenue share in 2025 driven by the increasing prevalence of food allergies and the growing need for accurate identification of allergenic substances. Allergen testing is widely adopted in clinical and laboratory settings due to its ability to provide reliable and standardized results, supporting effective diagnosis and management of allergic conditions. Increasing regulatory emphasis on food safety and labeling standards is further strengthening demand for allergen testing solutions. In addition, advancements in immunoassay and molecular diagnostic technologies are improving testing accuracy and efficiency. Growing collaboration between healthcare providers and diagnostic laboratories is also supporting wider adoption across developed and emerging markets.

The intolerance testing segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising consumer awareness regarding food sensitivities and digestive health. Intolerance testing is gaining popularity among individuals seeking personalized dietary solutions and preventive healthcare approaches, as it helps identify non-allergic food reactions and supports better nutritional planning. Increasing demand for at-home testing kits and digital health platforms is accelerating segment growth. Furthermore, the expansion of wellness and nutrition-focused services is encouraging the use of intolerance testing in lifestyle management. Continuous innovation in testing methods and improved accessibility are also contributing to higher adoption rates.

• By Method

On the basis of method, the market is segmented into In-Vitro and In-Vivo. The in-vitro segment held the largest market revenue share in 2025 driven by its high accuracy, safety, and convenience compared to traditional testing methods. In-vitro testing methods such as blood tests are widely preferred as they reduce the risk of allergic reactions and provide precise quantitative results, making them suitable for a wide range of patients. Increasing adoption in clinical laboratories and diagnostic centers is supporting segment dominance. In addition, technological advancements enabling faster turnaround times and automation are improving efficiency. Rising demand for non-invasive and patient-friendly diagnostic solutions is further boosting growth.

The in-vivo segment is expected to witness the fastest growth rate from 2026 to 2033, driven by its effectiveness in providing immediate and observable results through skin prick and patch tests. In-vivo testing remains an essential diagnostic approach, particularly in clinical settings, due to its ability to directly assess the body's reaction to specific allergens under controlled conditions. Growing demand for rapid diagnosis and real-time evaluation is supporting segment expansion. Furthermore, increasing use in specialized allergy clinics and hospitals is enhancing adoption. Continuous improvements in testing protocols and safety measures are also contributing to segment growth.

• By End User

On the basis of end user, the market is segmented into Allergen Testing End User and Intolerance Testing End User. The allergen testing end user segment held the largest market revenue share in 2025 driven by the high demand from hospitals, diagnostic laboratories, and clinics for allergy diagnosis and management. These end users rely on advanced testing solutions to ensure accurate detection and treatment planning for patients with allergic conditions. Increasing patient inflow and rising incidence of food allergies are further supporting demand. In addition, growing investments in healthcare infrastructure and diagnostic capabilities are strengthening segment growth. Collaboration between hospitals and research institutions is also enhancing testing accessibility and quality.

The intolerance testing end user segment is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of at-home testing kits and personalized nutrition services. Growing consumer interest in wellness and preventive healthcare is encouraging individuals to seek intolerance testing solutions, supporting expansion across direct-to-consumer channels and specialized diagnostic providers. Increasing availability of online platforms and telehealth services is improving accessibility and convenience. Furthermore, rising focus on lifestyle management and dietary optimization is driving demand. Continuous product innovation and expansion of service offerings are also contributing to the growth of this segment.

Food Allergens and Intolerance Testing Market Regional Analysis

• North America dominated the food allergens and intolerance testing market with the largest revenue share in 2025, driven by the high prevalence of food allergies and strong awareness regarding early diagnosis and preventive healthcare

• Consumers in the region highly value accurate diagnostic solutions, advanced laboratory testing, and personalized dietary management supported by reliable allergen detection methods

• This widespread adoption is further supported by well-established healthcare infrastructure, high healthcare spending, and increasing focus on food safety and labeling standards, establishing testing solutions as essential tools for both clinical and individual use

U.S. Food Allergens and Intolerance Testing Market Insight

The U.S. food allergens and intolerance testing market captured the largest revenue share in 2025 within North America, fueled by increasing cases of food allergies and strong adoption of advanced diagnostic technologies. Consumers are increasingly prioritizing early detection and effective management of food-related conditions through clinical and at-home testing solutions. The growing preference for personalized nutrition and preventive healthcare, combined with high demand for accurate and rapid testing methods, further propels the market. Moreover, the increasing integration of digital health platforms and telemedicine services is significantly contributing to market expansion.

Europe Food Allergens and Intolerance Testing Market Insight

The Europe food allergens and intolerance testing market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent food safety regulations and rising awareness regarding allergen labeling and consumer health. The increasing demand for advanced diagnostic solutions and growing adoption of preventive healthcare practices are fostering market growth. European consumers are also highly focused on food transparency and quality, encouraging the use of reliable testing methods. The region is experiencing strong growth across hospitals, diagnostic laboratories, and home testing applications.

U.K. Food Allergens and Intolerance Testing Market Insight

The U.K. food allergens and intolerance testing market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing awareness of food sensitivities and a growing focus on health and wellness. In addition, rising demand for accurate diagnosis and personalized dietary planning is encouraging individuals to adopt testing solutions. The U.K.’s strong healthcare system, combined with increasing use of at-home testing kits and digital health services, is expected to continue to stimulate market growth.

Germany Food Allergens and Intolerance Testing Market Insight

The Germany food allergens and intolerance testing market is expected to witness the fastest growth rate from 2026 to 2033, fueled by growing awareness of food allergies and increasing demand for advanced diagnostic technologies. Germany’s well-developed healthcare infrastructure and emphasis on quality and safety promote the adoption of reliable testing solutions, particularly in clinical and laboratory settings. The integration of testing services with personalized nutrition and healthcare programs is also becoming increasingly prevalent.

Asia-Pacific Food Allergens and Intolerance Testing Market Insight

The Asia-Pacific food allergens and intolerance testing market is expected to witness the fastest growth rate from 2026 to 2033, driven by increasing urbanization, rising healthcare awareness, and improving access to diagnostic services in countries such as China, Japan, and India. The region's growing focus on food safety and preventive healthcare is driving the adoption of testing solutions. Furthermore, expanding healthcare infrastructure and rising disposable incomes are making testing services more accessible to a broader population.

Japan Food Allergens and Intolerance Testing Market Insight

The Japan food allergens and intolerance testing market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced healthcare system, high awareness regarding food safety, and increasing demand for preventive diagnostics. The adoption of testing solutions is driven by the growing number of individuals seeking personalized nutrition and health management. Integration with digital healthcare technologies and increasing availability of advanced diagnostic tools are fueling growth.

China Food Allergens and Intolerance Testing Market Insight

The China food allergens and intolerance testing market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large population, increasing healthcare awareness, and rapid development of diagnostic infrastructure. China is emerging as a key market for food safety and testing solutions, with rising demand across clinical and consumer segments. The expansion of healthcare services, along with government initiatives promoting food safety and quality standards, is significantly propelling the market in China.

Food Allergens and Intolerance Testing Market Share

The Food Allergens and Intolerance Testing industry is primarily led by well-established companies, including:

• SGS SA (Switzerland)

• Agilent Technologies, Inc. (U.S.)

• NEOGEN Corporation (U.S.)

• ALS Limited (Australia)

• Mérieux NutriSciences (France)

• Eurofins Scientific (Luxembourg)

• Intertek Group plc (U.K.)

• TÜV SÜD (Germany)

• Bureau Veritas (France)

• Symbio Laboratories (Australia)

• R J Hill Laboratories Limited (New Zealand)

• NSF International (U.S.)

• Healthy Stuff Online Limited (U.K.)

• QIMA (China)

• IFP Institut Für Produktqualität GmbH (Germany)

• ADPEN Laboratories, Inc. (U.S.)

• AsureQuality (New Zealand)

• Microbac Laboratories, Inc. (U.S.)

• Romer Labs Division Holding GmbH (Austria)

• Food Safety Net Services (U.S.)

• PCAS Labs (U.S.)

• Element Materials Technology (U.K.)

• OMIC USA Inc. (U.S.)

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Food Allergens And Intolerance Testing Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Food Allergens And Intolerance Testing Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Food Allergens And Intolerance Testing Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.