Global Frontotemporal Disorders Treatment Market

Market Size in USD Million

CAGR :

%

USD

417.38 Million

USD

593.55 Million

2025

2033

USD

417.38 Million

USD

593.55 Million

2025

2033

| 2026 –2033 | |

| USD 417.38 Million | |

| USD 593.55 Million | |

| % | |

|

Frontotemporal Disorders Treatment Market Size

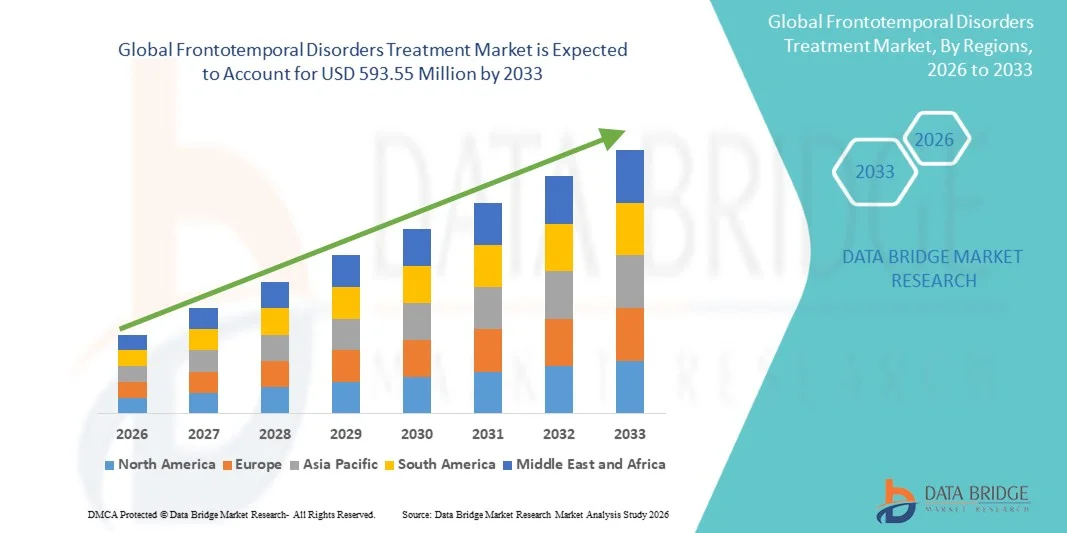

- The global frontotemporal disorders treatment market size was valued at USD 417.38 million in 2025and is expected to reach USD 593.55 million by 2033, at a CAGR of 4.50% during the forecast period

- The market growth is primarily driven by the rising prevalence of frontotemporal disorders, increasing awareness of early neurodegenerative disease diagnosis, and advancements in neurological therapeutics and supportive care approaches across clinical settings

- Furthermore, growing investment in neurodegenerative disease research, expanding clinical trials pipeline, and increasing demand for targeted symptomatic and disease-modifying therapies are supporting market expansion, thereby significantly boosting the industry's growth

Frontotemporal Disorders Treatment Market Analysis

- The frontotemporal disorders treatment market includes pharmacological therapies and supportive care approaches aimed at managing behavioral, psychological, and cognitive symptoms of progressive neurodegenerative conditions, with increasing reliance on multidisciplinary care across hospitals and specialty neurological centres

- The market growth is primarily driven by rising prevalence of frontotemporal disorders, increasing use of antidepressants (Selective Serotonin Reuptake Inhibitors and Serotonin and Noradrenaline Reuptake Inhibitors) and antipsychotics (risperidone and quetiapine) for symptom control, along with growing focus on behavioral and psychological symptom management strategies

- North America dominated the frontotemporal disorders treatment market with the largest revenue share of 38.6% in 2025, supported by advanced neurology infrastructure, strong access to specialty centres, and higher adoption of hospital-based treatment pathways for complex neurodegenerative disease management

- Asia-Pacific is expected to be the fastest growing region during the forecast period due to improving healthcare infrastructure, rising elderly population, increasing awareness of neurodegenerative diseases, and expanding availability of homecare and specialty centre-based treatment services

- Antidepressants dominated the frontotemporal disorders treatment market in 2025 with a share of 41.8% due to their widespread use in managing mood and behavioral symptoms

Report Scope and Frontotemporal Disorders Treatment Market Segmentation

|

Attributes |

Frontotemporal Disorders Treatment Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Development of disease-modifying therapies targeting tau and TDP-43 proteinopathies · Expansion of biomarker-based early diagnosis tools and companion diagnostics |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Frontotemporal Disorders Treatment Market Trends

“Expanding Precision Medicine and Neurobiological Targeting Approaches”

- A significant and accelerating trend in the global frontotemporal disorders treatment market is the growing shift toward precision medicine approaches focused on identifying underlying genetic mutations such as MAPT, GRN, and C9orf72 to enable more targeted therapeutic strategies

- For instance, ongoing clinical programs evaluating tau-targeting therapies are increasingly using biomarker-based patient selection to improve treatment specificity and clinical trial outcomes

- The integration of advanced neuroimaging and cerebrospinal fluid biomarker analysis is enabling earlier and more accurate differentiation of frontotemporal disorders from other dementias, improving diagnostic confidence and treatment planning

- Furthermore, digital cognitive assessment tools and remote behavioral monitoring platforms are being increasingly adopted to track disease progression and personalize symptom management in real time

- The growing adoption of combination approaches involving pharmacological treatment alongside behavioral and caregiver-led interventions is enhancing overall patient management outcomes across clinical settings

- Increasing collaboration between pharmaceutical companies and academic research institutes is accelerating innovation in disease-modifying drug development and expanding the therapeutic pipeline

Frontotemporal Disorders Treatment Market Dynamics

Driver

“Rising Prevalence of Neurodegenerative Disorders and Expanding Clinical Awareness”

- The increasing prevalence of frontotemporal disorders and related neurodegenerative conditions, coupled with growing clinical awareness among neurologists and primary care physicians, is a major driver for market growth

- For instance, research initiatives supported by organizations such as the National Institutes of Health are expanding global understanding of early-onset dementia patterns, improving diagnostic rates and treatment initiation

- As the global aging population increases, more patients are being identified at earlier stages, leading to higher demand for pharmacological and supportive care interventions

- Furthermore, growing availability of antidepressants and antipsychotics for off-label symptom management is supporting broader treatment adoption in both hospital and outpatient settings

- The increasing focus on multidisciplinary care involving neurologists, psychiatrists, and caregivers is further driving structured treatment pathways and improving patient management outcomes

- Expanding healthcare infrastructure and improved access to neurological services in developing regions are also accelerating diagnosis and treatment uptake across patient populations

- Rising investment in rare neurodegenerative disease research and orphan drug development programs is further strengthening the treatment landscape and accelerating innovation

- Increasing patient advocacy initiatives and caregiver support networks are improving early recognition and encouraging timely medical intervention

Restraint/Challenge

“Limited Disease-Modifying Therapies and Diagnostic Complexity”

- A key challenge in the global frontotemporal disorders treatment market is the absence of approved disease-modifying therapies, with most current treatments focused only on managing behavioral and psychological symptoms

- For instance, despite ongoing clinical trials targeting tau and TDP-43 protein aggregates, no widely approved curative treatment is currently available, limiting long-term therapeutic outcomes

- The clinical overlap of frontotemporal disorders with Alzheimer’s disease and psychiatric conditions often leads to misdiagnosis or delayed diagnosis, affecting treatment effectiveness

- Furthermore, limited awareness among general healthcare providers and lack of standardized diagnostic pathways in several regions contribute to underdiagnosis and treatment delays

- High dependence on symptomatic medications such as antidepressants and antipsychotics also raises concerns regarding long-term efficacy and patient quality of life

- Overcoming these challenges will require advancements in early diagnostic biomarkers, increased clinical awareness, and accelerated development of targeted disease-modifying therapies

- Variability in treatment response among patients due to heterogeneous disease progression further complicates the development of standardized therapeutic protocols

Frontotemporal Disorders Treatment Market Scope

The market is segmented on the basis of drug class, treatment type, route of administration, end-users, and distribution channel.

- By Drug Class

On the basis of drug class, the market is segmented into antidepressants (Selective Serotonin Reuptake Inhibitors, Serotonin and Noradrenaline Reuptake Inhibitors), antipsychotics (risperidone, quetiapine), and others. The antidepressants segment dominated the market with the largest revenue share of 41.8% in 2025, driven by their widespread use in managing behavioral and emotional symptoms such as depression, irritability, and compulsive behaviors associated with frontotemporal disorders. These drugs are frequently prescribed as first-line therapy due to their relatively favorable safety profile and ease of oral administration. Increasing clinical preference for SSRIs and SNRIs in symptom management across both early and mid-stage disease patients further strengthens segment dominance. Moreover, their availability across hospital and retail pharmacies ensures consistent accessibility for long-term treatment.

The antipsychotics segment is anticipated to witness the fastest growth rate of 9.6% from 2026 to 2033, fueled by rising use of agents such as risperidone and quetiapine for severe behavioral disturbances including agitation, aggression, and psychosis-like symptoms. These medications are increasingly adopted in specialty neurological centres and hospitals for managing complex cases where antidepressants alone are insufficient. Growing clinical awareness regarding behavioral stabilization in advanced disease stages is further accelerating demand. In addition, ongoing research into optimized dosing strategies is expanding their safe use in elderly populations. The increasing burden of severe neuropsychiatric symptoms is also contributing to faster uptake of antipsychotic-based regimens.

- By Treatment

On the basis of treatment, the market is segmented into behavioral symptoms management and psychological symptoms management. The behavioral symptoms management segment dominated the market with a revenue share of 58.3% in 2025, driven by the high prevalence of behavioral abnormalities such as disinhibition, compulsive actions, and social inappropriateness in frontotemporal disorders. Clinicians prioritize behavioral stabilization as the first step in patient care due to its direct impact on caregiver burden and patient safety. Pharmacological interventions combined with structured behavioral therapies are widely adopted across hospitals and specialty centres. Increasing use of caregiver-guided behavioral interventions and supportive care programs further strengthens this segment.

The psychological symptoms management segment is expected to witness the fastest growth rate of 10.2% from 2026 to 2033, driven by increasing recognition of anxiety, depression, and mood-related disturbances in patients. Rising integration of psychiatric evaluation within neurology care pathways is improving diagnosis and treatment of psychological symptoms. Expanding use of antidepressants and counseling-based interventions is supporting segment growth. In addition, growing adoption of multidisciplinary care models involving psychiatrists and psychologists is enhancing treatment effectiveness. Increasing awareness among caregivers about emotional and cognitive health is further accelerating demand.

- By Route of Administration

On the basis of route of administration, the market is segmented into oral and parenteral. The oral segment dominated the market with the largest revenue share of 67.5% in 2025, driven by its convenience, patient compliance, and suitability for long-term outpatient and homecare management. Most antidepressants and antipsychotics used in frontotemporal disorders are formulated for oral administration, making it the standard mode of treatment delivery. Oral medications allow easier dosage adjustments and are preferred for chronic symptom management in elderly patients. The widespread availability of oral formulations across pharmacies further supports dominance.

The parenteral segment is anticipated to witness the fastest growth rate of 8.8% from 2026 to 2033, fueled by increasing use in hospital settings for acute behavioral crises requiring rapid symptom control. Injectable formulations are preferred in severe cases where oral administration is not feasible or effective. Growing adoption of short-acting injectable antipsychotics in emergency neurological care is driving segment expansion. Hospitals and specialty centres are increasingly integrating parenteral therapies into acute management protocols. Rising focus on controlled and supervised treatment environments is further supporting growth.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty centres, and others. The hospitals segment dominated the market with a revenue share of 46.9% in 2025, driven by the availability of advanced diagnostic facilities, multidisciplinary care teams, and access to acute neuropsychiatric management. Hospitals remain the primary treatment setting for newly diagnosed and severe cases requiring close monitoring and medication adjustment. Strong infrastructure for neurological evaluation and psychiatric consultation further reinforces hospital dominance. Increasing hospital admissions for dementia-related behavioral complications also supports segment growth.

The homecare segment is expected to witness the fastest growth rate of 11.4% from 2026 to 2033, driven by rising preference for long-term, cost-effective, and patient-centric care outside hospital settings. Increasing availability of caregiver training programs and telehealth support is enabling better home-based disease management. Growing adoption of oral medications suitable for outpatient use further supports this trend. Families are increasingly opting for homecare due to reduced hospitalization costs and improved patient comfort. Expansion of remote monitoring technologies is also accelerating growth in this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with a revenue share of 52.1% in 2025, driven by high prescription volumes for newly diagnosed patients and acute care settings. Hospital pharmacies ensure controlled dispensing of antidepressants and antipsychotics under specialist supervision. Strong integration with inpatient and outpatient neurology departments supports sustained demand. In addition, hospitals remain the primary source of initial diagnosis and treatment initiation.

The online pharmacy segment is expected to witness the fastest growth rate of 12.6% from 2026 to 2033, driven by increasing digital health adoption and rising demand for convenient medication access. Expanding telemedicine consultations are directly boosting e-prescription fulfillment through online channels. Caregivers of chronic patients increasingly prefer home delivery of medications for long-term treatment adherence. Growing penetration of e-pharmacy platforms in urban and semi-urban regions is further accelerating growth. Improved regulatory support for digital pharmaceutical distribution is also strengthening this segment.

Frontotemporal Disorders Treatment Market Regional Analysis

- North America dominated the frontotemporal disorders treatment market with the largest revenue share of 38.6% in 2025, supported by advanced neurology infrastructure, strong access to specialty centres, and higher adoption of hospital-based treatment pathways for complex neurodegenerative disease management

- Patients and healthcare providers in the region benefit from strong access to specialty neurology centres, multidisciplinary care pathways, and wider availability of pharmacological therapies for symptom management

- This widespread adoption is further supported by high healthcare expenditure, strong research funding in neurodegenerative diseases, and increasing clinical awareness of early-onset dementia conditions, establishing structured treatment adoption across hospitals and specialty clinics

U.S. Frontotemporal Disorders Treatment Market Insight

The U.S. frontotemporal disorders treatment market captured the largest revenue share of 79% in 2025 within North America, driven by advanced neurological care infrastructure and high diagnosis rates of rare neurodegenerative diseases. Patients benefit from strong access to specialized memory clinics, neurologists, and multidisciplinary treatment pathways focused on symptom management. The growing use of antidepressants and antipsychotics for behavioral stabilization, along with strong clinical trial activity in disease-modifying therapies, further supports market expansion. Moreover, increasing research funding from public and private organizations and rising awareness of early-onset dementia are significantly contributing to market growth.

Europe Frontotemporal Disorders Treatment Market Insight

The Europe frontotemporal disorders treatment market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by improving neurological care access and increasing focus on early dementia diagnosis. The region benefits from structured healthcare systems and growing integration of psychiatric and neurological services for better disease management. Rising prevalence of aging populations and increasing awareness of behavioral and cognitive disorders are fostering demand for long-term treatment solutions. In addition, supportive healthcare policies and expanding research initiatives in neurodegenerative diseases are contributing to regional market growth.

U.K. Frontotemporal Disorders Treatment Market Insight

The U.K. frontotemporal disorders treatment market is anticipated to grow at a notable CAGR during the forecast period, driven by increasing recognition of rare dementia conditions and expanding access to specialist neurology services. The National Health Service (NHS) plays a key role in improving diagnosis and structured treatment pathways for affected patients. Growing emphasis on caregiver support programs and mental health integration is further enhancing disease management approaches. In addition, rising clinical research participation and adoption of pharmacological therapies for symptom control are supporting market development.

Germany Frontotemporal Disorders Treatment Market Insight

The Germany frontotemporal disorders treatment market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure and increasing awareness of neurodegenerative diseases. Germany’s emphasis on advanced diagnostic technologies, including neuroimaging and genetic testing, is improving early detection rates. The country’s focus on precision medicine and clinical research in dementia-related disorders is also strengthening treatment innovation. Moreover, growing adoption of structured hospital-based neurological care and supportive outpatient therapies is contributing to steady market growth.

Asia-Pacific Frontotemporal Disorders Treatment Market Insight

The Asia-Pacific frontotemporal disorders treatment market is poised to grow at the fastest CAGR of 12.8% during the forecast period of 2026 to 2033, driven by rising geriatric population and improving neurological healthcare access. Increasing awareness of neurodegenerative disorders and expanding availability of psychiatric and neurological services are accelerating diagnosis rates. Government initiatives supporting healthcare digitalization and hospital infrastructure development are further boosting treatment adoption. In addition, growing affordability of generic antidepressants and expanding specialty care centres are contributing to wider market penetration across the region.

Japan Frontotemporal Disorders Treatment Market Insight

The Japan frontotemporal disorders treatment market is gaining momentum due to its rapidly aging population and high healthcare awareness. The country’s advanced neurological care system supports early diagnosis and structured long-term management of dementia-related disorders. Increasing integration of behavioral therapy with pharmacological treatment is improving patient outcomes. Moreover, strong adoption of hospital-based specialty care and ongoing research in neurodegenerative diseases are further driving market growth.

India Frontotemporal Disorders Treatment Market Insight

The India frontotemporal disorders treatment market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to its large aging population, improving healthcare infrastructure, and growing awareness of neurological disorders. Increasing access to affordable antidepressants and antipsychotics is supporting wider treatment adoption across urban and semi-urban regions. Expansion of specialty neurology centres and rising hospital capacity are improving diagnosis rates. In addition, government initiatives focused on healthcare modernization and growing mental health awareness are key factors propelling market growth.

Frontotemporal Disorders Treatment Market Share

The Frontotemporal Disorders Treatment industry is primarily led by well-established companies, including:

- Alector, Inc. (U.S.)

- Passage Bio, Inc. (U.S.)

- Denali Therapeutics Inc. (U.S.)

- Biogen Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Eli Lilly and Company (U.S.)

- Novartis AG (Switzerland)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Lundbeck A/S (Denmark)

- Ionis Pharmaceuticals, Inc. (U.S.)

- AC Immune SA (Switzerland)

- Prilenia Therapeutics B.V. (Netherlands)

- AstraZeneca (U.K.)

- GSK plc (U.K.)

- Oryzon Genomics S.A. (Spain)

- Athira Pharma, Inc. (U.S.)

- Prevail Therapeutics (U.S.)

What are the Recent Developments in Global Frontotemporal Disorders Treatment Market?

- In March 2026, AviadoBio announced expansion of its Phase 1/2 ASPIRE-FTD clinical trial evaluating AVB-101 gene therapy for frontotemporal dementia caused by GRN mutations, extending enrollment across multiple international sites including the U.S., Canada, and several European countries. The trial expansion included advancement into a fourth dose-escalation cohort, reflecting continued progress in evaluating safety and biomarker response

- In April 2026, Passage Bio announced updated interim results from its Phase 1/2 upliFT-D clinical trial evaluating PBFT02 gene therapy for frontotemporal dementia caused by GRN mutations. The study reported biomarker improvements, including reductions in neurofilament light chain levels, suggesting decreased neurodegeneration activity in treated patients. The therapy is designed to restore progranulin expression in the brain using a one-time gene delivery approach. This development highlights growing progress in gene-based disease-modifying therapies for frontotemporal disorders

- In June 2025, AviadoBio advanced its ASPIRE-FTD clinical program evaluating AVB-101, a gene therapy designed for frontotemporal dementia associated with GRN mutations. The therapy uses an adeno-associated virus (AAV) vector to deliver a functional GRN gene directly into the central nervous system. Early clinical progress included expanded dosing across multiple international trial sites. The treatment aims to restore progranulin levels and slow disease progression in affected patients. This development underscores increasing momentum in gene therapy approaches for rare neurodegenerative diseases

- In March 2025, Alector Inc. completed key progress in its Phase 3 INFRONT-3 clinical trial evaluating latozinemab (AL001) for frontotemporal dementia caused by GRN mutations. The monoclonal antibody therapy is designed to increase progranulin levels by blocking sortilin-mediated degradation pathways. The trial represents one of the most advanced late-stage studies in FTD biologics development. While full regulatory outcomes are pending, the completion of late-stage evaluation marks a major milestone for disease-modifying biologics in neurodegeneration

- In August 2024, Passage Bio expanded its upliFT-D Phase 1/2 clinical trial evaluating PBFT02 gene therapy for GRN-associated frontotemporal dementia. The study included additional international sites across the United States and Europe to support broader patient enrollment. Early clinical observations showed sustained increases in cerebrospinal fluid progranulin levels following treatment. The therapy aims to restore missing progranulin protein to slow neurodegeneration. This expansion represents one of the earliest large-scale gene therapy efforts in FTD

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.