Global Functional Water Market

Market Size in USD Billion

CAGR :

%

USD

17.98 Billion

USD

31.21 Billion

2025

2033

USD

17.98 Billion

USD

31.21 Billion

2025

2033

| 2026 –2033 | |

| USD 17.98 Billion | |

| USD 31.21 Billion | |

| % | |

|

Functional Water Market Size

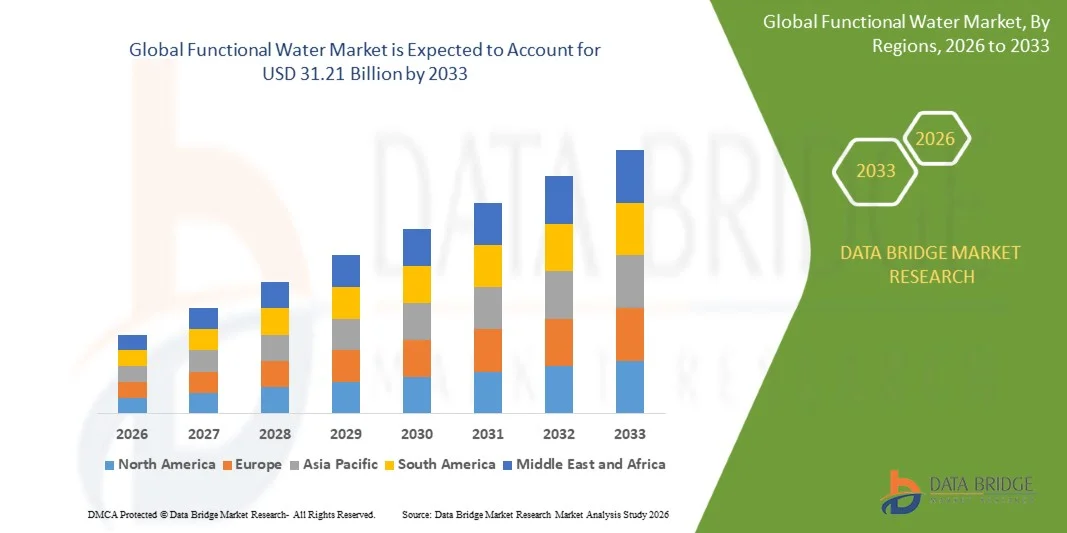

- The global functional water market size was valued at USD 17.98 billion in 2025 and is expected to reach USD 31.21 billion by 2033, at a CAGR of 7.14% during the forecast period

- The market growth is largely fueled by increasing consumer focus on health, hydration, and wellness, which is driving demand for beverages enriched with vitamins, minerals, electrolytes, and functional ingredients, leading to a shift from traditional sugary drinks toward healthier alternatives

- Furthermore, rising awareness regarding lifestyle-related conditions and the growing preference for convenient, on-the-go nutrition solutions is positioning functional water as a preferred beverage choice. These converging factors are accelerating product innovation and market penetration, thereby significantly boosting the industry's growth

Functional Water Market Analysis

- Functional water refers to enhanced water products infused with additional ingredients such as vitamins, minerals, herbs, antioxidants, or electrolytes designed to provide specific health benefits beyond basic hydration. These beverages cater to consumers seeking improved energy, immunity, digestion, and overall wellness through daily hydration

- The escalating demand for functional water is primarily fueled by increasing health consciousness, a shift away from carbonated soft drinks, and the rising popularity of fitness-oriented lifestyles, which is encouraging consumers to adopt beverages that support both hydration and functional health benefits

- North America dominated the functional water market with a share of 51.72% in 2025, due to strong consumer awareness regarding health, hydration, and wellness-focused beverages, along with increasing demand for low-calorie and nutrient-enhanced drinks

- Asia-Pacific is expected to be the fastest growing region in the functional water market during the forecast period due to rapid urbanization, rising disposable incomes, and increasing awareness of health and wellness

- PET Bottle segment dominated the market with a market share of 85.62% in 2025, due to its convenience, lightweight nature, and widespread availability across retail channels. Consumers prefer PET bottles for their portability and resealability, making them suitable for on-the-go consumption in daily routines. The cost-effectiveness of PET packaging also enables manufacturers to offer products at competitive pricing, supporting higher sales volumes

Report Scope and Functional Water Market Segmentation

|

Attributes |

Functional Water Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Functional Water Market Trends

“Growing Popularity of Clean-Label and Natural Functional Beverages”

- A significant trend in the functional water market is the increasing consumer preference for clean-label and naturally sourced beverages, driven by heightened awareness of ingredient transparency and health-conscious consumption patterns. This shift is encouraging manufacturers to develop vitamin and mineral enriched water products with minimal additives and recognizable ingredients, strengthening consumer trust and brand loyalty

- For instance, Danone S.A. has expanded its portfolio with naturally sourced mineral and functional water offerings under brands such as Evian and Volvic, focusing on purity and added nutritional benefits. These products cater to consumers seeking hydration solutions that align with clean-label expectations and natural wellness positioning

- The demand for plant-based and naturally derived ingredients in functional beverages is gaining traction as consumers prioritize products free from artificial sweeteners, colors, and preservatives. This is reshaping formulation strategies and encouraging the use of botanical extracts and naturally occurring minerals in functional water products

- Brands are increasingly emphasizing transparency in labeling and sourcing practices, which is influencing purchasing decisions and strengthening brand differentiation in a competitive market. This trend is also driving certifications and claims related to organic, non-GMO, and sustainable sourcing practices

- The shift toward natural functional beverages is further supported by rising environmental awareness, prompting companies to adopt sustainable packaging and responsible sourcing methods. This is reinforcing the alignment between product benefits and broader consumer values related to health and sustainability

- The growing inclination toward clean-label and natural formulations is significantly shaping product innovation and marketing strategies in the functional water market. This trend is expected to continue driving demand for vitamin and mineral enriched water solutions that offer both health benefits and ingredient transparency

Functional Water Market Dynamics

Driver

“Rising Demand for Convenient and On-the-Go Hydration Solutions”

- The increasing demand for convenient hydration options is a major driver in the functional water market, supported by fast-paced lifestyles and the need for portable, ready-to-consume beverages. Consumers are actively seeking vitamin and mineral enriched water products that provide both hydration and added health benefits without compromising convenience

- For instance, PepsiCo, Inc. has introduced functional hydration products under brands such as Propel, offering electrolyte-enhanced water in portable formats designed for active and on-the-go consumers. These offerings address the need for quick hydration solutions while delivering essential nutrients for performance and recovery

- The growing urban population and busy work routines are driving higher consumption of packaged functional beverages that can be easily carried and consumed throughout the day. This is increasing demand for single-serve bottles and innovative packaging formats that enhance portability and usability

- The rise of fitness and wellness trends is further boosting demand for functional water products that support hydration during workouts, travel, and daily activities. Consumers are prioritizing beverages that combine convenience with functional benefits such as energy support and electrolyte replenishment

- The sustained demand for convenient, health-oriented hydration solutions continues to strengthen this driver in the functional water market. The need for easily accessible and nutrient-enriched beverages is significantly influencing product development and driving overall market expansion

Restraint/Challenge

“Stringent Regulatory Requirements for Functional Claims and Ingredients”

- The functional water market faces challenges due to strict regulatory frameworks governing health claims, ingredient usage, and labeling standards, which vary across regions and require compliance with multiple authorities. These regulations increase complexity for manufacturers aiming to market vitamin and mineral enriched water with specific health benefits

- For instance, European Food Safety Authority enforces stringent guidelines on health claims and ingredient approvals, requiring companies to provide scientific evidence to support functional benefits. Compliance with such regulations can delay product launches and increase costs associated with testing and certification

- The requirement for clear and accurate labeling limits the extent to which brands can promote functional benefits, affecting marketing strategies and consumer communication. Companies must ensure that all claims are substantiated and aligned with regulatory standards to avoid penalties and reputational risks

- Variations in regulatory standards across different countries create additional challenges for global market players, as products may need reformulation or relabeling to meet local requirements. This adds complexity to international expansion and supply chain management

- The ongoing evolution of regulatory frameworks continues to pose challenges for the functional water market. Companies must continuously adapt to changing requirements while maintaining product innovation and ensuring compliance with global standards to sustain growth

Functional Water Market Scope

The market is segmented on the basis of product type, packaging, flavor, and distribution channel.

•By Product Type

On the basis of product type, the functional water market is segmented into vitamin-fortified, protein, electrolyte/mineral, and others. The vitamin-fortified segment dominated the largest market revenue share in 2025, driven by growing consumer inclination toward beverages that offer added health benefits such as immunity support, energy enhancement, and improved metabolism. Consumers increasingly prefer convenient nutrition sources, and vitamin-infused water provides an easy alternative to traditional supplements without compromising on taste or hydration. The rising focus on preventive healthcare and wellness lifestyles has further strengthened demand for vitamin-fortified variants across urban populations. In addition, continuous product innovation with diverse vitamin blends and clean-label positioning is enhancing consumer trust and adoption.

The protein segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising popularity of fitness-focused lifestyles and increasing demand for protein-enriched hydration solutions. Consumers engaged in sports and active routines are seeking beverages that support muscle recovery and sustained energy, making protein-based functional water a preferred choice. The segment is also benefiting from the expansion of plant-based protein formulations, catering to vegan and health-conscious consumers. Moreover, advancements in formulation technologies are improving taste and solubility, encouraging wider consumption beyond niche fitness groups.

•By Packaging

On the basis of packaging, the functional water market is segmented into PET bottle, can, and others. The PET bottle segment dominated the largest market revenue share of 85.62% in 2025, driven by its convenience, lightweight nature, and widespread availability across retail channels. Consumers prefer PET bottles for their portability and resealability, making them suitable for on-the-go consumption in daily routines. The cost-effectiveness of PET packaging also enables manufacturers to offer products at competitive pricing, supporting higher sales volumes. In addition, strong distribution networks and compatibility with various bottle sizes further reinforce the dominance of this segment.

The can segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for sustainable and recyclable packaging solutions. Consumers are becoming more environmentally conscious, driving preference toward aluminum cans due to their higher recycling rates and reduced environmental impact. The premium appeal and modern branding opportunities offered by cans are also attracting younger consumers. Furthermore, improved shelf stability and enhanced product preservation capabilities are supporting the adoption of canned functional water across multiple markets.

•By Flavor

On the basis of flavor, the functional water market is segmented into flavored and non-flavored. The flavored segment dominated the largest market revenue share in 2025, driven by strong consumer demand for enhanced taste combined with functional benefits. Flavored functional water offers a refreshing alternative to sugary beverages while delivering added nutrients, making it highly appealing to a broad consumer base. The availability of a wide variety of natural and exotic flavors is further attracting consumers seeking diverse taste experiences. In addition, product innovations focusing on low-calorie and natural sweeteners are supporting sustained growth in this segment.

The non-flavored segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing preference for clean-label and minimally processed beverages. Health-conscious consumers are gravitating toward simple hydration options without added flavors or sweeteners, aligning with natural wellness trends. The segment is also benefiting from growing awareness regarding ingredient transparency and reduced sugar intake. Moreover, the rising demand for functional hydration among consumers seeking purity and simplicity is driving the expansion of non-flavored functional water.

•By Distribution Channel

On the basis of distribution channel, the functional water market is segmented into supermarkets/hypermarkets, convenience/grocery stores, online retail stores, and other distribution channels. The supermarkets/hypermarkets segment dominated the largest market revenue share in 2025, driven by extensive product availability, strong brand visibility, and the ability for consumers to compare multiple options in a single location. These retail formats offer promotional pricing and bulk purchasing options, encouraging higher consumer spending. The presence of organized retail infrastructure and increasing footfall further contribute to the dominance of this segment. In addition, strategic shelf placement and in-store marketing activities enhance product exposure and sales.

The online retail stores segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rapid expansion of e-commerce platforms and changing consumer purchasing behavior. Consumers increasingly prefer the convenience of home delivery, subscription models, and access to a wider range of niche and premium products through online channels. Digital platforms also enable brands to engage directly with consumers and offer personalized recommendations. Furthermore, growing internet penetration and digital payment adoption are accelerating the shift toward online purchasing of functional water products.

Functional Water Market Regional Analysis

- North America dominated the functional water market with the largest revenue share of 51.72% in 2025, driven by strong consumer awareness regarding health, hydration, and wellness-focused beverages, along with increasing demand for low-calorie and nutrient-enhanced drinks

- Consumers in the region highly value functional benefits such as energy boost, immunity support, and electrolyte balance, encouraging the adoption of vitamin-infused and performance-based water products

- This widespread adoption is further supported by high disposable incomes, a well-established retail network, and continuous product innovation, establishing functional water as a preferred alternative to sugary beverages across diverse consumer groups

U.S. Functional Water Market Insight

The U.S. functional water market captured the largest revenue share within North America in 2025, fueled by the growing shift toward healthier beverage choices and increasing demand for clean-label products. Consumers are actively replacing carbonated and high-sugar drinks with functional water that offers added nutritional value and convenience. The strong presence of leading beverage companies, combined with aggressive marketing strategies and continuous product launches, is further driving market expansion. Moreover, rising fitness trends and demand for on-the-go hydration solutions are significantly contributing to the growth of the market.

Europe Functional Water Market Insight

The Europe functional water market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing health consciousness and stringent regulations promoting low-sugar beverage consumption. The rise in demand for natural and fortified drinks, along with growing awareness regarding hydration and wellness, is accelerating market growth. Consumers in the region are increasingly inclined toward clean-label and sustainably packaged products. The expansion of retail channels and rising adoption of functional beverages across urban populations are further supporting the market.

U.K. Functional Water Market Insight

The U.K. functional water market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing demand for healthier alternatives to traditional soft drinks and rising consumer focus on fitness and wellness. The growing popularity of flavored and vitamin-enhanced water products is supporting market expansion. In addition, the strong presence of organized retail and e-commerce platforms is enhancing product accessibility. Consumer preference for convenient, ready-to-drink beverages is further contributing to the growth of the market.

Germany Functional Water Market Insight

The Germany functional water market is expected to expand at a considerable CAGR during the forecast period, fueled by rising demand for premium and functional beverages combined with increasing awareness regarding nutrition and hydration. The country’s strong inclination toward health-conscious consumption and high-quality products is supporting the adoption of functional water. The presence of advanced beverage manufacturing infrastructure and emphasis on sustainable packaging solutions are further driving growth. Increasing product innovation and availability across retail stores are also contributing to market expansion.

Asia-Pacific Functional Water Market Insight

The Asia-Pacific functional water market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid urbanization, rising disposable incomes, and increasing awareness of health and wellness. The region's expanding middle-class population and changing lifestyle patterns are encouraging the consumption of fortified and functional beverages. Growing investments by global and regional players, along with expanding distribution networks, are accelerating market growth. Furthermore, increasing demand for convenient and affordable hydration solutions is strengthening market penetration across emerging economies.

Japan Functional Water Market Insight

The Japan functional water market is gaining momentum due to the country’s strong focus on health, innovation, and convenience-driven consumption patterns. Consumers show a high preference for functional beverages that offer specific health benefits such as improved digestion and energy support. The presence of technologically advanced beverage formulations and continuous product innovation is supporting market growth. Moreover, the demand for compact and convenient packaging formats is contributing to increased adoption across urban consumers.

China Functional Water Market Insight

The China functional water market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large population base, rapid urbanization, and increasing adoption of health-oriented beverages. The rising middle-class population and growing awareness regarding fitness and wellness are driving demand for functional water products. The strong presence of domestic manufacturers and expanding retail infrastructure are enhancing product availability. In addition, increasing investments in product innovation and marketing strategies are further propelling the growth of the market.

Functional Water Market Share

The functional water industry is primarily led by well-established companies, including:

- Voss Water (Norway)

- PepsiCo, Inc. (U.S.)

- Flow Beverage Corp. (Canada)

- Danone S.A. (France)

- Good Idea Inc. (Sweden)

- The Coca-Cola Company (U.S.)

- Nooma Inc. (U.S.)

- Nestlé S.A. (Switzerland)

- Centr Brands Corp. (Canada)

- Hint Inc. (U.S.)

- Vitamin Well (Sweden)

- The Vita Coco Company (U.S.)

- Disruptive Beverages Inc. (U.S.)

- Balance Water Company LLC (U.S.)

- The Wonderful Company LLC (U.S.)

- Perfect Hydration (U.S.)

- CENTR Brands Corp. (Canada)

- Nirvana Water Sciences Corp. (U.S.)

- Function Drinks (U.S.)

- Dr Pepper Snapple Group (U.S.)

Latest Developments in Global Functional Water Market

- In April 2025, Powerade expanded into the functional water segment with the launch of Power Water, a zero-sugar, electrolyte-enhanced flavored water designed for active consumers, which is strengthening competition in the hydration category and accelerating the shift toward performance-oriented, low-calorie beverages. This development is reinforcing the convergence between sports drinks and functional water, encouraging other brands to innovate in electrolyte-based hydration while expanding consumer adoption across fitness and lifestyle segments

- In April 2025, Wet Hydration introduced Build, a kiwi passionfruit-flavored protein water, along with new canned still and sparkling water variants, which is broadening product diversification and addressing the rising demand for protein-infused hydration solutions. This expansion is supporting market growth by targeting niche consumer groups such as athletes and wellness-focused individuals, while also driving innovation in functional formulations and packaging formats

- In March 2025, Rubicon Spring Vits launched its vitamin-enriched functional water in flavors including Black Cherry Pomegranate, Mango Passion, and Strawberry Watermelon, which is enhancing product appeal through low-calorie, nutrient-rich offerings aligned with health-conscious consumption trends. This development is contributing to increased market penetration by combining taste, functionality, and compliance with nutritional standards, thereby strengthening consumer trust and encouraging repeat purchases

- In January 2025, Nestlé expanded its vitamin and mineral enriched water portfolio across select markets, which is intensifying competition and reinforcing the role of multinational players in shaping market dynamics. This move is accelerating innovation and product standardization in fortified beverages while improving global accessibility and driving premiumization within the functional water segment

- In April 2024, Agua Plus expanded its product line by introducing four new functional beverages in multiple packaging sizes, which is enhancing availability and catering to diverse consumer preferences across different consumption occasions. This expansion is supporting broader market reach by improving shelf presence in retail channels and encouraging higher consumption through convenient packaging and variety-driven offerings

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Functional Water Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Functional Water Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Functional Water Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.