Global Game Engines And Development Software Market

Market Size in USD Billion

CAGR :

%

USD

3.12 Billion

USD

6.30 Billion

2025

2033

USD

3.12 Billion

USD

6.30 Billion

2025

2033

| 2026 –2033 | |

| USD 3.12 Billion | |

| USD 6.30 Billion | |

| % | |

|

Game Engines and Development Software Market Size

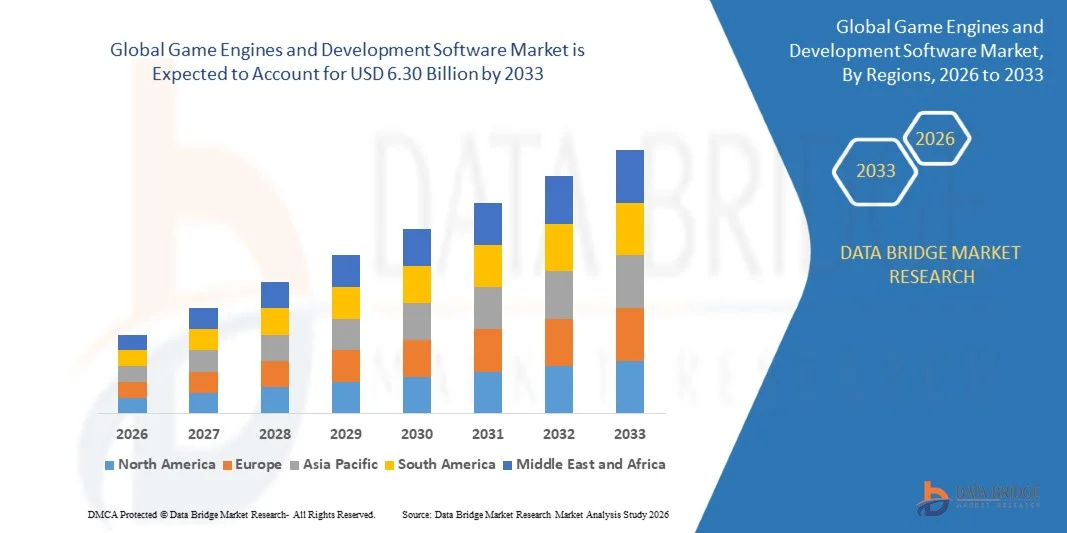

- The global game engines and development software market size was valued at USD 3.12 billion in 2025 and is expected to reach USD 6.30 billion by 2033, at a CAGR of 9.20% during the forecast period

- The market growth is largely fueled by the rapid expansion of real-time 3D content creation, increasing adoption of immersive technologies such as AR, VR, and metaverse platforms, and continuous advancements in graphics rendering and simulation capabilities within game engines and development software

- Furthermore, rising demand for cross-platform game development, cloud-based collaboration tools, and AI-assisted coding and asset generation is transforming production pipelines, enabling faster development cycles and higher-quality interactive experiences, thereby significantly accelerating industry growth

Game Engines and Development Software Market Analysis

- Game engines and development software, which enable the creation, rendering, and deployment of interactive digital content across gaming, simulation, and visualization applications, have become central to modern digital production ecosystems due to their ability to support scalable, real-time, and cross-platform development workflows

- The escalating demand for these platforms is primarily driven by the global growth of the gaming industry, increasing adoption of cloud gaming infrastructure, and rising integration of advanced technologies such as artificial intelligence, machine learning, and real-time physics simulation in game development processes

- North America dominated the game engines and development software market with a share of1% in 2025, due to strong presence of major game development studios, advanced digital infrastructure, and early adoption of real-time 3D technologies

- Asia-Pacific is expected to be the fastest growing region in the game engines and development software market during the forecast period due to rapid digitalization, expanding gaming populations, and strong mobile gaming penetration across China, India, Japan, and South Korea

- 3D game engines segment dominated the market with a market share of 58.9% in 2025, due to its extensive use in high-end gaming, console titles, and immersive PC experiences. These engines provide advanced rendering capabilities, realistic physics simulation, and high-quality visual effects that are essential for modern AAA game development. Strong adoption by major studios and continuous technological upgrades in graphics processing further strengthen its leading position

Report Scope and Game Engines and Development Software Market Segmentation

|

Attributes |

Game Engines and Development Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· CRYTEK (Germany) · SplitmediaLabs, Ltd. (Hong Kong) · Scirra Ltd. (U.K.) · ZENIMAX MEDIA INC. (U.S.) · Microsoft (U.S.) · Amazon Web Services, Inc (U.S.) · Blender Foundation (Netherlands) · Unity Technologies (U.S.) · Cocos2d (China) · YoYo Games Ltd. (U.K.) · Leadwerks Software (U.S.) · GameSalad Inc. (U.S.) · Corona Labs Inc (U.S.) · Silicon Studio Corp (Japan) · GarageGames (U.S.) · Audiokinetic Inc. (Canada) · Autodesk Inc. (U.S.) · Epic Games, Inc. (U.S.) · NVIDIA Corporation (U.S.) · Playtech plc (Isle of Man) · The Game Creators Ltd. (U.K.) |

|

Market Opportunities |

· Expansion of Cloud-Based Game Development and Streaming Ecosystems · Growing Adoption of Game Engines in Non-Gaming Industries such as Simulation and Virtual Production |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Game Engines and Development Software Market Trends

“Increasing Integration of Artificial Intelligence in Game Development”

- A significant trend in the game engines and development software market is the increasing integration of artificial intelligence into development pipelines, enabling automated asset creation, intelligent NPC behavior, and real-time content generation. This integration is reshaping traditional game production workflows by reducing manual effort and accelerating development cycles across studios of all sizes

- For instance, Epic Games has integrated AI-driven tools within Unreal Engine workflows through partnerships such as Inworld AI to enable dynamic non-player character behavior and adaptive dialogue systems. These capabilities enhance immersion and reduce scripting complexity for developers working on narrative-driven games and simulation environments

- The adoption of AI-assisted procedural generation is expanding rapidly as engines incorporate tools for terrain creation, animation synthesis, and environment design. This is enabling studios to scale content production efficiently while maintaining visual and gameplay consistency across large open-world projects

- AI-driven optimization tools are also being embedded into Unity Technologies’ development ecosystem, supporting performance tuning, automated debugging, and asset optimization. This is improving development efficiency and allowing creators to focus more on design and gameplay innovation rather than repetitive technical adjustments

- The integration of machine learning models into development engines is strengthening real-time decision-making systems used in gaming environments, including adaptive difficulty and intelligent enemy behavior. This is enhancing player engagement and improving personalization across gaming experiences

- The market is witnessing growing reliance on AI-powered content pipelines that support faster iteration and collaborative development across global teams. This increasing convergence of artificial intelligence with game engines is reinforcing efficiency, scalability, and innovation in interactive digital content creation

Game Engines and Development Software Market Dynamics

Driver

“Rising Demand for Cross-Platform and Real-Time 3D Content Creation”

- The rising demand for cross-platform compatibility and real-time 3D content creation is driving significant growth in the game engines and development software market, as developers seek unified tools that support multiple devices including PC, console, mobile, and AR/VR systems. This demand is enabling faster deployment cycles and improving accessibility across global gaming ecosystems

- For instance, Unity Technologies provides a cross-platform development environment widely used by studios such as Niantic and Tencent to deploy games across mobile and augmented reality platforms. This capability allows developers to maintain a single codebase while reaching diverse user segments efficiently

- The expansion of real-time rendering technologies such as Unreal Engine’s Nanite and Lumen systems is enhancing visual fidelity while enabling real-time scene creation. This is supporting industries beyond gaming, including film production and architectural visualization, where instant rendering feedback is critical

- The increasing popularity of cloud-based development environments is further accelerating collaboration across distributed teams working on large-scale projects. This is improving production efficiency and enabling seamless integration of assets, code, and design elements in real time

- The sustained requirement for faster development cycles and multi-platform deployment continues to reinforce this driver, positioning cross-platform real-time development as a core growth factor in the global game engines and development software market

Restraint/Challenge

“High Development Complexity and Performance Optimization Constraints”

- The game engines and development software market faces significant challenges due to the high complexity involved in developing and optimizing advanced real-time 3D applications, which require strong technical expertise and continuous performance tuning. These challenges increase development costs and limit accessibility for smaller studios and independent developers

- For instance, developers using Unreal Engine often require extensive optimization techniques to ensure smooth performance in high-fidelity environments, particularly for AAA titles developed by studios such as Ubisoft and CD Projekt Red. This increases production timelines and technical workload across development teams

- The complexity of managing large-scale assets, physics systems, and rendering pipelines creates significant strain on hardware resources, especially for real-time applications. This often forces developers to balance visual quality with performance efficiency, limiting creative flexibility

- Optimization across multiple platforms such as mobile, console, and VR adds additional layers of difficulty, as each platform has unique hardware constraints and performance requirements. This increases development fragmentation and testing complexity

- The market continues to face challenges in simplifying engine architecture while maintaining high-performance output across diverse use cases. These constraints collectively impact scalability and increase reliance on highly skilled development teams, shaping a more complex and resource-intensive industry environment

Game Engines and Development Software Market Scope

The market is segmented on the basis of type and application.

- By Type

On the basis of type, the game engines and development software market is segmented into 3D game engines, 2.5D game engines, and 2D game engines. The 3D game engines segment dominated the market with the largest share of 58.9% in 2025 due to its extensive use in high-end gaming, console titles, and immersive PC experiences. These engines provide advanced rendering capabilities, realistic physics simulation, and high-quality visual effects that are essential for modern AAA game development. Strong adoption by major studios and continuous technological upgrades in graphics processing further strengthen its leading position. Integration with VR and AR environments also enhances its relevance across next-generation gaming ecosystems. Growing demand for immersive gameplay experiences continues to reinforce the dominance of 3D engines.

The 2.5D game engines segment is expected to witness the fastest growth rate from 2026 to 2033 due to increasing demand for hybrid visual formats that combine 2D simplicity with 3D depth. These engines are widely preferred by indie developers and mobile game creators because they offer reduced development complexity while maintaining enhanced visual appeal. Rising popularity of cross-platform gaming and cost-efficient development cycles further supports their adoption. Improved accessibility of development tools and middleware solutions is encouraging small studios to experiment with 2.5D formats. Expanding mobile gaming markets and casual gaming trends continue to accelerate segment growth.

- By Application

On the basis of application, the market is segmented into game development companies, personal use, and others. The game development company segment dominated the market in 2025 due to large-scale production requirements and continuous demand for high-quality commercial games. These companies rely heavily on advanced game engines to streamline development workflows, manage large teams, and ensure consistent performance across platforms. Increasing investments in AAA game production and live-service gaming models further support segment leadership. Strong adoption of cloud-based development tools and collaborative platforms enhances efficiency in large studios. The dominance is reinforced by rising global demand for console, PC, and mobile games.

The personal use segment is expected to witness the fastest growth rate from 2026 to 2033 driven by the rise of independent developers and hobbyist creators. Increasing accessibility of no-code and low-code game development tools enables individuals to design and publish games without extensive technical expertise. Growth in online learning platforms and creator communities is encouraging more users to experiment with game development. Expanding monetization opportunities through app stores and digital distribution channels further boosts participation. Rising interest in indie gaming culture continues to accelerate adoption among individual developers.

Game Engines and Development Software Market Regional Analysis

- North America dominated the game engines and development software market with the largest revenue share of 36.1% in 2025, driven by strong presence of major game development studios, advanced digital infrastructure, and early adoption of real-time 3D technologies

- Developers in the region highly value high-performance rendering engines, cross-platform compatibility, and integrated development environments that support large-scale AAA game production

- This widespread adoption is further supported by a mature gaming ecosystem, strong investment in cloud-based development tools, and the rapid expansion of esports and interactive entertainment industries

U.S. Game Engines and Development Software Market Insight

The U.S. game engines and development software market captured the largest revenue share in North America in 2025, fueled by the presence of leading technology companies and a highly developed gaming industry. Demand is rising for advanced engines that support immersive graphics, virtual production, and real-time simulation across gaming, film, and metaverse applications. For instance, widespread usage of Unreal Engine and Unity reflects strong developer reliance on scalable and versatile platforms. The expansion of indie game development and cloud-based collaboration tools is further strengthening market growth across the country.

Europe Game Engines and Development Software Market Insight

The Europe game engines and development software market is projected to expand at a steady CAGR during the forecast period, driven by increasing investments in gaming startups and strong government support for digital innovation. Demand is rising for cost-efficient development tools that enable high-quality game creation across PC, console, and mobile platforms. The region benefits from a strong independent developer ecosystem and growing adoption of real-time rendering technologies. Growth is also supported by increasing collaboration between gaming studios and software providers across major European economies.

U.K. Game Engines and Development Software Market Insight

The U.K. game engines and development software market is expected to grow at a notable CAGR, supported by a well-established gaming industry and rising demand for interactive content development tools. Developers are increasingly adopting advanced engines for virtual production, simulation, and augmented reality applications. The presence of strong creative studios and innovation hubs is accelerating software adoption across the country. Growth is further driven by expanding esports engagement and rising demand for mobile and cloud-based gaming solutions.

Germany Game Engines and Development Software Market Insight

The Germany game engines and development software market is projected to grow at a considerable CAGR, driven by strong engineering capabilities and increasing focus on high-quality simulation and industrial gaming applications. Developers are prioritizing secure, scalable, and efficient engine platforms for both entertainment and enterprise use cases. Demand is rising for tools that support automotive simulation, training environments, and serious gaming applications. The market is further strengthened by Germany’s emphasis on digital transformation and advanced software engineering standards.

Asia-Pacific Game Engines and Development Software Market Insight

The Asia-Pacific game engines and development software market is poised to grow at the fastest CAGR during 2026 to 2033, driven by rapid digitalization, expanding gaming populations, and strong mobile gaming penetration across China, India, Japan, and South Korea. Developers are increasingly adopting cost-effective and scalable engines to support mobile-first game development and cloud-based workflows. The region also benefits from a large pool of game developers and growing investments in interactive entertainment platforms. Expansion of esports and government-led digital initiatives is further accelerating market adoption across APAC.

Japan Game Engines and Development Software Market Insight

The Japan game engines and development software market is gaining momentum due to strong technological expertise, a mature gaming culture, and high demand for visually advanced gaming experiences. Developers are increasingly integrating real-time engines for console, mobile, and animation production workflows. The market is driven by strong adoption of simulation tools and interactive storytelling platforms. Growth is further supported by the integration of game engines in robotics visualization, training systems, and entertainment content production.

China Game Engines and Development Software Market Insight

The China game engines and development software market accounted for the largest revenue share in Asia-Pacific in 2025, supported by a massive gaming population, rapid urban digitalization, and strong domestic development ecosystems. Developers are increasingly using advanced engines for mobile gaming, cloud gaming, and large-scale multiplayer platforms. The presence of strong domestic companies and continuous investment in gaming infrastructure is accelerating adoption. Government support for digital entertainment and expansion of esports ecosystems is further strengthening market growth in the country.

Game Engines and Development Software Market Share

The game engines and development software industry is primarily led by well-established companies, including:

- CRYTEK (Germany)

- SplitmediaLabs, Ltd. (Hong Kong)

- Scirra Ltd. (U.K.)

- ZENIMAX MEDIA INC. (U.S.)

- Microsoft (U.S.)

- Amazon Web Services, Inc (U.S.)

- Blender Foundation (Netherlands)

- Unity Technologies (U.S.)

- Cocos2d (China)

- YoYo Games Ltd. (U.K.)

- Leadwerks Software (U.S.)

- GameSalad Inc. (U.S.)

- Corona Labs Inc (U.S.)

- Silicon Studio Corp (Japan)

- GarageGames (U.S.)

- Audiokinetic Inc. (Canada)

- Autodesk Inc. (U.S.)

- Epic Games, Inc. (U.S.)

- NVIDIA Corporation (U.S.)

- Playtech plc (Isle of Man)

- The Game Creators Ltd. (U.K.)

Latest Developments in Global Game Engines and Development Software Market

- In October 2024, Epic Games launched Fab, a unified digital marketplace that consolidates assets, plugins, and tools for Unreal Engine workflows, significantly improving content accessibility and distribution efficiency in the game development ecosystem. This development reduced fragmentation across multiple asset stores and streamlined licensing and procurement processes for developers. It strengthened productivity by enabling faster asset discovery and integration into production pipelines, particularly for AAA and indie studios. Fab also expanded monetization opportunities for creators by increasing global visibility of digital assets, thereby reinforcing Epic Games’ ecosystem lock-in and enhancing overall platform engagement across the game engines market

- In October 2024, Unity Technologies advanced its Unity 6 preview development phase, focusing on enhanced real-time rendering performance, improved cross-platform deployment, and AI-assisted development workflows, which collectively improved efficiency in game creation pipelines. This update positively impacted developers by reducing iteration time and improving scalability across mobile, PC, and console platforms. It strengthened Unity’s competitive positioning in the mid- and light-weight game development segment by supporting faster prototyping and deployment cycles. The integration of automation and AI-driven tools further enhanced developer productivity, contributing to stronger adoption in both gaming and interactive simulation applications globally

- In August 2024, the Godot Engine 4.3 release introduced major upgrades in GPU-based rendering, animation systems, and scripting flexibility, expanding the capabilities of open-source game development tools. This development strengthened the open-source segment of the market by making high-quality game development more accessible to independent developers and small studios. Enhanced 3D tools improved visual output, enabling Godot to compete more effectively with proprietary engines in mid-scale production environments. The release reduced entry barriers for new developers by offering a powerful cost-free alternative, thereby increasing adoption in education, indie development, and experimental gaming segments worldwide

- In May 2024, Epic Games released Unreal Engine 5.4, delivering significant improvements in animation systems, rendering efficiency, and virtual production capabilities, which enhanced high-end game development workflows. This update improved the efficiency of nanite and lumen technologies, enabling developers to achieve higher visual fidelity with optimized performance. It strengthened adoption among AAA studios by accelerating content creation and reducing production complexity in large-scale environments. Beyond gaming, UE5.4 expanded its impact across film production, simulation, and architectural visualization industries, reinforcing Unreal Engine’s leadership in real-time 3D content creation markets

- In March 2024, NVIDIA showcased advancements in ACE (Avatar Cloud Engine) at GTC, integrating AI-powered digital human capabilities into game development ecosystems, which significantly influenced the evolution of interactive gaming experiences. This development enabled real-time conversational NPCs and adaptive character behaviors, enhancing immersion and storytelling in games. Its integration with major engines such as Unreal Engine accelerated the adoption of generative AI tools in development pipelines. The innovation also supported broader use cases in virtual assistants and simulation environments, marking a major shift toward AI-driven content creation within the global game engines and development software market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.