Global Hazardeous Area Sensors Market

Market Size in USD Billion

USD

4.96 Billion

USD

7.05 Billion

2025

2033

USD

4.96 Billion

USD

7.05 Billion

2025

2033

| 2026 - 2033 | |

| USD 4.96 Billion | |

| USD 7.05 Billion | |

| % | |

|

Hazardous Area Sensors Market Size

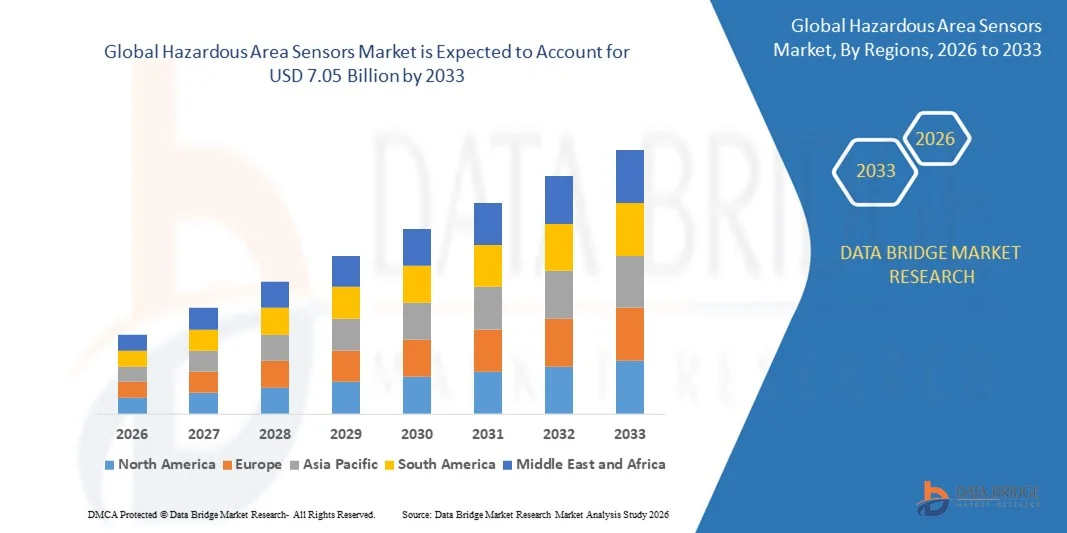

- The global hazardous area sensors market size was valued at USD 4.96 billion in 2025 and is expected to reach USD 7.05 billion by 2033, at a CAGR of 4.50% during the forecast period

- The market growth is largely fueled by increasing enforcement of industrial safety regulations and rising awareness regarding explosion risks across oil & gas, chemical, mining, and power generation industries, leading to higher deployment of intrinsically safe and explosion-proof sensing technologies in hazardous environments

- Furthermore, rapid industrial automation, expansion of petrochemical and energy infrastructure, and growing integration of IoT-enabled monitoring systems are establishing hazardous area sensors as critical components of modern process safety frameworks. These converging factors are accelerating adoption across high-risk facilities, thereby significantly boosting overall market expansion

Hazardous Area Sensors Market Analysis

- Hazardous area sensors, designed to detect gas leaks, temperature fluctuations, pressure variations, and electrical anomalies in explosive or high-risk environments, are increasingly essential for ensuring operational continuity, regulatory compliance, and worker safety across heavy industries

- The escalating demand for hazardous area sensors is primarily driven by stringent global safety standards, rising investments in smart industrial infrastructure, and the growing need for real-time monitoring and predictive maintenance solutions in hazardous process environments

- Asia-Pacific dominated the hazardous area sensors market with a share of 35.60% in 2025, due to rapid industrialization, expansion of oil & gas exploration activities, and growing investments in chemical and power generation infrastructure

- North America is expected to be the fastest growing region in the hazardous area sensors market during the forecast period due to expansion of shale gas production, petrochemical capacity additions, and modernization of industrial facilities

- Gas sensing segment dominated the market with a market share of 39.1% in 2025, due to stringent industrial safety regulations and the critical need to detect flammable and toxic gases in high-risk environments. Industries such as oil & gas, chemical, and mining prioritize gas sensors to prevent explosions, leaks, and occupational hazards

Report Scope and Hazardous Area Sensors Market Segmentation

|

Attributes |

Hazardous Area Sensors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Hazardous Area Sensors Market Trends

Integration of IoT and AI-Enabled Smart Hazardous Area Sensors

- A significant trend in the hazardous area sensors market is the integration of IoT connectivity and AI-driven analytics into explosion-proof sensing systems, driven by the need for real-time monitoring and predictive risk assessment across high-risk industrial environments. This integration is enhancing the ability of industries to detect gas leaks, temperature fluctuations, and pressure anomalies while ensuring compliance with hazardous location standards

- For instance, Honeywell International Inc. offers connected gas detection and fixed monitoring systems under its industrial safety portfolio that integrate cloud-based analytics for hazardous sites in oil and gas and chemical processing facilities. These solutions enable continuous remote diagnostics and predictive maintenance, improving operational safety and reducing unplanned shutdowns

- The adoption of AI-enabled hazardous area sensors is expanding across offshore platforms and refineries where machine learning models analyze environmental data to identify early-stage risks. This is strengthening proactive safety strategies and minimizing the likelihood of catastrophic incidents in explosive atmospheres

- Industries operating in mining and petrochemical sectors are incorporating wireless hazardous area sensors to enable centralized monitoring of distributed assets across vast facilities. This shift is reducing manual inspection requirements and improving response time during emergency situations

- The development of intrinsically safe smart sensors capable of transmitting encrypted data in real time is gaining traction as organizations focus on digital transformation initiatives within hazardous zones. This trend is reinforcing the transition toward intelligent, interconnected safety ecosystems across industrial operations

- The market is witnessing accelerated integration of IoT platforms with certified explosion-proof sensors to ensure continuous compliance, enhanced situational awareness, and optimized asset performance. This growing technological convergence is positioning smart hazardous area sensors as essential components of modern industrial risk management frameworks

Hazardous Area Sensors Market Dynamics

Driver

Stringent Industrial Safety Regulations and Compliance Mandates

- The enforcement of stringent industrial safety standards across oil and gas, chemical, and energy sectors is a major driver for hazardous area sensors, as organizations are required to deploy certified equipment in explosive and high-risk environments. Regulatory mandates ensure that monitoring systems meet rigorous performance and protection standards to safeguard personnel and infrastructure

- For instance, International Electrotechnical Commission governs IECEx certification standards that require the use of approved explosion-protected sensors in hazardous zones. Compliance with these global frameworks compels manufacturers and plant operators to invest in certified gas detection and environmental monitoring systems

- Governments and regulatory bodies are intensifying inspections and compliance audits in industries handling flammable gases and combustible dust. This is driving demand for high-reliability hazardous area sensors that provide continuous monitoring and documented safety assurance

- Industrial operators are prioritizing risk mitigation strategies to avoid penalties, operational disruptions, and reputational damage associated with non-compliance. This is strengthening investments in advanced sensing technologies that align with evolving safety directives

- The increasing emphasis on occupational safety and environmental protection continues to solidify regulatory compliance as a primary growth catalyst. This regulatory environment is sustaining long-term adoption of hazardous area sensors across multiple high-risk industries

Restraint/Challenge

High Installation and Certification Costs of Explosion-Proof Sensors

- The hazardous area sensors market faces constraints due to the high costs associated with manufacturing, installing, and certifying explosion-proof and intrinsically safe devices. These sensors require specialized enclosures, robust materials, and rigorous testing to meet hazardous location standards, increasing overall system expenditure

- For instance, Siemens AG provides explosion-proof process instrumentation designed for hazardous zones that must undergo extensive compliance testing and certification before deployment. The certification and installation processes elevate capital investment requirements for end users

- Installation in hazardous zones often demands additional protective infrastructure, certified wiring systems, and specialized labor with expertise in hazardous environment protocols. These factors increase project timelines and operational costs for industrial facilities

- Periodic maintenance and recertification requirements further add to the total cost of ownership for hazardous area sensing systems. Companies must allocate resources for inspections, calibration, and component replacement to maintain compliance

- The ongoing need to balance safety compliance with cost efficiency continues to challenge market expansion. High certification and installation expenses remain a significant barrier, influencing purchasing decisions and slowing adoption rates in cost-sensitive segments

Hazardous Area Sensors Market Scope

The market is segmented on the basis of type and application.

- By Type

On the basis of type, the hazardous area sensors market is segmented into gas sensing, pressure sensing, current sensing, voltage sensing, and temperature sensors. The gas sensing segment dominated the market with the largest market revenue share of 39.1% in 2025, driven by stringent industrial safety regulations and the critical need to detect flammable and toxic gases in high-risk environments. Industries such as oil & gas, chemical, and mining prioritize gas sensors to prevent explosions, leaks, and occupational hazards. Continuous monitoring requirements, regulatory compliance mandates, and advancements in infrared and electrochemical sensing technologies further strengthen demand. The integration of gas sensors with automated shutdown systems and industrial control platforms also enhances their adoption across hazardous locations.

The temperature sensors segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand for continuous thermal monitoring in explosive and high-temperature environments. Temperature fluctuations in hazardous zones can indicate equipment malfunction, fire risks, or chemical instability, driving the need for reliable sensing solutions. The expansion of process automation and Industry 4.0 initiatives further accelerates adoption of intrinsically safe temperature sensors. Their compatibility with wireless monitoring systems and predictive maintenance platforms enhances operational efficiency. Growing investments in smart manufacturing and remote asset monitoring contribute significantly to segment growth.

- By Application

On the basis of application, the hazardous area sensors market is segmented into power, oil & gas, mining & metal, grain storage, healthcare, chemical, pharmaceutical, waste & sewage management, fertilizer, and others. The oil & gas segment dominated the market with the largest market revenue share in 2025, driven by the inherently hazardous nature of upstream, midstream, and downstream operations. Exploration, drilling, refining, and storage activities involve exposure to flammable gases and volatile substances, necessitating advanced sensing technologies. Strict safety standards and regulatory compliance frameworks further support widespread deployment. Increasing offshore and shale exploration projects also contribute to sustained demand for explosion-proof and intrinsically safe sensors.

The chemical segment is expected to witness the fastest CAGR from 2026 to 2033, propelled by rising investments in specialty chemicals and process safety management systems. Chemical manufacturing facilities operate under high pressure and temperature conditions, creating a strong requirement for continuous hazard detection. Growing emphasis on worker safety, environmental protection, and automated plant monitoring accelerates sensor integration. Expansion of chemical production capacities in emerging economies further supports market growth. The adoption of smart hazardous area sensors integrated with centralized control systems enhances operational reliability and drives rapid segment expansion.

Hazardous Area Sensors Market Regional Analysis

- Asia-Pacific dominated the hazardous area sensors market with the largest revenue share of 35.60% in 2025, driven by rapid industrialization, expansion of oil & gas exploration activities, and growing investments in chemical and power generation infrastructure

- The region’s expanding manufacturing base, increasing enforcement of industrial safety regulations, and rising deployment of automation technologies are accelerating demand for explosion-proof and intrinsically safe sensors

- Strong presence of mining operations, rising energy consumption, and large-scale infrastructure projects across emerging economies are contributing to higher adoption of hazardous area monitoring systems

China Hazardous Area Sensors Market Insight

China held the largest share in the Asia-Pacific hazardous area sensors market in 2025, supported by its dominant position in global chemical production, coal mining, and refining industries. The country’s strong regulatory push toward industrial safety compliance and environmental monitoring is increasing adoption of advanced gas, temperature, and pressure sensors. Expansion of smart manufacturing initiatives and modernization of aging industrial plants are further enhancing demand. Large-scale infrastructure and energy projects continue to create sustained opportunities for hazardous area sensor deployment.

India Hazardous Area Sensors Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, fueled by rapid expansion of oil refining, fertilizer production, and chemical processing industries. Government initiatives promoting domestic manufacturing and infrastructure development are encouraging investment in industrial safety technologies. Rising awareness regarding workplace hazard prevention and compliance with safety standards is driving sensor installations across high-risk facilities. Growth in mining, power generation, and waste management projects further supports market expansion.

Europe Hazardous Area Sensors Market Insight

The Europe hazardous area sensors market is expanding steadily, supported by strict adherence to ATEX regulations and comprehensive occupational safety directives. The region’s mature industrial base and emphasis on advanced process control systems are promoting integration of high-precision hazardous area sensors. Investments in renewable energy plants, chemical processing facilities, and modernization of legacy infrastructure are strengthening demand. Focus on sustainability and risk mitigation strategies is also contributing to steady market growth.

Germany Hazardous Area Sensors Market Insight

Germany’s hazardous area sensors market is driven by its technologically advanced manufacturing ecosystem and strong presence in automotive, chemical, and energy sectors. The country’s leadership in Industry 4.0 adoption and smart factory implementation is increasing demand for real-time hazard detection systems. Robust engineering capabilities and continuous R&D investments support innovation in intrinsically safe sensor technologies. Export-oriented industrial production further sustains consistent deployment across hazardous environments.

U.K. Hazardous Area Sensors Market Insight

The U.K. market is supported by established offshore oil & gas activities, stringent health and safety regulations, and continuous upgrades in industrial automation systems. Emphasis on asset integrity management and remote monitoring solutions is increasing the use of hazardous area sensors across critical infrastructure. Investments in energy transition projects, including hydrogen and renewable energy facilities, are also generating new application areas. Strong regulatory oversight ensures consistent adoption across high-risk industrial operations.

North America Hazardous Area Sensors Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by expansion of shale gas production, petrochemical capacity additions, and modernization of industrial facilities. Strict regulatory frameworks related to occupational safety and environmental protection are accelerating sensor integration. Rising adoption of IoT-enabled monitoring platforms and predictive maintenance systems is enhancing operational safety. Continued investments in power generation and chemical manufacturing sectors further support regional growth momentum.

U.S. Hazardous Area Sensors Market Insight

The U.S. accounted for the largest share in the North America market in 2025, underpinned by its extensive upstream and downstream oil & gas infrastructure and strong chemical manufacturing base. Federal safety standards and compliance requirements are driving consistent installation of certified hazardous area sensing devices. Growing focus on digital transformation, industrial automation, and smart monitoring technologies is improving real-time risk detection capabilities. Presence of leading sensor manufacturers and advanced R&D facilities strengthens the country’s competitive position in the regional market.

Hazardous Area Sensors Market Share

The hazardous area sensors industry is primarily led by well-established companies, including:

- PATLITE Corporation (Japan)

- Eaton (Ireland)

- Siemens (Germany)

- ABB (Switzerland)

- R. STAHL AG (Germany)

- Rockwell Automation (U.S.)

- Emerson Electric Co. (U.S.)

- NHP Electrical Engineering Products (Australia)

- Honeywell International Inc. (U.S.)

- WERMA Signaltechnik GmbH + Co. KG (Germany)

- Potter Electric Signal Company, LLC (U.S.)

- Federal Signal Corporation (U.S.)

- E2S Warning Signals (U.K.)

Latest Developments in Global Hazardous Area Sensors Market

- In January 2026, Siemens introduced an upgraded portfolio of intrinsically safe wireless hazardous area sensors integrated with advanced edge computing capabilities. This development is expected to strengthen Siemens’ competitive position by enabling real-time data processing and faster hazard detection in remote industrial environments. The launch supports the growing industry shift toward decentralized monitoring and smart industrial infrastructure, enhancing operational reliability and reducing downtime across oil & gas and chemical facilities

- In February 2025, ABB expanded its hazardous area instrumentation range with ATEX-certified smart gas and temperature sensors tailored for high-risk process industries. This strategic expansion enhances ABB’s ability to cater to stringent safety compliance requirements while improving plant-level automation and predictive maintenance capabilities. The move reinforces the company’s market presence in energy and heavy industrial sectors, positioning it to capture rising demand for integrated and digitally enabled safety solutions

- In December 2024, Honeywell unveiled a cloud-based platform integrating hazardous area sensors with advanced data analytics tools. This development is strengthening Honeywell’s leadership by enabling end users to gain actionable insights for proactive risk mitigation and performance optimization. The platform aligns with accelerating digital transformation trends, redefining safety monitoring and enhancing long-term customer engagement through data-driven services

- In November 2024, Emerson announced a strategic partnership with a leading software firm to enhance advanced analytics capabilities for its hazardous area sensors. This collaboration improves predictive maintenance efficiency and supports integration of AI-driven diagnostics within hazardous industrial settings. The initiative reinforces Emerson’s technological differentiation and aligns its portfolio with the increasing adoption of intelligent and connected safety systems

- In October 2024, Schneider Electric launched a new line of explosion-proof sensors engineered for extreme industrial environments. This product expansion strengthens Schneider Electric’s compliance-driven positioning in sectors with rigorous safety standards such as oil & gas and chemicals. The introduction enhances its market competitiveness by broadening its certified sensor portfolio and addressing growing demand for reliable hazard detection solutions

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.