Global Hemophilia B Market

Market Size in USD Billion

CAGR :

%

USD

3.21 Billion

USD

6.39 Billion

2025

2033

USD

3.21 Billion

USD

6.39 Billion

2025

2033

| 2026 –2033 | |

| USD 3.21 Billion | |

| USD 6.39 Billion | |

| % | |

|

Hemophilia B Market Size

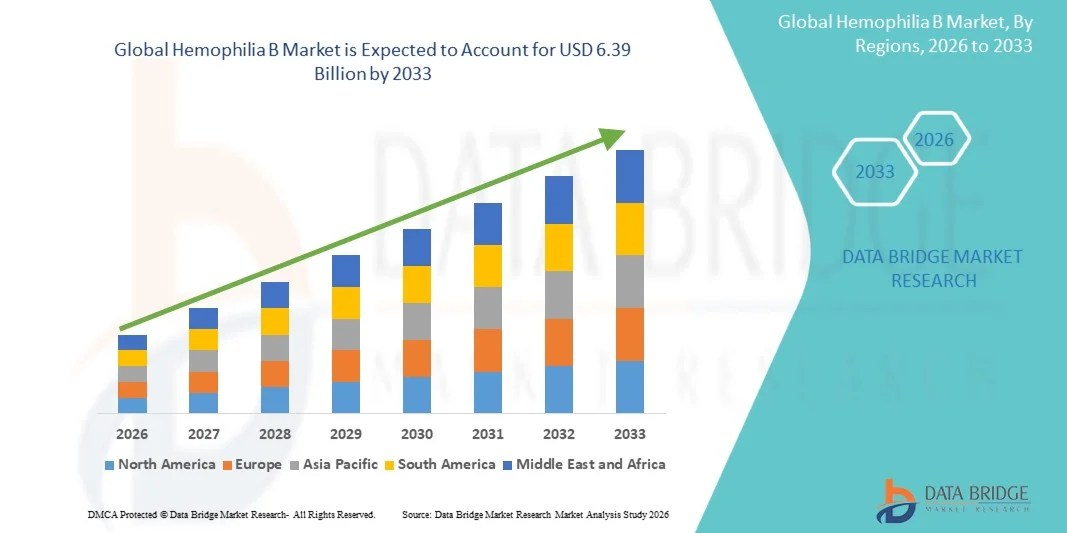

- The global Hemophilia B market size was valued at USD 3.21 billion in 2025 and is expected to reach USD 6.39 billion by 2033, at a CAGR of 9.00% during the forecast period

- The market growth is primarily driven by the increasing prevalence of Hemophilia B and continuous advancements in treatment options, including extended half-life factor IX therapies and emerging gene therapies, which are significantly improving patient outcomes and reducing treatment burden

- Furthermore, growing awareness, improved diagnostic rates, and rising demand for long-term, effective, and convenient treatment solutions are positioning advanced therapeutics as the preferred standard of care. These combined factors are accelerating the adoption of innovative Hemophilia B treatments, thereby substantially boosting market growth

Hemophilia B Market Analysis

- Hemophilia B, a rare genetic bleeding disorder caused by deficiency of clotting factor IX, requires lifelong management through replacement therapies and advanced treatment approaches, making it a critical segment within the broader rare disease therapeutics market across both developed and emerging healthcare systems

- The escalating demand for Hemophilia B treatments is primarily driven by increasing diagnosis rates, growing awareness programs, and significant advancements in treatment options such as extended half-life factor IX products and innovative gene therapies aimed at reducing treatment frequency and improving patient quality of life

- North America dominated the Hemophilia B market with the largest revenue share of 40.7% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, and early adoption of novel therapies, with the U.S. witnessing substantial growth due to the presence of leading biopharmaceutical companies and increased uptake of high-cost gene therapies

- Asia-Pacific is expected to be the fastest growing region in the Hemophilia B market during the forecast period due to improving healthcare access, rising awareness about rare bleeding disorders, and increasing government initiatives to support diagnosis and treatment in countries such as China and India

- Prophylaxis segment dominated the Hemophilia B market with a market share of 44.2% in 2025, driven by its effectiveness in preventing bleeding episodes, reducing long-term complications, and its growing adoption as the standard of care over on-demand treatment approaches

Report Scope and Hemophilia B Market Segmentation

|

Attributes |

Hemophilia B Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Hemophilia B Market Trends

“Advancements in Gene Therapy and Extended Half-Life Treatments”

- A significant and accelerating trend in the global Hemophilia B market is the rapid advancement in gene therapy and extended half-life factor IX treatments, which are transforming disease management and improving long-term patient outcomes across healthcare systems

- For instance, therapies such as Hemgenix have demonstrated the potential to provide long-term factor IX expression with a single administration, reducing or eliminating the need for frequent infusions. Similarly, extended half-life products such as Alprolix offer prolonged protection against bleeding episodes

- These innovations enable reduced treatment frequency, improved adherence, and better quality of life for patients. Furthermore, gene therapy approaches aim to address the root cause of Hemophilia B by introducing functional copies of the defective gene, offering the possibility of long-term or permanent therapeutic benefits

- The integration of advanced biologics and genetic technologies into treatment protocols facilitates more personalized and effective disease management. Through specialized treatment centers, patients can access innovative therapies alongside comprehensive care, creating a more optimized and coordinated treatment ecosystem

- This trend towards more effective, durable, and patient-centric therapies is fundamentally reshaping treatment expectations and clinical outcomes. Consequently, companies such as CSL Behring are developing next-generation therapies focused on long-term efficacy and reduced treatment burden

- The demand for advanced Hemophilia B treatments that offer long-lasting efficacy and reduced dosing frequency is growing rapidly across global healthcare systems, as patients and providers increasingly prioritize improved clinical outcomes and convenience

Hemophilia B Market Dynamics

Driver

“Rising Diagnosis Rates and Demand for Advanced Therapeutics”

- The increasing diagnosis rates of rare bleeding disorders, coupled with the growing demand for advanced and long-lasting treatment options, is a significant driver for the heightened demand for Hemophilia B therapies

- For instance, in recent years, World Federation of Hemophilia has expanded global registries and awareness initiatives, leading to improved identification and treatment access for patients. Such strategies by key organizations are expected to drive the Hemophilia B market growth in the forecast period

- As healthcare systems improve screening and diagnostic capabilities, more patients are being identified at earlier stages, increasing the demand for effective prophylactic and curative treatment options

- Furthermore, the growing adoption of gene therapies and extended half-life factor IX products is making advanced therapeutics an integral component of treatment strategies, offering improved efficacy and reduced treatment frequency

- The growing investment in rare disease research and development by major biopharmaceutical companies is significantly accelerating innovation and expanding the pipeline of advanced Hemophilia B therapies

- Furthermore, favorable government policies, orphan drug designations, and regulatory incentives are encouraging the development and commercialization of novel treatments, thereby boosting overall market expansion

- The need for long-term disease management, reduced bleeding episodes, and improved quality of life are key factors propelling the adoption of innovative therapies in both developed and emerging healthcare markets. The trend towards personalized medicine and specialized care centers further contributes to market growth

Restraint/Challenge

“High Treatment Costs and Limited Accessibility in Emerging Regions”

- Concerns surrounding the high cost of advanced therapies, including gene therapy and biologics, pose a significant challenge to broader market penetration. As these treatments require substantial investment, affordability remains a major barrier for many healthcare systems and patients

- For instance, high-cost gene therapies such as Hemgenix have raised concerns regarding reimbursement and accessibility, particularly in low- and middle-income countries

- Addressing these cost-related challenges through pricing strategies, reimbursement frameworks, and government support is crucial for expanding patient access. Companies such as Pfizer emphasize expanding access programs and collaborations to improve treatment availability. In addition, limited diagnostic infrastructure in some regions can delay treatment initiation, further restricting market growth

- While awareness and healthcare investments are increasing, disparities in access to advanced therapies persist, particularly in developing regions where healthcare resources are constrained

- Limited awareness and underdiagnosis of Hemophilia B in low-income regions continue to restrict early intervention and access to appropriate treatment options, hindering market growth potential

- In addition, the complexity of gene therapy administration and the requirement for specialized healthcare infrastructure create logistical and operational challenges for widespread adoption across all regions

- Overcoming these challenges through improved healthcare infrastructure, policy support, and cost-effective treatment innovations will be vital for sustained market growth

Hemophilia B Market Scope

The market is segmented on the basis of drugs, treatment, route of administration, end-users, and distribution channel.

- By Drugs

On the basis of drugs, the Hemophilia B market is segmented into plasma derived coagulation factor concentrate, recombinant coagulation factor concentrates, desmopressin, and others. The recombinant coagulation factor concentrates segment dominated the market with the largest market revenue share in 2025, driven by their superior safety profile, reduced risk of blood-borne infections, and widespread adoption as the standard of care. These products, including extended half-life factor IX therapies, offer improved efficacy and reduced dosing frequency, enhancing patient compliance and treatment outcomes. The growing preference for recombinant therapies over plasma-derived alternatives is further supported by technological advancements and strong regulatory approvals. In addition, increasing investments in biologics and innovations in factor replacement therapies are strengthening the dominance of this segment globally.

The plasma derived coagulation factor concentrate segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing demand in developing regions where cost-effective treatment options are essential. These therapies remain critical in regions with limited access to advanced biologics, ensuring broader patient coverage. Furthermore, improvements in purification technologies and safety measures are enhancing the reliability of plasma-derived products. Government initiatives to expand access to essential medicines and rising awareness about bleeding disorders are also contributing to the growth of this segment.

- By Treatment

On the basis of treatment, the Hemophilia B market is segmented into on-demand and prophylaxis. The prophylaxis segment dominated the market with the largest market revenue share of 44.2% in 2025, driven by its effectiveness in preventing bleeding episodes and long-term complications. Prophylactic therapy is increasingly considered the standard of care, particularly in developed healthcare systems, due to its ability to improve patient quality of life and reduce hospitalizations. The adoption of extended half-life factor IX therapies has further strengthened this segment by reducing injection frequency and improving adherence. In addition, growing clinical evidence supporting early prophylaxis in pediatric patients is boosting its widespread implementation.

The on-demand segment is expected to witness the fastest CAGR from 2026 to 2033, driven by its continued relevance in regions with limited healthcare access and high treatment costs. On-demand therapy provides flexibility for patients who cannot afford continuous prophylactic treatment. Furthermore, increasing awareness and diagnosis in emerging markets are expanding the patient pool relying on this treatment approach. The availability of rapid-acting therapies and improved healthcare infrastructure in developing countries are also contributing to the segment’s growth.

- By Route of Administration

On the basis of route of administration, the Hemophilia B market is segmented into oral and injectable. The injectable segment dominated the market with the largest market revenue share in 2025, driven by the widespread use of intravenous factor IX replacement therapies. Injectable administration remains the most effective and reliable method for delivering clotting factors directly into the bloodstream, ensuring rapid therapeutic action. The development of extended half-life injectables has further enhanced patient convenience by reducing dosing frequency. In addition, the availability of home infusion programs and training has supported the continued dominance of this segment.

The oral segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by ongoing research into non-invasive treatment alternatives and gene-based oral therapies. Although currently limited, advancements in drug delivery technologies are expected to enable oral administration options in the future. The increasing patient preference for convenient and pain-free treatment methods is also driving innovation in this segment. Furthermore, pharmaceutical companies are investing in novel formulations to improve bioavailability and therapeutic effectiveness.

- By End-Users

On the basis of end-users, the Hemophilia B market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with the largest market revenue share in 2025, driven by the availability of advanced treatment facilities, skilled healthcare professionals, and access to specialized diagnostic tools. Hospitals play a critical role in managing severe cases, administering complex therapies, and handling complications associated with Hemophilia B. The presence of multidisciplinary care teams and comprehensive treatment protocols further strengthens this segment. In addition, favorable reimbursement policies in developed regions support hospital-based treatment adoption.

The homecare segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the growing preference for self-administration and convenience among patients. Home-based treatment reduces hospital visits, lowers healthcare costs, and improves patient independence. The increasing availability of user-friendly infusion devices and training programs is enabling patients to manage their condition effectively at home. Furthermore, advancements in telemedicine and remote monitoring are supporting the expansion of homecare services.

- By Distribution Channel

On the basis of distribution channel, the Hemophilia B market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the market with the largest market revenue share in 2025, driven by the direct supply of specialized and high-cost therapies through hospital networks. These pharmacies ensure proper storage, handling, and administration of biologics and gene therapies, which require strict regulatory compliance. The strong integration of hospital pharmacies with treatment centers further supports their dominance in the market. In addition, reimbursement frameworks often favor hospital-based distribution channels.

The online pharmacy segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing digitalization and the growing adoption of e-commerce in healthcare. Online platforms offer convenience, accessibility, and competitive pricing, making them attractive to patients requiring long-term therapy. The expansion of digital health infrastructure and improved logistics networks are further supporting this growth. In addition, rising awareness and acceptance of online pharmaceutical services are contributing to the increasing demand in this segment.

Hemophilia B Market Regional Analysis

- North America dominated the Hemophilia B market with the largest revenue share of 40.7% in 2025, characterized by advanced healthcare infrastructure, strong reimbursement frameworks, and early adoption of novel therapies

- Patients and healthcare providers in the region highly value the availability of innovative treatments such as extended half-life factor IX products and gene therapies, along with comprehensive care programs offered through specialized treatment centers

- This widespread adoption is further supported by favorable reimbursement policies, high healthcare spending, and a strong presence of leading biopharmaceutical companies, establishing advanced Hemophilia B therapies as a preferred treatment approach across both hospital and homecare settings

U.S. Hemophilia B Market Insight

The U.S. Hemophilia B market captured the largest revenue share of 81% in 2025 within North America, fueled by the strong presence of advanced healthcare infrastructure and rapid adoption of innovative therapies. Patients and healthcare providers are increasingly prioritizing long-term disease management through extended half-life factor IX products and gene therapies. The growing preference for home-based treatment solutions, combined with robust reimbursement frameworks and insurance coverage, further propels the market. Moreover, continuous advancements in biotechnology and increasing approvals of novel therapies are significantly contributing to the market's expansion.

Europe Hemophilia B Market Insight

The Europe Hemophilia B market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by strong regulatory support and increasing focus on rare disease management. The rise in awareness programs, coupled with improved access to advanced therapies, is fostering the adoption of Hemophilia B treatments. European healthcare systems are also emphasizing early diagnosis and prophylactic care to improve patient outcomes. The region is experiencing steady growth across hospital and homecare settings, with innovative therapies being incorporated into both existing treatment protocols and new healthcare initiatives.

U.K. Hemophilia B Market Insight

The U.K. Hemophilia B market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of rare bleeding disorders and a strong emphasis on early diagnosis and treatment. In addition, government-supported healthcare programs and national treatment guidelines are encouraging the adoption of advanced therapeutic solutions. The country’s well-established healthcare infrastructure, alongside its focus on patient-centric care, is expected to continue to stimulate market growth.

Germany Hemophilia B Market Insight

The Germany Hemophilia B market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing adoption of advanced biologics and strong healthcare funding. Germany’s well-developed healthcare system, combined with its emphasis on innovation and clinical research, promotes the adoption of novel therapies, particularly in specialized treatment centers. The integration of advanced treatment protocols and personalized medicine approaches is also becoming increasingly prevalent, aligning with the country’s focus on high-quality patient care.

Asia-Pacific Hemophilia B Market Insight

The Asia-Pacific Hemophilia B market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by improving healthcare infrastructure, rising awareness about Hemophilia B, and increasing government initiatives in countries such as China, Japan, and India. The region's growing focus on rare disease management, supported by expanding diagnostic capabilities, is driving the adoption of Hemophilia B treatments. Furthermore, as APAC strengthens its healthcare systems and access to biologics, treatment availability is expanding to a wider patient population.

Japan Hemophilia B Market Insight

The Japan Hemophilia B market is gaining momentum due to the country’s advanced healthcare system, strong research capabilities, and increasing demand for effective long-term treatment solutions. The Japanese market places significant emphasis on quality care, and the adoption of advanced therapies is driven by increasing awareness and diagnosis rates. The integration of innovative biologics and gene therapies into treatment protocols is fueling growth. Moreover, Japan's aging population is likely to spur demand for improved healthcare services and long-term disease management solutions.

India Hemophilia B Market Insight

The India Hemophilia B market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding healthcare access, rising awareness, and increasing diagnosis rates. India stands as one of the key emerging markets for rare disease treatment, and Hemophilia B therapies are becoming increasingly accessible across hospitals and specialty centers. The push towards strengthening healthcare infrastructure and government support programs, alongside the availability of cost-effective treatment options, are key factors propelling the market in India.

Hemophilia B Market Share

The Hemophilia B industry is primarily led by well-established companies, including:

- Pfizer Inc. (U.S.)

- Novo Nordisk A/S (Denmark)

- CSL Behring LLC (U.S.)

- Bayer AG (Germany)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Sanofi (France)

- Takeda Pharmaceutical Company Limited (Japan)

- Grifols, S.A. (Spain)

- Octapharma AG (Switzerland)

- Kedrion S.p.A. (Italy)

- BioMarin Pharmaceutical Inc. (U.S.)

- Swedish Orphan Biovitrum AB (Sweden)

- uniQure N.V. (Netherlands)

- Freeline Therapeutics Holdings plc (U.K.)

- Catalyst Biosciences, Inc. (U.S.)

- Sangamo Therapeutics, Inc. (U.S.)

- Alnylam Pharmaceuticals, Inc. (U.S.)

- GC Biopharma Corp. (South Korea)

- Emergent BioSolutions Inc. (U.S.)

- Bio Products Laboratory Ltd (U.K.)

What are the Recent Developments in Global Hemophilia B Market?

- In December 2025, CSL Behring announced the publication of five-year clinical data for its gene therapy Hemgenix, demonstrating sustained factor IX levels and up to 90% reduction in bleeding rates, confirming long-term durability and effectiveness of one-time treatment for Hemophilia B patients

- In September 2025, Pfizer initiated extended follow-up and dose-escalation studies for its Hemophilia B gene therapy candidates, focusing on long-term safety, efficacy, and optimized dosing strategies to enhance treatment outcomes

- In February 2025, Pfizer announced the discontinuation of its Hemophilia B gene therapy Beqvez commercialization due to low market demand, highlighting challenges in adoption despite recent regulatory approvals

- In January 2025, multiple U.S. healthcare centers reported successful administration of Hemgenix gene therapy to new patients, marking continued real-world adoption of the first approved one-time gene therapy for Hemophilia B and demonstrating its transition from clinical trials to routine clinical use

- In June 2024, the National Institute for Health and Care Excellence approved Hemgenix for use within the NHS in England, enabling patient access to transformative gene therapy and marking a major milestone in public healthcare adoption of advanced Hemophilia B treatments

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.