Global Hemostasis Diagnostics Market

Market Size in USD Billion

CAGR :

%

USD

19.47 Billion

USD

76.21 Billion

2025

2033

USD

19.47 Billion

USD

76.21 Billion

2025

2033

| 2026 - 2033 | |

| USD 19.47 Billion | |

| USD 76.21 Billion | |

| % | |

|

Hemostasis Diagnostics Market Overview

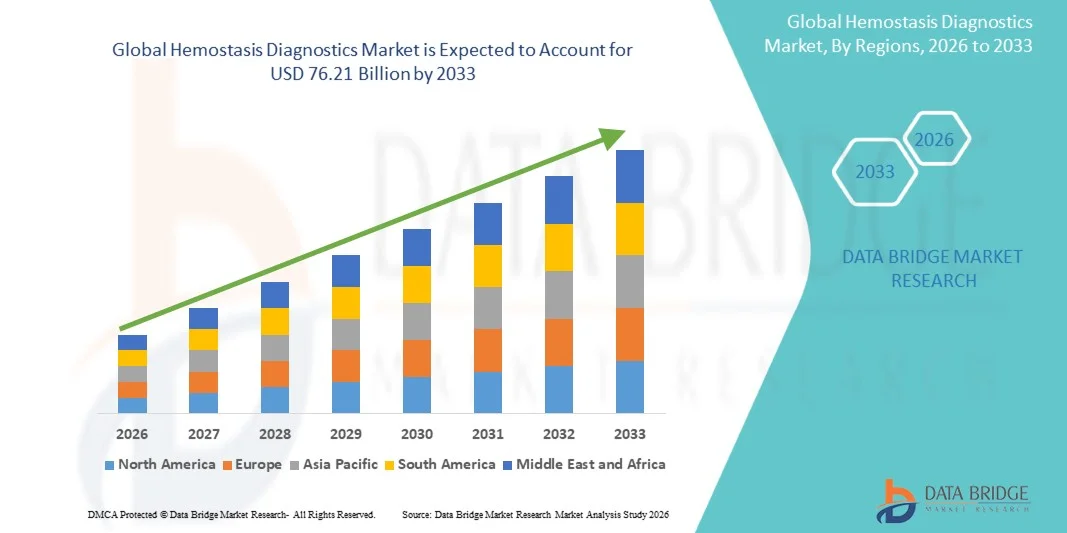

The Hemostasis Diagnostics Market was valued at USD 19.47 billion in 2025 and is projected to reach USD 76.21 billion by 2033, growing at a CAGR of 18.60% from 2026 to 2033. The Hemostasis Diagnostics Market is experiencing steady growth driven by the increasing prevalence of bleeding disorders, thrombotic diseases, cardiovascular conditions, and the growing demand for accurate coagulation testing across healthcare settings. Continuous advancements in diagnostic technologies, automation of laboratory workflows, and the expanding adoption of point-of-care coagulation testing are further supporting market expansion. Rising awareness regarding early diagnosis of hemostatic abnormalities and increasing utilization of coagulation assays in surgical procedures, critical care, and anticoagulant therapy monitoring are also contributing significantly to market growth.

The growing burden of disorders such as hemophilia, deep vein thrombosis (DVT), pulmonary embolism, liver diseases, and disseminated intravascular coagulation (DIC), combined with increasing healthcare expenditure and improved access to diagnostic services, is encouraging hospitals, diagnostic laboratories, and specialty clinics to adopt advanced hemostasis diagnostic solutions. Automated coagulation analyzers, molecular diagnostic technologies, and integrated laboratory systems are increasingly replacing conventional manual testing methods by providing faster turnaround times, improved accuracy, and enhanced workflow efficiency. Furthermore, the expanding geriatric population, rising number of surgical interventions, and increasing use of anticoagulant medications worldwide are accelerating the demand for reliable hemostasis diagnostics, creating substantial growth opportunities for market participants.

Key Market Trends & Insights

- North America dominated the Hemostasis Diagnostics Market with the largest revenue share of 39.18% in 2025, driven by the high prevalence of cardiovascular disorders and bleeding conditions, advanced healthcare infrastructure, widespread adoption of coagulation testing, favorable reimbursement policies, and the strong presence of leading diagnostic manufacturers. Increasing demand for early diagnosis and monitoring of thrombotic and coagulation disorders further supports regional market growth.

- The Laboratory Analyzers segment dominated the market with a share of 58.42% in 2025, driven by widespread adoption in hospitals and diagnostic laboratories for automated coagulation testing.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.2% from 2026 to 2033, fueled by increasing healthcare expenditure, expanding diagnostic infrastructure, rising prevalence of cardiovascular diseases, growing awareness regarding coagulation disorders, and improving access to advanced laboratory testing services across China, India, Japan, and Southeast Asia.

- The D-Dimer Test segment is projected to be the fastest-growing test type, registering a CAGR of 8.0%, reflecting increasing utilization in the diagnosis and monitoring of venous thromboembolism, deep vein thrombosis, pulmonary embolism, and other thrombotic conditions. Growing demand for rapid diagnostic assessment in emergency and critical care settings is further supporting segment growth.

- The Prothrombin Time (PT) Test segment dominates the test type category with a 29.74% revenue share in 2025, driven by its widespread use in evaluating blood clotting function, monitoring anticoagulant therapy, and diagnosing coagulation disorders across clinical settings.

- The Hospitals/Clinics segment accounted for 56.81% of the market in 2025, supported by high patient volumes, increasing surgical procedures, growing incidence of coagulation disorders, and extensive utilization of hemostasis diagnostic tests for routine screening, disease management, and perioperative monitoring.

- The Point-of-Care Testing Systems segment is expected to be the fastest-growing product category, with a CAGR of 7.9%, driven by increasing demand for rapid diagnostic results, decentralized healthcare delivery, improved patient management, and growing adoption of portable coagulation testing devices in emergency care, outpatient settings, and home healthcare environments.

Market Size & Forecast

- Global Market Value (2025): USD 19.47 Billion

- Expected Market Value (2033): USD 76.21 Billion

- Forecast CAGR (2026–2033): 18.60%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Hemostasis Diagnostics Market Segmentation

|

Attributes |

Hemostasis Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Abbott Laboratories (U.S.) |

|

Market Opportunities |

· Expansion of Point-of-Care (POC) Coagulation Testing Solutions · Growth in Personalized Medicine and Anticoagulation Monitoring · Technological Advancements in Automated and AI-Integrated Diagnostic Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Hemostasis Diagnostics Market Trends

Trend: Rising Adoption of Point-of-Care and Automated Coagulation Testing Systems

The Hemostasis Diagnostics market is witnessing a strong shift toward automated analyzers and point-of-care (POC) testing systems, driven by the need for faster diagnosis of coagulation disorders such as deep vein thrombosis (DVT), pulmonary embolism (PE), and bleeding disorders. Hospitals and emergency departments are increasingly adopting POC coagulation devices that deliver results within minutes, improving critical care decision-making. According to clinical laboratory trends reported across major healthcare systems, turnaround time reduction of up to 50–70% in emergency coagulation testing has significantly improved patient outcomes. In addition, increasing surgical volumes globally—estimated at over 300 million procedures annually—continues to drive demand for rapid PT, aPTT, and D-dimer testing solutions across hospitals and diagnostic centers.

Hemostasis Diagnostics Market Dynamics

Key Market Driver: Rising Prevalence of Cardiovascular and Coagulation Disorders

The increasing global burden of cardiovascular diseases, thrombotic disorders, and bleeding abnormalities is a major driver of the Hemostasis Diagnostics market. According to the World Health Organization (WHO), cardiovascular diseases are responsible for nearly 17.9 million deaths annually, many of which are associated with clotting and coagulation complications requiring diagnostic monitoring. Growing incidence of conditions such as atrial fibrillation, venous thromboembolism, liver disease–related coagulopathy, and hemophilia is further increasing demand for hemostasis testing. In addition, widespread use of anticoagulant therapies such as warfarin and direct oral anticoagulants (DOACs) has significantly increased the need for regular PT/INR monitoring, supporting sustained growth of laboratory analyzers, consumables, and POC testing systems across healthcare facilities.

Key Restraint/Challenge: High Cost and Complexity of Advanced Hemostasis Testing Systems

A major challenge in the Hemostasis Diagnostics market is the high cost associated with advanced automated coagulation analyzers and continuous maintenance requirements. High-throughput laboratory systems require significant capital investment, calibration, quality control reagents, and skilled laboratory personnel, limiting adoption in small and mid-sized diagnostic facilities. In addition, variability in reimbursement policies across regions creates financial pressure on healthcare providers. Supply chain disruptions for reagents and consumables, along with stringent regulatory compliance requirements for diagnostic accuracy, further add to operational complexity and can restrict market penetration in cost-sensitive regions.

Key Market Opportunity: Expansion of Integrated Laboratory Automation and AI-Driven Diagnostics The integration of laboratory automation and artificial intelligence represents a major opportunity for the Hemostasis Diagnostics market. AI-enabled diagnostic platforms are increasingly being used to interpret coagulation profiles, detect abnormal clotting patterns, and predict thrombotic risk with higher accuracy. The development of fully automated coagulation workstations and cloud-connected laboratory information systems (LIS) is improving workflow efficiency and reducing human error. Furthermore, growing investment in hospital laboratory modernization—particularly in Asia-Pacific and Middle Eastern countries—is accelerating adoption of advanced diagnostic platforms. Increasing collaborations between diagnostic companies and healthcare providers are also enabling development of predictive analytics models for personalized anticoagulation therapy management, creating new growth avenues for the market.

Hemostasis Diagnostics Market Scope

The Hemostasis Diagnostics market is segmented on the basis of product, test type, and end use.

- By Product

On the basis of product, the Hemostasis Diagnostics Market is segmented into laboratory analyzers, consumables, and point-of-care testing systems. The Laboratory Analyzers segment dominated the market with a share of 58.42% in 2025, driven by widespread adoption in hospitals and diagnostic laboratories for automated coagulation testing. These systems enable high-throughput analysis of PT, APTT, and fibrinogen tests with high accuracy and reproducibility. Increasing prevalence of bleeding and thrombotic disorders is strengthening demand for advanced analyzers. Growing laboratory automation and integration with LIS systems is further supporting segment expansion. Rising healthcare infrastructure development in emerging economies is also boosting adoption. Continuous technological advancements in fully automated platforms are enhancing efficiency and workflow management.

The Consumables segment is also witnessing steady demand due to recurring usage in every diagnostic cycle. Increasing test volumes in hospitals and labs is supporting consistent consumption. Rising awareness of early disease detection is driving routine coagulation testing adoption. The Point-of-Care Testing Systems segment is expected to be the fastest-growing segment, registering a CAGR of 7.6% from 2026 to 2033, driven by rising demand for rapid bedside diagnostics in emergency and critical care settings. These systems provide quick results for PT/INR and APTT tests, enabling immediate clinical decision-making. Increasing adoption in ambulances, ICUs, and remote healthcare facilities is accelerating growth. Technological advancements in portable and compact devices are improving usability and accuracy. Growing shift toward decentralized healthcare models is supporting adoption. Rising burden of cardiovascular and thrombotic disorders is further boosting demand. Expanding home-based anticoagulant monitoring is also contributing to segment growth. Integration of digital connectivity features is enhancing real-time reporting capabilities.

- By Test Type

On the basis of test type, the Hemostasis Diagnostics Market is segmented into APTT, D-Dimer, fibrinogen, PT, ACT, and platelet aggregation tests. The Prothrombin Time (PT) Test segment dominated the market with a share of 34.18% in 2025, due to its extensive use in anticoagulant therapy monitoring and routine coagulation screening. PT testing is widely performed in hospitals for patients on warfarin therapy. It is also essential in pre-surgical evaluations and liver disease diagnosis. High test reliability and standardized protocols support its dominance. Strong integration into automated analyzers increases efficiency. Rising incidence of cardiovascular diseases further drives demand. Growing elderly population requiring anticoagulation therapy supports sustained usage.

The APTT test also holds significant importance in monitoring intrinsic coagulation pathways. Increasing use in detecting clotting disorders is supporting adoption. The D-Dimer Test segment is expected to be the fastest-growing segment, registering a CAGR of 8.1% from 2026 to 2033, driven by rising use in rapid diagnosis of thrombotic conditions such as deep vein thrombosis and pulmonary embolism. Increasing emergency admissions are boosting demand for quick screening tests. Growing awareness of early clot detection is supporting clinical adoption. Expanding use in ICU and emergency departments is accelerating demand. Rising cardiovascular disease burden globally is further contributing to growth. Advancements in high-sensitivity assay technologies are improving diagnostic accuracy. Increasing use in COVID-related complications has also strengthened adoption trends. Growing preference for rapid exclusion testing in hospitals is fueling segment expansion.

- By End Use

On the basis of end use, the Hemostasis Diagnostics Market is segmented into hospitals/clinics, independent diagnostic laboratories, home care settings, and others. The Hospitals/Clinics segment dominated the market with a share of 52.63% in 2025, driven by high patient inflow and availability of advanced diagnostic infrastructure. Hospitals conduct the majority of coagulation testing for surgical, trauma, and chronic disease cases. Increasing prevalence of bleeding and thrombotic disorders supports strong test volumes. Availability of skilled healthcare professionals enhances diagnostic accuracy. Integrated laboratory systems improve workflow efficiency. Rising number of surgeries globally further boosts demand. Strong adoption of automated analyzers reinforces dominance. Continuous investment in hospital diagnostic infrastructure supports segment growth.

Independent diagnostic laboratories also contribute significantly due to outsourced testing services. Growing referral-based testing is increasing their share in the market. The Home Care Settings segment is expected to be the fastest-growing segment, registering a CAGR of 9.2% from 2026 to 2033, driven by rising adoption of portable coagulation monitoring devices for long-term anticoagulant therapy patients. Increasing preference for self-testing is reducing hospital visits. Growing geriatric population requiring continuous monitoring is supporting demand. Expansion of telehealth and remote patient monitoring is accelerating adoption. Technological advancements in compact POC devices are improving usability. Rising awareness of patient-centric healthcare models is driving uptake. Increasing healthcare digitization is enabling real-time data sharing with physicians. Growing cost-effectiveness of home-based testing is further boosting segment growth.

Hemostasis Diagnostics Market Regional Analysis

North America dominated the Hemostasis Diagnostics Market and accounted for the largest revenue share of 39.18% in 2025, driven by the high prevalence of cardiovascular disorders, thrombotic conditions, and bleeding abnormalities, along with advanced healthcare infrastructure and widespread adoption of coagulation testing solutions. The region benefits from strong reimbursement frameworks, the presence of leading diagnostic manufacturers, and well-established hospital laboratory networks. Increasing demand for early diagnosis and continuous monitoring of coagulation disorders such as deep vein thrombosis (DVT), pulmonary embolism (PE), and hemophilia is further strengthening market growth across North America.

U.S. Hemostasis Diagnostics Market Insight

The U.S. Hemostasis Diagnostics market is witnessing strong growth due to rising incidence of cardiovascular diseases and expanding use of anticoagulant therapies that require frequent monitoring through PT/INR and D-dimer testing. Advanced hospital infrastructure, high adoption of automated coagulation analyzers, and strong penetration of point-of-care testing systems are supporting market expansion. In addition, increasing focus on precision medicine, emergency care diagnostics, and laboratory automation is driving demand for faster and more accurate hemostasis testing solutions across healthcare facilities.

Europe Hemostasis Diagnostics Market Insight

The Europe Hemostasis Diagnostics market remains a major contributor to global revenue, supported by strong public healthcare systems, growing geriatric population, and increasing prevalence of chronic cardiovascular conditions. The region’s advanced diagnostic infrastructure and high adoption of standardized coagulation testing protocols are driving steady market expansion. Furthermore, increasing awareness regarding early diagnosis of clotting disorders and growing utilization of laboratory automation technologies continue to support demand across hospitals and diagnostic centers.

U.K. Hemostasis Diagnostics Market Insight

The U.K. Hemostasis Diagnostics market is experiencing steady growth, driven by rising incidence of thrombotic disorders, increasing surgical procedures, and strong adoption of advanced diagnostic technologies within the National Health Service (NHS). Growing use of point-of-care coagulation testing in emergency and critical care settings, along with expanding investment in laboratory modernization, is further enhancing diagnostic efficiency and patient outcomes across the country.

Germany Hemostasis Diagnostics Market Insight

The Germany Hemostasis Diagnostics market is expanding steadily due to the country’s strong healthcare infrastructure, high burden of cardiovascular diseases, and advanced laboratory diagnostic capabilities. Hospitals and diagnostic centers are increasingly adopting automated coagulation analyzers and molecular diagnostic tools to improve accuracy and efficiency. Additionally, strong emphasis on clinical research and innovation in hematology diagnostics is supporting continued market growth.

Asia-Pacific Hemostasis Diagnostics Market Insight

The Asia-Pacific Hemostasis Diagnostics market is expected to witness the fastest growth, registering a CAGR of 8.2% from 2026 to 2033. Growth is driven by increasing healthcare expenditure, expanding diagnostic infrastructure, rising prevalence of cardiovascular diseases, and improving awareness regarding coagulation disorders. Rapid urbanization and growing access to advanced laboratory testing services across China, India, Japan, and Southeast Asia are further supporting regional market expansion.

Japan Hemostasis Diagnostics Market Insight

The Japan Hemostasis Diagnostics market is witnessing consistent growth due to a rapidly aging population and increasing prevalence of cardiovascular and thrombotic disorders. The country’s advanced healthcare system, strong adoption of automated diagnostic platforms, and growing use of precision medicine approaches are supporting demand for coagulation testing solutions across hospitals and laboratories.

China Hemostasis Diagnostics Market Insight

The China Hemostasis Diagnostics market is growing rapidly, driven by increasing burden of cardiovascular diseases, expanding healthcare infrastructure, and rising adoption of advanced diagnostic technologies. Government initiatives aimed at strengthening healthcare access and improving chronic disease management are further accelerating market growth. In addition, growing investment in laboratory automation and point-of-care testing is enhancing diagnostic capabilities across urban and semi-urban healthcare facilities.

Hemostasis Diagnostics Market Share

The Hemostasis Diagnostics industry is primarily led by well-established companies, including:

- Abbott Laboratories (U.S.)

- Siemens Healthineers AG (Germany)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Sysmex Corporation (Japan)

- Werfen (Spain)

- Danaher Corporation (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Becton, Dickinson and Company (U.S.)

- bioMérieux SA (France)

- HORIBA Ltd. (Japan)

- Helena Laboratories Corporation (U.S.)

- Instrumentation Laboratory (Werfen Group) (Italy)

- HemoSonics LLC (U.S.)

- Grifols S.A. (Spain)

- Nihon Kohden Corporation (Japan)

- Stago Group (France)

- Randox Laboratories Ltd. (U.K.)

- Perosphere Technologies Inc. (U.S.)

- Diagnostica Stago Inc. (U.S.)

- Trinity Biotech plc (Ireland)

- Sekisui Diagnostics (U.S.)

- Mindray Medical International (China)

- Boule Diagnostics AB (Sweden)

- Erba Mannheim (Germany)

Latest Developments in Hemostasis Diagnostics Market

- In February 2021, Sysmex Corporation announced the expansion of its automated coagulation testing portfolio with enhanced high-throughput hemostasis analyzers, strengthening laboratory efficiency and supporting increased demand for routine PT, APTT, and D-dimer testing across clinical laboratories globally. This development reflects Sysmex’s focus on improving automation and standardization in coagulation diagnostics

- In June 2021, F. Hoffmann-La Roche Ltd expanded the availability of its cobas coagulation testing solutions in additional global markets, supporting integrated hemostasis testing workflows in clinical laboratories. The expansion aimed to improve diagnostic accuracy and streamline anticoagulation monitoring in hospital-based laboratories

- In March 2022, Werfen introduced updates to its ACL TOP family of hemostasis testing systems, enhancing automated coagulation analysis capabilities for high-volume laboratories. The upgraded systems focused on improving workflow efficiency, connectivity, and standardized coagulation testing performance across hospital laboratories

- In September 2022, Siemens Healthineers expanded its Atellica portfolio to strengthen integrated clinical laboratory diagnostics, including coagulation testing capabilities. The expansion supported improved laboratory consolidation and faster turnaround times for hemostasis assays in hospital environments

- In April 2023, HemoSonics received continued market expansion for its Quantra Hemostasis System, a viscoelastic point-of-care coagulation analyzer used in surgical and critical care settings. The system is designed to provide rapid assessment of clot formation and coagulopathy, supporting real-time clinical decision-making in operating rooms and trauma care

- In January 2024, Sysmex Corporation strengthened its global hemostasis diagnostics presence through continued deployment of advanced CN-series coagulation analyzers in clinical laboratories, supporting high-throughput testing and improved automation in routine and specialized coagulation diagnostics

- In May 2025, Siemens Healthineers and major clinical laboratory networks continued expanding adoption of fully automated hemostasis and integrated diagnostic platforms, driven by increasing demand for high-efficiency coagulation testing, digital connectivity, and laboratory workflow optimization across large hospital system

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.