Global High Performance Computing Market

Market Size in USD Billion

CAGR :

%

USD

27.08 Billion

USD

44.49 Billion

2025

2033

USD

27.08 Billion

USD

44.49 Billion

2025

2033

| 2026 –2033 | |

| USD 27.08 Billion | |

| USD 44.49 Billion | |

| % | |

|

What is the Global High Performance Computing Market Size and Growth Rate?

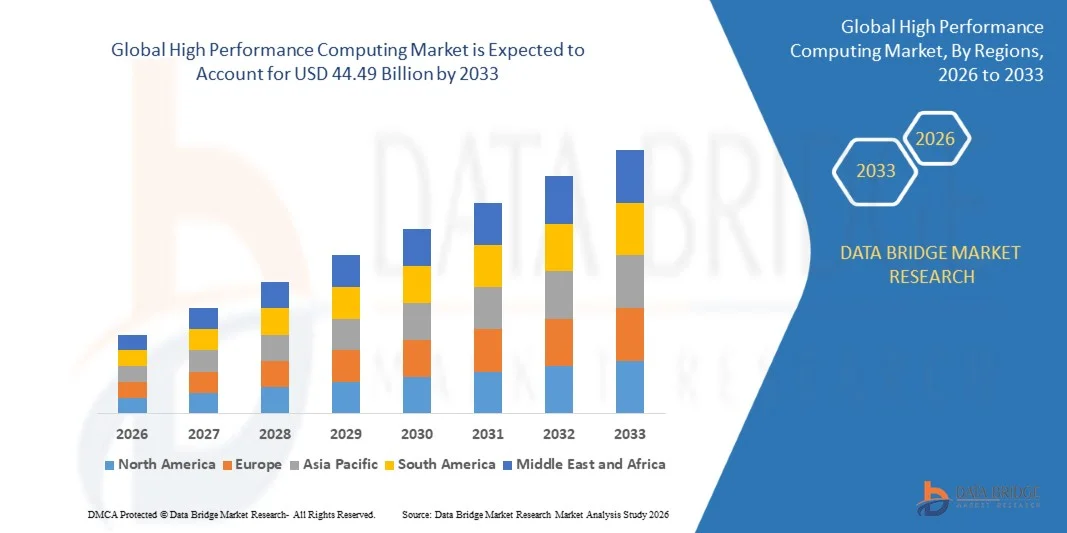

- The global high performance computing market size was valued at USD 27.08 billion in 2025 and is expected to reach USD 44.49 billion by 2033, at a CAGR of 6.40% during the forecast period

- The increase in demand for HPC in genomics research across the globe acts as one of the major factors driving the growth of high performance computing market

- The increase in need for efficient computing, enhanced scalability, and reliable storage, and growing need for continued diversification, expansion of the IT industry, high-efficiency computing and advances in virtualization, accelerate the market growth

What are the Major Takeaways of High Performance Computing Market?

- The rise in the adoption of high performance computing owning to its ability of HPC systems to process large volumes of data at higher speeds and high usage in various sectors further influence the market

- In addition, easy access to the high speed internet services, increase in demand for HPC in genomics research and high need for high-speed data processing with accuracy positively affect the high performance computing market. Furthermore, increase in focus on hybrid HPC solutions and advent of exascale computing to maximize the benefits of HPC extend profitable opportunities to the market players

- North America dominated the high performance computing market with a 41.6% revenue share in 2025, driven by strong investments in advanced computing infrastructure, artificial intelligence research, cloud computing platforms, and large-scale data centers across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 11.3% from 2026 to 2033, driven by rapid expansion of semiconductor manufacturing, strong growth in data center infrastructure, and increasing investments in national supercomputing programs across China, Japan, India, South Korea, and Southeast Asia

- The Solutions segment dominated the market with a 68.4% share in 2025, as organizations continue to invest heavily in HPC infrastructure including high-performance servers, storage systems, networking technologies, and advanced software platforms

Report Scope and High Performance Computing Market Segmentation

|

Attributes |

High Performance Computing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the High Performance Computing Market?

“Increasing Integration of AI Accelerators and Cloud-Based High Performance Computing Infrastructure”

- The high performance computing (HPC) market is witnessing strong adoption of AI-accelerated computing systems, GPU clusters, and cloud-based HPC platforms designed to support complex workloads such as scientific simulations, machine learning training, climate modeling, and genomic analysis

- Technology providers are introducing high-density computing architectures, advanced interconnect technologies, and energy-efficient processors to enhance performance, scalability, and computational efficiency in modern supercomputing environments

- Growing demand for large-scale data processing, real-time analytics, and high-performance simulations is driving adoption across research institutions, government agencies, financial services, and industrial R&D laboratories

- For instance, companies such as IBM, NVIDIA, Hewlett Packard Enterprise, and Dell Technologies are launching next-generation supercomputing platforms equipped with GPU accelerators, high-speed networking, and AI-optimized software frameworks

- Increasing need for high-speed data processing, AI model training, and digital twin simulations is accelerating the transition toward hybrid HPC infrastructures combining on-premise clusters and cloud-based computing environments

- As global demand for advanced computing capabilities expands, High Performance Computing systems will remain essential for scientific discovery, industrial innovation, and next-generation AI development

What are the Key Drivers of High Performance Computing Market?

- Rising demand for high-speed computing infrastructure to support complex simulations, big data analytics, artificial intelligence training, and large-scale scientific research is driving HPC adoption across multiple industries

- For instance, in 2025, leading companies such as IBM, NVIDIA, and Hewlett Packard Enterprise introduced advanced GPU-accelerated HPC systems and high-performance computing clusters designed to support AI workloads and high-throughput data processing

- Growing adoption of AI applications, weather forecasting models, genomics research, financial risk modeling, and digital engineering simulations is significantly increasing demand for powerful computing platforms across the U.S., Europe, and Asia-Pacific

- Advancements in parallel processing architectures, high-speed interconnects, advanced cooling technologies, and energy-efficient processors have improved system performance, scalability, and operational efficiency

- Rising use of deep learning models, autonomous vehicle simulations, and high-resolution scientific computing is creating demand for large-scale computing clusters capable of processing massive datasets efficiently

- Supported by strong investments in AI research, national supercomputing initiatives, and advanced data infrastructure, the High Performance Computing market is expected to witness sustained long-term growth

Which Factor is Challenging the Growth of the High Performance Computing Market?

- High capital investment and operational costs associated with building and maintaining large-scale supercomputing infrastructure remain a major barrier for small research organizations and emerging enterprises

- For instance, during 2024–2025, rising prices of advanced processors, GPUs, high-speed networking components, and energy costs increased the total cost of ownership for several HPC deployments globally

- Complexity in managing massive computing clusters, high-speed data transfer, and parallel computing architectures requires specialized technical expertise and skilled professionals

- Limited availability of high-performance computing infrastructure in developing regions and lack of awareness about HPC capabilities can slow adoption among small enterprises and academic institutions

- Competition from cloud computing platforms, distributed computing frameworks, and edge computing technologies may create cost pressures and shift some workloads away from traditional on-premise HPC clusters

- To address these challenges, technology providers are focusing on cloud-based HPC services, energy-efficient system architectures, advanced cooling technologies, and scalable computing frameworks to improve accessibility and expand global adoption of High Performance Computing solutions

How is the High Performance Computing Market Segmented?

The market is segmented on the basis of components, deployment type, organization size, server price band, and application.

• By Components

On the basis of components, the high performance computing market is segmented into Solutions and Services. The Solutions segment dominated the market with a 68.4% share in 2025, as organizations continue to invest heavily in HPC infrastructure including high-performance servers, storage systems, networking technologies, and advanced software platforms. HPC solutions enable large-scale data processing, complex scientific simulations, and AI model training across research laboratories, government institutions, and enterprise environments. Increasing demand for GPU-accelerated systems, high-speed interconnect technologies, and scalable computing clusters further strengthens the adoption of HPC solutions globally. These systems are widely deployed to support advanced workloads such as weather modeling, genomic research, engineering simulations, and financial risk analysis.

The Services segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising demand for HPC consulting, system integration, performance optimization, and managed cloud HPC services that help organizations efficiently deploy and manage high-performance computing environments.

• By Deployment Type

On the basis of deployment type, the high performance computing market is segmented into On-Premises and On Cloud. The On-Premises segment dominated the market with a 59.2% share in 2025, primarily due to the need for high data security, low latency, and direct control over computing resources. Many government agencies, research institutions, and large enterprises prefer on-premise HPC infrastructure to handle sensitive workloads such as defense simulations, advanced engineering design, and confidential scientific research. On-premise HPC clusters provide higher computational reliability and performance consistency, which are critical for complex modeling and simulation tasks. In addition, organizations with established data centers often invest in dedicated HPC systems to support continuous high-performance workloads.

The On-Cloud segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing adoption of cloud-based HPC platforms that offer scalable computing power, flexible resource allocation, and lower infrastructure investment.

• By Organization Size

On the basis of organization size, the high performance computing market is segmented into Small and Medium-sized Enterprises (SMEs) and Large Enterprises. The Large Enterprises segment dominated the market with a 64.7% share in 2025, supported by their strong financial capacity to invest in advanced HPC infrastructure and computing clusters. Large enterprises across industries such as aerospace, automotive, pharmaceuticals, and energy rely heavily on HPC systems for product design simulations, large-scale analytics, and AI-based research initiatives. These organizations often operate dedicated data centers equipped with GPU clusters, high-speed storage, and advanced networking technologies to support complex computing workloads. The increasing integration of HPC with artificial intelligence and big data analytics further drives adoption among large corporations.

The SMEs segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by rising availability of cloud-based HPC services that allow smaller organizations to access high-performance computing resources without major infrastructure investments.

• By Server Price Band

On the basis of server price band, the high performance computing market is segmented into USD 250,000 to 500,000 and Above, USD 250,000 to 100,000, and Below. The USD 250,000 to 500,000 and Above segment dominated the market with a 44.9% share in 2025, as large-scale supercomputing systems and advanced HPC clusters require high-end hardware, including GPU accelerators, high-speed networking components, and large-capacity storage solutions. These premium systems are widely deployed in national laboratories, large research institutions, and enterprise data centers to support highly complex computational workloads such as climate modeling, nuclear simulations, and AI training. Their superior computing capability and scalability make them essential for high-intensity data processing tasks.

The USD 250,000 to 100,000 segment is projected to grow at the fastest CAGR from 2026 to 2033, driven by increasing demand for mid-range HPC systems among universities, research centers, and mid-sized enterprises seeking cost-efficient high-performance computing solutions.

• By Application

On the basis of application, the high performance computing market is segmented into Government and Defense, BFSI, Education and Research, Manufacturing, Media and Entertainment, Healthcare and Life Sciences, Energy and Utilities, Earth Sciences, and Others. The Education and Research segment dominated the market with a 28.6% share in 2025, driven by extensive use of HPC systems in scientific simulations, academic research projects, and large-scale data analysis. Universities, national laboratories, and research institutions rely heavily on HPC infrastructure for applications such as climate modeling, particle physics simulations, genomic sequencing, and space exploration research. Continuous investments in scientific computing infrastructure and collaborative global research initiatives further strengthen adoption in this segment.

The Healthcare and Life Sciences segment is expected to grow at the fastest CAGR from 2026 to 2033, propelled by increasing use of HPC for drug discovery, genomic research, molecular modeling, and advanced medical data analytics.

Which Region Holds the Largest Share of the High Performance Computing Market?

- North America dominated the high performance computing market with a 41.6% revenue share in 2025, driven by strong investments in advanced computing infrastructure, artificial intelligence research, cloud computing platforms, and large-scale data centers across the U.S. and Canada. High adoption of GPU-accelerated computing systems, supercomputing clusters, and AI training platforms continues to fuel demand for High Performance Computing across government research laboratories, aerospace and defence organizations, financial institutions, and technology enterprises

- Leading companies in North America are introducing next-generation supercomputing platforms, AI-optimized processors, high-speed networking technologies, and scalable cloud HPC services, strengthening the region’s technological leadership in high-performance computing systems. Continuous investment in quantum computing research, national supercomputing initiatives, and AI-driven data analytics further accelerates long-term market expansion

- Strong research ecosystems, presence of leading technology companies, and extensive investments in scientific computing infrastructure further reinforce regional market dominance in the global HPC industry

U.S. High Performance Computing Market Insight

The U.S. is the largest contributor in North America, supported by strong demand for large-scale computing infrastructure across scientific research, artificial intelligence development, weather forecasting, and national security applications. Major research laboratories, universities, and government agencies rely heavily on HPC systems to perform complex simulations, data analytics, and advanced modeling tasks. Increasing development of AI accelerators, high-performance processors, and GPU clusters further drives the need for powerful HPC platforms capable of handling massive computational workloads. Presence of leading technology companies, strong venture capital investments, and large-scale cloud computing infrastructure significantly contribute to the expansion of the HPC market across the country.

Canada High Performance Computing Market Insight

Canada contributes significantly to regional growth, driven by expanding research computing networks, national supercomputing initiatives, and rising investments in artificial intelligence and scientific computing infrastructure. Universities and government research institutions increasingly utilize HPC platforms for climate modeling, genomic research, engineering simulations, and large-scale data analysis. The country’s growing AI ecosystem, supported by government-funded research programs and strong academic collaborations, further strengthens demand for high-performance computing systems. In addition, increasing adoption of HPC in healthcare research, environmental science, and advanced manufacturing supports long-term growth of the High Performance Computing market in Canada.

Asia-Pacific High Performance Computing Market

Asia-Pacific is projected to register the fastest CAGR of 11.3% from 2026 to 2033, driven by rapid expansion of semiconductor manufacturing, strong growth in data center infrastructure, and increasing investments in national supercomputing programs across China, Japan, India, South Korea, and Southeast Asia. Rising adoption of artificial intelligence, big data analytics, and high-performance cloud computing is increasing demand for HPC systems across government research institutes, universities, and large enterprises. Rapid development of smart manufacturing, automotive innovation, and digital infrastructure further accelerates the need for advanced computing platforms capable of processing massive datasets efficiently.

China High Performance Computing Market Insight

China is the largest contributor to the Asia-Pacific HPC market, supported by massive government investments in national supercomputing programs, semiconductor innovation, and advanced AI research. The country continues to develop some of the world’s fastest supercomputers to support applications such as weather forecasting, aerospace engineering, defense simulations, and scientific research. Growing adoption of HPC in industrial automation, financial modeling, and digital technology development further strengthens market demand. Strong domestic manufacturing capacity and government-backed innovation policies continue to expand the country’s leadership in high-performance computing technologies.

Japan High Performance Computing Market Insight

Japan demonstrates steady growth in the HPC market, supported by advanced research infrastructure, high-tech manufacturing capabilities, and strong focus on scientific computing innovation. The country widely utilizes HPC platforms in automotive design simulations, pharmaceutical research, robotics development, and earthquake modeling. Japanese research institutions and technology companies are investing in next-generation supercomputers designed to deliver higher processing speed, energy efficiency, and AI acceleration capabilities. Continuous advancements in semiconductor technologies and strong government support for scientific research further contribute to sustained HPC market expansion.

India High Performance Computing Market Insight

India is emerging as a significant growth hub in the HPC market, driven by increasing investments in national supercomputing missions, artificial intelligence research, and digital infrastructure development. Government initiatives aimed at strengthening scientific research capabilities and promoting indigenous supercomputing development are expanding HPC adoption across academic institutions and research laboratories. Growing demand for HPC in pharmaceutical research, weather forecasting, financial analytics, and engineering simulations further drives market expansion. In addition, rapid growth of technology startups and data-driven industries supports the rising demand for high-performance computing platforms in India.

South Korea High Performance Computing Market Insight

South Korea plays an important role in the Asia-Pacific HPC market due to strong demand for high-performance computing across semiconductor manufacturing, artificial intelligence development, and advanced electronics research. The country’s leadership in memory chip production, consumer electronics, and telecommunications technologies requires powerful computing systems for complex simulations and product development. Increasing investments in AI research centers, data analytics platforms, and next-generation computing infrastructure continue to strengthen HPC adoption. Rapid digital transformation and strong government support for innovation further drive sustained growth of the High Performance Computing market in South Korea.

Which are the Top Companies in High Performance Computing Market?

The high performance computing industry is primarily led by well-established companies, including:

- IBM Corporation (U.S.)

- Amazon Web Services, Inc. (U.S.)

- Microsoft (U.S.)

- Hewlett Packard Enterprise Development LP (U.S.)

- IDG Communications, Inc. (U.S.)

- Sabalcore Computing, Inc. (Canada)

- Google LLC (U.S.)

- Penguin Computing (U.S.)

- Adaptive Computing (U.S.)

- Nimbix, Inc. (U.S.)

- The UberCloud (Germany)

- Dell Inc. (U.S.)

- Cisco Systems Inc. (U.S.)

- Hitachi, Ltd. (Japan)

- Advanced Micro Devices, Inc. (U.S.)

- Atos SE (France)

- NVIDIA Corporation (U.S.)

- Rescale, Inc. (U.S.)

- Hadean Supercomputing Ltd. (U.K.)

- Super Micro Computer, Inc. (U.S.)

What are the Recent Developments in Global High Performance Computing Market?

- In August 2025, IBM unveiled its latest quantum computing system designed to integrate seamlessly with its existing High Performance Computing (HPC) infrastructure, strengthening its ability to deliver advanced computational capabilities for complex scientific and enterprise workloads. This strategic development positions the company at the forefront of next-generation computing technologies while enhancing innovation in quantum-HPC hybrid systems

- In March 2025, Hewlett Packard Enterprise Development LP, in collaboration with the European Space Agency (ESA), inaugurated the Space HPC high-performance computing facility at ESA’s ESRIN center in Italy, aimed at accelerating research activities and supporting advanced space missions and Earth observation programs. This initiative significantly strengthens Europe’s space research infrastructure and drives innovation in scientific computing

- In March 2025, Axelera AI introduced its high-performance and energy-efficient Titania AI inference chiplet, developed using an innovative Digital In-Memory Computing (D-IMC) architecture and supported by €61.6 million in funding from the EuroHPC Joint Undertaking under the Digital Autonomy with RISC-V for Europe (DARE) project. This advancement is expected to enhance AI and HPC processing efficiency while accelerating innovation in European semiconductor technologies

- In November 2024, Fujitsu and Advanced Micro Devices, Inc. signed a memorandum of understanding to establish a strategic partnership focused on developing advanced computing platforms for artificial intelligence and High Performance Computing applications. This collaboration aims to deliver energy-efficient and open-source HPC solutions while accelerating global innovation in AI-driven computing technologies

- In March 2024, NVIDIA Corporation launched the GeForce RTX 5060 graphics processing unit based on the new NVIDIA Blackwell RTX architecture, delivering improved gaming and application performance through technologies such as ray tracing, neural shaders, DLSS 4 with Multi Frame Generation, and NVIDIA Reflex. This product introduction strengthens NVIDIA’s leadership in GPU innovation and expands its capabilities in high-performance computing and AI-driven graphics processing

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.