Global Highway Driving Assist Market

Market Size in USD Billion

CAGR :

%

USD

6.93 Billion

USD

39.11 Billion

2025

2033

USD

6.93 Billion

USD

39.11 Billion

2025

2033

| 2026 –2033 | |

| USD 6.93 Billion | |

| USD 39.11 Billion | |

| % | |

|

Highway Driving Assist Market Size

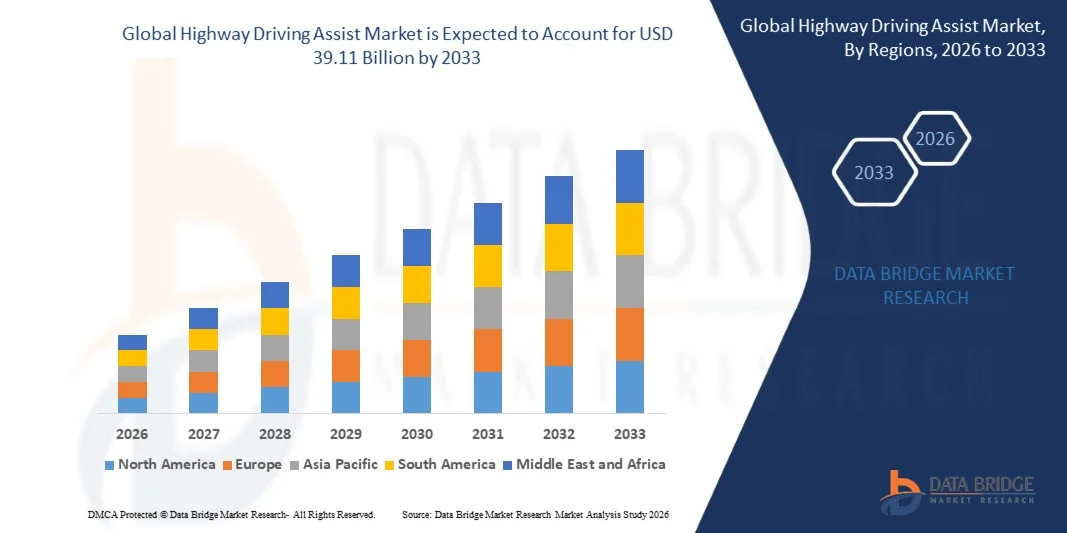

- The global highway driving assist market size was valued at USD 6.93 billion in 2025 and is expected to reach USD 39.11 billion by 2033, at a CAGR of 24.15% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced driver assistance systems and continuous technological advancements in automotive electronics, leading to enhanced vehicle automation and improved safety features across passenger and commercial vehicles

- Furthermore, rising consumer demand for safer, more convenient, and semi-autonomous driving experiences is establishing highway driving assist systems as a critical component of modern mobility solutions. These converging factors are accelerating the integration of intelligent driving technologies, thereby significantly boosting the industry's growth

Highway Driving Assist Market Analysis

- Highway driving assist systems, enabling automated control of steering, acceleration, and braking under specific highway conditions, are becoming essential components of next-generation vehicles due to their ability to enhance driving comfort, reduce driver fatigue, and improve overall road safety

- The escalating demand for highway driving assist systems is primarily fueled by increasing focus on vehicle safety, rapid advancements in sensor and software technologies, and growing adoption of connected and electric vehicles across global automotive markets

- Asia-Pacific dominated the highway driving assist market with a share of 37.48% in 2025, due to strong growth in automotive production, rising adoption of advanced driver assistance systems, and increasing demand for connected and intelligent vehicles

- North America is expected to be the fastest growing region in the highway driving assist market during the forecast period due to strong demand for advanced vehicle safety systems and increasing adoption of semi-autonomous driving technologies

- Luxury segment dominated the market with a market share of 49.1% in 2025, due to the early adoption of advanced driver assistance technologies and higher consumer willingness to pay for enhanced safety and comfort features. Premium automakers consistently integrate highway driving assist systems as standard or optional offerings, supported by strong R&D capabilities and brand positioning around innovation

Report Scope and Highway Driving Assist Market Segmentation

|

Attributes |

Highway Driving Assist Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· DENSO CORPORATION (Japan) · Valeo (France) · Magna International Inc. (Canada) · Aptiv plc (Ireland) · AVL List GmbH (Austria) · Continental AG (Germany) · Robert Bosch GmbH (Germany) · ZF Friedrichshafen AG (Germany) · Samsung Electro-Mechanics (South Korea) · Tesla, Inc. (U.S.) · Toyota Motor Corporation (Japan) · HELLA GmbH & Co. KGaA (Germany) · Hyundai Mobis (South Korea) · Visteon Corporation (U.S.) · NVIDIA Corporation (U.S.) · Qualcomm Technologies, Inc. (U.S.) · Toshiba Corporation (Japan) · Panasonic Corporation (Japan) |

|

Market Opportunities |

· Expansion Opportunities in Autonomous Freight and Logistics Applications · Growing Adoption in Emerging Markets with Expanding Highway Infrastructure |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

Highway Driving Assist Market Trends

“Increasing Integration of AI and Sensor Fusion in Highway Driving Assist Systems”

- A significant trend in the highway driving assist market is the increasing integration of artificial intelligence and sensor fusion technologies, driven by the need for more accurate real-time decision-making and enhanced vehicle autonomy on highways. This integration is strengthening the capability of driver assistance systems to interpret complex traffic environments and support safer long-distance driving experiences

- For instance, companies such as Tesla and BMW deploy advanced sensor fusion systems combining cameras, radar, and AI algorithms in their highway driving assist features to enable lane centering, adaptive cruise control, and automated lane changes. These systems enhance driving precision and reduce driver workload during extended highway travel

- The growing deployment of multi-sensor architectures is improving system reliability by enabling vehicles to cross-verify data from different sensing technologies. This approach minimizes errors in object detection and enhances performance in varying weather and lighting conditions

- Automakers are increasingly embedding AI-driven predictive analytics into highway driving assist systems to anticipate driver behavior and traffic flow patterns. This enables smoother navigation and proactive adjustments in speed and positioning on highways

- The integration of high-definition mapping and connectivity features is supporting more accurate localization and route planning for assisted driving systems. This is enhancing system efficiency and enabling better coordination with real-time traffic data

- Technology providers are focusing on developing scalable and modular sensor fusion platforms that can be integrated across multiple vehicle segments. This is contributing to broader adoption of highway driving assist systems and strengthening their role in advancing semi-autonomous mobility solutions

Highway Driving Assist Market Dynamics

Driver

“Rising Demand for Enhanced Road Safety and Driver Convenience”

- The rising demand for improved road safety and driver convenience is a major driver in the highway driving assist market, as consumers and regulators increasingly prioritize technologies that reduce accidents and enhance driving comfort. These systems help maintain safe distances, control vehicle speed, and assist in lane management, reducing the likelihood of human error

- For instance, organizations such as the European New Car Assessment Programme (Euro NCAP) promote the adoption of advanced driver assistance systems including highway assist features by incorporating them into vehicle safety ratings. This encourages automakers to integrate such systems to meet safety standards and improve vehicle appeal

- The increasing volume of highway traffic is intensifying the need for automated assistance systems that can reduce driver fatigue during long-distance travel. This is driving higher adoption of features such as adaptive cruise control and lane keeping assistance

- Consumers are showing greater preference for vehicles equipped with intelligent assistance systems that simplify driving tasks and enhance overall comfort. This shift in preference is influencing manufacturers to prioritize the integration of highway driving assist technologies

- The continued focus on reducing road fatalities and improving driving efficiency is reinforcing the importance of highway driving assist systems. This driver is sustaining long-term market growth and encouraging continuous innovation in assisted driving technologies

Restraint/Challenge

“High System Costs and Regulatory Complexity”

- The highway driving assist market faces significant challenges due to the high costs associated with advanced sensors, computing systems, and software development required for effective implementation. These cost factors limit accessibility, particularly in price-sensitive vehicle segments

- For instance, companies such as Waymo invest heavily in developing advanced autonomous driving technologies that rely on expensive sensor suites and complex software systems. These investments increase overall system costs and create barriers for widespread commercialization in conventional vehicles

- The integration of multiple sensing technologies and high-performance processors adds complexity to vehicle design and increases production expenses. This makes it challenging for manufacturers to maintain competitive pricing while offering advanced features

- Regulatory frameworks governing autonomous and semi-autonomous driving vary across regions, creating compliance challenges for automakers. These differences require extensive testing, validation, and certification processes before deployment

- The combined impact of high costs and complex regulatory requirements is limiting rapid adoption of highway driving assist systems. These challenges are compelling industry players to focus on cost optimization and regulatory alignment to support broader market expansion

Highway Driving Assist Market Scope

The market is segmented on the basis of car type, electric vehicle type, component, autonomous level, and function.

- By Car Type

On the basis of car type, the highway driving assist market is segmented into mid segment and luxury segment. The luxury segment dominated the market with the largest revenue share of 49.1% in 2025, driven by the early adoption of advanced driver assistance technologies and higher consumer willingness to pay for enhanced safety and comfort features. Premium automakers consistently integrate highway driving assist systems as standard or optional offerings, supported by strong R&D capabilities and brand positioning around innovation. The presence of high-end sensors, advanced software integration, and seamless connectivity in luxury vehicles further strengthens segment dominance. In addition, stricter safety expectations among premium vehicle buyers continue to accelerate the inclusion of such systems.

The mid segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by increasing affordability of ADAS technologies and their gradual penetration into mass-market vehicles. Automakers are focusing on cost optimization and platform standardization to introduce highway driving assist features in mid-range models. Rising consumer awareness regarding vehicle safety and government regulations mandating safety features are supporting adoption. Improvements in sensor cost efficiency and software scalability are enabling broader deployment. This segment is expected to expand rapidly as technology becomes more accessible across price-sensitive markets.

- By Electric Vehicle Type

On the basis of electric vehicle type, the highway driving assist market is segmented into BEV, HEV, PHEV, and FCEV. The BEV segment dominated the market in 2025 due to its strong alignment with advanced digital architectures and centralized electronic systems, which support seamless integration of highway driving assist features. Battery electric vehicles are often designed with next-generation platforms that accommodate sophisticated sensor suites and real-time data processing capabilities. Automakers prioritize ADAS deployment in BEVs to enhance driving efficiency and differentiate their offerings in a competitive EV market. The integration of over-the-air updates further strengthens system performance and feature upgrades.

The PHEV segment is projected to witness the fastest growth rate from 2026 to 2033, driven by its transitional role between conventional and fully electric vehicles. Increasing consumer preference for flexible powertrain options is encouraging automakers to equip PHEVs with advanced driving assistance systems. These vehicles benefit from both electric and combustion-based architectures, enabling wider adoption across varied driving conditions. Growing investments in hybrid technologies and regulatory incentives are supporting market expansion. Enhanced compatibility with ADAS features is expected to accelerate growth in this segment.

- By Component

On the basis of component, the highway driving assist market is segmented into camera, radar, ultrasonic sensor, software module, and navigation. The radar segment dominated the market in 2025 owing to its reliability in detecting objects over long distances and its effectiveness under diverse weather conditions. Radar sensors play a critical role in adaptive cruise control and collision avoidance functions, ensuring consistent performance even in low visibility environments. Automakers rely heavily on radar for its accuracy and robustness in high-speed highway scenarios. Continuous advancements in radar technology are improving detection precision and reducing system costs.

The software module segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing importance of data processing, artificial intelligence, and system integration. Software acts as the core enabler of highway driving assist functionalities by interpreting sensor data and executing real-time decisions. Growing adoption of machine learning algorithms and cloud connectivity is enhancing system intelligence and adaptability. Automakers are investing heavily in proprietary software platforms to differentiate their offerings. The shift toward software-defined vehicles is expected to accelerate segment growth significantly.

- By Autonomous Level

On the basis of autonomous level, the highway driving assist market is segmented into Level 2, Level 3, and above. The Level 2 segment dominated the market in 2025 due to its widespread commercial availability and regulatory acceptance across major automotive markets. These systems offer partial automation features such as steering and acceleration control while requiring driver supervision, making them practical for current infrastructure conditions. Automakers are actively deploying Level 2 systems as standard features in many vehicles. Consumer familiarity and affordability further contribute to the dominance of this segment.

The Level 3 and above segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by advancements in sensor fusion, AI capabilities, and regulatory approvals in select regions. These systems enable conditional automation, allowing drivers to disengage from certain driving tasks under specific conditions. Increasing investments in autonomous driving technologies and pilot deployments are supporting growth. Improvements in safety validation and infrastructure readiness are accelerating adoption. This segment is expected to gain momentum as technological and legal barriers continue to evolve.

- By Function

On the basis of function, the highway driving assist market is segmented into adaptive cruise control, lane keeping assist, lane centering assist, and collision avoidance assist. The adaptive cruise control segment dominated the market in 2025 due to its essential role in maintaining safe distances between vehicles during highway driving. This function is widely adopted as a foundational feature in most highway driving assist systems, offering improved driving comfort and reduced driver fatigue. Its compatibility with other ADAS features further strengthens its importance. Automakers prioritize adaptive cruise control as a standard offering across multiple vehicle categories.

The lane centering assist segment is projected to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for enhanced vehicle stability and automation in highway environments. This function provides continuous steering support to keep the vehicle centered within lanes, improving safety and driving precision. Advancements in camera and sensor technologies are enhancing system accuracy and responsiveness. Growing consumer preference for semi-autonomous driving experiences is accelerating adoption. Integration with higher-level automation systems is expected to further boost segment growth.

Highway Driving Assist Market Regional Analysis

- Asia-Pacific dominated the highway driving assist market with the largest revenue share of 37.48% in 2025, driven by strong growth in automotive production, rising adoption of advanced driver assistance systems, and increasing demand for connected and intelligent vehicles

- The region benefits from large-scale vehicle manufacturing, cost-efficient component production, and rapid integration of electronic and sensor-based technologies across passenger vehicles

- Rising urbanization, expanding middle-class population, and growing emphasis on vehicle safety features are accelerating market expansion across key economies

China Highway Driving Assist Market Insight

China held the largest share in the Asia-Pacific highway driving assist market in 2025, supported by its strong automotive manufacturing ecosystem and rapid adoption of smart mobility technologies. The country has a well-developed supply chain for sensors, semiconductors, and automotive electronics, enabling large-scale deployment of highway driving assist systems. Strong domestic demand for connected and electric vehicles is further driving adoption. In addition, government support for autonomous driving development and smart transportation infrastructure is strengthening China’s leadership in this market.

India Highway Driving Assist Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by increasing vehicle production, rising awareness regarding road safety, and growing demand for advanced in-vehicle technologies. Government initiatives promoting vehicle safety standards and domestic automotive manufacturing are supporting market growth. Expanding adoption of connected car features and digital technologies is further enhancing demand. In addition, increasing investments by global and domestic automakers in advanced driver assistance systems are accelerating long-term market expansion.

Europe Highway Driving Assist Market Insight

The Europe highway driving assist market is expanding steadily, supported by strong demand for premium vehicles, strict safety regulations, and high adoption of advanced driver assistance technologies. The region emphasizes vehicle safety and automation, encouraging integration of highway driving assist systems across various vehicle categories. Stringent regulatory frameworks are pushing automakers to include advanced safety features. In addition, continuous advancements in automotive electronics and autonomous driving technologies are enhancing market growth.

Germany Highway Driving Assist Market Insight

Germany accounted for the largest share in the Europe highway driving assist market in 2025, driven by its strong automotive manufacturing base and leadership in engineering innovation. The country has extensive adoption of advanced driver assistance systems across both premium and mid-segment vehicles. Strong R&D capabilities and presence of leading automotive OEMs are supporting continuous technological advancements. In addition, integration of high-performance sensors and software systems is reinforcing Germany’s dominance in the regional market.

U.K. Highway Driving Assist Market Insight

The U.K. market is supported by increasing adoption of connected vehicles and growing focus on automotive safety technologies. Strong investments in autonomous driving research and testing are driving innovation in highway driving assist systems. The country’s regulatory support for advanced vehicle technologies is encouraging adoption across vehicle segments. In addition, collaborations between automotive companies and technology firms are further supporting market development.

North America Highway Driving Assist Market Insight

North America is projected to grow at the fastest CAGR from 2026 to 2033, driven by strong demand for advanced vehicle safety systems and increasing adoption of semi-autonomous driving technologies. High consumer preference for technologically advanced vehicles is supporting integration of highway driving assist features. Continuous innovation in sensor technologies and software platforms is enhancing system capabilities. In addition, strong presence of leading automotive and technology companies is accelerating regional growth.

U.S. Highway Driving Assist Market Insight

The U.S. accounted for the largest share in the North America highway driving assist market in 2025, supported by high adoption of advanced driver assistance systems and strong demand for connected vehicles. The country benefits from a robust technology ecosystem and significant investments in autonomous driving development. Highway driving assist features are increasingly integrated across both premium and mid-range vehicles. In addition, regulatory support and ongoing advancements in artificial intelligence and vehicle automation are reinforcing the U.S. leadership in the regional market.

Highway Driving Assist Market Share

The highway driving assist industry is primarily led by well-established companies, including:

- DENSO CORPORATION (Japan)

- Valeo (France)

- Magna International Inc. (Canada)

- Aptiv plc (Ireland)

- AVL List GmbH (Austria)

- Continental AG (Germany)

- Robert Bosch GmbH (Germany)

- ZF Friedrichshafen AG (Germany)

- Samsung Electro-Mechanics (South Korea)

- Tesla, Inc. (U.S.)

- Toyota Motor Corporation (Japan)

- HELLA GmbH & Co. KGaA (Germany)

- Hyundai Mobis (South Korea)

- Visteon Corporation (U.S.)

- NVIDIA Corporation (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Toshiba Corporation (Japan)

- Panasonic Corporation (Japan)

Latest Developments in Global Highway Driving Assist Market

- In October 2025, Tesla expanded its Full Self-Driving capabilities with enhanced highway driving assist features, including improved lane navigation and traffic-aware cruise control, which is strengthening its leadership in semi-autonomous driving technologies and accelerating large-scale real-world data collection to refine system performance. This development is increasing competitive pressure on automakers to enhance their ADAS offerings while driving faster consumer adoption of intelligent highway driving solutions across both premium and mid-range vehicles

- In September 2025, Qualcomm and BMW introduced an advanced automated driving suite featuring hands-free highway assist, automatic lane changes, and self-parking capabilities, which is driving deeper integration between semiconductor platforms and automotive systems. This collaboration is enabling scalable, high-performance computing for real-time decision-making, thereby accelerating deployment of advanced highway driving assist features and strengthening the overall ecosystem for software-defined vehicles

- In July 2025, Lucid Motors launched a subscription-based hands-free highway assist system for its Air and Gravity models equipped with DreamDrive Pro, which is transforming the revenue model for ADAS features by shifting toward software-driven monetization. This approach is increasing accessibility of advanced driving capabilities while allowing continuous feature upgrades through over-the-air updates, thereby enhancing customer engagement and supporting long-term market growth

- In March 2025, Rivian rolled out its Enhanced Highway Assist system that supports steering, acceleration, and braking on designated roads, which is strengthening its competitive position in the electric vehicle segment through advanced safety and automation features. This development is encouraging broader adoption of highway driving assist technologies among EV manufacturers and is contributing to increased standardization of semi-autonomous capabilities across emerging vehicle platforms

- In February 2025, Stellantis introduced STLA AutoDrive 1.0, its first in-house Level 3 highway automation system enabling hands-free and eyes-off driving, which represents a major advancement toward conditional automation in mass-market vehicles. This launch is accelerating industry progress toward higher autonomy levels while supporting regulatory evolution and boosting consumer confidence in next-generation highway driving assist systems

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.