Global Huber Needles Market

Market Size in USD Million

CAGR :

%

USD

47.25 Million

USD

67.81 Million

2025

2033

USD

47.25 Million

USD

67.81 Million

2025

2033

| 2026 –2033 | |

| USD 47.25 Million | |

| USD 67.81 Million | |

| % | |

|

Huber Needles Market Size

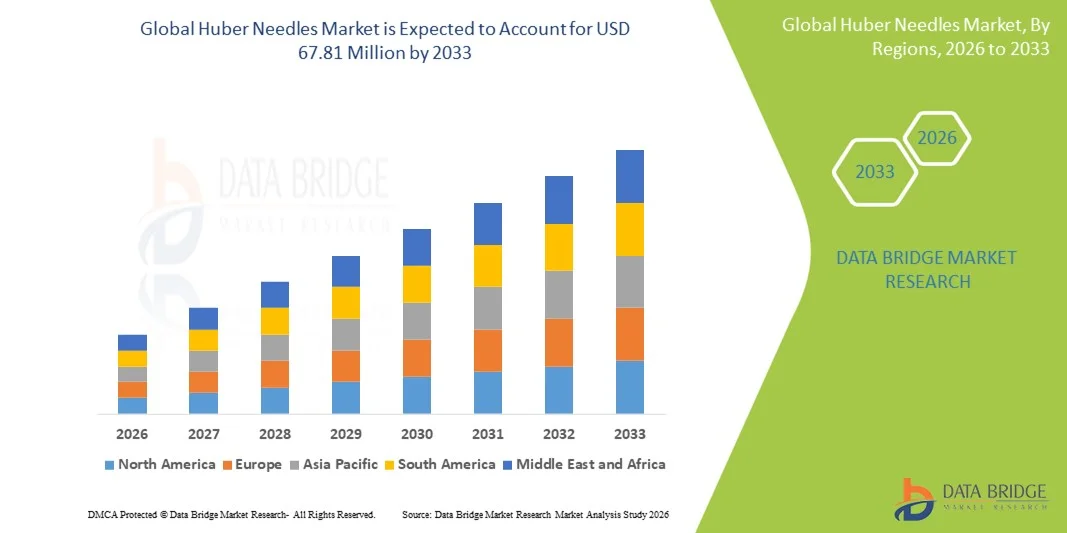

- The global huber needles market size was valued at USD 47.25 Million in 2025 and is expected to reach USD 67.81 Million by 2033, at a CAGR of 4.62% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic diseases requiring long-term intravenous therapies, rising adoption of chemotherapy and parenteral drug administration, and technological advancements in Huber needle design, including safety features, coatings, and improved durability

- Furthermore, growing patient awareness about infection prevention and demand for safer, more efficient vascular access devices are establishing Huber needles as a preferred choice for central venous access procedures. These factors are accelerating the uptake of Huber Needle solutions, thereby significantly boosting the Huber Needles Market growth

Huber Needles Market Analysis

- Huber needles, specialized medical devices used for safe and efficient vascular access, are increasingly vital components in oncology, hematology, and long-term infusion therapies in both hospitals and home care settings due to their enhanced safety features, ease of use, and compatibility with implantable ports

- The escalating demand for Huber needles is primarily fueled by the growing prevalence of chronic diseases, increasing adoption of chemotherapy and parenteral therapies, rising awareness about infection prevention, and a preference for safer, more durable vascular access solutions

- North America dominated the huber needles market with the largest revenue share of approximately 38.5% in 2025, characterized by advanced healthcare infrastructure, high adoption of central venous access devices, and a strong presence of key medical device manufacturers, with the U.S. experiencing substantial growth due to widespread use in oncology and home infusion therapies

- Asia-Pacific is expected to be the fastest-growing region in the huber needles market during the forecast period, registering a CAGR of around 12.8%, driven by increasing prevalence of chronic diseases, expanding healthcare infrastructure, and growing awareness of safe vascular access procedures

- The curved Huber needles segment dominated the market with a revenue share of 57.4% in 2025, driven by their superior ergonomics and clinical precision

Report Scope and Huber Needles Market Segmentation

|

Attributes |

Huber Needles Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• B. Braun S.E. (Germany) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Huber Needles Market Trends

Rising Demand for Safe and Efficient Drug Delivery Systems

- A notable trend in the global Huber Needles market is the increasing focus on precision and safety in medical procedures, particularly in oncology, parenteral therapies, and long-term infusion treatments. Huber needles are gaining widespread adoption due to their ability to provide leak-free access to implantable ports, ensuring accurate drug administration and minimizing patient discomfort

- For instance, in hospitals and outpatient care centers, Huber needles are being increasingly used for chemotherapy administration, total parenteral nutrition (TPN), and other long-term intravenous therapies. Their unique non-coring design reduces the risk of damage to port septa and enhances overall patient safety

- The growing emphasis on home healthcare and outpatient treatment is also driving the adoption of Huber needles, as they provide convenient, reliable, and low-risk options for patients requiring regular infusion therapy. Manufacturers are innovating with ergonomic designs, varying gauge sizes, and safety-engineered features to enhance user comfort and procedural efficiency

- In addition, rising investments in healthcare infrastructure and increased adoption of minimally invasive procedures across emerging economies are contributing to market growth. Training programs and awareness initiatives for healthcare professionals regarding safe port access techniques are further supporting the widespread utilization of Huber needles

- Global research and development efforts are focused on improving material biocompatibility, sterility, and needle durability, ensuring Huber needles remain the preferred choice in clinical settings worldwide. These advancements help reduce complications, improve treatment outcomes, and enhance patient satisfaction

Huber Needles Market Dynamics

Driver

Increasing Prevalence of Chronic Diseases and Oncology Treatments

- The growing incidence of cancer, chronic illnesses, and conditions requiring long-term intravenous therapy is a key driver for the Huber needles market. The need for safe, reliable, and minimally invasive vascular access devices is increasing across hospitals, clinics, and home healthcare settings globally

- For instance, chemotherapy administration and long-term infusion treatments rely heavily on implantable ports accessed using Huber needles, highlighting the critical role of these devices in patient care

- Furthermore, the expansion of outpatient treatment centers and home infusion services is fueling demand, as Huber needles enable healthcare providers to deliver precise therapy while minimizing complications and discomfort

- The rising adoption of automated infusion systems and combination therapies in modern healthcare practices is also encouraging the use of high-quality, reliable Huber needle

- Overall, global awareness regarding safe drug administration, coupled with a focus on improving patient outcomes, continues to drive market growth

Restraint/Challenge

High Cost of Advanced Needles and Limited Awareness in Emerging Markets

- The relatively high cost of premium Huber needles compared to standard intravenous needles can limit their adoption, particularly in resource-constrained regions or smaller clinics. Advanced safety features, specialized materials, and ergonomic designs often add to production costs

- For instance, hospitals in developing countries may opt for more affordable alternatives due to budget limitations, even though these options may not provide the same level of precision or safety

- In addition, lack of awareness and training among healthcare professionals in certain regions about the advantages and proper use of Huber needles can slow market penetration. Improper handling or limited knowledge about the non-coring design may reduce the perceived benefits of these devices

- Challenges such as maintaining sterility, preventing infections, and ensuring compatibility with various implantable ports also require careful handling and quality control, adding to operational considerations

- Overcoming these barriers through educational initiatives, cost-effective manufacturing techniques, and global distribution strategies will be essential to expand the reach of Huber needles and sustain market growth

Huber Needles Market Scope

The Huber Needles market is segmented into notable segments based on product type, application, and end user.

- By Product Type

On the basis of product type, the market is segmented into curved Huber needles and straight Huber needles. The curved Huber needles segment dominated the market with a revenue share of 57.4% in 2025, driven by their superior ergonomics and clinical precision. Curved needles are preferred for long-term vascular access procedures such as hemodialysis and oncology drug delivery due to reduced patient discomfort and lower risk of vascular trauma. Hospitals and oncology centers are major end users, contributing to consistent demand. The design allows accurate catheter insertion and improved stability during procedures, enhancing clinician preference. Adoption is further supported by compatibility with a wide range of implanted ports and infusion systems. Continuous innovations in needle coatings and materials improve safety and reduce infection risk. Strong adoption in home care nutrition and lap-band adjustments also reinforces dominance. Regulatory approvals in North America and Europe for safety and sterility standards enhance market confidence.

The straight Huber needles segment is expected to witness the fastest CAGR of 9.8% from 2026 to 2033, fueled by growing demand in home parenteral nutrition and outpatient care settings. Straight needles are favored for shorter procedures and quick access interventions, making them ideal for home care and emergency use. Increasing prevalence of chronic diseases, cancer treatment procedures, and dialysis sessions contributes to growth. Technological improvements such as anti-coring designs and high-quality stainless steel manufacturing further drive adoption. Rising healthcare infrastructure in emerging economies also supports market expansion. Growth is accelerated by increasing home healthcare services, remote patient management programs, and minimally invasive clinical practices.

- By Application

On the basis of application, the market is segmented into dialysis, blood transfusions, IV cancer application, lap-band adjustments, home parenteral nutrition, and others. The dialysis segment accounted for the largest revenue share of 44.1% in 2025, due to the high prevalence of chronic kidney disease and the widespread need for repeated vascular access in hemodialysis treatments. Hospitals and dialysis centers remain primary end users, with standardization of port access procedures driving adoption. The durability and safety of Huber needles reduce complications like infection and thrombosis, reinforcing preference. Technological advancements such as improved needle coatings and anti-coring tips enhance patient safety and clinical efficiency. Adoption is supported by established reimbursement policies and increasing awareness among nephrologists and healthcare professionals. Rising geriatric population and kidney transplant programs globally further sustain market dominance.

The home parenteral nutrition segment is expected to witness the fastest CAGR of 10.2% from 2026 to 2033, driven by rising chronic gastrointestinal disorders and patient preference for home-based care. Nano-coated Huber needles and patient-friendly designs improve comfort and adherence. Expansion of home healthcare services and remote monitoring programs enhances uptake. Increasing awareness among caregivers and healthcare providers about safe administration practices supports adoption. The segment also benefits from technological innovations that reduce complications and improve delivery efficiency. Growth is prominent in North America and Europe due to advanced healthcare infrastructure and increasing patient empowerment.

- By End User

On the basis of end user, the market is segmented into hospitals, oncology centers, clinics, ambulatory surgical centers, home care settings, and others. The hospitals segment dominated with a market share of 52.6% in 2025, owing to high procedural volumes, repeated vascular access requirements, and the availability of skilled clinical staff. Hospitals serve as primary procurement centers for Huber needles across applications including dialysis, oncology, and transfusions. Standardized protocols, safety compliance, and regulatory approvals enhance adoption. Hospitals also drive innovation adoption, integrating advanced needles with implanted port systems. High patient turnover and repeat treatment cycles ensure steady demand.

The home care settings segment is expected to witness the fastest CAGR of 11.4% from 2026 to 2033, due to the rising trend of at-home treatment for cancer, nutrition therapy, and chronic illness management. Patient-friendly designs, comfort, and minimally invasive administration contribute to growing acceptance. Expansion of home healthcare networks and reimbursement policies in developed regions further accelerate growth. Technological advances such as needle safety features and ease of use for caregivers enhance adoption. Increased patient awareness, convenience, and cost-effectiveness of home treatments also support segment growth.

Huber Needles Market Regional Analysis

- North America dominated the huber needles market, accounting for approximately 38.9% of the global revenue share in 2025

- The region’s leadership is supported by advanced healthcare infrastructure, high procedural volumes in hospitals and oncology centers

- Widespread adoption of minimally invasive and catheter-based therapies, and the strong presence of leading medical device manufacturers

U.S. Huber Needles Market Insight

The U.S. huber needles market held the largest share within North America in 2025, driven by high usage in hospitals, outpatient clinics, and homecare settings. Factors such as well-established enteral therapy protocols, increasing focus on patient safety, and robust adoption of advanced Huber needle designs significantly contributed to market growth. Furthermore, the presence of major domestic manufacturers and increasing hospital and homecare procurement of Huber needles accelerated the demand in the country.

Europe Huber Needles Market Insight

The Europe huber needles market is projected to expand at a substantial CAGR during the forecast period. Growth is primarily driven by increasing awareness of patient safety, rising adoption of advanced intravenous and enteral devices, and expanding hospital and homecare infrastructure. The market is witnessing strong growth in countries such as the U.K. and Germany, where advanced healthcare facilities, favorable reimbursement policies, and high procedural volumes support adoption.

U.K. Huber Needles Market Insight

The U.K. huber needles market is anticipated to grow at a notable CAGR, fueled by the country’s well-established healthcare system, increasing hospital and homecare usage, and adoption of modern minimally invasive devices. The emphasis on patient safety, coupled with growing outpatient care facilities, is driving demand for Huber needles across hospitals and clinics.

Germany Huber Needles Market Insight

Germany huber needles market is expected to witness considerable growth in the Huber Needles market during the forecast period, supported by advanced healthcare infrastructure, high awareness regarding safe infusion devices, and a strong focus on innovation in medical technology. Hospitals and specialty clinics are increasingly incorporating Huber needles into routine care protocols, promoting market expansion.

Asia-Pacific Huber Needles Market Insight

The Asia-Pacific huber needles market is poised to grow at the fastest CAGR during the forecast period, driven by increasing healthcare expenditure, expanding hospital networks, rising procedural volumes, and growing awareness of advanced homecare and enteral therapies. Countries such as China, Japan, and India are emerging as key markets, supported by rapid urbanization, increasing disposable incomes, and the growing adoption of modern Huber needle devices in both hospitals and homecare settings.

Japan Huber Needles Market Insight

The Japan huber needles market is gaining momentum due to a technologically advanced healthcare system, rising patient safety awareness, and increasing use of outpatient and homecare infusion therapies. The aging population further contributes to demand for reliable and easy-to-use Huber needles, promoting steady market growth in both hospital and homecare applications.

China Huber Needles Market Insight

China huber needles market accounted for the largest revenue share in the Asia-Pacific region in 2025. Market growth is attributed to rapid urbanization, a growing middle-class population, rising healthcare expenditure, and strong adoption of modern medical devices in hospitals and homecare. The expansion of domestic manufacturers and increasing penetration of Huber needles in oncology, chemotherapy, and enteral therapy applications are key drivers of market growth.

Huber Needles Market Share

The Huber Needles industry is primarily led by well-established companies, including:

• B. Braun S.E. (Germany)

• Teleflex Incorporated (U.S.)

• Smiths Medical (U.K.)

• AngioDynamics, Inc. (U.S.)

• Nipro Corporation (Japan)

• Terumo Corporation (Japan)

• Cook Medical (U.S.)

• Medtronic plc (Ireland)

• Vygon SA (France)

• Argon Medical Devices, Inc. (U.S.)

• ICU Medical, Inc. (U.S.)

• Polymedicure Ltd. (India)

• Merit Medical Systems, Inc. (U.S.)

• Galt Medical Corp. (U.S.)

Latest Developments in Global Huber Needles Market

- In January 2024, **Nipro Corporation expanded its Huber needle product portfolio with a new range of single‑use, safety‑engineered Huber needles designed to reduce needlestick injuries and improve safety for clinicians. The expanded lineup emphasized enhanced protection features and broader applications in oncology and dialysis treatments, reflecting industry focus on safety and preventive healthcare

- In October 2024, MedSafety Solutions introduced the TwoFer™ Needle, a dual‑purpose Huber‑tipped needle that enables both vented and non‑vented vial transfers without changing needles. This product was launched to streamline workflows and improve efficiency and safety in pharmaceutical handling and clinical settings, representing a notable innovation in the Huber needles segment

- In January 2025, **BD (Becton, Dickinson and Company) announced it was investing over USD 10 million to expand manufacturing operations in its Connecticut and Nebraska plants in the United States. The expansion includes new production lines for critical vascular access devices such as Huber needles, addressing increased demand driven by oncology treatments and home infusion care

- In March 2025, a new Safety Huber Needle with an integrated needlestick prevention mechanism received notice in the U.S. FDA 510(k) database, featuring manually activated protective shielding that significantly reduces accidental needlestick injuries and enhances healthcare worker safety during port access procedures

- In July 2025, industry insights reported that **Becton Dickinson launched a novel ergonomic curved Huber needle variant designed to reduce patient discomfort and improve precision when accessing implanted ports during long‑term infusion therapies. This product release underlined ongoing manufacturer emphasis on comfort, usability, and safety in advanced vascular access devices

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.