Global Iga Nephropathy Market

Market Size in USD Million

CAGR :

%

USD

178.25 Million

USD

771.56 Million

2025

2033

USD

178.25 Million

USD

771.56 Million

2025

2033

| 2026 –2033 | |

| USD 178.25 Million | |

| USD 771.56 Million | |

| % | |

|

Immunoglobulin A (IgA) Nephropathy Market Size

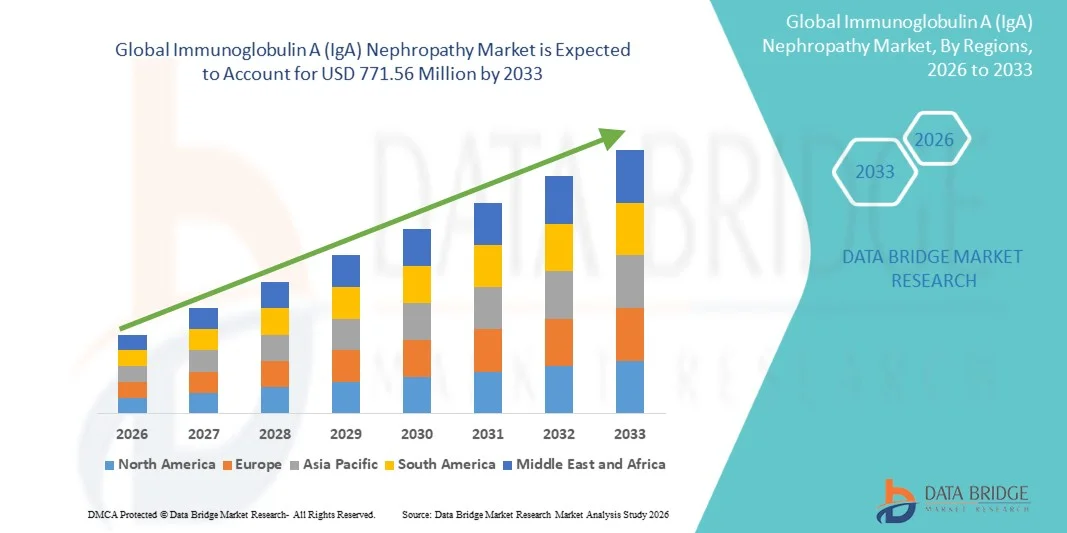

- The global Immunoglobulin A (IgA) Nephropathy market size was valued at USD 178.25 Million in 2025and is expected to reach USD 771.56 Million by 2033, at a CAGR of 20.10% during the forecast period

- The market growth is largely fueled by the increasing prevalence of chronic kidney disorders and rising awareness regarding autoimmune renal diseases, leading to greater demand for advanced nephrology treatments and targeted therapeutic solutions across healthcare systems

- Furthermore, growing investments in biologic drug development, increasing adoption of precision medicine, and rising demand for effective long-term renal disease management are establishing innovative therapies as the preferred treatment approach for Immunoglobulin A Nephropathy. These converging factors are accelerating the uptake of Immunoglobulin A (IgA) Nephropathy treatment solutions, thereby significantly boosting the industry’s growth

Immunoglobulin A (IgA) Nephropathy Market Analysis

- Immunoglobulin A Nephropathy therapeutics are increasingly vital in nephrology care due to their ability to manage kidney inflammation, slow disease progression, and improve long-term renal outcomes across hospitals and specialty clinics

- The escalating demand for Immunoglobulin A (IgA) Nephropathy treatments is primarily fueled by the rising prevalence of chronic kidney diseases, growing awareness regarding autoimmune renal disorders, and increasing adoption of targeted biologics and immunosuppressive therapies

- North America dominated the immunoglobulin A (IgA) nephropathy market with the largest revenue share of 43.1% in 2025, characterized by advanced healthcare infrastructure, strong rare disease research capabilities, and a robust presence of leading biopharmaceutical companies, with the U.S. experiencing substantial growth in the adoption of novel nephrology therapies driven by increasing clinical trials and regulatory approvals for targeted renal treatments

- Asia-Pacific is expected to be the fastest growing region in the immunoglobulin A (IgA) nephropathy market during the forecast period due to increasing healthcare expenditure, rising awareness regarding kidney disease management, and improving access to specialty nephrology care

- The adults segment held the largest market revenue share of 81.2% in 2025, driven by the higher prevalence of IgA nephropathy among the adult population and increasing incidence of chronic kidney disorders linked to hypertension and metabolic diseases

Report Scope and Immunoglobulin A (IgA) Nephropathy Market Segmentation

|

Attributes |

Immunoglobulin A (IgA) Nephropathy Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Novartis AG (Switzerland) |

|

Market Opportunities |

· Increasing development of targeted biologics and precision therapies for autoimmune kidney disorders · Rising awareness regarding early diagnosis of chronic kidney diseases |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Immunoglobulin A (IgA) Nephropathy Market Trends

“Increasing Focus on Targeted Therapies and Precision Medicine Approaches”

- A significant and rapidly evolving trend in the global Immunoglobulin A (IgA) Nephropathy market is the increasing focus on targeted therapies and precision medicine approaches aimed at improving disease management and slowing kidney function decline

- Pharmaceutical and biotechnology companies are increasingly investing in the development of advanced therapeutics that specifically target the underlying immune and inflammatory pathways associated with IgA nephropathy rather than relying solely on generalized immunosuppressive treatments

- For instance, several companies are developing complement inhibitors, endothelin receptor antagonists, and targeted-release corticosteroids designed to reduce proteinuria and preserve kidney function in patients with IgA nephropathy

- The growing adoption of precision medicine and biomarker-based diagnostics is enabling healthcare providers to personalize treatment strategies based on patient-specific disease progression, genetic profiles, and risk factors, thereby improving treatment effectiveness and minimizing adverse effects

- Furthermore, advancements in diagnostic technologies, including biomarker testing, genetic analysis, and improved kidney biopsy techniques, are supporting earlier diagnosis and more accurate disease monitoring among patients suffering from IgA nephropathy

- The increasing number of clinical trials, research collaborations, and regulatory support for rare kidney disease therapies is accelerating innovation and expanding the availability of novel treatment options globally

- This trend toward personalized therapies, targeted biologics, and advanced renal disease management strategies is significantly transforming the treatment landscape for Immunoglobulin A (IgA) nephropathy and improving long-term patient outcomes

Immunoglobulin A (IgA) Nephropathy Market Dynamics

Driver

“Growing Need Due to Rising Prevalence of Chronic Kidney Diseases and Increasing Awareness”

- A significant and rapidly evolving trend in the global Immunoglobulin A (IgA) Nephropathy market is the increasing focus on targeted therapies and precision medicine approaches aimed at improving disease management and slowing kidney function decline

- Pharmaceutical and biotechnology companies are increasingly investing in the development of advanced therapeutics that specifically target the underlying immune and inflammatory pathways associated with IgA nephropathy rather than relying solely on generalized immunosuppressive treatments

- For instance, several companies are developing complement inhibitors, endothelin receptor antagonists, and targeted-release corticosteroids designed to reduce proteinuria and preserve kidney function in patients with IgA nephropathy

- The growing adoption of precision medicine and biomarker-based diagnostics is enabling healthcare providers to personalize treatment strategies based on patient-specific disease progression, genetic profiles, and risk factors, thereby improving treatment effectiveness and minimizing adverse effects

- Furthermore, advancements in diagnostic technologies, including biomarker testing, genetic analysis, and improved kidney biopsy techniques, are supporting earlier diagnosis and more accurate disease monitoring among patients suffering from IgA nephropathy

- The increasing number of clinical trials, research collaborations, and regulatory support for rare kidney disease therapies is accelerating innovation and expanding the availability of novel treatment options globally

- This trend toward personalized therapies, targeted biologics, and advanced renal disease management strategies is significantly transforming the treatment landscape for Immunoglobulin A (IgA) nephropathy and improving long-term patient outcomes

Restraint/Challenge

“High Treatment Costs and Limited Availability of Approved Therapies”

- The high cost associated with advanced targeted therapies, biologics, and long-term renal disease management remains a significant challenge restraining the broader growth of the Immunoglobulin A (IgA) Nephropathy market

- Many patients require prolonged treatment, regular kidney monitoring, and specialized diagnostic procedures, creating substantial financial burdens for both patients and healthcare systems, particularly in developing economies

- For instance, several investigational and newly approved therapies for IgA nephropathy involve high research, development, and manufacturing costs, resulting in premium pricing that may limit patient accessibility

- In addition, the limited availability of approved therapies specifically designed for IgA nephropathy continues to create treatment gaps, as many patients still rely on conventional supportive care or generalized immunosuppressive therapies with varying effectiveness

- Furthermore, delayed diagnosis, limited disease awareness among general healthcare providers, and inadequate access to nephrology specialists can hinder timely treatment initiation and proper disease management

- The lack of comprehensive reimbursement policies and unequal access to advanced renal care infrastructure across certain regions also pose significant challenges to broader market penetration

- Addressing these challenges through increased awareness programs, expanded research funding, improved reimbursement support, and the development of cost-effective therapeutic solutions will be essential for sustaining long-term growth in the global Immunoglobulin A (IgA) Nephropathy market

Immunoglobulin A (IgA) Nephropathy Market Scope

The market is segmented on the basis of treatment, diagnosis, disease type, symptoms, population type, route of administration, end-users, and distribution channel.

- By Treatment

On the basis of treatment, the Immunoglobulin A (IgA) Nephropathy market is segmented into medication, kidney transplantation, and others. The medication segment dominated the largest market revenue share of 73.5% in 2025, driven by the widespread use of corticosteroids, immunosuppressive drugs, ACE inhibitors, and supportive therapies for long-term disease management. Medications remain the primary treatment option for IgA nephropathy patients because they help reduce inflammation, control blood pressure, and slow kidney damage progression. Physicians frequently prescribe pharmacological therapies during the early and moderate stages of the disease to delay the need for dialysis or transplantation. Increasing awareness regarding early diagnosis and routine renal monitoring is significantly contributing to segment growth globally. In addition, rising prevalence of chronic kidney disorders and growing adoption of targeted therapies are further supporting demand for medication-based treatment approaches. Favorable reimbursement policies and broader availability of generic renal drugs are also strengthening segment dominance. Continuous advancements in complement inhibitors and novel biologic therapies are expected to further enhance treatment effectiveness and support long-term market expansion.

The kidney transplantation segment is anticipated to witness the fastest growth rate with a CAGR of 21.6% from 2026 to 2033, fueled by the increasing number of patients progressing to end-stage renal disease due to severe IgA nephropathy. Kidney transplantation is increasingly preferred for patients with irreversible renal failure as it significantly improves long-term survival and quality of life. Growing advancements in transplant procedures, post-transplant immunosuppressive therapies, and organ preservation technologies are contributing to segment expansion globally. In addition, rising healthcare expenditure and improving access to advanced nephrology care are supporting the increasing adoption of transplantation procedures. Government initiatives promoting organ donation awareness and the expansion of transplant centers are also expected to accelerate market growth during the forecast period.

- By Diagnosis

On the basis of diagnosis, the Immunoglobulin A (IgA) Nephropathy market is segmented into iothalamate clearance test, kidney biopsy, blood tests, and urine tests. The kidney biopsy segment held the largest market revenue share of 42.8% in 2025, driven by its high diagnostic accuracy and widespread use as the gold standard procedure for confirming IgA nephropathy. Kidney biopsy allows healthcare professionals to evaluate renal tissue damage, detect IgA deposits, and determine disease severity for effective treatment planning. Increasing prevalence of chronic kidney disorders and growing awareness regarding early disease detection are significantly contributing to segment growth. In addition, advancements in biopsy technologies and minimally invasive renal diagnostic procedures are improving patient outcomes and supporting broader adoption globally. Hospitals and specialty nephrology centers continue to rely heavily on kidney biopsy procedures for accurate disease assessment and monitoring. Favorable reimbursement availability for advanced diagnostic procedures and increasing investments in renal healthcare infrastructure further strengthen segment dominance. The growing number of nephrologists and renal care specialists worldwide also contributes significantly to market expansion.

The blood tests segment is expected to witness the fastest CAGR of 20.9% from 2026 to 2033, driven by the increasing demand for non-invasive and routine diagnostic solutions for kidney disease management. Blood tests help evaluate kidney function, creatinine levels, and immune abnormalities associated with IgA nephropathy, making them an essential component of disease monitoring. Rising adoption of preventive healthcare screening programs and increasing awareness regarding renal health are supporting segment growth globally. Technological advancements in biomarker testing and laboratory diagnostics are further enhancing the accuracy and efficiency of blood-based diagnostic methods. In addition, the growing preference for cost-effective and easily accessible diagnostic procedures is expected to accelerate adoption during the forecast period.

- By Disease Type

On the basis of disease type, the Immunoglobulin A (IgA) Nephropathy market is segmented into primary IgA nephropathy and secondary IgA nephropathy. The primary IgA nephropathy segment accounted for the largest market revenue share of 69.7% in 2025, driven by the high prevalence of idiopathic IgA deposition disorders among patients with chronic kidney disease. Primary IgA nephropathy is the most commonly diagnosed form of the disease and often requires long-term medical management and continuous renal monitoring. Increasing awareness regarding autoimmune kidney disorders and improvements in diagnostic technologies are significantly contributing to segment growth globally. Physicians frequently recommend early therapeutic intervention for primary IgA nephropathy patients to reduce disease progression and minimize complications. In addition, rising investments in complement-targeted therapies and precision medicine approaches are supporting increased treatment adoption. Favorable reimbursement support for renal disease therapies and expanding nephrology care infrastructure further strengthen segment dominance. Growing clinical research activities focused on understanding the pathophysiology of primary IgA nephropathy are also expected to contribute to long-term market growth.

The secondary IgA nephropathy segment is anticipated to witness the fastest CAGR of 20.7% from 2026 to 2033, fueled by the increasing prevalence of chronic liver diseases, autoimmune disorders, and infections associated with secondary renal complications. Healthcare providers are increasingly focusing on identifying underlying systemic conditions contributing to secondary IgA nephropathy for improved disease management. Rising awareness regarding secondary kidney disorders and advancements in differential diagnostic techniques are further supporting segment growth globally. In addition, increasing adoption of personalized treatment strategies and supportive renal therapies is expected to contribute significantly to market expansion during the forecast period.

- By Symptoms

On the basis of symptoms, the Immunoglobulin A (IgA) Nephropathy market is segmented into hematuria, proteinuria, edema, and others. The proteinuria segment dominated the largest market revenue share of 39.6% in 2025, driven by its strong association with disease progression and chronic kidney damage in IgA nephropathy patients. Proteinuria is widely recognized as a major clinical indicator for monitoring renal function deterioration and evaluating treatment effectiveness. Physicians frequently utilize proteinuria levels for disease diagnosis, prognosis assessment, and therapeutic decision-making. Increasing awareness regarding kidney disease symptoms and the growing prevalence of chronic renal disorders are significantly supporting segment growth globally. In addition, advancements in urine protein testing technologies and routine renal screening programs are contributing to higher diagnosis rates. Healthcare providers increasingly emphasize proteinuria reduction as a primary treatment goal for preventing end-stage renal disease progression. Rising adoption of ACE inhibitors, ARBs, and targeted renal therapies further supports demand within this segment.

The hematuria segment is expected to witness the fastest CAGR of 19.8% from 2026 to 2033, driven by increasing awareness regarding early urinary abnormalities associated with IgA nephropathy. Hematuria is often one of the earliest detectable symptoms of the disease and plays a critical role in prompting diagnostic evaluation and treatment initiation. Growing adoption of preventive health screening programs and advancements in urinary diagnostic testing are supporting segment expansion globally. In addition, rising patient awareness regarding kidney health and increasing availability of point-of-care diagnostic technologies are expected to accelerate growth during the forecast period.

- By Population Type

On the basis of population type, the Immunoglobulin A (IgA) Nephropathy market is segmented into pediatrics and adults. The adults segment held the largest market revenue share of 81.2% in 2025, driven by the higher prevalence of IgA nephropathy among the adult population and increasing incidence of chronic kidney disorders linked to hypertension and metabolic diseases. Adults are more frequently diagnosed with progressive forms of IgA nephropathy requiring long-term disease management and continuous renal monitoring. Increasing aging population and rising healthcare awareness regarding kidney disease prevention are significantly supporting segment growth globally. In addition, lifestyle-related risk factors such as obesity, diabetes, and cardiovascular disorders are contributing to the growing disease burden among adults. Healthcare providers increasingly focus on early intervention and targeted treatment strategies for adult patients to reduce renal complications and dialysis dependency. Expanding access to nephrology care services and advanced renal diagnostics further strengthen the dominance of this segment.

The pediatrics segment is anticipated to witness the fastest CAGR of 18.9% from 2026 to 2033, fueled by increasing awareness regarding pediatric kidney disorders and advancements in early diagnostic techniques. Pediatric nephrologists are increasingly focusing on early disease detection and supportive treatment strategies to prevent long-term renal complications in children. Growing investments in pediatric healthcare infrastructure and increasing research activities related to childhood kidney diseases are further contributing to segment growth globally. In addition, supportive government initiatives promoting child healthcare and rare disease awareness are expected to accelerate adoption of pediatric renal treatment services during the forecast period.

- By Route of Administration

On the basis of route of administration, the Immunoglobulin A (IgA) Nephropathy market is segmented into oral, parenteral, and others. The oral segment accounted for the largest market revenue share of 67.4% in 2025, driven by the widespread availability of oral corticosteroids, ACE inhibitors, immunosuppressants, and supportive renal medications. Oral therapies are highly preferred due to convenience, long-term patient compliance, and ease of administration in chronic disease management. Physicians commonly prescribe oral drugs for controlling proteinuria, hypertension, and inflammatory kidney damage associated with IgA nephropathy. Increasing awareness regarding preventive renal healthcare and rising prevalence of chronic kidney disorders are significantly contributing to segment growth globally. In addition, pharmaceutical companies continue to invest in advanced oral drug formulations with improved safety and therapeutic efficacy. Favorable reimbursement policies and easy accessibility of oral medications through retail pharmacies further support segment dominance. The growing preference for home-based treatment solutions is also expected to sustain strong demand during the forecast period.

The parenteral segment is anticipated to witness the fastest CAGR of 21.3% from 2026 to 2033, fueled by the increasing use of biologics, monoclonal antibodies, and advanced immunotherapy treatments for severe renal disease management. Parenteral administration provides rapid therapeutic action and enhanced bioavailability, making it suitable for progressive and treatment-resistant IgA nephropathy cases. Rising investments in specialty biologics and targeted complement inhibitor therapies are significantly contributing to segment growth globally. Hospitals and specialty nephrology clinics increasingly utilize injectable therapies for intensive patient management and immune modulation. In addition, expanding clinical trials for innovative renal biologics and advancements in infusion therapy technologies are expected to support broader adoption during the forecast period.

- By End-Users

On the basis of end-users, the Immunoglobulin A (IgA) Nephropathy market is segmented into hospitals, specialty clinics, homecare, and others. The hospitals segment dominated the largest market revenue share of 48.7% in 2025, driven by the availability of advanced nephrology departments, renal diagnostic technologies, and multidisciplinary healthcare services. Hospitals remain the primary treatment centers for patients with moderate to severe IgA nephropathy due to their ability to provide comprehensive disease management and continuous patient monitoring. Increasing hospital admissions related to chronic kidney disease and autoimmune renal disorders are significantly contributing to segment growth globally. In addition, hospitals are the leading providers of kidney biopsy procedures, biologic therapies, and renal transplantation services requiring specialized infrastructure and expert supervision. Government investments in healthcare infrastructure and expansion of renal care facilities further strengthen segment dominance. Hospitals also participate extensively in clinical trials and rare kidney disease research programs, supporting broader therapeutic adoption. The growing number of specialized nephrology units and dialysis centers worldwide further contributes to market expansion.

The specialty clinics segment is expected to witness the fastest CAGR of 20.6% from 2026 to 2033, driven by increasing demand for personalized nephrology care and specialized outpatient renal treatment services. Specialty clinics provide focused expertise in kidney disease management, enabling faster diagnosis, customized treatment planning, and continuous patient follow-up. Rising patient preference for cost-effective outpatient care settings and shorter waiting times are contributing to increased adoption globally. Technological advancements in renal diagnostics and increasing awareness regarding early disease detection are further supporting segment growth. The expansion of private nephrology clinics and independent renal care centers is also expected to accelerate market growth during the forecast period.

- By Distribution Channel

On the basis of distribution channel, the Immunoglobulin A (IgA) Nephropathy market is segmented into hospital pharmacy, retail pharmacy, online pharmacy, and others. The hospital pharmacy segment held the largest market revenue share of 46.9% in 2025, driven by the increasing use of specialty renal medications, biologics, and immunosuppressive therapies requiring professional supervision. Hospital pharmacies play a critical role in dispensing advanced therapies for patients undergoing intensive renal treatment, kidney transplantation, and biologic administration. The presence of trained pharmacists and integrated patient monitoring systems further supports segment dominance globally. Increasing hospitalization rates related to chronic kidney disorders and autoimmune renal diseases are also significantly contributing to market growth. In addition, collaborations between pharmaceutical manufacturers and hospital networks for specialty drug supply strengthen medication accessibility and treatment continuity. Favorable reimbursement support for high-cost renal therapies and biologics further contributes to the dominance of this segment. Expanding nephrology treatment infrastructure and increasing investments in hospital-based renal care services are also expected to support long-term market growth.

The online pharmacy segment is anticipated to witness the fastest CAGR of 22.7% from 2026 to 2033, fueled by the rapid expansion of digital healthcare platforms and increasing consumer preference for convenient medicine purchasing solutions. Online pharmacies provide benefits such as home delivery, discounted pricing, subscription refill services, and easy accessibility to long-term renal medications. Rising internet penetration and smartphone adoption are significantly contributing to the expansion of e-pharmacy services worldwide. Patients increasingly prefer online platforms for repeat prescription purchases due to convenience and reduced travel requirements. In addition, supportive regulatory frameworks promoting telemedicine and digital healthcare ecosystems are accelerating market growth globally. Improvements in secure digital payment systems and pharmaceutical logistics infrastructure are also supporting broader adoption of online pharmacy services during the forecast period.

Immunoglobulin A (IgA) Nephropathy Market Regional Analysis

- North America dominated the immunoglobulin A (IgA) nephropathy market with the largest revenue share of 43.1% in 2025, characterized by advanced healthcare infrastructure, strong rare disease research capabilities, and a robust presence of leading biopharmaceutical companies. The region is witnessing substantial growth in the adoption of novel nephrology therapies, driven by increasing clinical trials and regulatory approvals for targeted renal treatments aimed at managing IgA nephropathy

- Rising awareness regarding chronic kidney diseases, growing emphasis on early diagnosis, and increasing availability of advanced biologic and immunosuppressive therapies are further contributing to market growth across North America. In addition, favorable reimbursement policies and expanding investments in nephrology research are supporting the development and commercialization of innovative treatment solutions

- The strong presence of specialized nephrology centers, well-established healthcare systems, and increasing collaborations between pharmaceutical companies and research institutions continue to strengthen North America’s leadership position in the Immunoglobulin A (IgA) Nephropathy market

U.S. Immunoglobulin A (IgA) Nephropathy Market Insight

The U.S. immunoglobulin A (IgA) nephropathy market captured the largest revenue share in 2025 within North America, fueled by the increasing prevalence of chronic kidney diseases and the rapid adoption of targeted renal therapies. The country is experiencing significant growth in clinical research activities and regulatory approvals for innovative nephrology drugs, supported by strong investments in rare disease treatment development. Furthermore, rising awareness regarding early diagnosis, expanding access to specialty nephrology care, and increasing use of precision medicine approaches are contributing substantially to market expansion in the U.S.

Europe Immunoglobulin A (IgA) Nephropathy Market Insight

The Europe immunoglobulin A (IgA) nephropathy market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness regarding rare kidney disorders and rising investments in renal healthcare infrastructure. The region benefits from strong government support for orphan drug development, advanced healthcare systems, and growing adoption of innovative treatment approaches for nephrology conditions. Additionally, increasing clinical collaborations and research initiatives focused on kidney disease management are accelerating the adoption of advanced therapies across Europe.

U.K. Immunoglobulin A (IgA) Nephropathy Market Insight

The U.K. immunoglobulin A (IgA) nephropathy market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing healthcare expenditure and growing focus on chronic kidney disease management. The country’s strong clinical research environment and expanding access to advanced nephrology therapies are supporting market growth. Moreover, favorable reimbursement policies, rising patient awareness, and increasing demand for personalized treatment approaches are expected to further stimulate the adoption of innovative therapies across the U.K. market.

Germany Immunoglobulin A (IgA) Nephropathy Market Insight

The Germany immunoglobulin A (IgA) nephropathy market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s advanced healthcare infrastructure and strong focus on medical innovation. Germany’s increasing investments in nephrology research and precision medicine are supporting the development and adoption of targeted therapies for IgA nephropathy. Furthermore, collaborations between pharmaceutical companies, academic institutions, and specialty renal care centers are contributing to improved patient access to advanced treatment options.

Asia-Pacific Immunoglobulin A (IgA) Nephropathy Market Insight

The Asia-Pacific immunoglobulin A (IgA) nephropathy market is expected to be the fastest growing region during the forecast period due to increasing healthcare expenditure, rising awareness regarding kidney disease management, and improving access to specialty nephrology care. Rapid improvements in healthcare infrastructure across countries such as China, Japan, and India are facilitating better diagnosis and treatment accessibility for IgA nephropathy patients. Additionally, growing government initiatives aimed at strengthening renal healthcare services and increasing investments in biotechnology research are driving significant market growth across the region.

Japan Immunoglobulin A (IgA) Nephropathy Market Insight

The Japan immunoglobulin A (IgA) nephropathy market is gaining momentum due to the country’s advanced healthcare system, increasing aging population, and rising burden of chronic kidney disorders. Japan’s strong focus on precision medicine and innovative renal therapies is supporting the adoption of advanced treatment approaches for IgA nephropathy. Moreover, increasing awareness regarding kidney disease prevention and expanding access to specialized nephrology care services are contributing significantly to market growth in the country.

China Immunoglobulin A (IgA) Nephropathy Market Insight

The China immunoglobulin A (IgA) nephropathy market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s rapidly improving healthcare infrastructure, increasing prevalence of kidney diseases, and rising healthcare expenditure. China is witnessing growing investments in biotechnology and nephrology research, which are accelerating the development and adoption of innovative renal therapies. In addition, expanding access to specialty healthcare services, increasing awareness regarding chronic kidney disease management, and supportive government healthcare initiatives are key factors propelling market growth in the country.

Immunoglobulin A (IgA) Nephropathy Market Share

The Immunoglobulin A (IgA) Nephropathy industry is primarily led by well-established companies, including:

• Novartis AG (Switzerland)

• F. Hoffmann-La Roche Ltd. (Switzerland)

• AstraZeneca (U.K.)

• Travere Therapeutics, Inc. (U.S.)

• Calliditas Therapeutics AB (Sweden)

• Otsuka Pharmaceutical Co., Ltd. (Japan)

• Chinook Therapeutics, Inc. (U.S.)

• Vertex Pharmaceuticals Incorporated (U.S.)

• Pfizer Inc. (U.S.)

• Bristol Myers Squibb (U.S.)

• Eli Lilly and Company (U.S.)

• AbbVie Inc. (U.S.)

• Sanofi (France)

• Regeneron Pharmaceuticals, Inc. (U.S.)

• Alexion Pharmaceuticals, Inc. (U.S.)

• Apellis Pharmaceuticals, Inc. (U.S.)

• CSL Limited (Australia)

• Amgen Inc. (U.S.)

• Takeda Pharmaceutical Company Limited (Japan)

• Biogen Inc. (U.S.)

Latest Developments in Global Immunoglobulin A (IgA) Nephropathy Market

- In December 2021, Calliditas Therapeutics announced that the U.S. Food and Drug Administration (FDA) accepted the New Drug Application for Nefecon, a targeted-release budesonide therapy developed for Immunoglobulin A (IgA) Nephropathy. The regulatory submission marked a major milestone for the first disease-specific therapy designed to reduce pathogenic IgA production in patients with primary IgA nephropathy

- In February 2023, Travere Therapeutics announced that the FDA granted accelerated approval to FILSPARI (sparsentan), the first and only non-immunosuppressive therapy approved for reducing proteinuria in adults with IgA nephropathy at risk of rapid disease progression. The approval was supported by positive Phase III PROTECT study results demonstrating substantial proteinuria reduction compared with irbesartan

- In October 2023, Novartis announced that its Phase III APPLAUSE-IgAN study evaluating investigational iptacopan met the primary endpoint in patients with IgA nephropathy. The oral Factor B inhibitor demonstrated clinically meaningful and statistically significant reductions in proteinuria, reinforcing the growing role of complement-targeted therapies in IgA nephropathy treatment

- In August 2024, Novartis announced that the FDA granted accelerated approval to Fabhalta (iptacopan) for reducing proteinuria in adults with primary IgA nephropathy who are at risk of rapid disease progression. The approval made Fabhalta the first complement inhibitor approved for IgA nephropathy, highlighting a major advancement in targeted kidney disease therapeutics

- In September 2024, Travere Therapeutics announced that the FDA granted full approval to FILSPARI (sparsentan) for slowing kidney function decline in adults with primary IgA nephropathy at risk of disease progression. The full approval was based on long-term Phase III PROTECT study data demonstrating durable kidney protection and superior preservation of kidney function compared with irbesartan

- In April 2025, Novartis announced continued expansion of its renal disease portfolio through ongoing development of complement-targeting therapies for IgA nephropathy and related glomerular diseases. The company highlighted growing global demand for precision therapies addressing underlying complement pathway dysregulation in chronic kidney disease

- In August 2025, Travere Therapeutics announced that the FDA approved modifications to the REMS program for FILSPARI, reducing liver monitoring requirements from monthly to quarterly and removing embryo-fetal toxicity monitoring requirements. The regulatory update was intended to improve treatment accessibility and patient convenience in IgA nephropathy management

- In November 2025, Otsuka Pharmaceutical announced that the FDA approved VOYXACT (sibeprenlimab), a monoclonal antibody therapy for reducing proteinuria in adults with primary IgA nephropathy. The approval was supported by Phase III VISIONARY trial results showing significant proteinuria reduction and reinforced the growing shift toward targeted biologic therapies for IgA nephropathy

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.