Global Implantable Auditory Devices Market

Market Size in USD Billion

CAGR :

%

USD

1.70 Billion

USD

2.40 Billion

2025

2033

USD

1.70 Billion

USD

2.40 Billion

2025

2033

| 2026 –2033 | |

| USD 1.70 Billion | |

| USD 2.40 Billion | |

| % | |

|

Implantable Auditory Devices Market Size

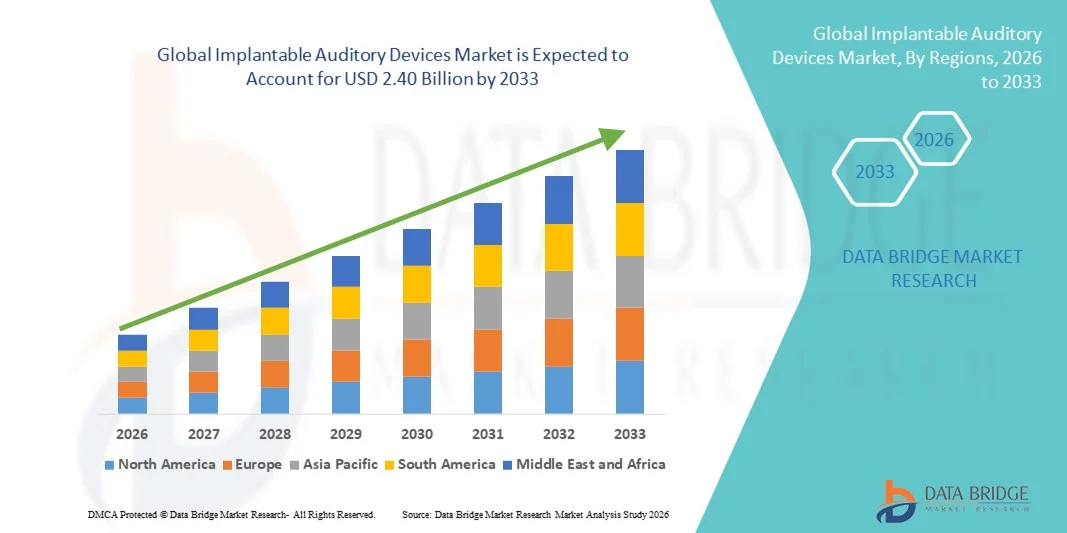

- The global implantable auditory devices market size was valued at USD 1.70 billion in 2025 and is expected to reach USD 2.40 billion by 2033, at a CAGR of 4.42% during the forecast period

- The market growth is largely driven by the rising prevalence of hearing loss disorders, increasing geriatric population, and continuous technological advancements in cochlear implants and bone-anchored hearing systems, leading to improved clinical outcomes and patient adoption worldwide

- Furthermore, growing awareness regarding early diagnosis of hearing impairment, favorable reimbursement policies in developed regions, and expanding healthcare infrastructure in emerging economies are positioning implantable auditory devices as a preferred long-term hearing restoration solution. These converging factors are accelerating the adoption of advanced auditory implants, thereby significantly boosting the industry's growth

Implantable Auditory Devices Market Analysis

- Implantable auditory devices, including cochlear implants, bone-anchored hearing systems, and middle ear implants, are increasingly critical solutions for individuals with severe to profound hearing loss, offering long-term hearing restoration and improved speech perception when conventional hearing aids provide limited benefit

- The escalating demand for implantable auditory devices is primarily fueled by the rising global prevalence of hearing impairment, expanding geriatric population, increasing awareness regarding early diagnosis and intervention, and continuous technological advancements enhancing device performance and patient outcomes

- North America dominated the implantable auditory devices market with the largest revenue share of 39.5% in 2025, characterized by advanced healthcare infrastructure, favorable reimbursement frameworks, strong presence of leading manufacturers, and high adoption of innovative cochlear implant technologies, with the U.S. witnessing significant procedural volumes supported by government and private insurance coverage

- Asia-Pacific is expected to be the fastest growing region in the implantable auditory devices market during the forecast period due to growing healthcare investments, improving access to specialized ENT services, rising awareness about hearing rehabilitation, and expanding patient pool in densely populated countries

- Cochlear implants segment dominated the implantable auditory devices market with a market share of 52.4% in 2025, driven by their proven clinical effectiveness in managing severe hearing loss and continuous technological enhancements such as smaller processors, wireless connectivity, and improved sound processing algorithms

Report Scope and Implantable Auditory Devices Market Segmentation

|

Attributes |

Implantable Auditory Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Implantable Auditory Devices Market Trends

Technological Advancements and Wireless Connectivity Integration

- A significant and accelerating trend in the global implantable auditory devices market is the integration of advanced digital sound processing, wireless connectivity, and smartphone-compatible technologies into cochlear implants and bone-anchored hearing systems. This convergence is significantly enhancing patient experience, customization, and post-implant care management

- For instance, Cochlear Limited’s Nucleus 8 Sound Processor offers direct streaming compatibility with smartphones and smart devices, enabling users to access calls, music, and app-based controls seamlessly. Similarly, MED-EL’s SONNET 2 audio processor integrates wireless connectivity options for improved user convenience and adaptability

- Technological integration in implantable auditory devices enables features such as AI-supported sound processing, improved noise reduction algorithms, and remote programming capabilities for audiologists. For instance, some advanced cochlear implant systems support remote fitting solutions, allowing clinicians to adjust device settings virtually while enhancing speech clarity in diverse listening environments. Furthermore, wireless connectivity offers users greater flexibility in managing device performance through mobile applications

- The seamless integration of implantable auditory devices with digital health platforms and tele-audiology services facilitates continuous monitoring and personalized rehabilitation programs. Through connected interfaces, healthcare providers can track patient progress, optimize device settings, and deliver follow-up care remotely, creating a more coordinated and efficient treatment ecosystem

- This trend toward smarter, more compact, and digitally connected auditory implant systems is fundamentally reshaping patient expectations for hearing restoration. Consequently, companies such as Advanced Bionics are developing next-generation cochlear implant solutions featuring enhanced sound processors, waterproof designs, and expanded connectivity options

- The demand for technologically advanced implantable auditory devices with enhanced connectivity and personalization features is growing rapidly across both developed and emerging healthcare markets, as patients and clinicians increasingly prioritize long-term performance and quality-of-life improvements

Implantable Auditory Devices Market Dynamics

Driver

Rising Prevalence of Hearing Loss and Expanding Access to Early Intervention

- The increasing global prevalence of hearing impairment across pediatric and geriatric populations, coupled with expanding early screening initiatives, is a significant driver for the heightened demand for implantable auditory devices

- For instance, in recent years, several national healthcare systems have strengthened universal newborn hearing screening programs and cochlear implant reimbursement coverage, supporting greater procedural adoption rates. Such strategies by healthcare authorities and device manufacturers are expected to drive the implantable auditory devices market growth in the forecast period

- As awareness regarding untreated hearing loss and its impact on cognitive development and social integration increases, implantable auditory devices offer clinically proven solutions for restoring functional hearing in patients who receive limited benefit from conventional hearing aids

- Furthermore, the growing investment in specialized ENT centers and audiology infrastructure is making implantable hearing solutions more accessible, particularly in emerging economies where large patient populations remain underserved

- The clinical benefits of early implantation, improved speech recognition outcomes, and long-term auditory rehabilitation success are key factors propelling the adoption of cochlear implants and bone-anchored systems in both pediatric and adult patient segments. The trend toward minimally invasive surgical techniques and improved device durability further contributes to market growth

- Government and non-government hearing health initiatives aimed at reducing the burden of disabling hearing loss are further supporting patient identification and referral rates for implant procedures

- The expanding geriatric population, which is more susceptible to age-related sensorineural hearing loss, is creating sustained long-term demand for advanced implantable hearing restoration solutions

Restraint/Challenge

High Procedural Costs and Surgical Complexity Concerns

- Concerns surrounding the high upfront cost of implantable auditory devices, including surgical expenses, device components, and post-operative rehabilitation, pose a significant challenge to broader market penetration, particularly in low- and middle-income countries

- For instance, limited reimbursement coverage in certain regions and lengthy approval processes for implantable medical devices have made some eligible patients hesitant to undergo implantation procedures

- Addressing cost-related and procedural concerns through expanded insurance coverage, government-funded hearing programs, and awareness campaigns is crucial for improving accessibility. Companies such as Cochlear Limited and MED-EL emphasize long-term clinical value and patient support programs to encourage adoption. In addition, the surgical nature of implantation, along with associated risks such as infection or device failure, can deter some patients and caregivers from choosing implantable solutions

- While technological advancements continue to enhance safety and reliability, the perception of surgery-related risks and the requirement for lifelong follow-up care can still limit acceptance, especially among elderly patients or those with comorbid conditions

- Overcoming these challenges through improved reimbursement frameworks, simplified surgical techniques, expanded training for specialists, and cost-optimized device innovations will be vital for sustained market growth

- Limited availability of skilled cochlear implant surgeons and audiologists in certain developing regions can delay diagnosis, implantation, and post-operative rehabilitation services

- Stringent regulatory approval processes and clinical trial requirements for implantable medical devices can extend product launch timelines and increase overall development costs for manufacturers

Implantable Auditory Devices Market Scope

The market is segmented on the basis of product, type, patient type, and end use.

- By Product

On the basis of product, the global implantable auditory devices market is segmented into active hearing implants and passive hearing implants. The active hearing implants segment dominated the market with the largest revenue share in 2025, driven by their advanced electronic components that actively amplify and process sound signals. These devices, including cochlear and bone conduction implants, provide superior sound quality and improved speech recognition compared to passive systems. Their ability to support wireless connectivity, remote programming, and AI-based sound optimization further strengthens adoption. In addition, increasing reimbursement support and continuous technological advancements contribute significantly to the segment’s leadership position.

The passive hearing implants segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by growing demand for cost-effective and surgically simpler implant solutions. Passive systems are increasingly preferred in cases requiring structural support or ossicular chain reconstruction without complex electronic processing. Advancements in biocompatible materials and minimally invasive surgical techniques are enhancing patient outcomes. Rising awareness in emerging markets and expanding ENT surgical capabilities are further supporting growth in this segment.

- By Type

On the basis of type, the market is segmented into cochlear implants, middle ear implants, bone conduction implants, and auditory brainstem implants. The cochlear implants segment dominated the market with the largest revenue share of 52.4% in 2025, owing to their proven effectiveness in treating severe to profound sensorineural hearing loss. These devices directly stimulate the auditory nerve, enabling significant improvements in speech perception and communication ability. Strong clinical evidence, continuous processor upgrades, and expanding pediatric implantation programs contribute to high adoption rates. Furthermore, favorable reimbursement frameworks in developed economies reinforce the dominance of this segment.

The bone conduction implants segment is projected to witness the fastest CAGR from 2026 to 2033, driven by increasing diagnosis of conductive and mixed hearing loss cases. These implants bypass the outer and middle ear to directly stimulate the cochlea via bone vibration, offering an effective alternative for patients unsuitable for traditional hearing aids. Technological enhancements in implant design and sound processors are improving comfort and performance. Growing awareness among ENT specialists and expanding outpatient implantation procedures are accelerating segment growth.

- By Patient Type

On the basis of patient type, the market is segmented into adult and pediatric. The adult segment dominated the market with the largest revenue share in 2025, primarily due to the high prevalence of age-related hearing loss globally. The expanding geriatric population and increasing awareness about the cognitive and social impact of untreated hearing impairment are driving adult implantation rates. Adults are more likely to seek advanced hearing restoration solutions supported by insurance coverage in developed regions. In addition, improved surgical outcomes and reduced complication rates contribute to sustained demand within this group.

The pediatric segment is expected to witness the fastest growth rate from 2026 to 2033, supported by universal newborn hearing screening initiatives and early intervention programs. Early cochlear implantation significantly enhances speech and language development outcomes in children with profound hearing loss. Government-supported pediatric implant programs and charitable funding initiatives are expanding accessibility in emerging economies. Increasing parental awareness and improved long-term clinical data further accelerate growth in this segment.

- By End Use

On the basis of end use, the market is segmented into hospitals, ENT clinics, and ambulatory surgical centers. The hospitals segment dominated the market with the largest revenue share in 2025, as implantable auditory procedures require specialized surgical infrastructure and multidisciplinary teams. Hospitals provide comprehensive pre-operative evaluation, surgical implantation, and post-operative rehabilitation services. Advanced imaging facilities and intensive care capabilities further support complex implantation procedures. The presence of experienced otologic surgeons in hospital settings reinforces segment leadership.

The ambulatory surgical centers segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by the shift toward cost-effective and minimally invasive outpatient procedures. Improvements in surgical techniques and anesthesia protocols enable select implant procedures to be performed safely in outpatient settings. These centers offer reduced hospital stay durations and lower procedural costs, attracting both patients and payers. Expanding healthcare infrastructure and increasing patient preference for shorter recovery times are further contributing to rapid segment growth.

Implantable Auditory Devices Market Regional Analysis

- North America dominated the implantable auditory devices market with the largest revenue share of 39.5% in 2025, characterized by advanced healthcare infrastructure, favorable reimbursement frameworks, strong presence of leading manufacturers, and high adoption of innovative cochlear implant technologies

- Patients in the region highly value the clinical effectiveness, long-term hearing restoration benefits, and advanced technological features offered by implantable auditory devices, including wireless connectivity and remote programming capabilities

- This widespread adoption is further supported by the presence of leading manufacturers, skilled otologic surgeons, favorable insurance frameworks, and increasing awareness regarding early hearing intervention, establishing implantable auditory devices as a preferred treatment solution for both adult and pediatric patients

U.S. Implantable Auditory Devices Market Insight

The U.S. implantable auditory devices market captured the largest revenue share in 2025 within North America, fueled by the high prevalence of sensorineural hearing loss and strong reimbursement coverage for cochlear implant procedures. Patients and healthcare providers are increasingly prioritizing early intervention and advanced hearing restoration technologies to improve speech recognition and quality of life. The growing presence of leading manufacturers and specialized cochlear implant centers further propels the industry. Moreover, expanding newborn hearing screening programs and favorable private and public insurance policies are significantly contributing to the market's expansion.

Europe Implantable Auditory Devices Market Insight

The Europe implantable auditory devices market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by well-established healthcare systems and supportive reimbursement frameworks. The increase in the geriatric population, coupled with growing awareness regarding untreated hearing loss, is fostering device adoption. European patients are also drawn to the clinical reliability and long-term benefits these implants offer. The region is experiencing significant growth across both adult and pediatric segments, with implant procedures increasingly incorporated into national hearing health programs and public hospital services.

U.K. Implantable Auditory Devices Market Insight

The U.K. implantable auditory devices market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of early hearing diagnosis and access to National Health Service-supported implantation programs. In addition, concerns regarding communication disabilities and cognitive decline linked to untreated hearing loss are encouraging timely clinical intervention. The U.K.’s strong network of ENT specialists and audiology clinics, alongside structured referral pathways, is expected to continue stimulating market growth.

Germany Implantable Auditory Devices Market Insight

The Germany implantable auditory devices market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing focus on advanced medical technologies and high healthcare expenditure. Germany’s well-developed hospital infrastructure, combined with its emphasis on research and clinical innovation, promotes the adoption of cochlear and bone conduction implants. The integration of digital sound processors and remote fitting solutions is also becoming increasingly prevalent, with a strong preference for precision-engineered and quality-certified medical devices aligning with local patient expectations.

Asia-Pacific Implantable Auditory Devices Market Insight

The Asia-Pacific implantable auditory devices market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by expanding healthcare infrastructure, rising disposable incomes, and growing awareness of hearing rehabilitation in countries such as China, Japan, and India. The region's increasing focus on early diagnosis programs, supported by government healthcare initiatives, is driving implant adoption. Furthermore, as APAC emerges as a key manufacturing and distribution hub for medical devices, the accessibility and affordability of implantable auditory systems are expanding to a broader patient population.

Japan Implantable Auditory Devices Market Insight

The Japan implantable auditory devices market is gaining momentum due to the country’s aging population, advanced medical technology landscape, and strong emphasis on quality healthcare. The Japanese market places significant importance on early diagnosis and precision treatment, and the adoption of cochlear implants is driven by increasing cases of age-related hearing loss. The integration of compact sound processors and wireless connectivity features is fueling growth. Moreover, Japan's structured healthcare reimbursement system is likely to spur demand for reliable and long-term hearing restoration solutions in both adult and pediatric populations.

India Implantable Auditory Devices Market Insight

The India implantable auditory devices market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s large patient pool with untreated hearing impairment, expanding middle class, and improving access to tertiary healthcare facilities. India stands as one of the fastest-growing markets for cochlear implantation, with increasing awareness across urban and semi-urban regions. The push toward early childhood hearing screening and government-supported assistance programs, alongside the presence of global and domestic device suppliers, are key factors propelling the market in India.

Implantable Auditory Devices Market Share

The Implantable Auditory Devices industry is primarily led by well-established companies, including:

- Cochlear Limited (Australia)

- MED-EL Medical Electronics (Austria)

- Advanced Bionics AG (Switzerland)

- Nurotron Biotechnology Co., Ltd. (China)

- Envoy Medical Corporation (U.S.)

- Sonova AG (Switzerland)

- Earlens Corporation (U.S.)

- Oticon Medical AB (Sweden)

- Demant A/S (Denmark)

- GN Hearing A/S (Denmark)

- William Demant Holding A/S (Denmark)

- Sivantos Pte. Ltd. (Singapore)

- Starkey Laboratories, Inc. (U.S.)

- Interacoustics A/S (Denmark)

- HANSATON Akustik GmbH (Germany)

- Audina Hearing Instruments, Inc. (U.S.)

- Platon Medical Ltd. (U.K.)

- AudioBone, Inc. (U.S.)

- MEDICA S.p.A. (Italy)

- Rion Co., Ltd. (Japan)

What are the Recent Developments in Global Implantable Auditory Devices Market?

- In December 2025, MED-EL USA received FDA approval for expanded usage of its cochlear implant system to include children as young as seven months old with bilateral sensorineural hearing loss, making it the only FDA-approved cochlear implant option for infants this young

- In July 2025, Cochlear Limited announced the FDA approval and launch of the Cochlear™ Nucleus® Nexa™ System, the world’s first smart cochlear implant system that supports upgradeable firmware and enhanced internal memory to store personalized hearing settings, enabling recipients to benefit from future innovations and improved user experience

- In November 2024, MED-EL Corporation announced the FDA approval of expanded candidacy indications for its cochlear implant system including the industry’s first formal approval related to hearing preservation outcomes broadening eligibility for more adults with sensorineural hearing loss and supporting residual hearing preservation post-implantation

- In July 2024, Oticon Medical announced FDA clearance and CE marking for its Sentio™ active transcutaneous bone conduction hearing system, offering an implant placed completely beneath the skin and the smallest transcutaneous processor to date, expanding bone-anchored hearing solutions for patients

- In March 2024, MED-EL unveiled a suite of breakthrough cochlear implant care innovations including remote care capabilities (HearCare MED-EL App), wireless streaming accessories (AudioStream Adapter for RONDO 3), and upgraded OTOPLAN surgical planning software designed to personalize and enhance cochlear implant fitting and post-operative outcomes

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.