Global In Flight Entertainment And Connectivity Market

Market Size in USD Billion

CAGR :

%

USD

7.42 Billion

USD

13.31 Billion

2025

2033

USD

7.42 Billion

USD

13.31 Billion

2025

2033

| 2026 –2033 | |

| USD 7.42 Billion | |

| USD 13.31 Billion | |

| % | |

|

In-flight Entertainment and Connectivity Market Size

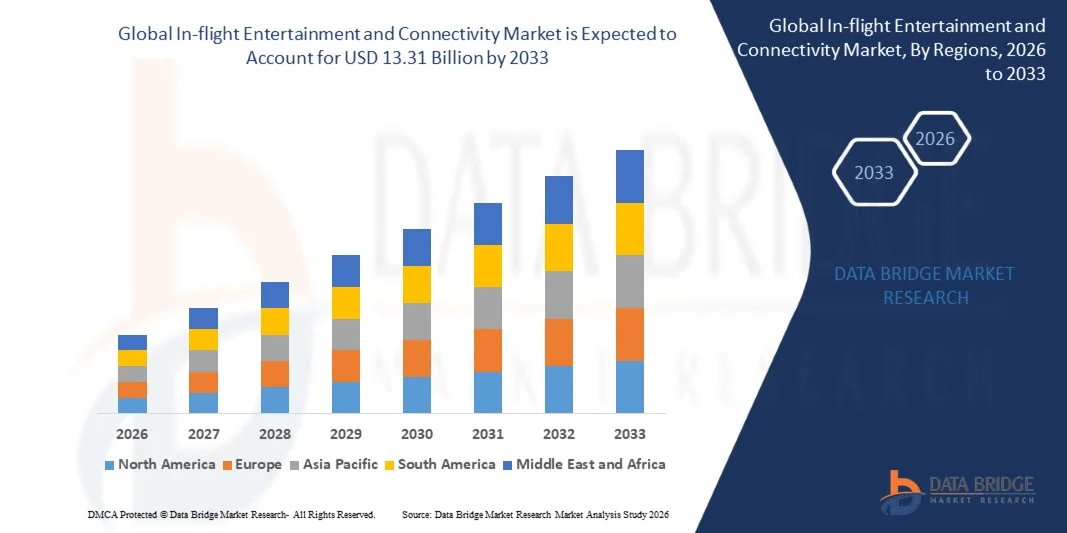

- The global in-flight entertainment and connectivity market size was valued at USD 7.42 billion in 2025 and is expected to reach USD 13.31 billion by 2033, at a CAGR of 7.58% during the forecast period

- The market growth is largely fuelled by the rising demand for seamless onboard connectivity, enhanced passenger experience, and increasing long-haul air travel

- Growing airline investments in advanced satellite communication technologies and high-speed broadband solutions are accelerating market expansion

In-flight Entertainment and Connectivity Market Analysis

- The market is witnessing strong momentum driven by continuous technological advancements in satellite communication, wireless connectivity, and content delivery systems aimed at improving passenger engagement and operational efficiency

- In addition, airlines are increasingly focusing on differentiating their services through enhanced digital experiences, monetization of onboard connectivity, and partnerships with content providers to strengthen competitive positioning

- North America dominated the in-flight entertainment and connectivity market with the largest revenue share in 2025, driven by strong presence of major airlines, rapid adoption of advanced satellite communication technologies, and high passenger demand for onboard Wi-Fi services

- Asia-Pacific region is expected to witness the highest growth rate in the global in-flight entertainment and connectivity market, driven by expanding airline networks, rising air passenger traffic, increasing investments in new aircraft deliveries, and growing adoption of advanced connectivity and wireless streaming technologies across emerging economies

- The IFE Hardware segment held the largest market revenue share in 2025 driven by continuous aircraft retrofitting programs and new aircraft deliveries requiring seatback screens, control panels, servers, and satellite communication equipment. Airlines are investing significantly in high-definition displays, lightweight cabin equipment, and advanced onboard servers to enhance passenger experience and reduce fuel consumption through optimized system design. Hardware upgrades also support integration with next-generation satellite antennas and wireless access points to enable seamless content distribution. Increasing fleet modernization initiatives across global carriers further strengthen demand for durable and scalable hardware platforms

Report Scope and In-flight Entertainment and Connectivity Market Segmentation

|

Attributes |

In-flight Entertainment and Connectivity Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Panasonic Corporation (Japan) |

|

Market Opportunities |

• Expansion Of High-Speed Satellite-Based Connectivity Services |

|

Value Added Data Infosets |

In addition to the market insights such as market value, growth rate, market segments, geographical coverage, market players, and market scenario, the market report curated by the Data Bridge Market Research team includes in-depth expert analysis, import/export analysis, pricing analysis, production consumption analysis, and pestle analysis. |

In-flight Entertainment and Connectivity Market Trends

“Integration Of Advanced Digital Connectivity And Personalized Passenger Experience”

• The increasing focus on enhancing passenger engagement and satisfaction is significantly shaping the in-flight entertainment and connectivity market, as airlines aim to deliver seamless digital experiences through high-speed internet and interactive platforms. Modern systems are gaining traction due to their ability to provide real-time streaming, live television, gaming, and e-commerce services, strengthening competitive differentiation and brand loyalty among carriers

• Growing passenger expectations for uninterrupted connectivity during long-haul and short-haul flights are accelerating investments in satellite-based broadband and wireless cabin technologies. Airlines are upgrading legacy seatback systems and introducing bring-your-own-device platforms to cater to evolving digital consumption patterns. This shift is also encouraging collaborations between connectivity providers and content streaming companies to expand onboard entertainment libraries

• Digital transformation strategies are influencing procurement and partnership decisions, with airlines emphasizing scalable connectivity infrastructure, cybersecurity integration, and data-driven personalization. These factors are helping operators monetize onboard services through subscription models, targeted advertising, and premium content access, while improving operational efficiency and customer insights

• For instance, in 2024, Delta Air Lines and Emirates expanded free Wi-Fi and enhanced streaming capabilities across selected fleets to strengthen passenger engagement. These upgrades were introduced to address rising demand for high-speed connectivity and were promoted through loyalty programs and digital campaigns to increase repeat travel and customer satisfaction

• While demand for enhanced onboard connectivity continues to grow, sustained market expansion depends on continuous technological upgrades, cost-effective satellite bandwidth management, and maintaining consistent service quality across global routes

In-flight Entertainment and Connectivity Market Dynamics

Driver

“Growing Investment In High-Speed Satellite Connectivity And Passenger-Centric Services”

• Rising airline investment in advanced satellite communication technologies is a major driver for the in-flight entertainment and connectivity market. Carriers are increasingly adopting next-generation broadband solutions to improve passenger experience, enable real-time communication, and support digital service expansion across fleets

• Expanding demand for seamless streaming, social media access, and cloud-based applications during flights is influencing market growth. Enhanced connectivity helps airlines differentiate service offerings, strengthen brand positioning, and generate ancillary revenue through premium internet packages and onboard digital services

• Aviation stakeholders are actively promoting connected aircraft ecosystems through fleet modernization, retrofit programs, and strategic alliances with satellite operators and technology providers. These efforts are supported by rising global air passenger traffic and the growing reliance on personal electronic devices for entertainment and productivity

• For instance, in 2023, United Airlines and Qatar Airways reported expanded deployment of high-speed connectivity solutions across international routes to meet passenger expectations for uninterrupted broadband access. Both companies emphasized service enhancement and digital innovation initiatives to improve customer loyalty and competitive advantage

• Although increasing connectivity demand supports market growth, broader adoption depends on bandwidth optimization, infrastructure investment, and efficient integration with aircraft systems to ensure consistent global coverage

Restraint/Challenge

“High Installation Costs And Connectivity Infrastructure Limitations”

• The substantial cost associated with installation, retrofitting, and maintenance of in-flight connectivity systems remains a key challenge, particularly for small and mid-sized carriers. Satellite bandwidth expenses and aircraft downtime during upgrades contribute to elevated operational costs and impact return on investment

• Regulatory compliance and technical integration complexities also affect market expansion. Connectivity systems must adhere to aviation safety standards and international communication regulations, increasing certification timelines and deployment costs

• Network coverage gaps and signal interruptions in remote or oceanic regions can reduce service reliability, impacting passenger satisfaction and limiting adoption on certain routes. Airlines must invest in multi-orbit satellite partnerships and advanced antenna technologies to mitigate these challenges

• For instance, in 2024, Lufthansa and Air India highlighted higher retrofit expenses and bandwidth pricing pressures while expanding onboard Wi-Fi services across long-haul fleets. Infrastructure constraints and certification requirements were identified as operational barriers affecting rollout timelines

• Addressing these challenges will require cost optimization strategies, stronger collaboration with satellite providers, and continuous innovation in lightweight antenna systems and network integration solutions to ensure sustainable growth of the global in-flight entertainment and connectivity market

In-flight Entertainment and Connectivity Market Scope

The market is segmented on the basis of product type, component, aircraft type, class, offering type, and end user.

• By Product Type

On the basis of product type, the in-flight entertainment and connectivity market is segmented into IFE Hardware, IFE Connectivity, and IFE Content. The IFE Hardware segment held the largest market revenue share in 2025 driven by continuous aircraft retrofitting programs and new aircraft deliveries requiring seatback screens, control panels, servers, and satellite communication equipment. Airlines are investing significantly in high-definition displays, lightweight cabin equipment, and advanced onboard servers to enhance passenger experience and reduce fuel consumption through optimized system design. Hardware upgrades also support integration with next-generation satellite antennas and wireless access points to enable seamless content distribution. Increasing fleet modernization initiatives across global carriers further strengthen demand for durable and scalable hardware platforms.

The IFE Connectivity segment is expected to witness the fastest growth rate from 2026 to 2033, driven by rising passenger demand for high-speed internet access and real-time streaming services during flights. Increasing adoption of satellite-based broadband systems and air-to-ground communication technologies is accelerating deployment across both long-haul and short-haul fleets. Airlines are leveraging connectivity solutions to introduce subscription-based Wi-Fi packages, onboard e-commerce, and digital advertising platforms. Continuous improvements in bandwidth capacity and latency reduction are further enhancing service reliability and passenger satisfaction.

• By Component

On the basis of component, the market is segmented into Hardware, Connectivity, and Content. The Hardware segment accounted for the largest revenue share in 2025 owing to the high installation cost of onboard equipment, including antennas, routers, seatback screens, and media servers. Airlines prioritize modern and energy-efficient systems to ensure operational reliability and long service life. Frequent technological upgrades and compliance with aviation safety standards also contribute to sustained hardware demand. In addition, integration of touchscreen displays and modular components enables easier maintenance and system scalability.

The Connectivity segment is projected to expand at the fastest rate from 2026 to 2033 due to increasing airline partnerships with satellite operators and communication technology providers. Growing monetization opportunities through premium internet services, data analytics, and personalized digital offerings are supporting rapid expansion. Enhanced satellite constellations and multi-orbit capabilities are improving global coverage, including remote and oceanic routes. These developments are enabling airlines to deliver consistent and high-speed broadband experiences to passengers worldwide.

• By Aircraft Type

On the basis of aircraft type, the market is segmented into Narrow-Body Aircraft (NBA), Wide-Body Aircraft (WBA), and Very Large Aircraft (VLA). The Wide-Body Aircraft segment held the largest market share in 2025 driven by higher passenger volumes on long-haul international routes and stronger demand for premium entertainment and broadband connectivity services. Wide-body aircraft typically operate extended flight durations, increasing passenger reliance on onboard streaming, gaming, and communication services. Airlines often equip these aircraft with advanced seatback systems and higher bandwidth capacity to enhance service differentiation.

The Narrow-Body Aircraft segment is expected to grow at a significant pace from 2026 to 2033 supported by fleet expansion in regional and domestic travel. Increasing integration of wireless streaming platforms and bring-your-own-device solutions in short-haul operations is driving adoption. Airlines are focusing on cost-effective connectivity systems that can be deployed efficiently across large narrow-body fleets. Rising low-cost carrier penetration further contributes to demand for scalable and lightweight entertainment solutions.

• By Class

On the basis of class, the market is segmented into First Class, Business Class, and Premium Economy and Economy. The Premium Economy and Economy segment accounted for the largest revenue share in 2025 due to the high passenger base and growing expectation for accessible onboard entertainment and connectivity services. Airlines are expanding wireless streaming capabilities and introducing free messaging services to enhance satisfaction among economy travelers. The integration of personal device-based entertainment platforms is reducing hardware dependency while maintaining service quality.

The Business Class segment is projected to expand at the fastest rate from 2026 to 2033 as airlines enhance premium cabin experiences with larger screens, high-speed internet, and exclusive digital content libraries. Business travelers increasingly require uninterrupted connectivity for productivity and communication purposes. Airlines are responding by offering complimentary broadband packages and priority network access in premium cabins. These enhancements strengthen brand loyalty and justify premium pricing strategies.

• By Offering Type

On the basis of offering type, the market is segmented into In-flight Entertainment (IFE) and In-flight Connectivity (IFC). The In-flight Entertainment segment dominated the market in 2025 supported by established seatback installations, extensive multimedia libraries, and interactive applications. Continuous content licensing agreements with studios and streaming providers ensure diverse programming options across languages and genres. Technological upgrades such as 4K displays and immersive audio systems are further enhancing passenger engagement.

The In-flight Connectivity segment is projected to expand at the fastest rate from 2026 to 2033 driven by increasing passenger reliance on personal electronic devices and demand for uninterrupted broadband access throughout flight duration. Airlines are integrating connectivity platforms with loyalty programs, onboard shopping portals, and real-time flight updates. Improved satellite infrastructure and competitive pricing models are supporting wider adoption across full-service and low-cost carriers.

• By End User

On the basis of end user, the market is segmented into OEM and Aftermarket. The OEM segment held the largest market share in 2025 owing to integration of advanced IFE and connectivity systems in newly manufactured aircraft. Aircraft manufacturers collaborate closely with technology providers to install factory-fitted solutions that meet evolving airline requirements. Early-stage integration ensures optimized system performance, weight efficiency, and regulatory compliance. Growing global aircraft orders further contribute to segment expansion.

The Aftermarket segment is projected to expand at the fastest rate from 2026 to 2033 as airlines continue retrofitting existing fleets with upgraded connectivity infrastructure and modernized entertainment systems. Retrofit programs allow carriers to remain competitive without purchasing new aircraft. Increasing focus on passenger experience improvement and ancillary revenue generation is encouraging frequent system upgrades. Cost-efficient installation techniques and modular solutions are supporting broader aftermarket adoption across global fleets.

In-flight Entertainment and Connectivity Market Regional Analysis

• North America dominated the in-flight entertainment and connectivity market with the largest revenue share in 2025, driven by strong presence of major airlines, rapid adoption of advanced satellite communication technologies, and high passenger demand for onboard Wi-Fi services

• Airlines in the region highly prioritize seamless broadband connectivity, live streaming capabilities, and integration of digital services with passenger loyalty programs and mobile applications

• This widespread adoption is further supported by high air passenger traffic, early technology adoption, and significant investments in fleet modernization, establishing advanced IFE and IFC systems as essential components of competitive airline service offerings

U.S. In-flight Entertainment and Connectivity Market Insight

The U.S. in-flight entertainment and connectivity market captured the largest revenue share in 2025 within North America, fueled by large commercial aircraft fleets and strong consumer expectation for uninterrupted in-flight internet access. Airlines are increasingly investing in next-generation satellite systems and high-capacity broadband networks to enhance passenger satisfaction. The growing preference for streaming on personal electronic devices, combined with integration of onboard connectivity with digital payment platforms and loyalty programs, further propels market growth. Moreover, partnerships between airlines and satellite service providers are accelerating nationwide connectivity coverage and service reliability.

Europe In-flight Entertainment and Connectivity Market Insight

The Europe in-flight entertainment and connectivity market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by increasing air travel demand and airline focus on enhancing passenger experience. Expansion of cross-border travel and rising competition among regional carriers are encouraging investments in advanced IFE systems and high-speed connectivity infrastructure. European airlines are actively upgrading legacy fleets with wireless streaming platforms and satellite-based broadband services. Growing emphasis on digital transformation and operational efficiency is further contributing to market expansion across the region.

U.K. In-flight Entertainment and Connectivity Market Insight

The U.K. in-flight entertainment and connectivity market is expected to witness the fastest growth rate from 2026 to 2033, driven by strong international travel networks and demand for premium onboard experiences. Airlines operating from the U.K. are increasingly introducing high-speed Wi-Fi services and personalized digital content libraries to differentiate their offerings. Passenger preference for productivity during flights, including business communication and streaming services, is accelerating connectivity investments. In addition, fleet modernization programs and retrofit initiatives are supporting sustained market development.

Germany In-flight Entertainment and Connectivity Market Insight

The Germany in-flight entertainment and connectivity market is expected to witness the fastest growth rate from 2026 to 2033, fueled by technological innovation and the presence of leading aviation stakeholders. German carriers are emphasizing secure and high-performance connectivity solutions to meet evolving passenger expectations. Growing demand for seamless digital experiences and advanced cabin systems is encouraging integration of lightweight hardware and satellite antennas. The country’s focus on engineering excellence and aviation efficiency further supports adoption across both long-haul and regional fleets.

Asia-Pacific In-flight Entertainment and Connectivity Market Insight

The Asia-Pacific in-flight entertainment and connectivity market is expected to witness the fastest growth rate from 2026 to 2033, driven by rapid expansion of commercial aviation, increasing middle-class air travelers, and rising investments in new aircraft deliveries. Airlines across the region are enhancing onboard digital services to attract tech-savvy passengers seeking high-speed internet and interactive entertainment. Government initiatives supporting aviation infrastructure development and fleet expansion are further accelerating deployment of advanced connectivity systems. The region’s growing prominence as an aviation manufacturing and maintenance hub also strengthens market growth.

Japan In-flight Entertainment and Connectivity Market Insight

The Japan in-flight entertainment and connectivity market is expected to witness the fastest growth rate from 2026 to 2033 due to the country’s advanced technological ecosystem and strong demand for premium travel experiences. Japanese airlines are investing in reliable satellite broadband and high-definition entertainment systems to maintain competitive service standards. Passenger preference for seamless connectivity, digital streaming, and integrated cabin services is driving system upgrades. In addition, focus on operational efficiency and passenger comfort is supporting long-term market expansion.

China In-flight Entertainment and Connectivity Market Insight

The China in-flight entertainment and connectivity market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid aviation sector growth, expanding domestic and international routes, and high adoption of digital technologies. Chinese airlines are increasingly equipping fleets with modern seatback systems and satellite-based connectivity solutions to meet rising passenger expectations. Strong government support for aviation infrastructure and the development of smart airports further propel market growth. The presence of domestic technology providers and large-scale aircraft procurement programs continues to strengthen China’s position in the regional market.

In-flight Entertainment and Connectivity Market Share

The In-flight Entertainment and Connectivity industry is primarily led by well-established companies, including:

• Panasonic Corporation (Japan)

• Gogo LLC (U.S.)

• Viasat, Inc. (U.S.)

• Thales Group (France)

• Rockwell Automation (U.S.)

• Honeywell International Inc. (U.S.)

• Zodiac Aerospace (France)

• Anuvu (U.S.)

• Inmarsat Global Limited (U.K.)

• Stellar Entertainment Group (U.S.)

• Lufthansa Systems (Germany)

• Safran S.A. (France)

• Burrana (Australia)

• EchoStar Corporation (U.S.)

• Kymeta Corporation (U.S.)

• ThiKom Solutions, Inc. (U.S.)

• Iridium Communications Inc. (U.S.)

• Astronics Corporation (U.S.)

• Kontron (Austria)

• BAE Systems (U.K.)

Latest Developments in Global In-flight Entertainment and Connectivity Market

- In August, 2024, Air Canada entered into a content partnership agreement with Anuvu to significantly expand its in-flight entertainment library, increasing onboard availability to over 1,000 movies and 3,500 TV episodes. This development is aimed at enhancing passenger engagement through broader and more frequently updated entertainment options. The initiative strengthens Air Canada’s competitive positioning and contributes to rising demand for premium content integration solutions in the global IFEC market

- In September, 2024, Delta Air Lines announced a fleet-wide IFE system upgrade focused on integrating high-definition seatback displays and expanding its digital content portfolio. The modernization program is designed to improve passenger satisfaction, boost brand loyalty, and support advanced interactive features. This upgrade reflects growing airline investment in next-generation cabin technologies, positively influencing hardware and content demand across the market

- In July, 2024, Panasonic Avionics Corporation inaugurated a new software design and development facility in Pune, India dedicated to advancing in-flight entertainment and connectivity (IFEC) solutions. The expansion enhances the company’s innovation capabilities and accelerates development of scalable digital platforms for airlines. This strategic move strengthens global R&D capacity and supports long-term technological advancement within the IFEC industry

- In April, 2024, JetBlue Airways introduced upgrades to its in-flight entertainment systems, including new partnerships with streaming platforms to diversify onboard content offerings. The initiative is intended to deliver a richer and more personalized entertainment experience for passengers. Such collaborations highlight increasing integration between airlines and digital content providers, driving content-centric growth in the market

- In August, 2022, Bluebox Aviation Systems partnered with Jetstar Group to deploy its Blueview digital passenger experience platform across Jetstar’s Airbus fleet. The agreement covers integration of Jetstar Entertainment systems with potential expansion to additional aircraft models. This deployment enhances wireless streaming capabilities and supports broader adoption of portable and device-based IFE solutions across regional airline fleets

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.