Global Integrated Marine Automation System Market

Market Size in USD Billion

CAGR :

%

USD

4.23 Billion

USD

5.14 Billion

2025

2033

USD

4.23 Billion

USD

5.14 Billion

2025

2033

| 2026 –2033 | |

| USD 4.23 Billion | |

| USD 5.14 Billion | |

| % | |

|

Integrated Marine Automation System Market Overview

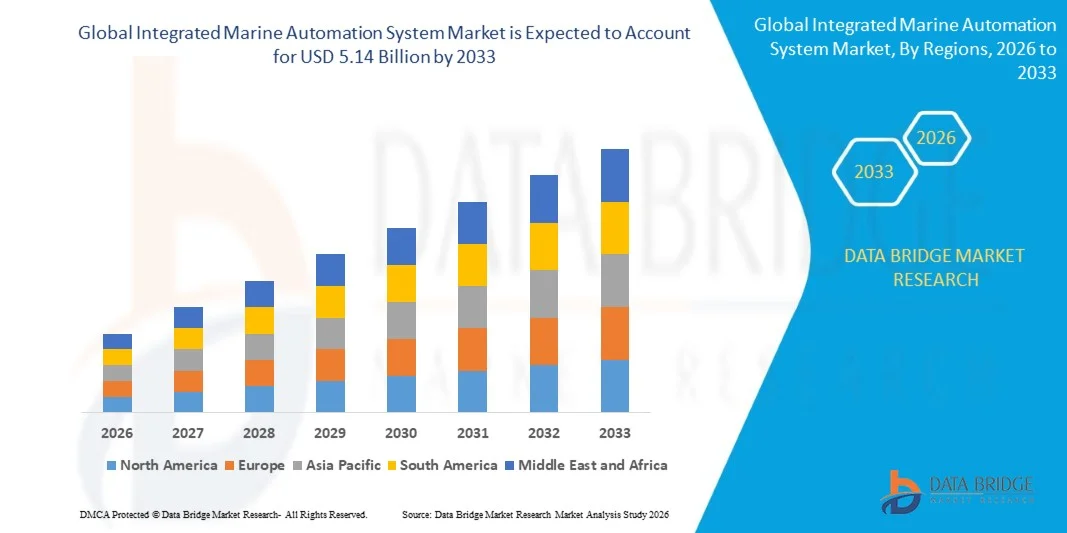

The Integrated Marine Automation System Market was valued at USD 4.23 Billion in 2025 and is projected to reach USD 5.14 Billion by 2033, growing at a CAGR of 2.47% from 2026 to 2033. The market is experiencing consistent growth driven by increasing adoption of smart shipping technologies, rising demand for vessel efficiency optimization, and growing emphasis on maritime safety and regulatory compliance. Expanding deployment of AI-enabled navigation systems, predictive maintenance solutions, and digital vessel control platforms is further supporting market expansion across commercial and defense maritime sectors.

The increasing global focus on maritime digitalization and operational efficiency, combined with stringent emission reduction regulations, is accelerating the adoption of integrated automation systems across new vessels and retrofitted fleets. Ship operators are increasingly integrating advanced automation solutions to optimize fuel consumption, enhance voyage performance, and reduce human dependency in critical operations. In addition, rapid advancements in autonomous shipping technologies and smart port infrastructure are further strengthening long-term market growth.

Key Market Trends & Insights

- Asia-Pacific dominated the Integrated Marine Automation System Market with the largest revenue share of 40.9% in 2025, supported by rapid expansion of commercial shipping activities, strong shipbuilding capacity, and increasing adoption of digital maritime technologies across major economies

- The commercial ship segment led the market with a 62.5% share in 2025, driven by strong global trade expansion and increasing demand for automated navigation, engine control, and cargo handling systems

- North America is expected to be the fastest-growing region at a CAGR of 9.4% from 2026 to 2033, fueled by rapid adoption of autonomous shipping technologies, strong naval modernization programs, and increasing demand for advanced vessel efficiency solutions

- Autonomous are the fastest-growing autonomy type, projected to register a CAGR of 16.8% from 2026 to 2033, supported by rapid advancements in AI-enabled navigation, machine learning-based decision systems, and unmanned vessel technologies

- The product segment dominated the component category with a 57.8% revenue share in 2025, led by high deployment of control systems, navigation interfaces, propulsion automation units, and integrated bridge systems across new vessel builds and retrofits

- Remotely-operated accounted for 48.2% of the market in 2025, preferred by widespread deployment across commercial vessels and defense fleets where human-in-the-loop control remains essential for operational reliability

- The power management system segment is the fastest-growing solution category, with a CAGR of 15.9% from 2026 to 2033, driven by rising focus on fuel efficiency optimization and hybrid propulsion systems

Market Size & Forecast

- Global Market Value (2025): USD 4.23 Billion

- Expected Market Value (2033): USD 5.14 Billion

- Forecast CAGR (2026–2033): 2.47%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Integrated Marine Automation System Market Segmentation

|

Attributes |

Integrated Marine Automation System Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Consilium Safety Group (Sweden) · ABB (Switzerland) · Siemens (Germany) · Kongsberg Maritime (Norway) · Thales Group (France) · Marine Technologies, LLC (U.S.) · Honeywell International Inc. (U.S.) · Rolls-Royce plc (U.K.) · Praxis Automation Technology B.V. (Netherlands) · Wärtsilä (Finland) · Rockwell Automation, Inc. (U.S.) · Hyundai Heavy Industries Co., Ltd. (South Korea) · General Electric (U.S.) · TOKYO KEIKI (Japan) · FINCANTIERI S.p.A. (Italy) · Northrop Grumman (U.S.) · Jason Marine Group (Singapore) · Emerson Electric Co (U.S.) · API Marine Inc. (U.S.) |

|

Market Opportunities |

· Expansion of Autonomous Shipping Technologies in Deep-Sea Cargo Transport · Growth of Smart Port Infrastructure and Digital Maritime Ecosystems · Rising Retrofitting Demand for Legacy Vessels with Integrated Automation Systems |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Integrated Marine Automation System Market Trends

Trend: AI-Based Autonomous Vessel Adoption

The Integrated Marine Automation System market is witnessing strong adoption of AI-enabled autonomous and semi-autonomous vessel technologies aimed at improving navigation accuracy, operational safety, and voyage efficiency. Shipping companies are increasingly integrating AI-driven decision-support systems, sensor fusion, and machine learning-based route optimization to reduce human intervention in complex maritime operations. Autonomous ship trials and smart navigation projects are accelerating across commercial and defense fleets, supported by advancements in satellite communication and edge computing.

Companies such as Kongsberg Maritime have developed autonomous vessel solutions through projects such as the Yara Birkeland, the world’s first fully electric and autonomous container ship, demonstrating real-world deployment of AI-driven marine automation systems.

Integrated Marine Automation System Market Dynamics

Key Market Driver: Rising Demand for Fuel Efficiency and Cost Reduction

The increasing pressure on shipping operators to reduce fuel consumption, operational costs, and carbon emissions is significantly driving demand for integrated marine automation systems. Vessel operators are adopting advanced engine control systems, predictive maintenance tools, and real-time performance monitoring platforms to optimize fuel usage and improve fleet efficiency. Regulatory frameworks such as IMO 2030 and IMO 2050 decarbonization targets are further accelerating adoption of automation technologies across global fleets.

Companies such as Wärtsilä and ABB are actively providing energy-efficient marine automation and propulsion optimization solutions, enabling ship operators to reduce fuel consumption and emissions through intelligent vessel control systems.

Key Restraint/Challenge: High System Cost and Integration Complexity

High installation costs and complex integration requirements remain a major challenge in the adoption of integrated marine automation systems, particularly for retrofitting older vessels. Integration of advanced digital control systems, sensors, and AI-based navigation platforms requires significant capital investment and skilled technical expertise. Compatibility issues with legacy ship systems and long installation downtime further slow down adoption across mid-sized shipping operators.

The deployment of integrated bridge and automation upgrades across aging commercial fleets in Europe highlights the operational and financial challenges associated with large-scale system modernization in the maritime sector.

Key Market Opportunity: Growth of Smart Port Infrastructure and Digital Maritime Ecosystems

The expansion of smart ports and digital maritime ecosystems is creating significant opportunities for integrated marine automation system providers. Ports are increasingly adopting AI-based traffic management, automated cargo handling systems, and real-time vessel tracking solutions to enhance operational efficiency and reduce turnaround time. Integration between port infrastructure and vessel automation systems is enabling seamless data exchange and improved supply chain visibility.

Companies such as Siemens and Honeywell are actively involved in developing smart port solutions, including automated terminal systems and digital control platforms, supporting the broader adoption of integrated marine automation technologies across global maritime trade routes.

Integrated Marine Automation System Market Scope

The integrated marine automation system market is segmented on the basis of autonomy, ship type, component, end-user, and solution.

- By Autonomy

On the basis of autonomy, the Integrated Marine Automation System Market is segmented into autonomous, remotely-operated, and partial automation systems. The Remotely-Operated segment dominated the market with the largest share of 48.2% in 2025, driven by widespread deployment across commercial vessels and defense fleets where human-in-the-loop control remains essential for operational reliability. Increasing demand for real-time monitoring and centralized vessel control systems strengthens adoption across long-haul shipping operations. Integration with advanced sensor networks and predictive maintenance tools further enhances operational efficiency. The segment continues to benefit from cost-effective implementation compared to fully autonomous systems.

The Autonomous segment is projected to register the fastest growth at a CAGR of 16.8% from 2026 to 2033, supported by rapid advancements in AI-enabled navigation, machine learning-based decision systems, and unmanned vessel technologies. Expanding trials of autonomous cargo ships and naval drones is accelerating commercialization across developed maritime corridors. Rising emphasis on crew reduction and safety enhancement is further encouraging adoption. Continuous improvements in satellite communication and edge computing are strengthening system reliability in deep-sea operations. Regulatory progress toward autonomous vessel certification is reinforcing long-term growth momentum.

- By Ship Type

On the basis of ship type, the Integrated Marine Automation System Market is segmented into commercial ships and defense vessels. The Commercial Ship segment dominated the market with a share of 62.5% in 2025, driven by strong global trade expansion and increasing demand for automated navigation, engine control, and cargo handling systems. Shipping operators are prioritizing fuel efficiency optimization and voyage performance management, which strengthens automation deployment across container ships, bulk carriers, and tankers. Rising adoption of smart port connectivity further enhances operational coordination. Large-scale fleet modernization programs continue to support segment leadership.

The Defense segment is projected to register the fastest growth at a CAGR of 14.9% from 2026 to 2033, driven by increasing naval modernization programs and rising demand for intelligent combat support systems. Integration of automation in surveillance, threat detection, and mission-critical vessel operations is improving strategic readiness. Growing investments in unmanned surface vessels and hybrid naval platforms are further accelerating adoption. Enhanced focus on maritime security across contested waters is supporting procurement of advanced automation systems. Continuous upgrades in naval digital infrastructure are reinforcing segment expansion.

- By Component

On the basis of component, the Integrated Marine Automation System Market is segmented into product and services. The Product segment dominated the market with a share of 57.8% in 2025, driven by high deployment of control systems, navigation interfaces, propulsion automation units, and integrated bridge systems across new vessel builds and retrofits. Increasing demand for integrated hardware-software platforms is enhancing operational precision and safety. Shipbuilders are prioritizing advanced automation products to comply with strict maritime regulations. Continuous technological upgrades in onboard systems further reinforce dominance.

The Services segment is projected to register the fastest growth at a CAGR of 15.6% from 2026 to 2033, driven by rising demand for maintenance, system integration, remote diagnostics, and lifecycle support services. Growing fleet digitization is increasing reliance on continuous software updates and cybersecurity management. Expansion of aftermarket service contracts across global shipping operators is strengthening recurring revenue streams. Increasing complexity of automation systems is encouraging outsourcing of technical support. Digital twin-based monitoring services are further accelerating segment growth.

- By End-User

On the basis of end-user, the Integrated Marine Automation System Market is segmented into OEM and aftermarket. The OEM segment dominated the market with a share of 66.3% in 2025, driven by strong integration of automation systems during vessel construction and new ship deliveries. Shipbuilders are increasingly embedding advanced control architectures at the design stage to enhance efficiency and regulatory compliance. Rising demand for smart ships and digital-ready fleets is further strengthening OEM adoption. Large-scale orders from commercial shipping companies support sustained demand. Standardization of automation platforms across new builds reinforces segment leadership.

The Aftermarket segment is projected to register the fastest growth at a CAGR of 14.2% from 2026 to 2033, driven by increasing retrofitting of legacy vessels with modern automation systems. Operators are focusing on upgrading existing fleets to improve fuel efficiency and operational safety. Rising maintenance requirements for complex digital systems are boosting aftermarket service demand. Expansion of global shipping fleets with aging vessels is further accelerating upgrades. Growing emphasis on lifecycle optimization is supporting long-term aftermarket expansion.

- By Solution

On the basis of solution, the Integrated Marine Automation System Market is segmented into power management systems, vessel management systems, process control systems, and safety systems. The Vessel Management System segment dominated the market with a share of 39.6% in 2025, driven by its critical role in centralized monitoring, navigation control, and operational coordination across modern vessels. Increasing integration of digital dashboards and real-time analytics is enhancing situational awareness for ship operators. Strong adoption across commercial fleets supports continuous deployment. Integration with IoT-based maritime platforms further strengthens its dominance.

The Power Management System segment is projected to register the fastest growth at a CAGR of 15.9% from 2026 to 2033, driven by rising focus on fuel efficiency optimization and hybrid propulsion systems. Increasing adoption of electric and LNG-powered vessels is accelerating demand for advanced energy control solutions. Integration of renewable energy sources onboard ships is further enhancing system relevance. Growing regulatory pressure to reduce emissions is driving energy optimization technologies. Continuous innovation in smart grid-based vessel systems is reinforcing segment growth.

Integrated Marine Automation System Market Regional Analysis

Asia-Pacific dominated the integrated marine automation system market and accounted for the largest revenue share of 40.9% in 2025, supported by rapid expansion of commercial shipping activities, strong shipbuilding capacity, and increasing adoption of digital maritime technologies across major economies. The region benefits from large-scale investments in port modernization, growing seaborne trade, and rising demand for fuel-efficient and automated vessel operations. Increasing integration of smart navigation systems, engine automation, and vessel performance monitoring solutions is further strengthening market growth. In addition, supportive government initiatives for maritime digitalization and fleet modernization are accelerating adoption of advanced automation systems across both commercial and defense segments.

China Integrated Marine Automation System Market Insight

China held the largest share in the Asia-Pacific Integrated Marine Automation System market in 2025, driven by its dominant shipbuilding industry, strong export-oriented maritime trade, and rapid adoption of smart ship technologies. The country has a highly developed shipyard ecosystem that integrates advanced automation systems into new vessel construction at scale. Growing investments in autonomous navigation systems, AI-based vessel monitoring, and intelligent port infrastructure are further strengthening market expansion. In addition, increasing focus on naval modernization and expansion of commercial fleet capacity is reinforcing China’s leadership in maritime automation adoption.

India Integrated Marine Automation System Market Insight

India is witnessing the fastest growth in the Asia-Pacific region, driven by expanding coastal shipping activities, rising investments in port infrastructure under maritime development programs, and increasing adoption of digital vessel management systems. Growing demand for efficient cargo transportation and modernization of aging fleets is accelerating deployment of automation technologies. The country is also benefiting from rising defense expenditure focused on naval surveillance and operational efficiency improvements. In addition, increasing integration of smart shipping solutions across inland waterways and coastal trade routes is supporting long-term market expansion.

Europe Integrated Marine Automation System Market Insight

The Europe Integrated Marine Automation System market is expanding steadily, supported by strong regulatory focus on maritime safety, decarbonization goals, and advanced shipbuilding capabilities. The region is witnessing increased adoption of vessel automation systems across commercial fleets, offshore vessels, and naval platforms. Rising demand for energy-efficient shipping operations and compliance with strict emission standards is strengthening market penetration. In addition, growing investments in autonomous ship trials and digital maritime infrastructure are supporting technological advancement across major European ports and shipping corridors.

Germany Integrated Marine Automation System Market Insight

Germany accounted for the largest share in the Europe Integrated Marine Automation System market in 2025, driven by its advanced shipbuilding industry, strong engineering capabilities, and high adoption of industrial automation technologies. The country has a well-established maritime manufacturing base that integrates sophisticated control systems into commercial and defense vessels. Increasing demand for smart navigation systems, predictive maintenance solutions, and energy-efficient vessel operations is further supporting market growth. In addition, strong focus on maritime digitalization and sustainability initiatives is reinforcing Germany’s leadership in regional adoption.

U.K. Integrated Marine Automation System Market Insight

The U.K. market is supported by increasing modernization of naval fleets, growing adoption of autonomous maritime technologies, and strong emphasis on maritime security systems. Rising investments in smart vessel control systems and digital navigation platforms are driving market expansion across commercial and defense applications. The country is also witnessing increased integration of AI-based monitoring and remote vessel operation systems. In addition, development of next-generation naval programs and expansion of offshore energy logistics are further supporting adoption of integrated marine automation solutions.

North America Integrated Marine Automation System Market Insight

North America is projected to grow at the fastest CAGR of 9.4% from 2026 to 2033, driven by rapid adoption of autonomous shipping technologies, strong naval modernization programs, and increasing demand for advanced vessel efficiency solutions. Rising investments in digital maritime infrastructure and smart port development are further accelerating market expansion. The region is also witnessing strong integration of AI, IoT, and cloud-based vessel management systems across commercial fleets. In addition, stringent regulatory focus on emissions reduction and operational safety is boosting adoption of next-generation marine automation systems.

U.S. Integrated Marine Automation System Market Insight

The U.S. accounted for the largest share in the North America Integrated Marine Automation System market in 2025, supported by strong naval modernization initiatives, advanced maritime technology development, and extensive commercial shipping operations. The country benefits from high adoption of digital vessel management platforms, predictive maintenance systems, and autonomous navigation technologies. Growing investments in unmanned surface vessels and smart defense fleets are further strengthening market growth. In addition, increasing focus on fuel efficiency optimization and maritime cybersecurity is reinforcing the U.S. leadership position in the regional market.

Integrated Marine Automation System Market Share

The integrated marine automation system industry is primarily led by well-established companies, including:

- Consilium Safety Group (Sweden)

- ABB (Switzerland)

- Siemens (Germany)

- Kongsberg Maritime (Norway)

- Thales Group (France)

- Marine Technologies, LLC (U.S.)

- Honeywell International Inc. (U.S.)

- Rolls-Royce plc (U.K.)

- Praxis Automation Technology B.V. (Netherlands)

- Wärtsilä (Finland)

- Rockwell Automation, Inc. (U.S.)

- Hyundai Heavy Industries Co., Ltd. (South Korea)

- General Electric (U.S.)

- TOKYO KEIKI (Japan)

- FINCANTIERI S.p.A. (Italy)

- Northrop Grumman (U.S.)

- Jason Marine Group (Singapore)

- Emerson Electric Co (U.S.)

- API Marine Inc. (U.S.)

Latest Developments in Integrated Marine Automation System Market

- In January 2026, Japan committed to advancing AI-powered robotics in shipbuilding, targeting practical deployment within one year to address persistent labor shortages in the maritime manufacturing sector. This development is expected to accelerate automation adoption across shipyards, improve production efficiency, and strengthen demand for integrated marine automation systems linked with smart manufacturing and vessel control technologies. It also supports faster digital transformation of ship design and construction processes, reinforcing long-term competitiveness in advanced maritime automation markets

- In November 2025, HD Hyundai and Siemens signed a memorandum aimed at modernizing U.S. commercial shipbuilding through the deployment of digital twin technology and industrial software solutions. This collaboration is expected to enhance ship design accuracy, optimize lifecycle vessel performance, and increase integration of advanced automation systems across new builds. The initiative is strengthening demand for connected marine automation platforms that enable real-time monitoring, predictive maintenance, and operational efficiency improvements in commercial fleets

- In November 2025, South Korea exempted the feasibility study requirement for a Level 4 autonomous ship project, accelerating development of core technologies targeting deployment by 2032. This regulatory relaxation is expected to fast-track innovation in autonomous navigation, AI-driven vessel control, and remote operations systems. It is also likely to boost investment in high-level marine automation solutions, strengthening South Korea’s position in next-generation autonomous shipping technologies and expanding the global integrated marine automation ecosystem

- In June 2023, Wärtsilä Automation, Navigation, and Control Systems (ANCS) launched an advanced upgrade solution for existing marine engine governor systems, enabling extended system lifespan alongside improved fuel efficiency and reduced emissions. The solution leverages AI-based optimization and digital control technologies to enhance engine performance across multiple vessel types. This development is strengthening retrofit demand in the integrated marine automation market, particularly for fuel optimization and emissions compliance solutions in aging fleets

- In December 2020, Rolls-Royce acquired Servowatch Systems, a British marine automation company specializing in ship control and monitoring systems, to strengthen its Power Systems division. This acquisition enhanced Rolls-Royce’s ability to deliver integrated “bridge-to-propeller” automation solutions across vessel operations. The integration of Servowatch technology expanded its marine automation portfolio, improving competitiveness in advanced ship control systems and reinforcing consolidation trends within the Integrated Marine Automation System Market

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Integrated Marine Automation System Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Integrated Marine Automation System Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Integrated Marine Automation System Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.