Global Iot Middleware Market

Market Size in USD Billion

CAGR :

%

USD

14.74 Billion

USD

57.72 Billion

2025

2033

USD

14.74 Billion

USD

57.72 Billion

2025

2033

| 2026 –2033 | |

| USD 14.74 Billion | |

| USD 57.72 Billion | |

| % | |

|

What is the IOT Middleware Market Size and Growth Rate?

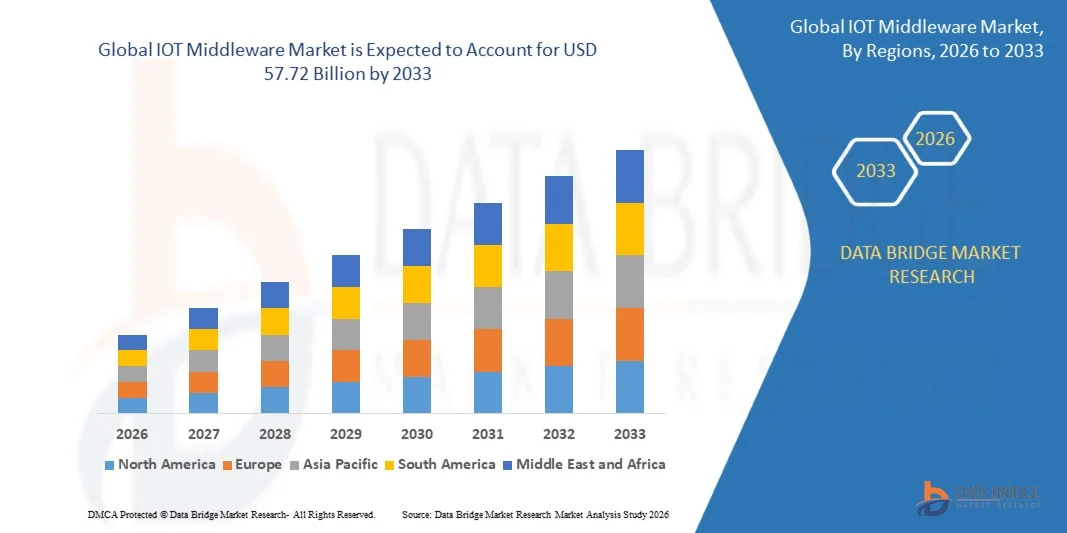

- The IOT Middleware Market size was valued at USD 14.74 billion in 2025 and is expected to reach USD 57.72 billion by 2033, at a CAGR of 18.60% during the forecast period

- Rise in the need for centralized monitoring is a crucial factor accelerating the market growth, also rise in the adoption of cloud, increase in the evolution of high-speed network technologies, increase in the adoption of cloud of things technology in organizations to address the problem of data storage and management and increase in the trend of smart homes, connected cities & factories, connected cars, wearables, consumer electronics, and others are the major factors among others boosting the internet of things (IoT) middleware market

What are the Major Takeaways of IOT Middleware Market?

- Increase in the shift toward outcome and pull economies, rise in the adoption of IoT in SMEs and increase in the drones for the enforcement of compliance will further create new opportunities for internet of things (IoT) middleware market in the forecast period mentioned above

- However, rise in the integration with legacy systems, absence of uniform IoT standards, lack of interoperability and rise in the concerns over data security and privacy are the major factors among others restraining the market growth, while dearth of skilled workforce and continuous implementation and security challenges and continuous disruption in logistics and supply chain will further challenge the internet of things (IoT) middleware market

- North America dominated the IoT Middleware market with a 32.16% revenue share in 2025, driven by rapid adoption of cloud computing, strong digital transformation initiatives, and large-scale IoT deployments across the U.S. and Canada

- Asia-Pacific is projected to register the fastest CAGR of 7.12% from 2026 to 2033, driven by expanding industrial automation, rising smart city investments, rapid 5G deployment, and increasing IoT device penetration across China, Japan, India, South Korea, and Southeast Asia

- The Device Management segment dominated the market with a 38.7% share in 2025, driven by the rapid expansion of connected devices across industrial, commercial, and consumer environments

Report Scope and IOT Middleware Market Segmentation

|

Attributes |

IOT Middleware Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, pricing analysis, brand share analysis, consumer survey, demography analysis, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

What is the Key Trend in the IOT Middleware Market?

“Increasing Shift Toward Cloud-Native, AI-Integrated, and Edge-Enabled IoT Middleware Platforms”

- The IoT Middleware market is witnessing strong adoption of cloud-native and edge-enabled platforms designed to support large-scale device connectivity, real-time data processing, and seamless integration across heterogeneous IoT ecosystems

- Vendors are introducing AI-powered middleware solutions with advanced analytics, device orchestration, API management, and secure data routing to enhance operational efficiency and scalability

- Growing demand for lightweight, interoperable, and microservices-based middleware architectures is driving deployment across manufacturing, smart cities, healthcare, and industrial automation environments

- For instance, companies such as Microsoft, Amazon Web Services, IBM, and SAP have enhanced their IoT middleware platforms with edge computing support, AI-driven analytics, and improved device lifecycle management capabilities

- Increasing need for secure data exchange, real-time monitoring, and multi-cloud interoperability is accelerating the transition toward flexible and software-centric middleware ecosystems

- As IoT deployments expand in complexity and scale, IoT middleware platforms will remain essential for device integration, data harmonization, and intelligent automation across connected environments

What are the Key Drivers of IOT Middleware Market?

- Rising adoption of IoT devices across smart manufacturing, connected vehicles, smart grids, healthcare monitoring, and retail automation is driving demand for scalable middleware solutions

- For instance, during 2025, leading vendors such as Cisco Systems and Oracle expanded their IoT middleware capabilities to support enhanced data analytics, secure device provisioning, and multi-cloud integration

- Growing implementation of Industry 4.0 initiatives, digital twins, and predictive maintenance solutions is accelerating middleware deployment across global enterprises

- Advancements in edge computing, 5G connectivity, API standardization, and containerized application frameworks have strengthened platform flexibility and performance

- Increasing cybersecurity concerns and regulatory compliance requirements are encouraging enterprises to adopt middleware platforms with integrated security, encryption, and access control mechanisms

- Supported by sustained investments in digital transformation, smart infrastructure, and enterprise automation, the IoT Middleware market is expected to witness robust long-term growth

Which Factor is Challenging the Growth of the IOT Middleware Market?

- High implementation and integration costs associated with large-scale IoT middleware deployments restrict adoption among small and medium-sized enterprises

- For instance, during 2024–2025, supply chain disruptions, rising cloud infrastructure expenses, and increased cybersecurity investments elevated overall deployment costs for several global solution providers

- Complexity in integrating diverse legacy systems, multiple communication protocols, and heterogeneous device ecosystems increases deployment timelines and technical challenges

- Data privacy regulations, cross-border data transfer restrictions, and compliance requirements create operational hurdles in global IoT rollouts

- Competition from in-house middleware development, open-source platforms, and vertically integrated IoT ecosystems creates pricing pressure and limits differentiation

- To address these challenges, companies are focusing on modular architectures, subscription-based pricing models, low-code integration tools, and enhanced security frameworks to accelerate global adoption of IoT middleware solutions

How is the IOT Middleware Market Segmented?

The market is segmented on the basis of platform type, organization size, and vertical.

• By Platform Type

On the basis of platform type, the IoT Middleware market is segmented into Device Management, Application Management, and Connectivity Management. The Device Management segment dominated the market with a 38.7% share in 2025, driven by the rapid expansion of connected devices across industrial, commercial, and consumer environments. Enterprises increasingly require centralized platforms for device provisioning, monitoring, firmware updates, lifecycle management, and remote diagnostics. As IoT ecosystems grow in scale and complexity, device management platforms ensure operational continuity, security enforcement, and real-time performance visibility.

The Connectivity Management segment is projected to grow at the fastest CAGR from 2026 to 2033, supported by rising deployment of 5G, LPWAN, and edge networks. Increasing need for seamless network orchestration, SIM management, and secure data routing across multi-network environments is accelerating adoption of connectivity-focused middleware solutions.

• By Organization Size

On the basis of organization size, the IoT Middleware market is segmented into Large Enterprises and Small and Medium-Sized Enterprises. The Large Enterprises segment dominated the market with a 64.5% share in 2025, owing to significant investments in digital transformation, Industry 4.0 initiatives, and enterprise-wide IoT deployments. Large organizations require scalable middleware platforms capable of handling high device volumes, real-time analytics, cross-border compliance, and multi-cloud integration. Their financial strength and technical capabilities enable faster adoption of advanced middleware architectures.

The Small and Medium-Sized Enterprises segment is expected to grow at the fastest CAGR from 2026 to 2033, driven by increasing availability of cloud-based, subscription-driven, and low-code middleware platforms. Cost-effective SaaS models and simplified deployment frameworks are enabling SMEs to adopt IoT solutions for automation, asset tracking, and predictive maintenance.

• By Vertical

On the basis of vertical, the IoT Middleware market is segmented into Manufacturing, Government and Defense, Automotive and Transportation, Energy and Utilities, Healthcare, Retail, Banking, Financial Services and Insurance, and Others. The Manufacturing segment dominated the market with a 27.9% share in 2025, driven by strong adoption of smart factory solutions, predictive maintenance systems, industrial automation, and digital twin technologies. Middleware platforms enable seamless device integration, real-time production monitoring, and operational analytics across connected manufacturing environments.

The Energy and Utilities segment is projected to grow at the fastest CAGR from 2026 to 2033, fueled by increasing deployment of smart grids, intelligent metering systems, renewable energy monitoring, and distributed energy resource management. Rising emphasis on energy efficiency, remote infrastructure monitoring, and grid modernization is accelerating middleware adoption across global utility networks.

Which Region Holds the Largest Share of the IOT Middleware Market?

- North America dominated the IoT Middleware market with a 32.16% revenue share in 2025, driven by rapid adoption of cloud computing, strong digital transformation initiatives, and large-scale IoT deployments across the U.S. and Canada. Enterprises across manufacturing, healthcare, retail, and energy sectors are increasingly deploying middleware platforms to manage connected devices, enable real-time analytics, and ensure secure data integration

- Leading technology providers in North America are introducing AI-enabled, edge-integrated, and cloud-native IoT middleware solutions with enhanced security, scalability, and multi-cloud interoperability, strengthening the region’s technological advantage. Continuous investment in smart infrastructure, 5G networks, and enterprise automation supports long-term market expansion

- High concentration of technology innovators, strong venture capital ecosystem, and mature IT infrastructure further reinforce North America’s leadership in the global IoT middleware landscape

U.S. IoT Middleware Market Insight

The U.S. is the largest contributor within North America, supported by extensive enterprise IoT adoption and strong presence of major cloud and software providers. Rapid implementation of Industry 4.0 strategies, smart city projects, and connected healthcare systems drives demand for scalable middleware platforms. Increasing deployment of AI-driven analytics, cybersecurity frameworks, and edge computing solutions further accelerates domestic market growth.

Canada IoT Middleware Market Insight

Canada contributes steadily to regional expansion, supported by government-backed innovation initiatives and increasing adoption of IoT solutions in energy, utilities, and smart infrastructure projects. Growing demand for secure device management, data integration, and cloud connectivity strengthens middleware deployment across enterprises and public sector organizations.

Asia-Pacific IoT Middleware Market

Asia-Pacific is projected to register the fastest CAGR of 7.12% from 2026 to 2033, driven by expanding industrial automation, rising smart city investments, rapid 5G deployment, and increasing IoT device penetration across China, Japan, India, South Korea, and Southeast Asia. Strong growth in manufacturing digitization and connected infrastructure significantly accelerates middleware demand across the region.

China IoT Middleware Market Insight

China is a major contributor to Asia-Pacific growth due to large-scale smart manufacturing initiatives, smart city programs, and expanding domestic IoT ecosystems. Government support for digital infrastructure and industrial modernization continues to drive middleware platform adoption.

Japan IoT Middleware Market Insight

Japan demonstrates steady growth supported by advanced automation technologies, robotics integration, and strong industrial IoT adoption. Emphasis on precision engineering and digital transformation strengthens middleware implementation across multiple industries.

India IoT Middleware Market Insight

India is emerging as a high-growth market driven by expanding digital infrastructure, startup ecosystem growth, and government-backed smart city and manufacturing initiatives. Rising enterprise cloud adoption further supports middleware expansion.

South Korea IoT Middleware Market Insight

South Korea contributes significantly due to strong 5G infrastructure, advanced electronics manufacturing, and smart factory investments. Increasing deployment of connected devices and AI-driven automation supports sustained IoT middleware market growth.

Which are the Top Companies in IOT Middleware Market?

The IOT Middleware industry is primarily led by well-established companies, including:

- Microsoft (U.S.)

- IBM (U.S.)

- PTC (U.S.)

- Amazon Web Services, Inc. (U.S.)

- SAP (Germany)

- Cisco Systems (U.S.)

- Hitachi, Ltd. (Japan)

- Hewlett Packard Enterprise Development LP (U.S.)

- Oracle (U.S.)

- Robert Bosch GmbH (Germany)

- Salesforce (U.S.)

- General Electric (U.S.)

- Schneider Electric (France)

- ClearBlade (U.S.)

- Davra (Ireland)

- MuleSoft LLC (U.S.)

- Axiros (Germany)

- TIBCO Software Inc. (U.S.)

- Siemens (Germany)

- Eurotech (Italy)

- Flutura (U.S.)

- Litmus Automation Inc. (U.S.)

- Ayla Networks Inc. (U.S.)

- QiO Technologies Ltd (U.K.)

- Aeris (U.S.)

What are the Recent Developments in IOT Middleware Market?

- In May 2024, Hitachi, Ltd. and Google LLC entered into a multi-year partnership to accelerate enterprise innovation and productivity through generative AI technologies, aiming to enhance digital transformation initiatives across industries. This collaboration is expected to create new opportunities for IoT middleware platforms by integrating AI-driven analytics, automation, and intelligent data orchestration capabilities, thereby strengthening enterprise efficiency and smart ecosystem management

- In April 2024, Microsoft Corporation and Cloud Software Group announced an eight-year strategic alliance to deliver joint cloud solutions and generative AI capabilities to over 100 million users globally. This agreement is anticipated to drive innovation within the IoT middleware market by enabling deeper integration of cloud computing and AI technologies, improving real-time data processing, scalability, and cross-platform interoperability for connected applications across diverse industry verticals

- In December 2024, Scenera, a U.S.-based AI-powered video analytics provider, acquired TnM AI, a South Korean AIoT company focused on smart city and smart factory technologies, to strengthen its artificial intelligence portfolio and expand its footprint in the Asia-Pacific region. This acquisition highlights the growing convergence of AI and IoT middleware solutions, reinforcing the demand for intelligent data platforms that support scalable, analytics-driven connected infrastructure

- In December 2024, Rev.io, a provider of billing and back-office software solutions, acquired a specialized IoT billing platform to broaden its service capabilities and enhance subscription and usage-based billing management for connected device ecosystems. This strategic move reflects the rising importance of integrated billing and revenue management solutions within the expanding IoT middleware landscape, supporting improved monetization and operational efficiency

- In September 2023, InterVision Systems LLC announced a multi-year strategic collaboration agreement with Amazon Web Services, Inc. to accelerate cloud modernization and adoption among public sector and commercial clients. This partnership leverages InterVision’s AWS expertise to deliver advanced cloud-native and data modernization solutions, ultimately reinforcing the role of scalable cloud infrastructure in strengthening IoT middleware deployments and digital transformation initiatives

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.