Global Ischemic Cerebral Stroke Market

Market Size in USD Billion

CAGR :

%

USD

5.26 Billion

USD

9.08 Billion

2025

2033

USD

5.26 Billion

USD

9.08 Billion

2025

2033

| 2026 –2033 | |

| USD 5.26 Billion | |

| USD 9.08 Billion | |

| % | |

|

Ischemic Cerebral Stroke Market Size

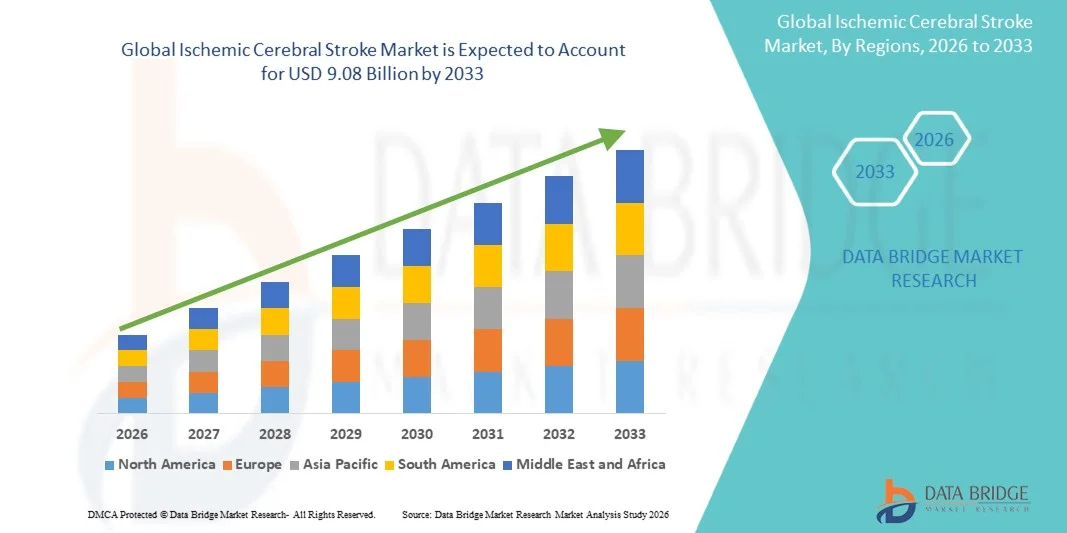

- The global ischemic cerebral stroke market size was valued at USD 5.26 billion in 2025 and is expected to reach USD 9.08 billion by 2033, at a CAGR of 7.07% during the forecast period

- The market growth is largely fueled by the rising global prevalence of ischemic cerebral stroke, increasing incidence of cardiovascular disorders, and growing awareness regarding early diagnosis and rapid treatment intervention. Advancements in neuroimaging technologies, thrombolytic therapies, and minimally invasive endovascular procedures are contributing to improved clinical outcomes and expanding treatment adoption across hospitals and specialized stroke centers

- Furthermore, increasing government initiatives focused on stroke awareness programs, expanding emergency medical services infrastructure, and growing investments in advanced stroke care facilities are establishing ischemic cerebral stroke treatment solutions as critical components of acute neurological care. These converging factors are accelerating the uptake of ischemic cerebral stroke therapies and devices, thereby significantly boosting the industry's growth

Ischemic Cerebral Stroke Market Analysis

- Ischemic cerebral stroke treatment solutions, including thrombolytic drugs, mechanical thrombectomy devices, and advanced neuroimaging systems, are critical components of modern acute stroke management. These solutions enable rapid diagnosis, timely clot removal, restoration of cerebral blood flow, and improved patient survival rates across emergency departments and specialized stroke centers

- The escalating demand for ischemic cerebral stroke therapies is primarily fueled by the rising global incidence of cardiovascular diseases, increasing geriatric population, growing awareness about early stroke symptoms, and improvements in emergency response systems. In addition, advancements in minimally invasive endovascular procedures are significantly enhancing treatment efficacy and recovery outcomes

- North America dominated the ischemic cerebral stroke market with the largest revenue share of 39.4% in 2025, driven by advanced healthcare infrastructure, high adoption of mechanical thrombectomy procedures, strong reimbursement policies, and the presence of leading medical device manufacturers. The U.S. experienced substantial growth due to the expansion of comprehensive stroke centers and increased utilization of rapid neuroimaging and clot retrieval technologies

- Asia-Pacific is expected to be the fastest-growing region in the ischemic cerebral stroke market during the forecast period, projected to expand at a CAGR of 11.8%, supported by rising stroke prevalence, improving healthcare access, expanding hospital infrastructure, and increasing government initiatives focused on cardiovascular disease management in countries such as China, India, and Japan

- The Intravenous route dominated with 63.7% share in 2025, reflecting its critical role in emergency thrombolytic treatments

Report Scope and Ischemic Cerebral Stroke Market Segmentation

|

Attributes |

Ischemic Cerebral Stroke Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Bayer AG (Germany) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Ischemic Cerebral Stroke Market Trends

“Advancements in AI-Driven Imaging and Precision Treatment Technologies”

- A significant and accelerating trend in the global ischemic cerebral stroke market is the integration of artificial intelligence (AI) in neuroimaging, diagnosis, and treatment planning to enable faster and more accurate clinical decision-making. These advanced technologies assist clinicians in identifying large vessel occlusions, assessing infarct core volume, and determining patient eligibility for thrombolysis or mechanical thrombectomy within critical time windows

- For instance, in May 2022, Viz.ai received expanded regulatory clearance for its AI-powered stroke imaging platform designed to rapidly detect suspected large vessel occlusion and alert stroke specialists in real time. Similarly, RapidAI continues to enhance its RAPID platform, which supports automated perfusion imaging analysis to guide acute stroke treatment decisions

- The adoption of advanced mechanical thrombectomy devices and next-generation stent retrievers is further shaping treatment standards. Innovations in catheter design and clot retrieval systems are improving recanalization rates and patient outcomes, particularly in comprehensive stroke centers

- In addition, growing implementation of tele-stroke networks and cloud-based imaging platforms is enabling faster consultation between primary stroke centers and neurologists, especially in remote and underserved regions. This digital transformation is reducing door-to-needle time and expanding access to timely intervention

- The increasing emphasis on precision medicine, data-driven triage, and workflow optimization is fundamentally reshaping acute stroke management protocols across hospitals worldwide

- The demand for technologically advanced diagnostic and interventional solutions is rising rapidly across developed and emerging healthcare systems as providers prioritize faster response times and improved survival and recovery outcomes

Ischemic Cerebral Stroke Market Dynamics

Driver

“Rising Global Incidence of Stroke and Expanding Access to Acute Care”

- The increasing global prevalence of ischemic cerebral stroke, driven by aging populations, sedentary lifestyles, hypertension, diabetes, and cardiovascular disorders, is a major factor fueling market growth. As the burden of cerebrovascular disease rises, healthcare systems are prioritizing early diagnosis and rapid intervention solutions

- For instance, in January 2023, Medtronic announced continued advancements in its neurovascular portfolio, including Solitaire™ stent retrievers used in mechanical thrombectomy procedures, strengthening its position in acute ischemic stroke intervention. Such strategic developments by key industry players are expected to accelerate market expansion during the forecast period

- Government initiatives and awareness campaigns promoting early stroke recognition—such as FAST (Face, Arms, Speech, Time)—are encouraging faster hospital admissions and increasing demand for diagnostic imaging and interventional therapies

- The expansion of dedicated stroke centers, improved reimbursement frameworks in developed economies, and investments in advanced CT and MRI infrastructure are further supporting treatment accessibility

- The growing availability of thrombolytic agents and endovascular procedures, combined with improved emergency medical response systems, is significantly enhancing survival rates and functional recovery, thereby driving sustained market demand

Restraint/Challenge

“High Treatment Costs and Limited Access in Low-Resource Settings”

- The high cost associated with advanced imaging systems, thrombectomy devices, intensive care management, and post-stroke rehabilitation presents a considerable barrier to market growth, particularly in low- and middle-income countries. Many healthcare facilities lack the infrastructure required to provide comprehensive stroke care

- For instance, mechanical thrombectomy procedures require specialized neurointerventional suites and trained specialists, which are often concentrated in urban tertiary hospitals, limiting access for patients in rural areas

- Delayed patient presentation beyond the therapeutic time window further restricts the use of thrombolysis and endovascular therapy, reducing treatment eligibility rates

- Regulatory complexities, stringent clinical validation requirements, and reimbursement disparities across regions can also slow the adoption of novel stroke therapies and devices

- Moreover, inadequate public awareness in certain regions regarding early stroke symptoms contributes to delayed diagnosis and poorer outcomes, indirectly limiting demand for advanced treatment solutions

- Addressing these challenges through healthcare infrastructure investment, cost optimization strategies, professional training programs, and expanded insurance coverage will be essential to ensure equitable access and sustained long-term growth in the global ischemic cerebral stroke market

Ischemic Cerebral Stroke Market Scope

The market is segmented on the basis of drug class, treatment, diagnosis, symptoms, dosage, route of administration, end-users, and distribution channel.

• By Drug Class

On the basis of drug class, the market is segmented into Calcium Channel Blockers, Thrombolytics, and Others. The Thrombolytics segment dominated the market with a revenue share of 52.3% in 2025, owing to its critical role in dissolving blood clots in acute ischemic stroke. Thrombolytics are widely used across hospitals due to their proven efficacy in reducing neuronal damage. The segment’s dominance is supported by emergency stroke protocols requiring rapid administration. Recombinant tissue plasminogen activator (rtPA) is the most commonly used thrombolytic therapy globally. Hospitals maintain well-stocked emergency kits to ensure timely treatment. Growing stroke prevalence and awareness of early intervention drive adoption. Thrombolytics benefit from favorable reimbursement schemes in developed markets. Strong clinical evidence encourages widespread physician acceptance. The segment sees adoption in both urban and semi-urban healthcare facilities. Advanced training for medical staff further ensures optimal usage. Government initiatives supporting acute stroke care reinforce growth. Ongoing research in extended window thrombolysis may enhance patient pool and adoption.

The Calcium Channel Blockers segment is expected to witness the fastest CAGR of 15.2% from 2026 to 2033, driven by their increasing use in secondary prevention of ischemic stroke. Rising hypertension prevalence and cardiovascular comorbidities increase segment adoption. Generic formulations make therapy more accessible. Expansion of preventive healthcare programs supports growth in emerging economies. Clinical guidelines recommend calcium channel blockers for long-term management. Physician awareness programs improve prescription rates. Telemedicine platforms enhance patient adherence. Integration with remote monitoring devices further boosts adoption. Government funding for chronic disease management supports usage. Patient education programs highlight benefits for recurrence prevention. The segment sees growing demand in outpatient settings. New drug delivery formulations enhance compliance and market penetration.

• By Treatment

On the basis of treatment, the market is segmented into Medication, Surgery, and Others. The Medication segment dominated the market with a share of 58.7% in 2025, driven by non-invasive pharmacological interventions like antiplatelets, anticoagulants, and thrombolytics. Medications are preferred due to rapid initiation during the acute phase. Hospitals ensure high stock levels for emergency use. Clinical guidelines strongly advocate early drug administration. Medications reduce treatment costs compared to surgical interventions. Awareness campaigns improve patient compliance. Telemedicine and digital platforms enable timely prescriptions. Government funding for stroke medications supports widespread access. Medication-based management is standard in emergency stroke protocols. Advanced formulations improve efficacy and minimize side effects. Insurance coverage increases affordability. Continuous R&D strengthens therapeutic options. Hospitals benefit from established drug supply chains ensuring constant availability.

The Surgery segment is expected to witness the fastest CAGR of 14.9% from 2026 to 2033, due to advancements in minimally invasive procedures like mechanical thrombectomy. Rising availability of neuro-interventional facilities drives adoption. Severe or complex stroke cases increasingly require surgical interventions. Insurance support enhances patient access. Technological innovations, including robotic and AI-assisted surgery, improve outcomes. Expansion of dedicated stroke centers facilitates procedure adoption. Post-operative rehabilitation programs increase success rates. Telehealth monitoring supports follow-up care. Minimally invasive surgeries reduce hospital stay duration, driving preference. Increased trained neurosurgeon availability supports growth. Patient awareness campaigns highlight effectiveness of surgery. Continuous development of surgical devices enhances segment expansion.

• By Diagnosis

On the basis of diagnosis, the market is segmented into CT Angiography and CT Scan, Carotid Duplex Scanning, MRI, Digital Subtraction Angiography, and Others. The CT Angiography and CT Scan segment dominated with 49.8% market share in 2025, owing to rapid and accurate detection of ischemic lesions. Hospitals rely on CT imaging for emergency stroke evaluation and treatment eligibility. CT scans are widely available and cost-effective compared to MRI. Integration with PACS systems ensures smooth workflow. Short scanning times enable fast triage and treatment initiation. Government initiatives supporting emergency imaging infrastructure boost adoption. Emergency departments prioritize CT for thrombolytic therapy. AI-assisted CT imaging improves diagnostic accuracy. Continuous technological advancements enhance image resolution. High patient throughput supports consistent demand. Training programs ensure accurate interpretation. Hospitals in both urban and semi-urban regions utilize CT extensively.

The MRI segment is expected to witness the fastest CAGR of 13.7% from 2026 to 2033, due to its higher sensitivity in detecting early ischemic changes and superior tissue evaluation. Expansion of MRI facilities in hospitals and clinics supports growth. Advanced sequences like diffusion-weighted imaging enhance diagnostic precision. Increasing availability of high-field MRI systems improves image resolution and diagnostic accuracy. Integration of AI-assisted imaging tools allows faster detection and automated analysis of ischemic lesions. Rising adoption of MRI in outpatient and emergency stroke centers enhances early diagnosis. Continuous training of radiologists and technicians improves utilization efficiency and interpretation accuracy. Government and private investments in healthcare infrastructure expand MRI accessibility in semi-urban and rural regions. Technological innovations, including portable and open MRI systems, increase patient comfort and scanning feasibility. Collaboration with telemedicine platforms allows remote review of MRI scans, boosting early intervention rates.

• By Symptoms

On the basis of symptoms, the market is segmented into Sudden Onset of Hemiparesis, Quadriparesis, Monoparesis, Monocular Visual Loss, Diplopia, Visual Field Deficits, Hemisensory Deficits, Dysarthria, Facial Droop, Vertigo, Ataxia, Nystagmus, Aphasia, Loss of Consciousness, and Others. The Sudden Onset of Hemiparesis segment dominated with 55.6% share in 2025, as it is the most common early indicator of ischemic stroke. Early recognition by emergency teams ensures rapid intervention and reduces long-term disability. Hospitals and clinics follow strict diagnostic protocols for hemiparesis detection. Awareness campaigns by government and NGOs enhance timely patient visits. Diagnostic imaging, including CT and MRI, is rapidly performed for confirmation. Rehabilitation programs prioritize hemiparesis cases to restore motor function. Multidisciplinary stroke teams focus on functional recovery and coordinated care. Availability of thrombolytics and surgical interventions increases treatment efficiency. Emergency stroke units and dedicated neurocritical care facilities further strengthen adoption. Government initiatives support hemiparesis-related stroke care programs. Patient education programs improve recognition of early symptoms in both urban and rural areas. Technological integration in stroke units enhances monitoring and follow-up care. Continuous training for medical personnel ensures accurate assessment and intervention.

The Vertigo and Ataxia segments are expected to witness the fastest CAGR of 15.1% from 2026 to 2033, due to improved recognition of posterior circulation strokes and better diagnostic modalities. Increased use of advanced MRI and AI-based imaging facilitates early detection. Telehealth tools enable remote monitoring of at-risk patients, improving adherence to treatment. Expansion of specialty neurology clinics supports outpatient management of these symptoms. Rising awareness of subtle stroke signs among patients and caregivers contributes to early diagnosis. Hospital protocols increasingly include vertigo screening for high-risk populations. Digital patient records and AI-assisted symptom tracking enhance early detection rates. Growing geriatric population with comorbidities increases segment demand. Training programs for clinicians emphasize accurate assessment of balance and coordination deficits. Technological adoption, including wearable monitoring devices, improves functional outcome tracking. Preventive interventions and timely therapy reduce complications and support segment growth. Government and private initiatives promote awareness campaigns targeting neurological symptom recognition.

• By Dosage

On the basis of dosage, the market is segmented into Injection, Tablets, and Others. The Injection segment dominated with 61.2% market share in 2025, primarily for intravenous thrombolytic therapy in acute ischemic stroke. Rapid systemic delivery ensures immediate therapeutic effects and minimizes brain damage. Hospitals maintain stock for emergency administration at stroke units. Monitoring protocols ensure patient safety during administration. Early intervention programs drive segment adoption across urban and semi-urban hospitals. Insurance coverage supports access to high-cost thrombolytic injections. Ongoing R&D in injection formulations improves efficacy and reduces side effects. Availability across tertiary care centers and emergency departments strengthens adoption. Medical staff training ensures correct dosing and reduces complications. Emergency stroke protocols prioritize intravenous therapy for eligible patients. Government-funded programs enhance accessibility in public hospitals. Integration with telehealth platforms supports post-injection follow-up and monitoring. Expansion of hospital pharmacy networks ensures consistent supply and availability.

The Tablet segment is expected to witness the fastest CAGR of 14.5% from 2026 to 2033, driven by long-term use of oral anticoagulants and antiplatelets for secondary prevention. Patient convenience and homecare management enhance adherence. Growth is supported by increasing awareness of stroke recurrence prevention. Generic formulations improve affordability and accessibility. Outpatient clinics and community pharmacies facilitate tablet distribution. Integration with mobile apps and reminders increases patient compliance. Clinical guidelines recommend oral therapies for long-term management. Expansion of preventive health programs boosts prescription rates. Insurance and reimbursement schemes enhance accessibility. Education campaigns encourage adherence to daily tablet regimens. Telemedicine monitoring supports dose adjustments and tracking. Availability in rural and semi-urban pharmacies strengthens market penetration.

• By Route of Administration

On the basis of route, the market is segmented into Oral, Intravenous, and Others. The Intravenous route dominated with 63.7% share in 2025, reflecting its critical role in emergency thrombolytic treatments. Rapid systemic delivery is essential for stroke survival and minimizing neuronal damage. Hospitals prioritize IV therapy availability in emergency departments. Advanced infusion pumps and protocols ensure precise dosing. High patient inflow at tertiary care centers reinforces adoption. Government-supported acute stroke programs promote timely IV therapy. Continuous medical training ensures accurate administration. Integration with hospital electronic health records enhances treatment tracking. Emergency stroke units maintain immediate IV drug availability. Early intervention guidelines reinforce intravenous therapy preference. Urban hospitals report high usage due to awareness and infrastructure. Monitoring protocols reduce adverse reactions during therapy. Pharmaceutical innovations improve stability and efficacy of IV formulations.

The Oral route is expected to witness the fastest CAGR of 15.0% from 2026 to 2033, driven by preventive therapies for high-risk patients. Oral medications are widely used in outpatient and homecare settings for long-term anticoagulation and secondary prevention. Patient-friendly formulations enhance adherence and convenience. Telemedicine and remote monitoring ensure proper intake and compliance. Preventive health programs encourage oral therapy for recurrent stroke risk management. Expansion of primary care clinics supports oral therapy adoption. Generic tablets improve affordability and accessibility. Awareness campaigns highlight the importance of oral preventive therapy. Insurance coverage and reimbursement facilitate patient access. Patient education programs support correct and consistent usage. Integration with mobile health applications improves adherence tracking. Rural and semi-urban expansion boosts segment penetration.

• By End-Users

On the basis of end-users, the market is segmented into Clinic, Hospital, and Others. The hospital segment held the largest market revenue share of 65.4% in 2025, attributed to the strong presence of specialized stroke care units and advanced neuroimaging infrastructure. Hospitals remain the first point of contact for acute ischemic stroke cases due to their emergency response capabilities. The availability of CT and MRI imaging, thrombolytic therapy, and intensive care monitoring strengthens segment dominance. Multidisciplinary teams including neurologists, neurosurgeons, and critical care specialists further enhance treatment outcomes. Increasing establishment of certified stroke centers across developed and emerging economies supports revenue growth. Government investments in emergency healthcare systems significantly contribute to higher patient admissions. Hospitals are better equipped to perform complex surgical procedures such as mechanical thrombectomy. Rising incidence of cardiovascular diseases globally also drives hospitalization rates. Favorable reimbursement frameworks for inpatient stroke treatment further sustain demand. Integration of tele-stroke programs within hospital networks enhances rapid diagnosis and drug administration. Continuous infrastructure expansion and adoption of advanced life-support systems reinforce the segment’s leading position.

The clinic segment is expected to witness the fastest CAGR of 16.8% from 2026 to 2033, driven by increasing demand for post-stroke rehabilitation and long-term neurological care. Clinics play a vital role in follow-up consultations and secondary stroke prevention programs. Rising awareness about early symptom management is encouraging outpatient visits. Expansion of specialty neurology and rehabilitation clinics is accelerating segment growth. Clinics provide cost-effective treatment options compared to prolonged hospital stays. Increasing elderly population requiring routine monitoring further supports demand. Growth in preventive healthcare initiatives promotes regular neurological screening. Technological advancements in portable diagnostic equipment enable clinics to manage mild stroke cases efficiently. Improved accessibility in semi-urban and rural areas enhances patient reach. Rising partnerships between hospitals and outpatient centers further strengthen the referral network. Growing focus on personalized rehabilitation therapy also contributes to sustained CAGR during the forecast period.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Online Pharmacy. The hospital pharmacy segment dominated the market with a revenue share of 48.5% in 2025, primarily due to immediate availability of critical stroke medications within hospital premises. During acute stroke management, rapid drug administration is essential to minimize neurological damage. Hospital pharmacies maintain specialized stock of thrombolytics, anticoagulants, and supportive therapies. Strong procurement contracts and centralized supply chains enhance operational efficiency. Increasing hospital admissions for emergency stroke treatment support high dispensing volumes. Availability of trained pharmacists ensures proper dosage and monitoring of high-risk medications. Strict regulatory compliance and quality assurance standards further reinforce segment leadership. Rising government funding for hospital infrastructure strengthens pharmaceutical procurement capacity. Integration of electronic medical records streamlines prescription management. Expansion of tertiary care hospitals globally continues to support segment dominance.

The online pharmacy segment is projected to witness the fastest CAGR of 20.4% from 2026 to 2033, fueled by rapid digitalization of healthcare services. Increasing internet penetration and smartphone usage are encouraging patients to order medications online. Online platforms provide convenience, competitive pricing, and doorstep delivery services. Growing preference for chronic medication refills through digital portals supports recurring demand. Regulatory approvals for e-pharmacies in multiple regions enhance market credibility. Secure digital payment systems and prescription upload features strengthen consumer trust. Expansion of telemedicine consultations further boosts online drug sales. Rising awareness about preventive stroke therapy also contributes to sustained growth. Increasing investments in healthcare e-commerce infrastructure accelerate scalability. The convenience factor, combined with broader product availability, ensures strong forecast expansion for this segment.

Ischemic Cerebral Stroke Market Regional Analysis

- North America dominated the ischemic cerebral stroke market with the largest revenue share of 39.4% in 2025. This leadership is attributed to advanced healthcare infrastructure, high adoption of mechanical thrombectomy procedures, strong reimbursement policies, and the presence of leading medical device manufacturers

- The market experienced substantial growth due to the expansion of comprehensive stroke centers and increased utilization of rapid neuroimaging and clot retrieval technologies

- In addition, well-established emergency medical services and widespread public awareness of stroke symptoms have facilitated faster hospital admissions, supporting early intervention and improved patient outcomes

U.S. Ischemic Cerebral Stroke Market Insight

The U.S. ischemic cerebral stroke market accounted for a significant portion of North America’s revenue, driven by high adoption rates of mechanical thrombectomy and thrombolytic therapies in hospitals. The growing number of stroke centers equipped with advanced CT and MRI facilities enables timely diagnosis and treatment. Increasing investment in tele-stroke networks allows smaller hospitals to access specialist consultations remotely, further enhancing treatment efficiency. The prevalence of cardiovascular risk factors such as hypertension and diabetes is also contributing to higher demand for acute stroke interventions.

Europe Ischemic Cerebral Stroke Market Insight

Europe ischemic cerebral stroke market is projected to witness steady growth in the ischemic cerebral stroke market, supported by stringent healthcare regulations, increased funding for stroke care, and rising awareness of stroke prevention and management. Urbanization, improved hospital infrastructure, and greater adoption of endovascular devices are driving market expansion. Countries such as Germany, France, and the U.K. are investing in advanced neuroimaging systems and expanding access to thrombectomy-capable centers, ensuring timely treatment for patients. In addition, initiatives to improve public stroke literacy and early symptom recognition are encouraging faster hospital admissions, positively impacting market growth.

U.K. Ischemic Cerebral Stroke Market Insight

The U.K. ischemic cerebral stroke market is expected to grow at a noteworthy CAGR due to increasing emphasis on early intervention and access to advanced stroke care. Expansion of stroke-ready hospitals and enhanced training of healthcare professionals are improving treatment delivery. Moreover, government-led initiatives aimed at reducing stroke-related mortality and morbidity, combined with higher adoption of thrombolytic therapies, are expected to continue driving market growth in both urban and semi-urban regions.

Germany Ischemic Cerebral Stroke Market Insight

Germany ischemic cerebral stroke market is anticipated to exhibit considerable market growth, fueled by well-developed hospital infrastructure, increasing awareness of stroke treatment protocols, and the adoption of minimally invasive clot retrieval devices. Investment in advanced imaging technologies such as perfusion CT and MR angiography supports timely and precise diagnosis, while government initiatives to enhance cardiovascular healthcare standards further reinforce market expansion.

Asia-Pacific Ischemic Cerebral Stroke Market Insight

The Asia-Pacific ischemic cerebral stroke market is poised to grow at the fastest CAGR of 11.8% during the forecast period. Rising stroke prevalence, improving healthcare access, expanding hospital infrastructure, and increasing government initiatives focused on cardiovascular disease management are driving growth. Countries such as China, India, and Japan are witnessing rapid urbanization and greater investment in tertiary care hospitals, leading to enhanced availability of mechanical thrombectomy procedures and advanced neuroimaging technologies. In addition, awareness campaigns and government-supported screening programs are improving early detection rates, further supporting market expansion.

Japan Ischemic Cerebral Stroke Market Insight

Japan’s ischemic cerebral stroke market is gaining momentum due to an aging population, increasing incidence of stroke, and strong focus on early diagnosis. Advanced hospital networks equipped with stroke units, combined with the integration of tele-stroke consultations, enable rapid treatment, including mechanical thrombectomy and thrombolysis. Growing healthcare expenditure and government initiatives aimed at improving cardiovascular outcomes are further accelerating market growth.

China Ischemic Cerebral Stroke Market Insight

China ischemic cerebral stroke market accounted for the largest share in the Asia-Pacific region in 2025, driven by a rising elderly population, increasing prevalence of cardiovascular risk factors, and significant expansion of tertiary care hospitals. Government initiatives promoting early stroke detection, investment in neuroimaging technologies, and increasing awareness of acute stroke treatment have contributed to greater adoption of thrombolytic therapy and mechanical thrombectomy. The growing number of specialized stroke centers is further enhancing patient access to rapid and effective interventions.

Ischemic Cerebral Stroke Market Share

The Ischemic Cerebral Stroke industry is primarily led by well-established companies, including:

• Bayer AG (Germany)

• Boehringer Ingelheim International GmbH (Germany)

• Pfizer Inc. (U.S.)

• Bristol-Myers Squibb Company (U.S.)

• Johnson & Johnson (U.S.)

• Sanofi (France)

• F. Hoffmann-La Roche Ltd (Switzerland)

• Abbott (U.S.)

• Medtronic plc (Ireland)

• Stryker Corporation (U.S.)

• Penumbra, Inc. (U.S.)

• Terumo Corporation (Japan)

• Boston Scientific Corporation (U.S.)

• Siemens Healthineers AG (Germany)

• GE HealthCare Technologies Inc. (U.S.)

• Merck & Co., Inc. (U.S.)

• Amgen Inc. (U.S.)

• Daiichi Sankyo Company, Limited (Japan)

• AstraZeneca plc (U.K.)

• Novartis AG (Switzerland)

Latest Developments in Global Ischemic Cerebral Stroke Market

- In March 2024, Medtronic introduced the Solitaire™ X Platinum+ Stent Retriever, an advanced thrombectomy device with enhanced flexibility and radial force that improves clot removal success in patients with acute ischemic stroke, reducing trauma to the vessel wall and supporting higher recanalization rates

- In October 2024, Prolong Pharmaceuticals, LLC announced that its investigational therapy PP-007 (PEGylated carboxyhemoglobin, bovine) was granted FDA Fast Track designation for the treatment of acute ischemic stroke, designed to improve tissue oxygenation and outcomes following stroke onset

- In September 2024, Simcere Pharmaceutical Co. Ltd. announced that Sanbexin Sublingual Tablets (edaravone and dexborneol) received FDA Breakthrough Therapy designation for the treatment of acute ischemic stroke, recognizing its potential to improve clinical outcomes compared with existing therapies

- In March 2025, Genentech received U.S. FDA approval for TNKase (tenecteplase) as a thrombolytic agent for adults with acute ischemic stroke, marking the first new FDA-approved stroke thrombolytic in decades and offering a rapid single-bolus administration option for clot dissolution

- In May 2025, results from the ASSET-IT randomized trial showed that adding intravenous tirofiban to standard systemic thrombolysis significantly improved functional outcomes in patients treated within 4.5 hours of acute ischemic stroke onset, advancing evidence for adjunctive treatment strategies

- In July 2025, pharmaceutical and biotech innovators such as Pharmazz Inc. enrolled the first patient in a Phase III trial of sovateltide, a novel endothelin-B receptor agonist aimed at improving functional recovery following acute ischemic stroke, signaling continued R&D momentum

- In July 2025, Revalesio received FDA Fast Track designation for RNS60, an oxygen-supersaturated saline therapy under evaluation for its mitochondrial supportive and anti-inflammatory effects in ischemic stroke, underscoring diversified therapeutic approaches beyond traditional thrombolysis

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.