Global Knee Arthroplasty Market

Market Size in USD Billion

CAGR :

%

USD

11.02 Billion

USD

17.56 Billion

2025

2033

USD

11.02 Billion

USD

17.56 Billion

2025

2033

| 2026 - 2033 | |

| USD 11.02 Billion | |

| USD 17.56 Billion | |

| % | |

|

Knee Arthroplasty Market Overview

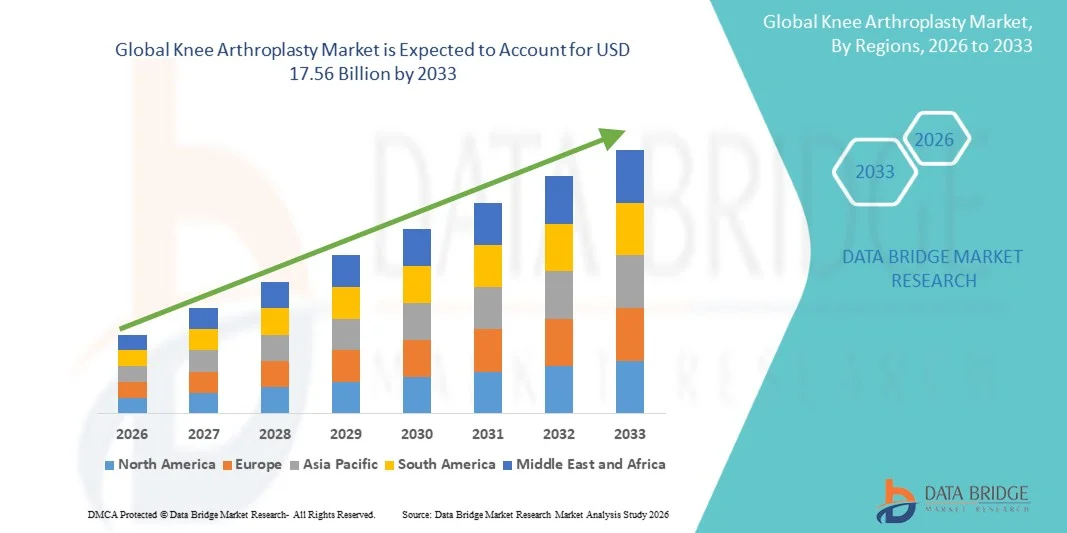

The Knee Arthroplasty Market was valued at USD 11.02 billion in 2025 and is projected to reach USD 17.56 billion by 2033, growing at a CAGR of 6.00% from 2026 to 2033. The Knee Arthroplasty Market is experiencing steady growth driven by the rising prevalence of osteoarthritis, rheumatoid arthritis, obesity-related joint disorders, and an aging population worldwide. Increasing demand for effective solutions to restore mobility, reduce chronic knee pain, and improve quality of life is accelerating the adoption of knee replacement procedures across both developed and emerging healthcare markets.

The growing burden of degenerative joint diseases, combined with advancements in implant materials, robotic-assisted surgical systems, computer-assisted navigation technologies, and minimally invasive surgical techniques, is encouraging hospitals and orthopedic centers to perform a greater number of knee arthroplasty procedures. Modern knee replacement systems offer improved implant longevity, enhanced surgical precision, faster recovery times, and better functional outcomes compared to conventional approaches. Furthermore, rising healthcare expenditure, expanding access to orthopedic care, increasing awareness regarding joint replacement benefits, and favorable reimbursement policies in several countries are supporting market expansion. The continued development of personalized implants, smart surgical technologies, and outpatient joint replacement programs is further strengthening growth prospects for the Knee Arthroplasty Market.

Key Market Trends & Insights

- North America dominated the Knee Arthroplasty Market with the largest revenue share of 39.12% in 2025, supported by a high volume of knee replacement procedures, advanced orthopedic healthcare infrastructure, strong adoption of robotic-assisted surgical technologies, favorable reimbursement policies, and the presence of leading implant manufacturers. The region also benefits from a growing elderly population, rising prevalence of osteoarthritis, and increasing demand for minimally invasive joint replacement procedures.

- The Metal-On-Plastic segment dominated the market with a 78.64% share in 2025 owing to its excellent clinical performance, affordability, and extensive long-term evidence supporting safety and durability.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.7% from 2026 to 2033, fueled by rapidly aging populations, rising healthcare expenditure, increasing orthopedic surgery volumes, expanding healthcare infrastructure, and growing adoption of advanced knee replacement technologies across China, India, Japan, and South Korea.

- The Revision Knee Replacement Systems segment is projected to register the fastest CAGR of 8.9% from 2026 to 2033, reflecting the growing number of revision procedures associated with implant wear, loosening, infection, and the increasing population of patients who previously underwent knee replacement surgery.

- The Three-Compartmental Knee Implants segment dominated the device type category with a 63.48% revenue share in 2025, owing to its widespread use in total knee arthroplasty procedures, comprehensive joint restoration capabilities, and strong clinical outcomes in patients with advanced degenerative knee disease.

- Cemented fixation accounted for 72.56% of the market in 2025, preferred by orthopedic surgeons due to its proven long-term clinical performance, immediate implant stability, extensive procedural experience, and suitability for elderly patients with reduced bone quality.

- The Technology-Assisted Surgery segment is the fastest-growing surgery type category, with a CAGR of 9.4%, driven by increasing adoption of robotic-assisted surgery, computer navigation systems, artificial intelligence-based surgical planning, and patient-specific instrumentation that improve surgical precision and postoperative outcomes.

- The Metal-on-Plastic segment dominated the material category with a 69.25% revenue share in 2025, supported by its long-established clinical success, cost-effectiveness, durability, and widespread acceptance across both developed and emerging healthcare markets.

- Highly Cross-Linked Polyethylene Inserts are projected to be the fastest-growing polyethylene insert category at a CAGR of 8.8%, driven by superior wear resistance, improved implant longevity, reduced revision risk, and increasing adoption in younger and more active patient populations.

- Hospitals dominated the end-use segment with a 78.34% share in 2025, owing to their advanced surgical infrastructure, availability of specialized orthopedic surgeons, access to robotic-assisted surgical platforms, and ability to manage complex primary and revision knee arthroplasty procedures.

Market Size & Forecast

- Global Market Value (2025): USD 11.02 Billion

- Expected Market Value (2033): USD 17.56 Billion

- Forecast CAGR (2026–2033): 6.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Knee Arthroplasty Market Segmentation

|

Attributes |

Knee Arthroplasty Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Zimmer Biomet Holdings, Inc. (U.S.) |

|

Market Opportunities |

· Growing Adoption of Robotic-Assisted and Navigation-Guided Knee Replacement Procedures · Expansion of Knee Replacement Procedures in Emerging Markets · Development of Patient-Specific Implants and Advanced Bearing Materials |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Knee Arthroplasty Market Trends

Trend: Increasing Adoption of Robotic-Assisted and Technology-Enabled Knee Replacement Procedures

The Knee Arthroplasty Market is witnessing a strong trend toward robotic-assisted and technology-enabled knee replacement surgeries as healthcare providers increasingly focus on improving implant positioning accuracy, surgical precision, and long-term patient outcomes. Orthopedic surgeons are adopting robotic platforms, computer-assisted navigation systems, and patient-specific instrumentation to optimize knee implant alignment and reduce variability during surgery. For instance, robotic-assisted total knee arthroplasty procedures have grown significantly across North America and Europe, supported by increasing installations of robotic systems such as Mako and VELYS. Clinical studies have demonstrated that robotic-assisted knee replacement can improve implant placement accuracy and reduce soft-tissue damage compared with conventional techniques. In addition, the growing adoption of outpatient joint replacement programs and enhanced recovery protocols is accelerating demand for advanced knee arthroplasty solutions globally.

Knee Arthroplasty Market Dynamics

Key Market Driver: Rising Prevalence of Osteoarthritis and Growing Aging Population

The increasing prevalence of osteoarthritis and age-related joint disorders is a major driver of the Knee Arthroplasty Market. According to the World Health Organization (WHO), more than 528 million people worldwide were living with osteoarthritis in recent years, with knee osteoarthritis representing one of the most common causes of disability among older adults. The growing geriatric population, rising obesity rates, sedentary lifestyles, and increasing incidence of sports-related injuries are contributing to higher demand for knee replacement procedures. According to the Organisation for Economic Co-operation and Development (OECD), several developed countries perform hundreds of knee replacement procedures per 100,000 population annually. In addition, growing awareness regarding the benefits of joint replacement surgery, improvements in implant durability, and increasing access to orthopedic care are supporting market expansion. The continued shift toward minimally invasive surgical techniques and faster recovery pathways is further driving adoption of knee arthroplasty procedures worldwide.

Key Restraint/Challenge: High Procedure Costs and Risk of Revision Surgeries

A significant challenge in the Knee Arthroplasty Market is the high cost associated with knee replacement procedures and advanced implant technologies. Total knee replacement surgery involves substantial expenses related to implants, surgical equipment, hospital stays, rehabilitation services, and postoperative care. Advanced robotic-assisted systems and premium implant materials further increase procedural costs, limiting accessibility in price-sensitive healthcare markets. In addition, implant wear, infection, aseptic loosening, and implant failure can lead to revision surgeries, which are often more complex and costly than primary procedures. According to orthopedic registry data from several countries, revision knee replacement procedures continue to represent a considerable clinical and economic burden on healthcare systems. Furthermore, reimbursement limitations and disparities in access to specialized orthopedic services in developing regions may hinder broader market adoption.

Key Market Opportunity: Expansion of Robotic Surgery, Smart Implants, and Emerging Healthcare Markets

The rapid expansion of robotic-assisted orthopedic surgery and next-generation implant technologies presents a significant growth opportunity for the knee arthroplasty market. Advanced robotic systems are enabling surgeons to perform highly personalized procedures with improved precision and reproducibility. For instance, manufacturers including Zimmer Biomet, Stryker, and Johnson & Johnson MedTech continue to expand robotic surgery platforms and digital orthopedic ecosystems globally. The development of smart implants featuring sensor-based monitoring capabilities is also creating opportunities for real-time postoperative assessment and personalized patient management. In addition, emerging economies such as China, India, Brazil, and Southeast Asian countries are investing heavily in orthopedic infrastructure and joint replacement programs to address growing musculoskeletal disease burdens. Rising healthcare expenditure, expanding private hospital networks, increasing medical tourism, and improved access to advanced orthopedic technologies are expected to create substantial growth opportunities for knee arthroplasty manufacturers throughout the forecast period.

Knee Arthroplasty Market Scope

The Knee Arthroplasty market is segmented on the basis of product, device type, component, implant type, design, surgery type, fixation material, material, polyethylene inserts, and end use.

- By Product

On the basis of product, the Knee Arthroplasty Market is segmented into Primary Knee Replacement Systems, Revision Knee Replacement Systems, and Partial Knee Replacement Systems. The Primary Knee Replacement Systems segment dominated the market with a 61.42% share in 2025 due to the large volume of first-time knee replacement procedures performed worldwide for the treatment of advanced osteoarthritis, rheumatoid arthritis, and degenerative joint diseases. The increasing aging population, rising obesity prevalence, and growing incidence of musculoskeletal disorders continue to drive demand for primary knee replacement procedures. These systems are widely adopted due to their proven clinical outcomes, long implant lifespan, and broad availability across healthcare facilities. Technological advancements in implant materials, patient-specific instrumentation, and robotic-assisted surgery are further improving surgical precision and patient satisfaction. Growing awareness regarding early intervention and increasing healthcare expenditure also support segment growth. Hospitals and orthopedic centers continue to prioritize primary knee replacement procedures owing to favorable reimbursement policies and established surgical protocols. As a result, the segment maintains its leading position across the global market.

The Revision Knee Replacement Systems segment is expected to witness the fastest CAGR of 7.8% from 2026 to 2033. Growth is driven by the increasing number of aging knee implants requiring replacement due to wear, loosening, infection, instability, or implant failure. Rising life expectancy and growing volumes of primary knee arthroplasty procedures are creating a larger pool of patients likely to require revision surgeries in the future. Technological advancements in revision implant designs, fixation techniques, and bone reconstruction systems are improving clinical outcomes. Increasing surgeon expertise and the adoption of robotic-assisted revision procedures are further supporting growth. Healthcare providers are investing in specialized revision surgery programs to address growing patient demand. Additionally, increasing awareness regarding revision treatment options and improvements in healthcare accessibility are expected to accelerate adoption globally.

- By Device Type

On the basis of device type, the Knee Arthroplasty Market is segmented into Three-Compartmental Knee Implants, Bi-Compartmental Knee Implants, and Uni-Compartmental Knee Implants. The Three-Compartmental Knee Implants segment dominated the market with a 67.35% share in 2025 due to its widespread use in total knee replacement procedures involving advanced degeneration across the entire knee joint. These implants provide comprehensive restoration of knee function and long-term pain relief for patients with severe osteoarthritis. Their extensive clinical validation, high success rates, and broad surgeon familiarity contribute to strong adoption worldwide. Increasing demand for total knee arthroplasty among elderly patients continues to support market dominance. Advancements in implant design, wear-resistant materials, and surgical technologies further strengthen growth. The segment also benefits from favorable reimbursement structures and growing procedural volumes globally.

The Uni-Compartmental Knee Implants segment is projected to register the fastest CAGR of 7.4% from 2026 to 2033. Growth is driven by increasing preference for minimally invasive surgical approaches and bone-preserving procedures. These implants offer faster recovery, shorter hospital stays, and improved postoperative mobility compared to total knee replacement. Rising awareness among patients and surgeons regarding the benefits of partial knee replacement is accelerating adoption. Technological innovations and improved patient selection techniques are further enhancing clinical outcomes and supporting segment expansion.

- By Component

On the basis of component, the Knee Arthroplasty Market is segmented into Femoral, Tibial, and Patellar components. The Femoral Component segment dominated the market with a 43.87% share in 2025 owing to its critical role in restoring knee articulation, stability, and mobility during knee replacement procedures. The component experiences significant biomechanical loading, making high-performance implant materials and advanced engineering essential. Increasing demand for durable and anatomically optimized femoral implants is driving adoption. Manufacturers continue to introduce innovative designs aimed at improving range of motion and reducing implant wear. Rising knee replacement procedure volumes globally further contribute to segment growth. Strong technological innovation and broad product availability reinforce market leadership.

The Patellar Component segment is anticipated to witness the fastest CAGR of 7.1% from 2026 to 2033. Growing focus on improving postoperative knee function, reducing anterior knee pain, and enhancing patient satisfaction is supporting adoption. Advances in polyethylene technology and implant design are improving durability and long-term performance. Increasing surgeon emphasis on optimized patellofemoral mechanics is expected to further drive growth.

- By Implant Type

On the basis of implant type, the Knee Arthroplasty Market is segmented into Fixed-Bearing Implants, Mobile-Bearing Implants, and Medial Pivot Implants. The Fixed-Bearing Implants segment dominated the market with a 64.28% share in 2025 due to their extensive clinical history, cost-effectiveness, and proven long-term performance. These implants remain the standard choice for most knee replacement procedures globally. Their simple design, broad availability, and suitability for a wide patient population support widespread adoption. Hospitals and surgeons continue to prefer fixed-bearing implants because of their reliability and lower complication rates. Ongoing improvements in implant materials and design continue to enhance clinical outcomes. In addition, strong reimbursement support and widespread availability across developed and emerging healthcare markets contribute to segment dominance. The growing number of total knee replacement procedures among aging populations further supports demand. Established clinical guidelines and extensive surgeon familiarity continue to reinforce adoption worldwide.

The Medial Pivot Implants segment is projected to register the fastest CAGR of 8.0% from 2026 to 2033. Growth is driven by increasing demand for implants that better replicate natural knee kinematics and improve patient satisfaction. Clinical evidence demonstrating enhanced stability and functional outcomes is accelerating adoption. Technological advancements and growing surgeon familiarity are further supporting market expansion. Increasing focus on patient-reported outcome measures is encouraging healthcare providers to adopt advanced implant technologies. Rising awareness regarding long-term functional benefits and reduced instability is also contributing to growth. Furthermore, expanding product launches and innovation in implant design are expected to accelerate market penetration during the forecast period.

- By Design

On the basis of design, the Knee Arthroplasty Market is segmented into Cruciate Retaining and Posterior Stabilized Design. The Posterior Stabilized Design segment dominated the market with a 57.93% share in 2025 due to its ability to provide enhanced stability and predictable knee mechanics following surgery. These implants are widely utilized in patients with compromised posterior cruciate ligaments and advanced joint degeneration. Strong clinical outcomes, extensive surgeon experience, and broad applicability continue to support segment leadership. Increasing adoption of advanced implant technologies further contributes to growth. The design offers reliable postoperative motion and functional improvement, making it a preferred option in complex cases. Rising procedural volumes among elderly patients with severe osteoarthritis further support segment growth. Continuous advancements in implant engineering are enhancing durability and surgical outcomes.

The Cruciate Retaining Design segment is expected to witness the fastest CAGR of 7.2% from 2026 to 2033. Rising preference for preserving natural knee anatomy and improving proprioception is driving demand. Growing evidence supporting improved functional outcomes and patient satisfaction is accelerating adoption among orthopedic surgeons worldwide. Patients seeking more natural knee movement after surgery are increasingly opting for cruciate-retaining implants. Technological improvements in implant design and surgical techniques are improving procedural success rates. In addition, increasing surgeon confidence and favorable long-term clinical data are expected to strengthen segment expansion.

- By Surgery Type

On the basis of surgery type, the Knee Arthroplasty Market is segmented into Traditional Surgery Type and Technology Assisted Surgery Type. The Traditional Surgery Type segment dominated the market with a 71.24% share in 2025 owing to its extensive adoption across hospitals and orthopedic centers globally. Lower procedural costs, widespread surgeon expertise, and established clinical workflows continue to support market leadership. The availability of conventional surgical instruments and broad reimbursement coverage further strengthen adoption. Traditional surgical approaches remain highly accessible across both developed and developing healthcare systems. High procedural familiarity among orthopedic surgeons contributes to consistent clinical outcomes. In addition, lower capital investment requirements compared with advanced robotic platforms support continued utilization.

The Technology Assisted Surgery Type segment is expected to register the fastest CAGR of 9.1% from 2026 to 2033. Growth is driven by increasing adoption of robotic-assisted surgery, computer navigation systems, and AI-enabled surgical planning technologies. Improved implant alignment, enhanced precision, and superior patient outcomes are accelerating demand for technology-assisted knee replacement procedures worldwide. Hospitals are increasingly investing in robotic systems to improve surgical efficiency and reduce revision rates. Growing evidence supporting better postoperative outcomes and shorter recovery periods is further driving adoption. Continuous technological innovation and expanding surgeon training programs are expected to support long-term market growth.

- By Fixation Material

On the basis of fixation material, the Knee Arthroplasty Market is segmented into Cemented, Cementless, and Hybrid. The Cemented segment dominated the market with a 69.48% share in 2025 due to its long-standing clinical success, immediate implant fixation, and broad applicability across patient populations. Cemented implants continue to be widely utilized due to predictable outcomes and strong surgeon familiarity. Their ability to provide stable fixation in elderly patients with lower bone quality further supports widespread adoption. Extensive long-term clinical evidence demonstrating durability and effectiveness reinforces physician confidence. In addition, broad availability and cost-effectiveness continue to strengthen segment leadership globally.

The Cementless segment is projected to witness the fastest CAGR of 8.3% from 2026 to 2033. Growing demand for biologic fixation, improved implant longevity, and advancements in porous implant surfaces are supporting adoption. Increasing utilization among younger and more active patients is further driving growth. Enhanced osseointegration capabilities and advancements in implant coating technologies are improving clinical outcomes. Surgeons are increasingly recommending cementless options for patients seeking longer implant lifespan. Rising innovation and growing acceptance of next-generation implant materials are expected to accelerate market expansion.

- By Material

On the basis of material, the Knee Arthroplasty Market is segmented into Metal-On-Plastic, Ceramic-On-Plastic, Ceramic-On-Ceramic, and Metal-On-Metal. The Metal-On-Plastic segment dominated the market with a 78.64% share in 2025 owing to its excellent clinical performance, affordability, and extensive long-term evidence supporting safety and durability. The material combination remains the industry standard for most knee replacement procedures globally. Its favorable balance between wear resistance, mechanical strength, and cost-effectiveness continues to support strong adoption. Extensive surgeon experience and broad regulatory approvals further reinforce market dominance. Increasing global procedure volumes are also contributing to sustained demand.

The Ceramic-On-Plastic segment is anticipated to register the fastest CAGR of 7.5% from 2026 to 2033. Growing demand for wear-resistant materials and improved implant longevity is accelerating adoption. Advancements in ceramic technologies and increasing surgeon confidence continue to support market expansion. Ceramic components help reduce wear particle generation and improve long-term implant performance. Rising patient demand for durable and high-performance implants is further encouraging adoption. In addition, ongoing product development and favorable clinical outcomes are supporting segment growth worldwide.

- By Polyethylene Inserts

On the basis of polyethylene inserts, the Knee Arthroplasty Market is segmented into Conventional Polyethylene Inserts, Highly Cross-Linked Polyethylene Inserts, and Antioxidant Polyethylene Inserts. The Highly Cross-Linked Polyethylene Inserts segment dominated the market with a 46.82% share in 2025 due to superior wear resistance and enhanced implant longevity. Increasing utilization in primary and revision knee arthroplasty procedures is driving growth. These inserts significantly reduce wear-related complications and improve long-term implant survivorship. Growing clinical evidence supporting superior performance compared with conventional alternatives is accelerating adoption. In addition, increasing use in younger patient populations is contributing to market expansion.

The Antioxidant Polyethylene Inserts segment is expected to witness the fastest CAGR of 8.4% from 2026 to 2033. Rising demand for advanced biomaterials capable of reducing oxidative degradation and extending implant lifespan is supporting adoption. Ongoing research and product innovation continue to strengthen growth prospects. Antioxidant technologies help maintain material integrity and reduce long-term wear-related failures. Increasing investment in biomaterial research and development is accelerating commercialization. Furthermore, growing physician awareness regarding enhanced implant durability is expected to drive future demand.

- By End Use

On the basis of end use, the Knee Arthroplasty Market is segmented into Hospitals and Ambulatory Surgical Centers. The Hospitals segment dominated the market with a 74.56% share in 2025 due to the high volume of knee replacement procedures performed in hospital settings, availability of advanced surgical infrastructure, and access to specialized orthopedic surgeons. Hospitals also offer comprehensive postoperative rehabilitation and management services, supporting their dominant position. The availability of robotic-assisted surgical systems and multidisciplinary care teams further enhances treatment outcomes. Large patient inflow and strong reimbursement frameworks continue to support procedural volumes. In addition, hospitals remain the preferred setting for complex and revision knee replacement surgeries.

The Ambulatory Surgical Centers segment is projected to register the fastest CAGR of 8.6% from 2026 to 2033. Growth is driven by increasing preference for outpatient joint replacement procedures, lower treatment costs, shorter recovery times, and advancements in minimally invasive surgical techniques. Expanding healthcare infrastructure and favorable reimbursement trends are further accelerating adoption of knee arthroplasty procedures in ambulatory settings. Improved perioperative care protocols and enhanced patient selection criteria are supporting procedural safety. Rising healthcare cost-containment efforts are encouraging a shift toward outpatient surgical settings. Furthermore, increasing investment in specialized orthopedic ambulatory centers is expected to boost segment growth during the forecast period.

Knee Arthroplasty Market Regional Analysis

North America dominated the Knee Arthroplasty Market and accounted for the largest revenue share of 39.12% in 2025, supported by a high volume of knee replacement procedures, advanced orthopedic healthcare infrastructure, strong adoption of robotic-assisted surgical technologies, favorable reimbursement policies, and the presence of leading implant manufacturers. The region also benefits from a rapidly aging population and increasing prevalence of osteoarthritis, which remains one of the primary causes of knee joint degeneration. Growing awareness regarding the benefits of early surgical intervention, coupled with continuous advancements in implant materials and surgical techniques, is further supporting market expansion. Increasing demand for minimally invasive procedures and personalized orthopedic solutions continues to strengthen North America's leadership position in the global market.

U.S. Knee Arthroplasty Market Insight

The U.S. Knee Arthroplasty market is witnessing strong growth due to the increasing burden of osteoarthritis, rising obesity rates, and growing demand for joint replacement procedures among elderly patients. The country has one of the highest volumes of knee replacement surgeries globally, supported by advanced hospital infrastructure and strong reimbursement coverage. In addition, increasing adoption of robotic-assisted knee replacement systems, computer-assisted navigation technologies, and patient-specific implants is improving surgical precision and patient outcomes. Continuous investments in orthopedic innovation and expanding access to outpatient joint replacement procedures are further accelerating market growth across the United States.

Europe Knee Arthroplasty Market Insight

The Europe Knee Arthroplasty market remains a major contributor to global revenue, driven by increasing prevalence of degenerative joint disorders, favorable healthcare systems, and strong adoption of advanced orthopedic technologies. The region benefits from a well-established network of hospitals and specialized orthopedic centers performing high volumes of knee replacement procedures. Growing awareness regarding the benefits of early intervention, coupled with rising healthcare expenditure, continues to support market expansion. Furthermore, increasing adoption of cementless implants, robotic-assisted surgery, and enhanced recovery protocols is contributing to improved patient outcomes and market growth throughout Europe.

U.K. Knee Arthroplasty Market Insight

The U.K. Knee Arthroplasty market is experiencing steady growth, supported by a rising elderly population, increasing incidence of osteoarthritis, and growing demand for advanced orthopedic care. The country continues to invest in improving access to joint replacement procedures through both public and private healthcare systems. Increasing adoption of minimally invasive surgical techniques, robotic-assisted procedures, and advanced implant technologies is contributing to better clinical outcomes and shorter recovery times. In addition, ongoing efforts to reduce waiting times for orthopedic surgeries are expected to support future market growth in the United Kingdom.

Germany Knee Arthroplasty Market Insight

The Germany Knee Arthroplasty market is expanding steadily due to the country’s advanced healthcare infrastructure, strong orthopedic research capabilities, and high procedural volumes. Germany remains one of the leading European markets for joint replacement procedures, supported by widespread adoption of innovative implant technologies and robotic-assisted surgery systems. Increasing investments in orthopedic healthcare services and growing demand for high-performance knee implants are driving market expansion. Moreover, favorable reimbursement policies and a strong focus on improving patient outcomes continue to support the adoption of advanced knee arthroplasty solutions across the country.

Asia-Pacific Knee Arthroplasty Market Insight

The Asia-Pacific Knee Arthroplasty market is expected to witness rapid growth and is projected to register the fastest CAGR of 8.7% from 2026 to 2033. Growth is driven by rapidly aging populations, rising healthcare expenditure, increasing orthopedic surgery volumes, expanding healthcare infrastructure, and growing adoption of advanced knee replacement technologies across China, India, Japan, and South Korea. Increasing awareness regarding the benefits of joint replacement surgery and improving access to specialized orthopedic care are further supporting market expansion. In addition, government initiatives to strengthen healthcare systems and growing investments by private healthcare providers are accelerating regional market growth.

Japan Knee Arthroplasty Market Insight

The Japan Knee Arthroplasty market is witnessing consistent growth due to the country's rapidly aging population and increasing prevalence of osteoarthritis-related knee disorders. Rising demand for mobility restoration and improved quality of life among elderly patients is driving procedural volumes. Japanese healthcare providers are increasingly adopting advanced implant technologies, robotic-assisted surgical systems, and minimally invasive techniques to improve treatment outcomes. Furthermore, strong healthcare infrastructure and continued investments in orthopedic innovation are supporting sustained market growth across the country.

China Knee Arthroplasty Market Insight

The China Knee Arthroplasty market is growing rapidly, driven by a large aging population, increasing healthcare spending, and expanding access to orthopedic surgical services. Rising prevalence of osteoarthritis, obesity, and age-related joint disorders is creating substantial demand for knee replacement procedures. The growing adoption of advanced implant systems, robotic-assisted surgery platforms, and modern hospital infrastructure is significantly boosting market growth. In addition, supportive government healthcare reforms, increasing patient awareness, and rising investments in orthopedic care are positioning China as one of the fastest-growing markets for knee arthroplasty globally.

Knee Arthroplasty Market Share

The Knee Arthroplasty industry is primarily led by well-established companies, including:

- Zimmer Biomet Holdings, Inc. (U.S.)

- Stryker Corporation (U.S.)

- Johnson & Johnson MedTech (DePuy Synthes) (U.S.)

- Smith+Nephew plc (U.K.)

- B. Braun Melsungen AG (Germany)

- Exactech, Inc. (U.S.)

- MicroPort Scientific Corporation (China)

- Corin Group (U.K.)

- Medacta International SA (Switzerland)

- Enovis Corporation (DJO Surgical) (U.S.)

- LimaCorporate S.p.A. (Italy)

- Meril Life Sciences Pvt. Ltd. (India)

- United Orthopedic Corporation (Taiwan)

- Aesculap Implant Systems, LLC (Germany/U.S.)

- Peter Brehm GmbH (Germany)

- Waldemar Link GmbH & Co. KG (Germany)

- Beijing Chunlizhengda Medical Instruments Co., Ltd. (China)

- AK Medical Holdings Limited (China)

- Kinamed Incorporated (U.S.)

- Mathys AG Bettlach (Switzerland)

- Amplitude Surgical SA (France)

- Orthofix Medical Inc. (U.S.)

- Conformis, Inc. (U.S.)

- Elite Surgical Pvt. Ltd. (India)

- Evolutis India Pvt. Ltd. (India)

- Shalby Advanced Technologies Inc. (U.S./India)

- Baumer S.A. (Brazil)

- SurgTech Inc. (South Korea)

- KYOCERA Corporation (Japan)

- Japan Medical Dynamic Marketing, Inc. (Japan)

- OMNIlife Science, Inc. (U.S.)

- Response Ortho LLC (U.S.)

- Adler Ortho S.p.A. (Italy)

- Corentec Co., Ltd. (South Korea)

- Beijing AKEC Medical Co., Ltd. (China)

Latest Developments in Global Knee Arthroplasty Market

- In November 2024, Zimmer Biomet Holdings, Inc. announced that it received U.S. FDA Premarket Approval (PMA) for the Oxford Cementless Partial Knee, making it the first and only FDA-approved cementless partial knee replacement implant in the United States. The implant is designed to promote natural bone ingrowth for long-term fixation and improve surgical efficiency compared with cemented partial knee procedures. The approval was supported by clinical and non-clinical data and represents a significant advancement in cementless knee arthroplasty technology

- In August 2024, Zimmer Biomet expanded its technology-assisted knee arthroplasty portfolio through a limited distribution agreement with THINK Surgical for the TMINI® miniature robotic system for total knee arthroplasty. The collaboration complements Zimmer Biomet’s ROSA® Knee robotic platform and reflects the growing adoption of robotic-assisted technologies aimed at improving implant positioning accuracy, surgical workflow efficiency, and patient outcomes in knee replacement procedures

- In August 2023, Exactech announced U.S. FDA 510(k) clearance for Activit-E™ polyethylene for its Truliant Knee Replacement System. The next-generation polyethylene incorporates vitamin E antioxidant technology and advanced crosslinking methods designed to improve wear resistance, durability, and implant longevity. The development highlights the industry's focus on advanced biomaterials to enhance long-term clinical performance in knee arthroplasty

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.