Global Lymphedema Diagnostics Market

Market Size in USD Billion

CAGR :

%

USD

46.59 Billion

USD

83.71 Billion

2025

2033

USD

46.59 Billion

USD

83.71 Billion

2025

2033

| 2026 –2033 | |

| USD 46.59 Billion | |

| USD 83.71 Billion | |

| % | |

|

Lymphedema Diagnostics Market Size

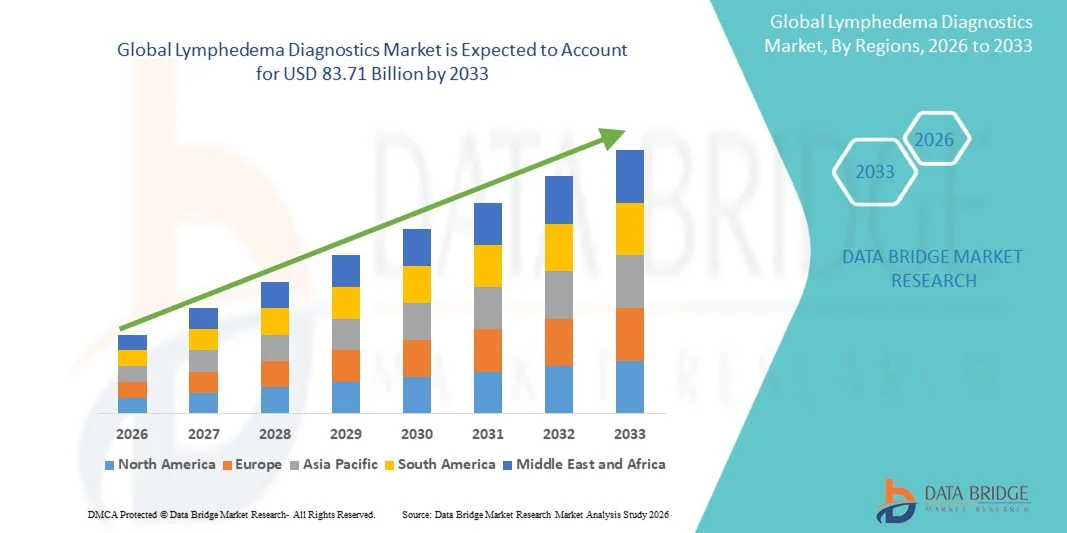

- The global lymphedema diagnostics market size was valued at USD 46.59 billion in 2025 and is expected to reach USD 83.71 billion by 2033, at a CAGR of 7.60% during the forecast period

- The market growth is largely fueled by the increasing prevalence of lymphedema caused by cancer treatments, obesity, and chronic diseases, driving the need for accurate and early diagnostic solutions in hospitals and specialized clinics

- Furthermore, rising demand for non-invasive, precise, and timely lymphedema detection tools is establishing lymphedema diagnostics solutions as essential for patient management and treatment planning, thereby significantly boosting the market’s growth

Lymphedema Diagnostics Market Analysis

- Lymphedema diagnostics, which include imaging systems, bioimpedance spectroscopy, and other non-invasive diagnostic tools, are increasingly becoming essential in both clinical and outpatient settings due to the rising prevalence of lymphedema and the need for early and accurate detection to guide treatment and improve patient outcomes

- The escalating demand for lymphedema diagnostics is primarily driven by the growing incidence of cancer-related lymphedema, chronic diseases, and obesity, coupled with increasing awareness among healthcare providers and patients about the importance of timely diagnosis and management

- North America dominated the lymphedema diagnostics market with the largest revenue share of 38.9% in 2025, supported by advanced healthcare infrastructure, high adoption of diagnostic technologies, and the presence of major medical device and diagnostics companies in the U.S., which is witnessing significant growth in lymphedema screening and monitoring solutions

- Asia-Pacific is expected to be the fastest growing region in the lymphedema diagnostics market during the forecast period, owing to rising healthcare awareness, increasing investments in medical infrastructure, and growing demand for early detection and management of lymphedema in countries such as China, India, and Japan

- The secondary lymphedema segment dominated the largest market revenue share of 61.4% in 2025, driven by its higher prevalence, particularly among patients undergoing cancer treatments such as breast, pelvic, and gynecological surgeries

Report Scope and Lymphedema Diagnostics Market Segmentation

|

Attributes |

Lymphedema Diagnostics Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• F. Hoffmann-La Roche Ltd. (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Lymphedema Diagnostics Market Trends

“Enhanced Convenience Through Advanced Diagnostic Technologies”

- A significant and accelerating trend in the global Lymphedema Diagnostics market is the integration of advanced diagnostic technologies, including imaging systems, bioimpedance spectroscopy, and wearable monitoring devices. This convergence of technologies is enhancing early detection, patient monitoring, and treatment management for lymphedema

- For instance, devices such as the L-Dex U400 bioimpedance spectroscopy system allow clinicians to monitor lymphatic fluid levels non-invasively, providing accurate and real-time assessment of lymphedema progression. Similarly, imaging solutions like near-infrared fluorescence (NIRF) imaging are being adopted in specialized clinics to guide precise diagnosis and treatment

- The increasing incorporation of wearable and sensor-based monitoring systems allows continuous tracking of limb volume and fluid accumulation, enabling clinicians to provide personalized interventions. These technologies also facilitate patient compliance by offering real-time feedback on therapy effectiveness

- The seamless integration of these diagnostic tools with electronic health record (EHR) systems and telemedicine platforms allows centralized patient monitoring and remote consultation. Clinicians can now manage multiple patients efficiently while maintaining accurate records of disease progression and therapy outcomes

- This trend towards more intelligent, precise, and patient-centric diagnostic systems is fundamentally reshaping expectations for lymphedema care. Consequently, companies such as ImpediMed and BSN Medical are developing advanced diagnostic solutions with improved accuracy, ease of use, and integration into clinical workflows

- The demand for advanced lymphedema diagnostics is growing rapidly across hospitals, outpatient clinics, and rehabilitation centers, as healthcare providers increasingly prioritize early detection, preventive care, and effective therapy management

Lymphedema Diagnostics Market Dynamics

Driver

“Rising Incidence of Lymphedema and Growing Awareness”

- The increasing prevalence of lymphedema, driven by cancer therapies, obesity, and aging populations, is a major driver for the growing demand for diagnostic solutions

- For instance, in March 2025, ImpediMed launched an upgraded bioimpedance spectroscopy system with enhanced sensitivity for early-stage lymphedema detection. Such innovations by leading companies are expected to boost market adoption in clinical settings

- Healthcare providers are becoming more aware of the importance of early diagnosis, which can significantly reduce complications, improve patient outcomes, and lower long-term treatment costs

- The growing trend of patient-centric care and preventive healthcare is pushing hospitals and rehabilitation centers to invest in accurate, rapid, and non-invasive diagnostic solutions

- The increasing adoption of lymphedema diagnostics in post-surgical care and cancer rehabilitation programs is further driving market growth, particularly in developed regions with advanced healthcare infrastructure

- Expanding research and clinical trials are generating robust evidence supporting the efficacy of early detection and continuous monitoring, motivating more healthcare institutions to implement advanced lymphedema diagnostic protocols

- Rising patient awareness and advocacy programs are encouraging proactive healthcare-seeking behavior, ensuring that individuals at risk for lymphedema seek timely evaluation and monitoring

- Integration of portable and home-based monitoring systems is allowing patients to track progress outside clinical settings, enhancing patient engagement and adherence to treatment regimens

Restraint/Challenge

“High Costs, Limited Awareness, and Infrastructure Barriers”

- High initial costs of advanced lymphedema diagnostic systems, including bioimpedance devices and imaging solutions, can limit adoption among smaller clinics and budget-conscious healthcare providers

- For instance, premium imaging systems such as NIRF devices require significant investment in both equipment and training, which can be a barrier in resource-limited settings

- Limited awareness about lymphedema and its early diagnosis among patients and healthcare practitioners in developing regions may slow market penetration

- Regulatory approvals and the need for clinician training also pose challenges, as integrating advanced diagnostics into routine clinical workflows requires time and resources

- Inadequate healthcare infrastructure in rural and underserved regions may restrict access to advanced lymphedema diagnostics, creating disparities in patient care and limiting market growth

- Reimbursement challenges and inconsistent insurance coverage for advanced diagnostic procedures can discourage healthcare providers from adopting expensive technologies

- Variability in clinical guidelines across regions may cause delays in the standardization and widespread adoption of advanced diagnostic protocols

- Ensuring affordability, improving clinician education, strengthening healthcare infrastructure, and increasing patient awareness campaigns are critical to overcoming these challenges and driving broader adoption of lymphedema diagnostics globally

Lymphedema Diagnostics Market Scope

The Lymphedema Diagnostics market is segmented on the basis of type, technology, disease type, treatment type, and end user.

• By Type

On the basis of type, the Lymphedema Diagnostics market is segmented into primary and secondary lymphedema. The secondary lymphedema segment dominated the largest market revenue share of 61.4% in 2025, driven by its higher prevalence, particularly among patients undergoing cancer treatments such as breast, pelvic, and gynecological surgeries. Secondary lymphedema often results from lymph node removal, radiation therapy, or trauma, creating a critical need for accurate and timely diagnostics. Hospitals and diagnostic centers widely adopt imaging, bio-impedance, and fluorescence techniques to detect early fluid accumulation and prevent disease progression. Continuous monitoring programs for post-surgical patients also contribute to adoption. Rising awareness among oncologists and patients about the importance of early intervention enhances market demand. Government initiatives supporting post-operative care and rehabilitation further boost usage. The availability of skilled healthcare professionals and well-established treatment protocols reinforces adoption. Ongoing research into lymphatic imaging technologies increases detection efficiency. The segment benefits from both outpatient and hospital-based lymphedema management programs.

The primary lymphedema segment is expected to witness the fastest CAGR of 19.2% from 2026 to 2033, fueled by growing recognition of congenital and hereditary lymphedema cases. Early detection in pediatric and young adult populations improves quality of life and reduces long-term complications. Genetic testing and family screening programs are increasingly adopted. Non-invasive imaging, near-infrared fluorescence, and bio-impedance analysis are driving technological adoption. Increasing healthcare infrastructure and awareness in emerging markets also support growth. Patient education programs and telemedicine integration further facilitate early diagnosis. Technological advances that reduce cost and improve accuracy enhance market expansion. Adoption is particularly growing in specialized clinics and academic research centers. Rising prevalence of rare lymphatic disorders contributes to the segment’s momentum. Clinical guidelines emphasizing early detection reinforce market penetration.

• By Technology

On the basis of technology, the market is segmented into lymphoscintigraphy, MRI, ultrasound imaging, CT, X-ray lymphography, bio-impedance analysis, and near-infrared fluorescence imaging. The lymphoscintigraphy segment dominated the largest market revenue share of 45.7% in 2025, due to its established clinical use and high accuracy in visualizing lymphatic flow and obstruction. Hospitals prefer lymphoscintigraphy for diagnosis and treatment planning, especially for secondary lymphedema. It offers reproducible results, supports post-surgical monitoring, and is integrated into oncology care pathways. The segment benefits from skilled radiologists, established procedural protocols, and reimbursement policies. Continuous improvements in tracer technology increase detection precision. Widespread adoption in both developed and emerging markets supports dominance. Public health programs and hospital-based screening initiatives further boost demand. The technique’s ability to identify early-stage lymphedema and prevent progression strengthens clinical adoption. Its role in therapy planning and monitoring is critical in improving patient outcomes. Lymphoscintigraphy remains the gold standard in lymphedema imaging.

The near-infrared fluorescence imaging segment is expected to witness the fastest CAGR of 20.5% from 2026 to 2033, fueled by its minimally invasive approach and real-time visualization of lymphatic vessels. It enables early detection, surgical planning, and monitoring of therapeutic interventions. Hospitals, diagnostic centers, and research institutes increasingly adopt NIR fluorescence for superior resolution and workflow efficiency. Technological integration with surgical microscopes enhances intraoperative guidance. Increasing research funding and rising awareness about advanced lymphatic imaging drive adoption. Its use in both pediatric and adult populations further expands the market. Portable systems and ease of use in outpatient clinics support broader application. Emerging markets with growing diagnostic infrastructure are adopting NIR imaging rapidly. Training programs and clinical validation studies further reinforce confidence. The segment benefits from combining imaging with lymphatic functional assessment. Increasing demand for precision medicine supports its high growth rate.

• By Disease Type

On the basis of disease type, the market is segmented into cancer, inflammatory diseases, cardiovascular disease, and other diseases. The cancer-related lymphedema segment dominated the largest market revenue share of 58.6% in 2025, driven by the high incidence of post-surgical lymphedema following breast, gynecological, and pelvic cancer treatments. Hospitals rely heavily on imaging and bio-impedance technologies for monitoring and early diagnosis. Early detection prevents complications, reduces hospitalization, and improves patient quality of life. Rising oncologist awareness and post-operative care programs enhance adoption. Technological improvements in imaging resolution and workflow efficiency increase diagnostic accuracy. Government and private healthcare programs supporting cancer patient monitoring also boost market growth. Patient demand for quality post-surgical care further reinforces adoption. The segment benefits from insurance reimbursement in certain regions. Specialized clinics and academic research institutes contribute to diagnostic innovation. Rising cancer prevalence in emerging markets sustains long-term demand. Continuous development of standardized protocols strengthens hospital adoption globally.

The inflammatory disease segment is expected to witness the fastest CAGR of 18.7% from 2026 to 2033, driven by increased recognition of autoimmune and chronic inflammatory conditions affecting the lymphatic system, such as rheumatoid arthritis and chronic infections. Early diagnosis enables prompt management, improving outcomes and reducing secondary complications. Diagnostic centers and hospitals increasingly adopt bio-impedance and imaging techniques for precise detection. Technological improvements, non-invasive methods, and growing research focus on lymphatic inflammation fuel segment growth. Expanding healthcare infrastructure in developing regions supports adoption. Awareness campaigns and early screening programs in chronic inflammatory diseases are boosting market penetration. Rising investments in molecular and functional imaging further strengthen the segment. The segment benefits from integration of AI-based imaging and automated analysis for precise diagnosis. Increasing prevalence of chronic inflammatory diseases globally sustains growth momentum.

• By Treatment Type

On the basis of treatment type, the market is segmented into surgery, compression therapy, and others. The compression therapy segment dominated the largest market revenue share of 49.5% in 2025, driven by its position as the first-line treatment for managing lymphedema. Hospitals and clinics rely on diagnostic tools to tailor compression garments and monitor therapy effectiveness. It is widely adopted due to non-invasiveness, cost-effectiveness, and patient adherence. Increasing availability of advanced compression devices and patient education programs boost market adoption. Insurance coverage for conservative management supports growth. Outpatient and home-based care models further enhance adoption. Technological integration, such as combining compression therapy with bio-impedance monitoring, increases efficiency. Clinical guidelines recommending compression therapy as standard care drive widespread usage. Rising incidence of secondary lymphedema contributes to segment dominance.

The surgical treatment segment is expected to witness the fastest CAGR of 19.0% from 2026 to 2033, fueled by rising adoption of lymphatic microsurgery, lymph node transfer, and debulking procedures. Hospitals and surgical centers increasingly rely on advanced imaging to map lymphatic vessels preoperatively. Technological advancements and minimally invasive surgical techniques enhance patient outcomes and encourage adoption. Awareness campaigns, improved success rates, and growing clinical expertise drive market expansion. Research initiatives and specialized academic centers adopting surgical interventions also support growth. Emerging markets with expanding healthcare infrastructure are adopting surgical treatments more rapidly. Increasing demand for definitive treatment options in refractory lymphedema fuels segment growth. The combination of imaging and surgical planning is critical in high-growth regions.

• By End User

On the basis of end user, the market is segmented into hospitals, diagnostic centers, research and academic institutes, and others. The hospitals segment dominated the largest market revenue share of 53.2% in 2025, driven by high patient volumes, advanced imaging facilities, and the need for timely and accurate diagnosis. Hospitals handle both primary and secondary lymphedema cases, integrating diagnostic results into treatment and rehabilitation plans. Insurance coverage and government programs for cancer and post-surgical patients further strengthen adoption.

The diagnostic centers segment is expected to witness the fastest CAGR of 20.1% from 2026 to 2033, fueled by the growing number of specialized outpatient diagnostic facilities and advanced imaging adoption. These centers offer cost-effective, high-throughput, and non-invasive solutions for early detection and monitoring. Technological advancements, increased healthcare awareness, and the expansion of diagnostic networks globally drive this high growth.

Lymphedema Diagnostics Market Regional Analysis

- North America dominated the lymphedema diagnostics market with the largest revenue share of 38.9% in 2025, supported by advanced healthcare infrastructure, high adoption of diagnostic technologies, and the presence of major medical device and diagnostics companies in the U.S., which is witnessing significant growth in lymphedema screening and monitoring solutions

- The region’s healthcare providers are increasingly emphasizing early detection and preventive management of lymphedema, leveraging advanced bioimpedance spectroscopy, imaging systems, and wearable monitoring solutions to improve patient outcomes

- High levels of healthcare expenditure, strong insurance coverage, and extensive hospital and outpatient clinic networks are further supporting the adoption of lymphedema diagnostics. The growing collaboration between hospitals, rehabilitation centers, and research institutions is driving innovation and the deployment of standardized diagnostic protocols across the region

U.S. Lymphedema Diagnostics Market Insight

The U.S. lymphedema diagnostics market captured the largest revenue share in 2025 within North America, driven by robust investments in advanced diagnostic equipment and widespread adoption of lymphedema monitoring solutions in hospitals, outpatient centers, and rehabilitation clinics. Increasing awareness among clinicians about the benefits of early detection, coupled with ongoing research in post-cancer and chronic condition-related lymphedema, is propelling market growth. Initiatives by medical device companies to provide cost-effective, accurate, and non-invasive diagnostic systems are further contributing to the expansion of this market.

Europe Lymphedema Diagnostics Market Insight

The Europe lymphedema diagnostics market is projected to expand at a substantial CAGR throughout the forecast period, driven by the increasing prevalence of lymphedema, rising demand for advanced diagnostic solutions, and stringent healthcare regulations. The region is witnessing strong adoption of bioimpedance and imaging-based diagnostic techniques, particularly in hospitals and specialized clinics. Increasing urbanization, coupled with enhanced medical infrastructure, is further supporting the market, while patient awareness campaigns and clinical guidelines are promoting early detection and effective management of lymphedema.

U.K. Lymphedema Diagnostics Market Insight

The U.K. lymphedema diagnostics market t is anticipated to grow at a noteworthy CAGR during the forecast period, fueled by the rising need for early detection and preventive care for lymphedema. Healthcare providers and rehabilitation centers are increasingly investing in diagnostic solutions to enhance patient outcomes and reduce long-term treatment costs. Additionally, national health programs and growing patient awareness about the risks associated with lymphedema are supporting market growth.

Germany Lymphedema Diagnostics Market Insight

The Germany lymphedema diagnostics market is expected to expand at a considerable CAGR during the forecast period, driven by strong healthcare infrastructure, advanced medical technology adoption, and a growing emphasis on early disease detection. Hospitals and outpatient clinics are adopting state-of-the-art diagnostic solutions to monitor lymphatic conditions accurately. The region’s focus on innovation and sustainable medical practices, along with skilled healthcare professionals, is further propelling the market.

Asia-Pacific Lymphedema Diagnostics Market Insight

The Asia-Pacific lymphedema diagnostics market is poised to grow at the fastest CAGR during the forecast period, driven by rising healthcare awareness, increasing investments in medical infrastructure, and growing demand for early detection and management of lymphedema in countries such as China, India, and Japan. Expansion of hospitals, specialized clinics, and rehabilitation centers, coupled with government initiatives promoting preventive healthcare, is further supporting market growth. Additionally, the affordability and increasing accessibility of diagnostic technologies are facilitating wider adoption across the region.

Japan Lymphedema Diagnostics Market Insight

The Japan lymphedema diagnostics market is gaining momentum due to the country’s high emphasis on healthcare innovation, rapid urbanization, and the rising need for early detection solutions. The adoption of advanced diagnostic technologies in hospitals and specialized clinics is increasing, supported by government programs for preventive care and rehabilitation. Furthermore, Japan’s aging population is driving demand for accessible, accurate, and non-invasive lymphedema monitoring systems in both residential and clinical settings.

China Lymphedema Diagnostics Market Insight

The China lymphedema diagnostics market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rapid urbanization, growing middle-class healthcare demand, and increased investments in medical infrastructure. Hospitals, diagnostic laboratories, and cancer rehabilitation centers are increasingly deploying advanced diagnostic solutions to support early detection and effective management of lymphedema. Government initiatives promoting preventive healthcare and the rise of private healthcare facilities are also key factors propelling market growth in China.

Lymphedema Diagnostics Market Share

The Lymphedema Diagnostics industry is primarily led by well-established companies, including:

• F. Hoffmann-La Roche Ltd. (Switzerland)

• Thermo Fisher Scientific Inc. (U.S.)

• Siemens Healthineers AG (Germany)

• Medtronic plc (Ireland)

• Hologic, Inc. (U.S.)

• GE Healthcare (U.S.)

• Canon Medical Systems Corporation (Japan)

• Hitachi Medical Corporation (Japan)

• Koninklijke Philips N.V. (Netherlands)

• bioMérieux S.A. (France)

• PerkinElmer, Inc. (U.S.)

• Lonza Group AG (Switzerland)

• Miraca Holdings Inc. (Japan)

• LymphTech Inc. (U.S.)

• KIKKOMAN Biotech Co., Ltd. (Japan)

• OptoMedic Systems Pvt. Ltd. (India)

• Terumo Corporation (Japan)

• Stryker Corporation (U.S.)

• Arjo AB (Sweden)

Latest Developments in Global Lymphedema Diagnostics Market

- In December 2023, the National Heart, Lung, and Blood Institute (NHLBI) launched the first‑ever National Commission on Lymphatic Diseases (NCLD), aimed at advancing research and improving diagnostic methodologies for lymphatic disorders including lymphedema, marking a major regulatory and clinical initiative in the field

- In July 2024, FIJIFILM Healthcare introduced the APERTO Lucent 0.4T open MRI system, featuring RADAR motion‑compensation technology designed to improve imaging quality for lymphatic system assessment and support more accurate lymphedema diagnosis in clinical settings

- In July 2024, a Transparency Market Research report highlighted that the global lymphedema diagnostics market is expanding due to increasing incidence of chronic conditions like lymphedema and adoption of advanced imaging techniques, emphasizing growth in lymphoscintigraphy, MRI, and ultrasound technologies that aid early detection

- In March 2025, Transparency Market Research projected that the global lymphedema diagnostics market will reach USD 70.7 million by 2034, driven by rising cases of lymphedema, technological advancements in imaging modalities, and increased demand for early diagnosis and monitoring tools

- In April 2025, a Scientific Reports publication demonstrated a deep learning‑based classification model for lymphedema and other lower limb edema diseases using clinical images, indicating rapid growth in AI‑driven diagnostic tools aimed at improving early detection accuracy and clinical decision support

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.