Global Maternal Health Market

Market Size in USD Billion

CAGR :

%

USD

19.83 Billion

USD

39.51 Billion

2025

2033

USD

19.83 Billion

USD

39.51 Billion

2025

2033

| 2026 - 2033 | |

| USD 19.83 Billion | |

| USD 39.51 Billion | |

| % | |

|

Maternal Health Market Overview

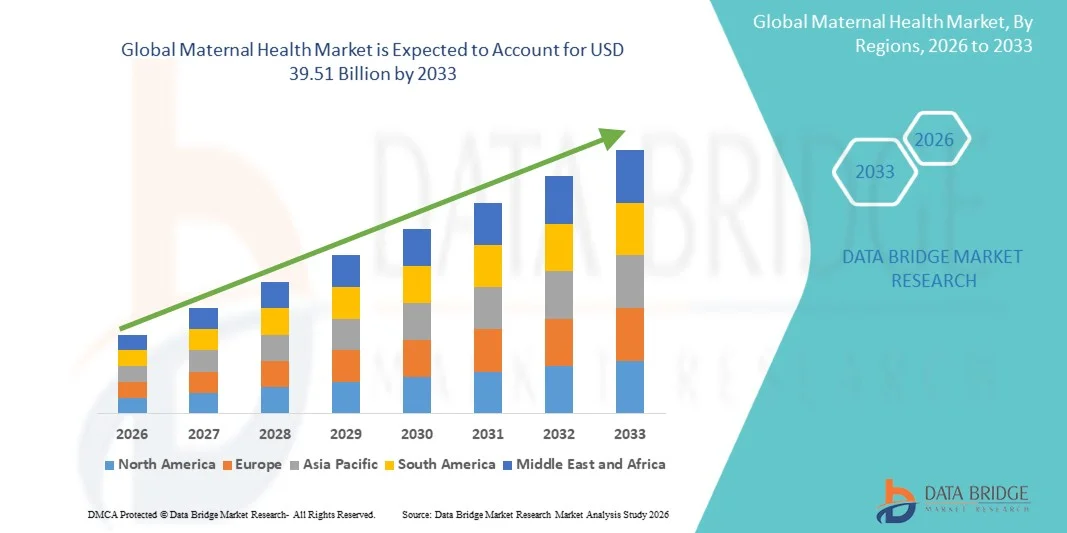

The Maternal Health Market was valued at USD 19.83 billion in 2025 and is projected to reach USD 39.51 billion by 2033, growing at a CAGR of 9.00% from 2026 to 2033. The market is witnessing steady expansion driven by increasing focus on reducing maternal mortality rates, improving access to prenatal and postnatal care, and rising investments in maternal healthcare infrastructure across both developed and emerging economies.

The growing prevalence of pregnancy-related complications, coupled with government and NGO-led initiatives to enhance maternal and child health outcomes, is significantly driving demand for advanced maternal health services and solutions. Expanding use of digital health platforms, telemedicine in obstetric care, and improved screening and diagnostic tools are further supporting early risk detection and better pregnancy management, thereby improving overall maternal health outcomes globally.

Key Market Trends & Insights

- North America dominated the Maternal Health Market with the largest revenue share of 38.46% in 2025, supported by strong maternal care infrastructure, high healthcare spending, and widespread adoption of advanced prenatal monitoring technologies.

- The Hormones segment led the market with a 34.62% share in 2025, driven by widespread use in fertility regulation, pregnancy support therapies, and management of hormonal imbalances during pregnancy

- Asia-Pacific is expected to be the fastest-growing region from 2026 to 2033, with a CAGR of 7.6%, fueled by high birth rates, expanding healthcare access, government maternal health initiatives, and improving rural healthcare infrastructure.

- Ectopic Pregnancy are the fastest-growing pregnancy type, projected to register a CAGR of 7.9%, reflecting the surge in incidence linked to delayed pregnancies and reproductive health complications.

- The Premature Labor and Birth segment dominated the complications category with a 46.21% revenue share in 2025, led by the increasing incidence of preterm deliveries globally and associated neonatal care requirements.

- Vaginal Delivery accounted for 55.63% of the market, preferred by its lower cost, faster recovery time, and reduced medical intervention requirements.

- The Cesarean Section segment is the fastest-growing delivery type category, with a CAGR of 7.6%, driven by the rising high-risk pregnancies and increasing maternal age globally.

Market Size & Forecast

- Global Market Value (2025): USD 19.83 Billion

- Expected Market Value (2033): USD 39.51 Billion

- Forecast CAGR (2026–2033): 9.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Maternal Health Market Segmentation

|

Attributes |

Maternal Health Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Merck & Co., Inc., (U.S.) · Bayer AG (Germany) · Abbott (U.S.) · Johnson & Johnson Services, Inc. (U.S.) · Pfizer Inc. (U.S.) · Novartis AG (Switzerland) · F. Hoffmann-La Roche Ltd (Switzerland) · Sanofi (France) · GSK plc (U.K.) · Organon & Co. (U.S.) · CooperSurgical Inc. (U.S.) · Hologic, Inc. (U.S.) · GE HealthCare. (U.S.) · Siemens Healthineers AG (Germany) · Koninklijke Philips N.V. (Netherlands) · BD (U.S.) · Medtronic (Ireland) · Danaher (U.S.) · Thermo Fisher Scientific Inc. (U.S.) |

|

Market Opportunities |

· Expansion of AI-driven maternal risk prediction platforms · Growth of home-based maternal care ecosystems using wearable fetal and maternal monitoring devices · Increasing opportunity for integrated maternal nutrition and micronutrient management programs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Maternal Health Market Trends

Trend: Growth in Digital Maternal Care & Remote Monitoring

Healthcare providers are increasingly adopting digital maternal care solutions including telehealth consultations, remote fetal monitoring, and mobile health applications to improve pregnancy tracking and early risk detection. The integration of wearable devices enables continuous monitoring of maternal vital signs and fetal health indicators, while AI-driven analytics help in identifying complications such as preeclampsia and gestational diabetes at an early stage. For instance, cloud-based maternal health platforms and connected monitoring kits are being deployed across hospitals and home-care settings to enhance continuity of care and reduce maternal mortality risks.

Maternal Health Market Dynamics

Key Market Driver: Rising Focus on Reducing Maternal Mortality Rates

The global push to reduce maternal and infant mortality is significantly driving investments in maternal healthcare infrastructure, skilled birth attendance, and prenatal screening programs across both developed and developing regions. Governments and global health organizations are expanding access to antenatal care services, emergency obstetric care, and postnatal follow-ups to improve pregnancy outcomes and reduce preventable deaths. For instance, large-scale maternal welfare initiatives and hospital-based safe delivery programs are being implemented in rural and underserved regions to strengthen maternal care delivery systems.

Key Restraint/Challenge: Limited Access to Quality Maternal Healthcare in Low Income Regions

A major restraint in the maternal health market is the lack of access to quality healthcare services, skilled healthcare professionals, and advanced diagnostic facilities in low-income and rural regions. Inadequate infrastructure, transportation barriers, and financial constraints further limit timely prenatal and emergency obstetric care, increasing the risk of complications during pregnancy and childbirth. For instance, many remote areas still rely on under-equipped primary health centers with limited access to specialized maternal care services, restricting overall market penetration.

Key Market Opportunity: Expansion of AI Enabled Maternal Risk Prediction Platforms

The integration of artificial intelligence and predictive analytics in maternal healthcare presents a significant opportunity to enhance early detection of pregnancy-related complications and personalize care pathways. AI-powered platforms can analyze patient history, biometric data, and real-time monitoring inputs to identify high-risk pregnancies and recommend timely interventions. For instance, digital health ecosystems combining AI algorithms with remote monitoring devices are being deployed in hospital networks and telehealth platforms to improve maternal outcomes and optimize clinical decision making.

Maternal Health Market Scope

The maternal health market is segmented on the basis of type, pregnancy type, risk in pregnancy, complications, delivery type, and application.

- By Type

On the basis of type, the Maternal Health Market is segmented into hormones, nutritives, analgesics, anti-infectives, and others. The Hormones segment dominated the market with a 34.62% share in 2025, owing to widespread use in fertility regulation, pregnancy support therapies, and management of hormonal imbalances during pregnancy. These products are extensively used for luteal phase support, prevention of preterm labor, and management of high-risk pregnancies under clinical supervision. Increasing prevalence of hormonal disorders and infertility cases is further driving demand across both developed and emerging regions. Strong clinical adoption in assisted reproductive technologies is also supporting segment growth. Hospitals and fertility clinics remain the primary end users for hormone-based therapies. Continuous pharmaceutical innovation in safer pregnancy-compatible formulations is reinforcing market dominance.

The Nutritives segment is expected to witness the fastest growth at a CAGR of 8.4% from 2026 to 2033, driven by rising awareness of maternal nutrition and increasing demand for prenatal supplements. These include essential vitamins, minerals, iron, folic acid, and omega fatty acids required for fetal development and maternal health. Government-led supplementation programs and WHO guidelines are strongly promoting their use in developing economies. Growing incidence of anemia and micronutrient deficiencies among pregnant women is further accelerating adoption. Expanding e-pharmacy channels and over-the-counter availability are improving accessibility. Rising focus on preventive maternal healthcare is significantly boosting long-term growth prospects.

- By Pregnancy

On the basis of pregnancy type, the market is segmented into intrauterine, ectopic, tubal, and others. The Intrauterine Pregnancy segment dominated the market with a 71.38% share in 2025, due to its high prevalence and standard clinical management across global healthcare systems. Most prenatal care services, diagnostic procedures, and therapeutic interventions are designed for intrauterine pregnancies. Strong integration of routine antenatal monitoring and hospital-based care further supports dominance. Increasing use of ultrasound and non-invasive prenatal testing enhances early detection and monitoring. Availability of structured maternal care pathways ensures consistent treatment outcomes. High global birth rates also contribute significantly to this segment’s leadership.

The Ectopic Pregnancy segment is expected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033, driven by rising incidence linked to delayed pregnancies and reproductive health complications. Early diagnosis through advanced imaging and biomarker testing is improving detection rates. Increasing awareness among women regarding early pregnancy symptoms is supporting timely medical intervention. Hospitals are increasingly adopting minimally invasive surgical and pharmacological treatments for better outcomes. Growing infertility treatments and assisted reproduction procedures are also contributing to risk prevalence. Expanding emergency obstetric care infrastructure is further supporting segment growth.

- By Risk in Pregnancy

On the basis of risk in pregnancy, the market is segmented into high risk and molar pregnancy. The High-Risk Pregnancy segment dominated the market with a 68.94% share in 2025, driven by increasing maternal age, rising prevalence of chronic diseases, and lifestyle-related complications during pregnancy. Advanced monitoring systems and frequent prenatal checkups are widely used for managing such cases. Hospitals and specialty clinics provide intensive maternal-fetal care to reduce complications. Government programs focusing on safe motherhood initiatives further strengthen this segment. Increasing use of AI-based risk prediction tools is improving early identification and management. High healthcare expenditure on complicated pregnancies supports sustained dominance.

The Molar Pregnancy segment is expected to witness the fastest growth at a CAGR of 7.5% from 2026 to 2033, due to improved diagnostic capabilities and rising clinical awareness. Early ultrasound screening and hormonal testing are enhancing detection accuracy. Increasing adoption of specialized gynecological treatments is improving patient outcomes. Although rare, growing reporting rates are contributing to measured market expansion. Better access to tertiary care hospitals is supporting treatment availability. Research advancements in reproductive pathology are further strengthening clinical management approaches.

- By Complications

On the basis of complications, the market is segmented into miscarriage, premature labor and birth, and others. The Premature Labor and Birth segment dominated the market with a 46.21% share in 2025, driven by increasing incidence of preterm deliveries globally and associated neonatal care requirements. Advanced neonatal intensive care units (NICUs) are heavily utilized in such cases. Rising maternal stress, infections, and chronic conditions are contributing to higher preterm birth rates. Strong hospital infrastructure for emergency obstetric care supports this segment’s dominance. Government programs focused on reducing neonatal mortality are further strengthening demand. Continuous monitoring technologies are improving management of preterm labor risks.

The Miscarriage segment is expected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by increasing awareness, improved diagnostic screening, and better reporting systems. Early pregnancy monitoring and hormonal testing are enabling faster detection of pregnancy loss risks. Expanding access to reproductive health services is improving treatment adoption. Growing psychological counseling and post-miscarriage care services are supporting holistic maternal care. Rising infertility treatments are indirectly increasing monitored pregnancies. Enhanced maternal health education is contributing to early intervention and management.

- By Delivery Type

On the basis of delivery type, the market is segmented into vaginal delivery, cesarean section, and others. The Vaginal Delivery segment dominated the market with a 55.63% share in 2025, due to its lower cost, faster recovery time, and reduced medical intervention requirements. It remains the preferred mode of delivery in both developed and developing regions when no complications are present. Strong emphasis on natural birth practices and maternal health guidelines supports this dominance. Hospitals provide structured labor monitoring and pain management support to facilitate safe deliveries. Increasing awareness of long-term health benefits also contributes to preference for vaginal birth. Public healthcare systems strongly encourage this delivery method where medically feasible.

The Cesarean Section segment is expected to witness the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by rising high-risk pregnancies and increasing maternal age globally. Improved surgical safety and advanced hospital infrastructure are making cesarean procedures more accessible. Growing preference for scheduled deliveries among urban populations is also contributing to growth. Increased monitoring of fetal distress and pregnancy complications is leading to higher surgical intervention rates. Expanding insurance coverage is reducing financial barriers. Technological advancements in obstetric surgery are further improving outcomes.

- By Application

On the basis of application, the market is segmented into hospitals, clinics, household, and others. The Hospitals segment dominated the market with a 63.85% share in 2025, driven by availability of comprehensive maternal care services, advanced diagnostic facilities, and skilled healthcare professionals. Hospitals serve as the primary centers for both routine and high-risk pregnancy management. Strong infrastructure for emergency obstetric care and neonatal services further supports dominance. Increasing adoption of digital maternal monitoring systems in hospitals enhances care efficiency. Government funding and insurance coverage also favor hospital-based deliveries. Continuous technological upgrades strengthen their leadership position.

The Household segment is expected to register the fastest growth at a CAGR of 8.2% from 2026 to 2033, driven by rising adoption of home-based maternal care and telehealth services. Wearable devices and remote monitoring tools enable safe pregnancy tracking outside clinical settings. Increasing preference for personalized and convenient care is supporting this trend. Expansion of digital health platforms is improving accessibility in rural and underserved areas. Cost-effective home monitoring solutions are further accelerating adoption. Growing awareness of maternal self-care and preventive health practices is strengthening this segment’s growth trajectory.

Maternal Health Market Regional Analysis

North America dominated the Maternal Health Market with the largest revenue share of 38.46% in 2025, supported by strong maternal care infrastructure, high healthcare spending, and widespread adoption of advanced prenatal monitoring technologies. The region also benefits from well-established hospital networks, extensive insurance coverage, and high awareness of maternal and fetal health management. Increasing use of AI-enabled risk assessment tools, telehealth-based prenatal consultations, and continuous fetal monitoring systems is further strengthening regional leadership. Growing focus on reducing maternal mortality and improving pregnancy outcomes continues to support North America’s dominance in the global market.

U.S. Maternal Health Market Insight

The U.S. maternal health market is witnessing strong growth due to advanced maternal care infrastructure, high healthcare spending, and widespread adoption of digital health and prenatal monitoring solutions. The country’s well-established hospital networks, strong insurance coverage, and focus on reducing maternal mortality are driving demand across prenatal, delivery, and postnatal care services. Increasing use of AI-enabled risk prediction tools, telehealth consultations, and remote fetal monitoring systems is further enhancing care quality. In addition, rising awareness of high-risk pregnancies and continuous innovation in maternal-fetal medicine are strengthening market growth in the U.S.

Europe Maternal Health Market Insight

The Europe maternal health market remains a major contributor to global revenue, driven by strong public healthcare systems, government-supported maternal welfare programs, and high standards of prenatal and postnatal care. Widespread access to hospital-based maternal services and increasing focus on early screening and preventive care are supporting regional expansion. The adoption of digital health platforms, telemedicine in obstetrics, and advanced diagnostic technologies is improving maternal outcomes. Furthermore, stringent healthcare regulations and increasing investments in maternal health infrastructure continue to enhance the adoption of comprehensive maternal care solutions across Europe.

U.K. Maternal Health Market Insight

The U.K. maternal health market is experiencing steady growth, supported by the National Health Service (NHS) maternal care programs, rising adoption of digital maternity records, and increasing focus on reducing pregnancy-related complications. Growing demand for personalized prenatal care and expanding use of telehealth services for antenatal consultations are contributing to market development. Integration of AI-based risk assessment tools and remote monitoring solutions is improving early detection of maternal health risks. Furthermore, continuous investments in improving maternity ward infrastructure and workforce training are strengthening overall maternal care delivery in the country.

Germany Maternal Health Market Insight

The Germany maternal health market is expanding steadily due to a strong healthcare system, advanced diagnostic capabilities, and increasing focus on maternal-fetal medicine. Hospitals and specialized clinics are widely adopting advanced prenatal screening technologies and digital health tools to improve pregnancy outcomes. Rising awareness of high-risk pregnancies and increasing maternal age are further driving demand for enhanced monitoring and care services. In addition, government support for maternal health programs and continuous innovation in clinical practices are strengthening Germany’s position in the European maternal health market.

Asia-Pacific Maternal Health Market Insight

The Asia-Pacific maternal health market is expected to witness rapid growth, driven by high birth rates, improving healthcare access, and increasing government initiatives focused on maternal and child health. Expanding hospital infrastructure and rising adoption of digital health solutions are supporting better prenatal and postnatal care across the region. Growing awareness of maternal nutrition, safe delivery practices, and early pregnancy monitoring is further boosting demand. In addition, increasing investments in rural healthcare systems and telemedicine platforms are accelerating maternal health service penetration in emerging economies.

Japan Maternal Health Market Insight

The Japan maternal health market is witnessing consistent growth due to advanced healthcare infrastructure, high-quality maternal care services, and strong focus on maternal-fetal safety. Increasing maternal age and rising prevalence of high-risk pregnancies are driving demand for advanced prenatal monitoring and diagnostic technologies. Widespread adoption of digital health tools and AI-enabled risk assessment systems is improving pregnancy management. Moreover, Japan’s emphasis on precision medicine and continuous innovation in obstetric care is further contributing to market growth.

China Maternal Health Market Insight

The China maternal health market is growing rapidly, driven by expanding healthcare infrastructure, rising government focus on maternal and child health, and increasing awareness of prenatal care services. Growing adoption of hospital-based delivery systems and improved access to antenatal care in urban and rural areas are supporting market expansion. Integration of digital health platforms, telemedicine services, and AI-based maternal monitoring solutions is significantly enhancing care delivery. In addition, rising healthcare investments and efforts to reduce maternal mortality are positioning China as one of the fastest-growing maternal health markets globally.

Maternal Health Market Share

The maternal health industry is primarily led by well-established companies, including:

- Merck & Co., Inc., (U.S.)

- Bayer AG (Germany)

- Abbott (U.S.)

- Johnson & Johnson Services, Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Novartis AG (Switzerland)

- Hoffmann-La Roche Ltd (Switzerland)

- Sanofi (France)

- GSK plc (U.K.)

- Organon & Co. (U.S.)

- CooperSurgical Inc. (U.S.)

- Hologic, Inc. (U.S.)

- GE HealthCare. (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- BD (U.S.)

- Medtronic (Ireland)

- Danaher (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

Latest Developments in Maternal Health Market

- In April 2024, the World Health Organization (WHO) updated its global recommendations on prevention and management of postpartum hemorrhage, one of the leading causes of maternal deaths worldwide. The updated guidance focuses on early detection, rapid intervention protocols, and improved access to uterotonic medicines in low-resource settings. It also promotes standardized clinical training for birth attendants and improved emergency obstetric response systems. This development is expected to significantly strengthen maternal survival outcomes globally

- In November 2023, the U.S. Centers for Disease Control and Prevention (CDC) published updated maternal mortality data showing persistently high maternal death rates and significant disparities across racial and ethnic groups. The report highlighted cardiovascular conditions as a leading cause of pregnancy-related deaths and emphasized the importance of early diagnosis and continuous postpartum care. It also reinforced the need for improved maternal mortality review committees across states. These findings have influenced ongoing policy reforms and healthcare funding priorities

- In May 2023, the World Health Organization (WHO), along with UNICEF and the World Bank Group, released updated global estimates on maternal mortality covering 2000–2020, highlighting that progress has stagnated in many regions despite earlier improvements. The report emphasized the need for stronger health systems, skilled birth attendance, and emergency obstetric care to prevent avoidable deaths. It also identified sub-Saharan Africa and South Asia as high-burden regions requiring urgent intervention. The findings reinforced global policy focus on maternal survival and healthcare equity

- In March 2022, the White House released the “Blueprint for Addressing the Maternal Health Crisis,” outlining a comprehensive national strategy to reduce maternal mortality and improve maternal care in the United States. The initiative focuses on expanding Medicaid coverage, improving data collection, strengthening workforce capacity, and addressing racial disparities in maternal health outcomes. It also emphasizes increasing access to doula services and community-based care models. This policy framework has accelerated federal and state-level investments in maternal health infrastructure

- In March 2021, the U.S. Centers for Medicare & Medicaid Services (CMS) enabled states under the American Rescue Plan Act to extend postpartum Medicaid coverage from 60 days to 12 months, significantly improving continuity of maternal care and reducing gaps in postnatal treatment access for low-income women. This policy change has been widely adopted across multiple states, strengthening maternal health outcomes by ensuring longer access to essential healthcare services after childbirth. It also supports early detection and management of postpartum complications such as hypertension and depression. The initiative marked a major structural reform in U.S. maternal healthcare delivery

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.