Global Medical Devices Vigilance Market

Market Size in USD Billion

CAGR :

%

USD

73.46 Billion

USD

125.18 Billion

2025

2033

USD

73.46 Billion

USD

125.18 Billion

2025

2033

| 2026 –2033 | |

| USD 73.46 Billion | |

| USD 125.18 Billion | |

| % | |

|

Global Medical Devices Vigilance Market Segmentation, By Delivery Mode (On-Demand/Cloud Based (SAAS) Delivery Mode, and On-Premises Delivery Mode), Application (Diagnostic, Therapeutic, Surgical, and Research), End-User (Clinical Research Organizations (CROs), Original Equipment Manufacturers (OEMs), and Business Process Outsourcing (BPO))- Industry Trends and Forecast to 2033

Medical Devices Vigilance Market Size

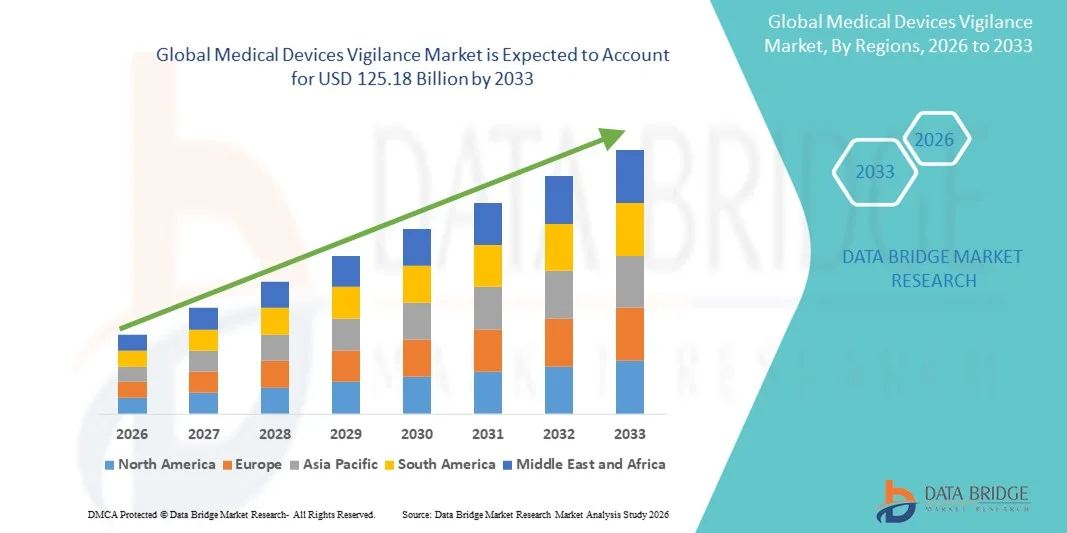

- The global medical devices vigilance market size was valued at USD 73.46 billion in 2025 and is expected to reach USD 125.18 billion by 2033, at a CAGR of 6.89% during the forecast period

- The market growth is largely driven by the rising volume of medical device usage worldwide, coupled with increasingly stringent regulatory requirements for post-market surveillance, adverse event reporting, and patient safety monitoring across healthcare system

- Furthermore, growing awareness among manufacturers and healthcare providers regarding risk management, product traceability, and compliance with global regulations is positioning medical devices vigilance systems as a critical component of modern healthcare infrastructure. These combined factors are accelerating adoption and significantly strengthening the overall market growth

Medical Devices Vigilance Market Analysis

- Medical devices vigilance systems, which enable the monitoring, reporting, and analysis of adverse events and safety issues associated with medical devices, are becoming an essential component of healthcare quality and patient safety frameworks across hospitals, manufacturers, and regulatory bodies due to their role in ensuring compliance and minimizing clinical risk

- The growing demand for medical devices vigilance solutions is primarily driven by the increasing use of complex medical devices, heightened focus on patient safety, and stricter post-market surveillance regulations imposed by global health authorities

- North America dominated the medical devices vigilance market with the largest revenue share of 39.2% in 2025, supported by a mature regulatory environment, strong adoption of digital health solutions, and the presence of major medical device manufacturers, with the U.S. witnessing steady growth in vigilance system adoption to meet stringent FDA post-market surveillance and reporting requirements

- Asia-Pacific is expected to be the fastest growing region in the medical devices vigilance market during the forecast period due to expanding healthcare infrastructure, increasing medical device penetration, and strengthening regulatory frameworks across emerging economies

- On-Demand/Cloud-Based (SaaS) delivery mode dominated the medical devices vigilance market with a market share of 46.8% in 2025, driven by its scalability, cost efficiency, faster deployment, and ability to support real-time adverse event reporting and regulatory compliance across geographically distributed manufacturers and service providers

Report Scope and Medical Devices Vigilance Market Segmentation

|

Attributes |

Medical Devices Vigilance Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Medical Devices Vigilance Market Trends

Digital Transformation Through AI-Enabled Vigilance Platforms

- A significant and accelerating trend in the global medical devices vigilance market is the increasing integration of artificial intelligence (AI), automation, and advanced analytics into post-market surveillance systems to enhance adverse event detection, reporting accuracy, and regulatory compliance

- For instance, leading vigilance software providers are incorporating AI-driven signal detection tools that automatically analyze large volumes of device safety data to identify potential risks earlier, supporting proactive corrective actions and regulatory submissions

- AI integration in medical devices vigilance enables capabilities such as automated case intake, intelligent prioritization of adverse events, and predictive risk assessment based on historical safety data. For instance, AI-based algorithms can flag unusual reporting patterns across diagnostic or therapeutic devices, allowing manufacturers to address safety issues before escalation

- The growing adoption of cloud-based vigilance platforms further supports seamless data integration across geographies, enabling centralized monitoring of device performance, regulatory reporting, and audit readiness within a unified digital ecosystem

- This trend toward intelligent, data-driven, and automated vigilance systems is reshaping how manufacturers and service providers manage post-market compliance, with increased focus on real-time monitoring and regulatory transparency

- The demand for AI-enabled and cloud-integrated medical devices vigilance solutions is rising steadily among OEMs, CROs, and BPOs as they seek scalable, cost-effective, and compliant approaches to manage growing device portfolios globally

- The growing availability of SaaS-based vigilance solutions is further accelerating adoption by reducing infrastructure dependency and enabling faster deployment for global manufacturers

Medical Devices Vigilance Market Dynamics

Driver

Rising Regulatory Scrutiny and Growing Emphasis on Patient Safety

- The increasing stringency of global regulatory requirements for post-market surveillance and adverse event reporting is a major driver accelerating the adoption of medical devices vigilance systems across the healthcare industry

- For instance, regulatory authorities have strengthened mandates around timely reporting, traceability, and documentation of device-related adverse events, compelling manufacturers to invest in structured vigilance platforms

- As the use of complex diagnostic, therapeutic, and surgical devices expands worldwide, the need to systematically monitor device performance and patient outcomes is intensifying, reinforcing the role of vigilance systems.

- • Furthermore, heightened awareness of patient safety risks and product liability concerns is driving manufacturers to adopt proactive vigilance strategies to minimize recalls, penalties, and reputational damage

- The growing involvement of CROs and BPOs in managing vigilance activities for OEMs, combined with increasing outsourcing of compliance functions, is further supporting market growth and solution adoption

- The rising volume of adverse event data generated from increased device usage is necessitating automated and scalable vigilance solutions to manage reporting obligations efficiently

- Continuous updates to regulatory guidelines across regions are compelling manufacturers to modernize legacy vigilance processes, thereby driving sustained demand for advanced vigilance platforms

Restraint/Challenge

Data Complexity, Integration Issues, and Compliance Burden

- Managing large volumes of heterogeneous safety data across multiple device categories, regions, and regulatory frameworks poses a significant challenge for effective implementation of medical devices vigilance systems

- For instance, inconsistencies in reporting formats, regional regulatory variations, and fragmented data sources can complicate timely adverse event analysis and regulatory submissions

- Ensuring data accuracy, validation, and traceability across on-premises and cloud-based systems remains complex, particularly for organizations operating across multiple markets and jurisdictions

- In addition, high implementation costs, integration challenges with legacy IT systems, and the need for skilled regulatory professionals can act as barriers, especially for small and mid-sized manufacturers

- Overcoming these challenges through standardized data frameworks, improved system interoperability, and regulatory harmonization efforts will be essential to sustain long-term growth in the global medical devices vigilance market. Data privacy and cybersecurity concerns related to cloud-based vigilance platforms can further restrain adoption, particularly in regions with strict data protection regulations.

- Limited internal regulatory expertise within smaller organizations may increase reliance on external service providers, adding to operational costs and complexity

Medical Devices Vigilance Market Scope

The market is segmented on the basis of delivery mode, application, and end-user.

- By Delivery Mode

On the basis of delivery mode, the global medical devices vigilance market is segmented into On-Demand/Cloud-Based (SaaS) Delivery Mode and On-Premises Delivery Mode. The On-Demand/Cloud-Based (SaaS) delivery mode dominated the market with the largest revenue share of 46.8% in 2025, driven by its scalability, cost-effectiveness, and ability to support real-time adverse event reporting across geographies. Cloud-based vigilance platforms allow manufacturers and service providers to centralize safety data from multiple regions, ensuring faster regulatory submissions and improved compliance management. The reduced need for internal IT infrastructure and maintenance further enhances adoption, particularly among small and mid-sized OEMs. In addition, SaaS solutions support frequent regulatory updates, ensuring systems remain aligned with evolving global compliance requirements. The growing reliance on remote work environments and distributed regulatory teams has also strengthened demand for cloud-based vigilance platforms. These factors collectively position SaaS delivery as the dominant delivery mode in the market.

The On-Premises delivery mode is expected to witness the fastest growth rate during the forecast period, driven by heightened data security concerns and stringent internal compliance policies among large medical device manufacturers. Organizations operating in regions with strict data localization and privacy regulations often prefer on-premises deployment to maintain full control over sensitive patient and device safety data. On-premises solutions offer greater customization capabilities, allowing companies to tailor vigilance workflows to complex internal processes. Large OEMs with legacy IT systems also favor on-premises models due to easier integration with existing enterprise software. Furthermore, concerns around cybersecurity threats in cloud environments continue to support demand for on-premises deployment. These factors are contributing to steady growth of on-premises vigilance solutions globally.

- By Application

On the basis of application, the global medical devices vigilance market is segmented into diagnostic, therapeutic, surgical, and research applications. The Diagnostic application segment dominated the market in 2025, driven by the widespread and increasing use of diagnostic devices across hospitals, laboratories, and imaging centers. High volumes of diagnostic procedures generate substantial adverse event and performance data, necessitating robust vigilance systems. Frequent updates and innovations in diagnostic technologies further increase the need for continuous post-market monitoring and regulatory reporting. Diagnostic devices are often used across diverse patient populations, increasing the importance of systematic safety surveillance. Regulatory authorities also place strong emphasis on diagnostic accuracy and reliability, reinforcing vigilance adoption in this segment. As a result, diagnostic applications account for the largest share of the medical devices vigilance market.

The Therapeutic application segment is expected to register the fastest growth during the forecast period, supported by the rising adoption of implantable and advanced therapeutic devices. These devices often carry higher patient risk, requiring intensive post-market surveillance and risk management. Increasing use of combination products and digitally enabled therapeutic devices further amplifies vigilance requirements. Manufacturers are investing heavily in advanced vigilance solutions to detect safety signals early and avoid costly recalls. In addition, regulatory agencies are tightening monitoring requirements for therapeutic devices, accelerating adoption of vigilance systems. These factors are driving rapid growth in the therapeutic application segment.

- By End-User

On the basis of end-user, the global medical devices vigilance market is segmented into Clinical Research Organizations (CROs), Original Equipment Manufacturers (OEMs), and Business Process Outsourcing (BPO) providers. The Original Equipment Manufacturers (OEMs) segment dominated the market with the largest revenue share in 2025, as OEMs bear primary responsibility for regulatory compliance and post-market surveillance of their devices. Increasing regulatory scrutiny has compelled manufacturers to invest directly in robust vigilance platforms. OEMs manage large and diverse product portfolios, generating significant volumes of safety data that require centralized monitoring and reporting. Vigilance systems help OEMs mitigate legal risks, reduce recall costs, and protect brand reputation. The integration of vigilance solutions with quality management and regulatory systems further supports OEM adoption. These factors collectively position OEMs as the leading end-user segment.

The Business Process Outsourcing (BPO) segment is anticipated to witness the fastest growth rate during the forecast period, driven by the increasing outsourcing of vigilance and compliance activities by medical device manufacturers. BPO providers offer cost-efficient, scalable, and specialized regulatory expertise, making them attractive to OEMs managing multi-country reporting obligations. Growing complexity of global regulations has increased reliance on external service providers for adverse event reporting and documentation. BPOs leverage advanced vigilance platforms to handle large case volumes efficiently across regions. In addition, emerging markets are becoming key hubs for vigilance outsourcing services. These dynamics are accelerating the growth of the BPO end-user segment in the global medical devices vigilance market.

Medical Devices Vigilance Market Regional Analysis

- North America dominated the medical devices vigilance market with the largest revenue share of 39.2% in 2025, supported by a mature regulatory environment, strong adoption of digital health solutions, and the presence of major medical device manufacturers, with the U.S. witnessing steady growth in vigilance system adoption to meet stringent FDA post-market surveillance and reporting requirements

- Healthcare stakeholders in the region place significant emphasis on regulatory compliance, data accuracy, and timely adverse event reporting, supported by advanced digital health infrastructure and widespread adoption of automated vigilance platforms

- This strong market position is further reinforced by the presence of major medical device manufacturers, well-established regulatory frameworks, and high investments in compliance technologies, positioning medical devices vigilance systems as a critical component of healthcare quality management across the region

U.S. Medical Devices Vigilance Market Insight

The U.S. medical devices vigilance market captured the largest revenue share within North America in 2025, driven by strict FDA regulations, high medical device utilization, and strong emphasis on patient safety. Manufacturers and healthcare stakeholders increasingly prioritize robust post-market surveillance systems to ensure timely adverse event reporting and regulatory compliance. The growing complexity of diagnostic, therapeutic, and surgical devices is further increasing vigilance requirements. In addition, widespread adoption of digital health technologies and automated reporting platforms supports market growth. The strong presence of global medical device OEMs and CROs continues to reinforce the U.S. market’s leading position.

Europe Medical Devices Vigilance Market Insight

The Europe medical devices vigilance market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by stringent EU Medical Device Regulation (MDR) and heightened focus on post-market surveillance. Increasing regulatory scrutiny across member states is compelling manufacturers to strengthen vigilance systems and documentation processes. Rising adoption of advanced medical technologies across hospitals and clinics is also generating higher volumes of safety data. European stakeholders value standardized, compliant vigilance frameworks to manage multi-country reporting obligations. Growth is evident across diagnostic, therapeutic, and surgical device segments, supporting overall market expansion.

U.K. Medical Devices Vigilance Market Insight

The U.K. medical devices vigilance market is anticipated to grow at a notable CAGR during the forecast period, driven by evolving regulatory frameworks and increased focus on patient safety post-Brexit. Medical device manufacturers operating in the U.K. are investing in advanced vigilance solutions to align with national and international compliance requirements. Growing use of innovative medical devices across healthcare settings is increasing adverse event reporting volumes. The U.K.’s strong clinical research ecosystem further supports vigilance adoption. In addition, rising outsourcing of regulatory and vigilance activities is contributing to market growth.

Germany Medical Devices Vigilance Market Insight

The Germany medical devices vigilance market is expected to expand at a considerable CAGR during the forecast period, supported by the country’s strong medical technology sector and emphasis on regulatory compliance. Germany’s advanced healthcare infrastructure generates significant demand for systematic post-market surveillance solutions. Manufacturers place high importance on data accuracy, traceability, and patient safety, driving adoption of sophisticated vigilance platforms. The country’s focus on quality management and risk mitigation further reinforces market growth. Integration of vigilance systems with existing quality and regulatory frameworks is becoming increasingly prevalent.

Asia-Pacific Medical Devices Vigilance Market Insight

The Asia-Pacific medical devices vigilance market is poised to grow at the fastest CAGR during the forecast period, driven by expanding healthcare infrastructure, rising medical device adoption, and strengthening regulatory oversight across emerging economies. Countries such as China, Japan, and India are witnessing increased awareness of post-market surveillance requirements. Growing participation of global OEMs in APAC markets is also accelerating demand for scalable vigilance solutions. In addition, the region’s emergence as a hub for clinical research and manufacturing is increasing adverse event reporting volumes. These factors collectively support rapid market growth in Asia-Pacific.

Japan Medical Devices Vigilance Market Insight

The Japan medical devices vigilance market is gaining momentum due to the country’s advanced healthcare system, aging population, and strong regulatory focus on device safety. Increased use of high-end diagnostic and therapeutic devices is driving the need for robust vigilance mechanisms. Japanese manufacturers emphasize precision, reliability, and compliance, supporting adoption of advanced vigilance platforms. Integration of digital technologies into healthcare workflows is further streamlining adverse event monitoring. The demand for efficient and accurate reporting systems continues to support steady market growth.

India Medical Devices Vigilance Market Insight

The India medical devices vigilance market accounted for a significant revenue share within Asia Pacific in 2025, driven by rapid healthcare expansion, increasing medical device penetration, and growing regulatory awareness. India’s rising adoption of diagnostic and therapeutic devices is generating higher volumes of safety and performance data. Government initiatives aimed at strengthening regulatory frameworks are encouraging manufacturers to adopt structured vigilance systems. The presence of cost-effective vigilance service providers and BPOs further supports market development. In addition, increased participation of global OEMs in the Indian market is reinforcing long-term growth prospects.

Medical Devices Vigilance Market Share

The Medical Devices Vigilance industry is primarily led by well-established companies, including:

- AssurX, Inc. (U.S.)

- Ennov (France)

- Sparta Systems (U.S.)

- Veeva Systems Inc. (U.S.)

- IQVIA (U.S.)

- AB Cube (France)

- EXTEDO GmbH (Germany)

- Oracle (U.S.)

- Medtronic (Ireland)

- Johnson & Johnson Services, Inc. (U.S.)

- Abbott (U.S.)

- Siemens Healthineers AG (Germany)

- Koninklijke Philips N.V. (Netherlands)

- Baxter (U.S.)

- Boston Scientific Corporation (U.S.)

- Stryker (U.S.)

- Thermo Fisher Scientific Inc. (U.S.)

- Cardinal Health (U.S.)

- Zimmer Biomet (U.S.)

- Hologic, Inc. (U.S.)

What are the Recent Developments in Global Medical Devices Vigilance Market?

- In July 2025, the Therapeutic Goods Administration (TGA) of Australia reported that mandatory reporting of medical device adverse events by healthcare facilities has commenced, with voluntary reporting starting March 2025 and full mandatory reporting set to begin March 2026 to boost device safety monitoring and regulatory responsiveness

- In February 2025, the Medical Device Coordination Group (MDCG) of the European Union published an updated MDCG 2023-3 Rev.2 guidance, clarifying and strengthening definitions and timelines for incident and serious incident reporting and aligning vigilance processes with the Eudamed post-market surveillance database to improve transparency and compliance

- In January 2025, the UK Medicines and Healthcare products Regulatory Agency (MHRA) released a new suite of post-market surveillance (PMS) guidance aligned with the 2024 Amendment to Great Britain’s PMS regulations, enhancing vigilance reporting expectations and compliance frameworks for medical device manufacturers in the UK

- In November 2024, the Medical Device Coordination Group (MDCG) updated its European vigilance guidance MDCG 2023-3 to now include in vitro diagnostic devices (IVDs) within the scope of EUDAMED vigilance reporting expanding regulatory clarity and reporting criteria for IVD incidents and serious incidents across the EU

- In May 2024, India’s Central Drugs Standard Control Organisation (CDSCO) issued a circular mandating all medical device license holders to adopt robust adverse event reporting systems and use the Materiovigilance Programme of India (MvPI) platform for timely identification, documentation, and reporting of device-related adverse events

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.