Global Medical Terminology Software Market

Market Size in USD Billion

CAGR :

%

USD

1.97 Billion

USD

7.67 Billion

2025

2033

USD

1.97 Billion

USD

7.67 Billion

2025

2033

| 2026 –2033 | |

| USD 1.97 Billion | |

| USD 7.67 Billion | |

| % | |

|

Medical Terminology Software Market Size

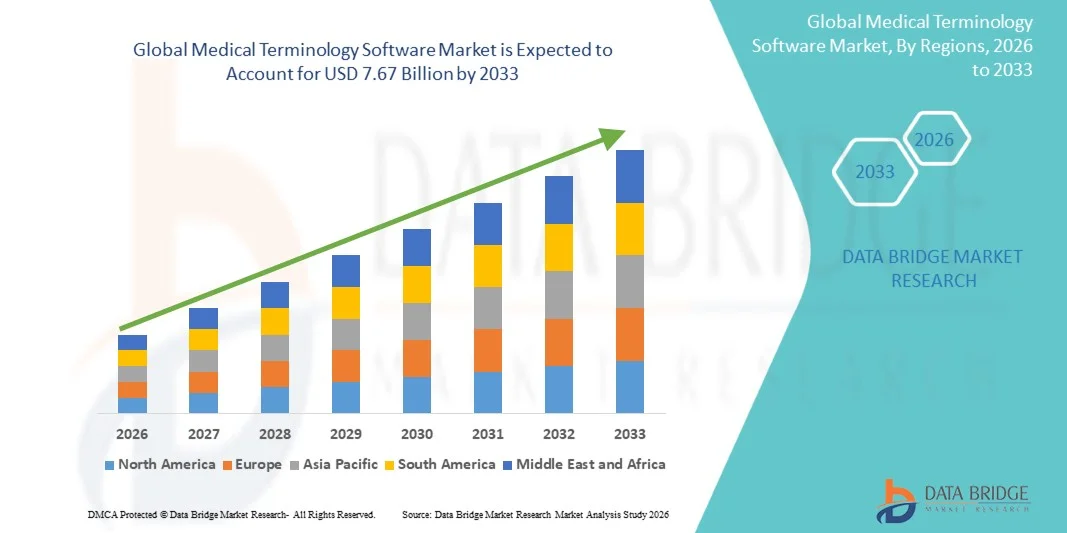

- The global medical terminology software market size was valued at USD 1.97 billion in 2025and is expected to reach USD 7.67 billion by 2033, at a CAGR of 18.52% during the forecast period

- The market growth is largely fueled by the increasing adoption of electronic health records (EHRs), clinical documentation improvement initiatives, and the growing need for standardized healthcare data across hospitals, payers, and research organizations

- Furthermore, rising demand for accurate coding, interoperability, and regulatory compliance, along with advancements in healthcare IT and AI-driven language processing, is establishing medical terminology software as a critical component of modern healthcare systems. These converging factors are accelerating the adoption of terminology solutions, thereby significantly boosting the industry's growth

Medical Terminology Software Market Analysis

- Medical terminology software, designed to standardize, manage, and map clinical vocabulary across healthcare systems, is becoming a critical component of modern healthcare IT infrastructure in both clinical and administrative settings due to its role in ensuring data accuracy, interoperability, and efficient health information exchange

- The escalating demand for medical terminology software is primarily fueled by the widespread adoption of electronic health records (EHRs), increasing regulatory requirements for standardized clinical data, and a growing emphasis on accurate medical coding and billing processes

- North America dominated the medical terminology software market with the largest revenue share of 41.3% in 2025, characterized by advanced healthcare IT infrastructure, strong regulatory frameworks, and early adoption of digital health solutions, with the U.S. witnessing significant implementation across hospitals and payer systems driven by the need for interoperability and compliance standards

- Asia-Pacific is expected to be the fastest growing region in the medical terminology software market during the forecast period due to rapid healthcare digitization, expanding hospital networks, and increasing government initiatives supporting health IT adoption

- The platform segment dominated the medical terminology software market with a market share of 52.8% in 2025, driven by its critical role in enabling real-time terminology management, seamless integration with healthcare IT systems, and support for applications such as data integration, reimbursement, and clinical decision support systems

Report Scope and Medical Terminology Software Market Segmentation

|

Attributes |

Medical Terminology Software Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of AI-driven clinical decision support and natural language processing · Growing demand for global healthcare data interoperability |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Medical Terminology Software Market Trends

“Advancement Through AI-Driven Clinical Language Standardization”

- A significant and accelerating trend in the global medical terminology software market is the deepening integration with artificial intelligence (AI) and advanced natural language processing (NLP) technologies within healthcare IT ecosystems such as electronic health records, clinical decision support systems, and data analytics platforms. This fusion of technologies is significantly enhancing clinical accuracy and data usability

- For instance, 3M Health Information Systems offers AI-powered coding and terminology solutions that integrate with clinical workflows, enabling automated extraction and standardization of medical data across systems. Similarly, Wolters Kluwer provides terminology management integrated with decision support tools to improve documentation accuracy

- AI integration in medical terminology software enables features such as automated clinical coding, real-time error detection, and intelligent mapping across multiple vocabularies. For instance, some platforms utilize AI to continuously learn from clinical inputs to enhance coding precision and can flag inconsistencies or gaps in documentation. Furthermore, NLP capabilities offer users the ability to process unstructured clinical notes into standardized formats efficiently

- The seamless integration of terminology software with broader healthcare IT systems facilitates centralized control over clinical data management. Through a unified interface, healthcare providers can manage coding, billing, reporting, and analytics functions, creating a streamlined and interoperable healthcare environment

- This trend towards more intelligent, intuitive, and interconnected terminology systems is fundamentally reshaping expectations for healthcare data management. Consequently, companies such as Oracle Health are developing AI-enabled solutions with features such as automated terminology updates and interoperability support across global standards

- The demand for medical terminology software that offers seamless AI and NLP integration is growing rapidly across hospitals, research organizations, and payers, as stakeholders increasingly prioritize data accuracy and efficient clinical workflows

- Rising focus on global standardization initiatives such as SNOMED CT and ICD systems is driving the evolution of terminology software toward multi-language support and cross-border interoperability, supporting international healthcare collaboration and public health monitoring

Medical Terminology Software Market Dynamics

Driver

“Growing Need Due to Increasing Healthcare Digitization and Data Standardization Requirements”

- The increasing prevalence of healthcare digitization initiatives and the growing need for standardized clinical data, coupled with the expanding adoption of electronic health record systems, is a significant driver for the heightened demand for medical terminology software

- For instance, in March 2025, Optum announced enhancements in its data interoperability solutions, focusing on improving terminology mapping and coding accuracy. Such strategies by key companies are expected to drive the medical terminology software industry growth in the forecast period

- As healthcare organizations become more focused on improving data quality and regulatory compliance, terminology software offers advanced features such as standardized vocabularies, automated coding, and real-time validation, providing a compelling upgrade over manual processes

- Furthermore, the growing emphasis on value-based care and data-driven decision-making is making terminology software an integral component of healthcare IT systems, offering seamless integration with analytics and reporting platforms

- The need for accurate reimbursement processes, improved clinical documentation, and efficient data exchange between stakeholders are key factors propelling the adoption of terminology software across healthcare ecosystems. The trend towards digital transformation and increasing availability of cloud-based solutions further contribute to market growth

- Growing government mandates and healthcare policies promoting interoperability and standardized reporting are further accelerating adoption, as providers are required to comply with evolving data exchange frameworks and quality reporting standards

- Increasing volume of healthcare data generated from digital health tools, wearable devices, and telehealth platforms is driving demand for advanced terminology solutions capable of managing and structuring large-scale clinical datasets effectively

Restraint/Challenge

“Data Complexity and Integration Challenges with Legacy Systems”

- Concerns surrounding the complexity of integrating medical terminology software with existing legacy healthcare systems, including compatibility issues and data inconsistencies, pose a significant challenge to broader market penetration. As healthcare organizations rely on diverse IT infrastructures, seamless implementation can be difficult

- For instance, reports of interoperability gaps between legacy systems and modern terminology platforms have made some organizations cautious about adopting new solutions due to potential workflow disruptions

- Addressing these integration challenges through standardized frameworks, scalable architectures, and continuous system updates is crucial for ensuring smooth adoption. Companies such as Cerner Corporation emphasize interoperability and integration capabilities in their solutions to mitigate such concerns. In addition, the relatively high implementation cost and need for skilled professionals to manage these systems can be a barrier to adoption for smaller healthcare providers

- While cloud-based and modular solutions are emerging to reduce costs, the perceived complexity and resource requirements can still hinder widespread adoption, particularly in developing healthcare systems or smaller institutions

- Overcoming these challenges through improved interoperability standards, workforce training, and cost-effective deployment models will be vital for sustained market growth

- Data privacy and security concerns related to handling sensitive patient information within terminology platforms can create hesitation among healthcare organizations, particularly with increasing cyber threats and strict data protection regulations

- Limited availability of skilled professionals with expertise in clinical informatics and terminology management can further restrict effective implementation and optimization of these systems across healthcare settings

Medical Terminology Software Market Scope

The market is segmented on the basis of products, application, and end users.

- By Products

On the basis of products, the medical terminology software market is segmented into services and platform. The platform segment dominated the market with the largest market revenue share of 52.8% in 2025, driven by its central role in enabling standardized terminology management, interoperability, and real-time clinical data processing across healthcare systems. Platforms provide integrated solutions that support multiple applications such as coding, reimbursement, and decision support, making them indispensable for large healthcare organizations. Their ability to seamlessly integrate with electronic health records and hospital information systems further strengthens their dominance. In addition, continuous advancements in cloud-based platforms and AI-powered functionalities enhance scalability and efficiency, attracting widespread adoption. The growing demand for centralized data governance and improved clinical accuracy also contributes significantly to the dominance of this segment.

The services segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the increasing need for implementation, consulting, maintenance, and training services associated with terminology solutions. As healthcare providers adopt more complex digital systems, the demand for expert support to ensure smooth deployment and optimization is rising rapidly. Services play a critical role in customizing solutions according to organizational needs and ensuring compliance with evolving healthcare regulations. Furthermore, the expansion of cloud-based and subscription-based models is driving recurring service demand. The rising focus on interoperability and data migration from legacy systems is also accelerating the growth of this segment.

- By Application

On the basis of application, the medical terminology software market is segmented into data aggregation, reimbursement, public health surveillance, data integration, decision support, clinical trials, quality reporting, and clinical guidelines. The reimbursement segment dominated the market with the largest market revenue share in 2025, driven by the critical need for accurate coding and billing processes in healthcare systems. Terminology software ensures standardized clinical documentation, reducing claim denials and improving revenue cycle efficiency for healthcare providers and payers. The increasing complexity of coding standards such as ICD and CPT further necessitates advanced terminology tools. In addition, the rising emphasis on value-based care models is boosting the demand for precise reimbursement systems. The ability of these solutions to minimize errors and ensure compliance with regulatory requirements strengthens their widespread adoption.

The clinical trials segment is expected to witness the fastest CAGR from 2026 to 2033, driven by the growing number of clinical research activities and the need for standardized data across global trial sites. Terminology software plays a vital role in harmonizing clinical data, ensuring consistency, and enabling efficient data sharing among stakeholders. The increasing adoption of decentralized and digital clinical trials is further accelerating demand for advanced terminology solutions. Moreover, regulatory requirements for accurate and transparent trial data reporting are contributing to segment growth. The integration of AI and analytics tools into clinical trial processes is also enhancing the adoption of terminology platforms in this segment.

- By End Users

On the basis of end users, the medical terminology software market is segmented into healthcare providers, healthcare payers, and healthcare IT vendors. The healthcare providers segment dominated the market with the largest market revenue share in 2025, driven by the extensive use of terminology software in hospitals, clinics, and diagnostic centers for clinical documentation and patient data management. Providers rely heavily on these solutions to ensure accurate coding, improve patient care, and maintain compliance with regulatory standards. The widespread adoption of electronic health records and digital health systems further supports segment growth. In addition, the need for efficient data exchange and interoperability among healthcare systems is strengthening the demand among providers. The increasing patient volume and complexity of medical data also contribute significantly to this dominance.

The healthcare IT vendors segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by the rising demand for integrated healthcare solutions and software platforms. These vendors are increasingly embedding terminology management capabilities into their products to enhance functionality and interoperability. The growing trend of digital transformation in healthcare is driving partnerships between IT vendors and healthcare organizations. Furthermore, continuous innovation in AI, cloud computing, and data analytics is enabling vendors to offer advanced terminology solutions. The increasing need for scalable and customizable healthcare IT systems is also accelerating the growth of this segment.

Medical Terminology Software Market Regional Analysis

- North America dominated the medical terminology software market with the largest revenue share of 41.3% in 2025, characterized by advanced healthcare IT infrastructure, strong regulatory frameworks, and early adoption of digital health solutions

- Healthcare organizations in the region highly value the accuracy, interoperability, and regulatory compliance offered by medical terminology software, along with its seamless integration with systems such as electronic health records and clinical decision support platforms

- This widespread adoption is further supported by advanced healthcare infrastructure, high healthcare spending, a technologically advanced ecosystem, and the growing preference for data-driven decision-making, establishing medical terminology software as a critical solution for healthcare providers, payers, and IT vendors

U.S. Medical Terminology Software Market Insight

The United States medical terminology software market captured the largest revenue share of 79% in 2025 within North America, fueled by the rapid adoption of digital health technologies and the widespread implementation of electronic health records systems. Healthcare organizations are increasingly prioritizing accurate clinical documentation and standardized data exchange through advanced terminology solutions. The growing preference for AI-powered coding tools, combined with strong demand for interoperability and compliance-driven platforms, further propels the industry. Moreover, the increasing integration of healthcare IT systems, such as clinical decision support and data analytics platforms, is significantly contributing to the market's expansion.

Europe Medical Terminology Software Market Insight

The Europe medical terminology software market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by stringent regulatory frameworks and the growing need for standardized healthcare data across countries. The increase in digital health adoption, coupled with the demand for interoperable systems, is fostering the adoption of terminology software. European healthcare providers are also drawn to the accuracy and efficiency these solutions offer. The region is experiencing significant growth across hospitals, research institutions, and public health systems, with terminology platforms being integrated into both new and existing healthcare IT infrastructures.

U.K. Medical Terminology Software Market Insight

The United Kingdom medical terminology software market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by the increasing focus on healthcare digitization and the need for improved data accuracy and patient outcomes. In addition, regulatory requirements and reporting standards are encouraging healthcare providers to adopt standardized terminology systems. The UK’s strong healthcare infrastructure, alongside its emphasis on data-driven care, is expected to continue to stimulate market growth.

Germany Medical Terminology Software Market Insight

The Germany medical terminology software market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of data standardization and the demand for advanced healthcare IT solutions. Germany’s well-developed healthcare infrastructure, combined with its emphasis on innovation and efficiency, promotes the adoption of terminology software across hospitals and research centers. The integration of terminology solutions with digital health systems is also becoming increasingly prevalent, with a strong preference for secure and compliant data management aligning with local requirements.

Asia-Pacific Medical Terminology Software Market Insight

The Asia-Pacific medical terminology software market is poised to grow at the fastest CAGR of 23% during the forecast period of 2026 to 2033, driven by increasing healthcare digitization, rising investments in healthcare IT, and technological advancements in countries such as China, Japan, and India. The region's growing inclination towards digital healthcare systems, supported by government initiatives promoting interoperability and data standardization, is driving adoption. Furthermore, as Asia-Pacific emerges as a key hub for healthcare infrastructure development, the accessibility and implementation of terminology software are expanding across a broader range of healthcare providers.

Japan Medical Terminology Software Market Insight

The Japan medical terminology software market is gaining momentum due to the country’s advanced healthcare system, rapid technological adoption, and demand for precision in clinical data management. The Japanese market places a significant emphasis on accuracy and efficiency, and the adoption of terminology software is driven by the increasing use of digital health platforms. The integration of terminology solutions with electronic health records and analytics systems is fueling growth. Moreover, Japan's aging population is likely to spur demand for more efficient and standardized healthcare data systems in both clinical and administrative settings.

India Medical Terminology Software Market Insight

The India medical terminology software market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country's expanding healthcare infrastructure, rapid digital transformation, and increasing adoption of health IT solutions. India stands as one of the fastest-growing markets for digital healthcare technologies, and terminology software is becoming increasingly important in hospitals, clinics, and research organizations. The push towards digital health initiatives and the availability of scalable, cost-effective solutions, alongside growing domestic IT capabilities, are key factors propelling the market in India.

Medical Terminology Software Market Share

The Medical Terminology Software industry is primarily led by well-established companies, including:

- Wolters Kluwer N.V. (Netherlands)

- 3M (U.S.)

- Intelligent Medical Objects, Inc. (U.S.)

- Clinical Architecture, LLC (U.S.)

- Apelon, Inc. (U.S.)

- CareCom A/S (Denmark)

- B2i Healthcare (Hungary)

- BiTAC Informatica S.A. (Spain)

- BT Clinical Computing (Belgium)

- HiveWorx Ltd (Ireland)

- Clinithink Limited (U.K.)

- InterSystems Corporation (U.S.)

- Optum, Inc. (U.S.)

- Elsevier B.V. (Netherlands)

- Epic Systems Corporation (U.S.)

- Oracle Corporation (U.S.)

- Health Catalyst, Inc. (U.S.)

- SNOMED International (U.K.)

- First Databank, Inc. (U.S.)

- Medisolv, Inc. (U.S.)

What are the Recent Developments in Global Medical Terminology Software Market?

- In January 2024, Wolters Kluwer announced that its Health Language Platform is being leveraged by Innovaccer to enhance healthcare data interoperability and normalization across providers, payers, and life sciences organizations. The collaboration enables organizations to standardize disparate clinical data and generate meaningful insights for value-based care. This development highlights the increasing role of terminology platforms in enabling unified patient data views and improving healthcare outcomes

- In October 2023, Wolters Kluwer launched its Health Language Platform as a cloud-based FHIR terminology server integrated with Microsoft Azure Health Data Services, designed to standardize and harmonize healthcare data across systems. The platform enables organizations to map and manage clinical vocabularies efficiently, improving interoperability and supporting AI-driven analytics. This launch underscores the growing shift toward cloud-native and interoperable terminology solutions in healthcare IT

- In December 2023, Wolters Kluwer highlighted the growing impact of generative AI in healthcare, emphasizing its role in improving clinical decision-making, reducing administrative burden, and enhancing data standardization across systems. The company’s focus on AI-driven innovation signals a broader industry trend toward embedding intelligent capabilities within terminology and clinical decision support platforms

- In July 2022, 3M announced plans to spin off its healthcare business, including its health information systems and medical terminology-related solutions, into a separate entity to enhance focus and innovation. The move aims to create a dedicated healthcare technology company better positioned to advance solutions in clinical documentation, coding, and data standardization

- In March 2022, Intelligent Medical Objects was acquired by Thomas H. Lee Partners in a deal valued at over USD 1.5 billion, aimed at accelerating innovation in clinical data quality and terminology solutions. The company’s flagship platform, IMO Core, enables clinicians to document patient data using familiar language while mapping it to standardized medical codes

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.