Global Melanoma Market

Market Size in USD Billion

CAGR :

%

USD

8.38 Billion

USD

20.45 Billion

2025

2033

USD

8.38 Billion

USD

20.45 Billion

2025

2033

| 2026 –2033 | |

| USD 8.38 Billion | |

| USD 20.45 Billion | |

| % | |

|

Melanoma Market Size

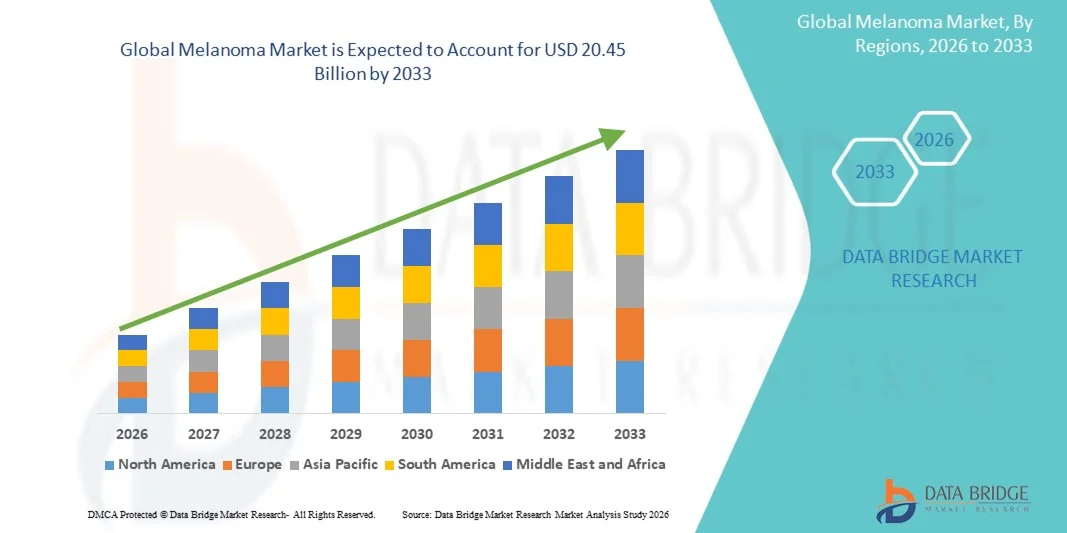

- The global melanoma market size was valued at USD 8.38 billion in 2025and is expected to reach USD 20.45 billion by 2033, at a CAGR of 11.80% during the forecast period

- The market growth is largely driven by the increasing incidence of melanoma cases worldwide, along with advancements in targeted therapies and immunotherapies, leading to improved treatment outcomes and higher adoption rates

- Furthermore, rising awareness regarding early skin cancer detection, growing screening initiatives, and the demand for more effective and personalized treatment options are positioning melanoma therapies as a critical component of oncology care. These converging factors are accelerating the adoption of melanoma treatments, thereby significantly boosting the market’s growth

Melanoma Market Analysis

- Melanoma, a serious form of skin cancer originating in melanocytes, has become a critical focus area in oncology due to its high metastatic potential and increasing global incidence, driving the need for advanced therapeutic approaches across both early-stage and advanced disease settings

- The escalating demand for melanoma treatments is primarily fueled by the rising prevalence of skin cancer, growing awareness regarding early diagnosis, and significant advancements in immunotherapy and targeted therapy, which have markedly improved survival outcomes

- North America dominated the melanoma market with the largest revenue share of 40.8% in 2025, supported by well-established healthcare infrastructure, high awareness levels, and strong adoption of novel therapies, with the U.S. witnessing substantial growth due to increasing screening programs and rapid uptake of checkpoint inhibitors and combination therapies

- Asia-Pacific is expected to be the fastest growing region in the melanoma market during the forecast period due to improving healthcare infrastructure, increasing awareness, and rising healthcare expenditure across emerging economies

- Immunotherapy segment dominated the melanoma market with a market share of 43.6% in 2025, driven by its superior efficacy, durable response rates, and growing preference over conventional chemotherapy treatments

Report Scope and Melanoma Market Segmentation

|

Attributes |

Melanoma Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expansion of combination immunotherapy and targeted therapy regimens · Increasing adoption of AI-driven dermatology tools and telemedicine platforms |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Melanoma Market Trends

“Rising Dominance of Immunotherapy and Precision Oncology”

- A significant and accelerating trend in the global melanoma market is the growing adoption of immunotherapy and precision medicine approaches, including checkpoint inhibitors and targeted therapies, which are transforming treatment paradigms and improving patient outcomes

- For instance, therapies such as pembrolizumab and nivolumab have become standard treatments for advanced melanoma, while targeted drugs such as BRAF and MEK inhibitors are widely used in patients with specific genetic mutations, demonstrating strong clinical efficacy

- Integration of biomarker testing and genomic profiling enables clinicians to tailor treatments based on individual tumor characteristics, improving response rates and minimizing unnecessary exposure to ineffective therapies. For instance, patients with BRAF-mutant melanoma are increasingly treated with combination targeted therapies to enhance survival benefits

- The incorporation of advanced diagnostic tools and digital health platforms supports early detection and continuous disease monitoring, facilitating timely intervention and better management of melanoma across various stages of the disease

- This trend toward more personalized, effective, and technology-driven treatment strategies is fundamentally reshaping oncology care standards for melanoma. Consequently, companies such as Bristol Myers Squibb and Merck & Co., Inc. are expanding their immuno-oncology portfolios and investing in next-generation therapies

- The demand for advanced melanoma therapies offering higher efficacy and personalized treatment approaches is growing rapidly across healthcare systems, as providers increasingly prioritize improved survival outcomes and patient-centric care

- Growing use of real-world evidence and data analytics is supporting better clinical decision-making and optimizing treatment pathways for melanoma patients

Melanoma Market Dynamics

Driver

“Rising Incidence of Skin Cancer and Advancements in Treatment Options”

- The increasing global incidence of melanoma, coupled with continuous advancements in immunotherapy and targeted therapies, is a significant driver for the heightened demand for melanoma treatments

- For instance, in recent years, multiple regulatory approvals for novel immunotherapies and combination regimens have expanded treatment options, significantly improving survival rates for patients with advanced melanoma

- As awareness regarding skin cancer increases and screening programs become more widespread, early diagnosis rates are improving, leading to a higher number of patients receiving timely and effective treatment interventions

- Furthermore, ongoing research and development activities, along with strong clinical pipelines, are accelerating the introduction of innovative therapies, enhancing treatment accessibility and effectiveness across different patient populations

- The growing emphasis on personalized medicine, combined with supportive healthcare policies and reimbursement frameworks in developed regions, is further propelling the adoption of advanced melanoma treatments

- Increasing collaborations between pharmaceutical companies and research institutions are accelerating drug development and commercialization timelines in the melanoma market

- Rising healthcare expenditure and improved access to oncology care services are further supporting the uptake of advanced melanoma therapies globally

Restraint/Challenge

“High Treatment Costs and Limited Accessibility in Emerging Regions”

- The high cost associated with advanced melanoma therapies, particularly immunotherapies and targeted treatments, poses a significant challenge to widespread market adoption, especially in low- and middle-income countries

- For instance, premium-priced biologics and combination therapies often create financial burdens for patients and healthcare systems, limiting accessibility despite their clinical benefits

- Addressing these cost-related barriers requires improved pricing strategies, expanded insurance coverage, and the development of cost-effective treatment alternatives. For instance, the introduction of biosimilars and government-led reimbursement initiatives can help improve affordability and access

- In addition, disparities in healthcare infrastructure and limited access to specialized oncology care in emerging regions hinder early diagnosis and timely treatment, impacting overall patient outcomes

- While efforts are being made to expand healthcare access and reduce treatment costs, these challenges continue to restrict market growth, particularly in regions with constrained healthcare resources

- Stringent regulatory requirements and lengthy approval timelines for novel therapies can delay market entry and limit the availability of innovative treatments

- Adverse effects and variability in patient response to immunotherapies and targeted treatments can impact treatment adherence and overall clinical outcomes

Melanoma Market Scope

The market is segmented on the basis of treatment type, route of administration, end-users, and distribution channel.

- By Treatment Type

On the basis of treatment type, the melanoma market is segmented into chemotherapy, targeted therapy, immunotherapy, and others. The immunotherapy segment dominated the market with the largest market revenue share of 43.6% in 2025, driven by its superior clinical efficacy and long-term survival benefits compared to conventional treatments. Immunotherapies, particularly checkpoint inhibitors, have revolutionized melanoma treatment by enabling the immune system to recognize and attack cancer cells more effectively. These therapies are widely adopted in advanced-stage melanoma due to their durable response rates and reduced relapse risk. The growing number of regulatory approvals and expanding indications for immunotherapy drugs further strengthen their market dominance. In addition, strong physician preference and inclusion in standard treatment guidelines are contributing to the widespread use of immunotherapy. Continuous innovation and combination regimens with other therapies are also enhancing treatment outcomes and reinforcing the segment’s leadership position.

The targeted therapy segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by advancements in precision medicine and increasing adoption of biomarker-based treatments. Targeted therapies, such as BRAF and MEK inhibitors, are specifically designed for patients with genetic mutations, offering higher treatment specificity and improved outcomes. The rising use of genetic testing and companion diagnostics is enabling better patient selection, thereby boosting the effectiveness of these therapies. Pharmaceutical companies are increasingly investing in the development of next-generation targeted drugs and combination approaches to overcome resistance mechanisms. Furthermore, growing awareness among healthcare providers regarding personalized medicine is accelerating the adoption of targeted therapies. Expanding access to molecular diagnostics and increasing clinical trial activity are also supporting the rapid growth of this segment.

- By Route of Administration

On the basis of route of administration, the melanoma market is segmented into oral, parenteral, and others. The parenteral segment dominated the market with the largest revenue share in 2025, primarily due to the widespread use of injectable immunotherapies and biologics administered in clinical settings. Parenteral administration ensures rapid drug delivery and precise dosing, making it the preferred route for advanced melanoma treatments. Many leading immunotherapy drugs are administered intravenously, contributing significantly to this segment’s dominance. In addition, hospital-based treatment protocols and the need for continuous monitoring during therapy further support the reliance on parenteral routes. The increasing adoption of combination therapies involving biologics also reinforces demand for injectable formulations. Strong clinical outcomes and physician preference for controlled administration are key factors sustaining the segment’s leadership.

The oral segment is expected to witness the fastest growth rate from 2026 to 2033, driven by the increasing availability of oral targeted therapies and patient preference for convenient treatment options. Oral medications offer ease of administration, improved patient compliance, and reduced need for hospital visits, making them highly attractive for long-term therapy. Advances in drug formulation and the development of effective oral targeted agents are expanding treatment possibilities. Patients undergoing maintenance therapy or those with stable disease conditions often prefer oral regimens due to their flexibility. In addition, the shift toward outpatient care and home-based treatment models is further supporting the growth of oral therapies. The rising focus on improving quality of life for cancer patients is also accelerating the adoption of this segment.

- By End-Users

On the basis of end-users, the melanoma market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with the largest revenue share in 2025, attributed to the availability of advanced diagnostic facilities, specialized oncology departments, and skilled healthcare professionals. Hospitals serve as primary centers for melanoma diagnosis, staging, and treatment, particularly for complex and advanced cases requiring multidisciplinary care. The administration of immunotherapies and combination treatments often requires clinical supervision, further driving patient preference for hospital settings. In addition, access to clinical trials and novel therapies is more prominent in hospital environments. Strong reimbursement frameworks and infrastructure support also contribute to the dominance of this segment. The presence of integrated care pathways ensures comprehensive treatment, enhancing patient outcomes.

The specialty clinics segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing demand for specialized and personalized cancer care services. Specialty clinics offer focused expertise in oncology, enabling more efficient diagnosis and tailored treatment plans for melanoma patients. These clinics often provide quicker access to consultations and reduced waiting times compared to hospitals. The growing trend toward decentralized healthcare and outpatient oncology services is further boosting the adoption of specialty clinics. In addition, advancements in diagnostic technologies and targeted therapies are enabling clinics to manage a broader range of melanoma cases. The emphasis on patient-centric care and improved treatment experiences is also supporting the rapid growth of this segment.

- By Distribution Channel

On the basis of distribution channel, the melanoma market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the market with the largest revenue share in 2025, driven by the high volume of melanoma treatments administered in hospital settings. Many advanced therapies, particularly biologics and immunotherapies, are dispensed directly through hospital pharmacies to ensure proper handling and administration. Hospital pharmacies also play a critical role in managing complex drug regimens and ensuring patient safety. The integration of pharmacy services with clinical care allows for better monitoring of treatment outcomes and adverse effects. In addition, reimbursement policies often favor hospital-based drug dispensing, further supporting the segment’s dominance. The presence of specialized oncology pharmacists enhances the quality of care and medication management.

The online pharmacy segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by the increasing adoption of digital healthcare platforms and the growing demand for convenient medication access. Online pharmacies offer home delivery services, competitive pricing, and easy access to prescription medications, making them an attractive option for patients undergoing long-term treatment. The expansion of telemedicine and e-prescriptions is further facilitating the growth of this channel. Patients in remote or underserved areas particularly benefit from the accessibility provided by online platforms. In addition, advancements in digital infrastructure and secure payment systems are enhancing consumer trust in online pharmacies. The shift toward patient-centric healthcare delivery models is significantly contributing to the rapid expansion of this segment.

Melanoma Market Regional Analysis

- North America dominated the melanoma market with the largest revenue share of 40.8% in 2025, supported by well-established healthcare infrastructure, high awareness levels, and strong adoption of novel therapies

- Patients and healthcare providers in the region highly prioritize early diagnosis, access to cutting-edge therapies, and comprehensive cancer care supported by well-established screening programs and awareness initiatives

- This widespread adoption is further supported by favorable reimbursement policies, high healthcare expenditure, and the presence of leading pharmaceutical companies, establishing advanced melanoma treatments as a standard of care across both hospital and specialty clinic settings

U.S. Melanoma Market Insight

The U.S. melanoma market captured the largest revenue share of 81% in 2025 within North America, fueled by the high incidence of skin cancer and the rapid adoption of advanced therapies such as immunotherapies and targeted treatments. Patients and healthcare providers are increasingly prioritizing early diagnosis and access to innovative treatment options. The growing presence of leading pharmaceutical companies, combined with strong clinical research and regulatory approvals, further propels the melanoma market. Moreover, the increasing integration of precision medicine approaches, including biomarker testing and personalized therapies, is significantly contributing to the market's expansion.

Europe Melanoma Market Insight

The Europe melanoma market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of skin cancer and the rising demand for effective treatment solutions. The increase in healthcare expenditure, coupled with improved diagnostic capabilities, is fostering the adoption of advanced melanoma therapies. European patients are also drawn to the availability of innovative treatment options and structured screening programs. The region is experiencing significant growth across hospital and specialty clinic settings, with melanoma therapies being incorporated into both early-stage and advanced treatment protocols.

U.K. Melanoma Market Insight

The U.K. melanoma market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness regarding early skin cancer detection and a strong emphasis on preventive healthcare. In addition, increasing incidence rates and government-led screening initiatives are encouraging patients to seek timely treatment solutions. The country’s adoption of advanced therapies, alongside its well-established healthcare system, is expected to continue to stimulate market growth.

Germany Melanoma Market Insight

The Germany melanoma market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of oncology care and the demand for technologically advanced treatment solutions. Germany’s well-developed healthcare infrastructure, combined with its focus on innovation and research, promotes the adoption of melanoma therapies, particularly immunotherapies and targeted treatments. The integration of advanced diagnostics with treatment planning is also becoming increasingly prevalent, with a strong preference for effective, personalized care aligning with patient expectations.

Asia-Pacific Melanoma Market Insight

The Asia-Pacific melanoma market is poised to grow at the fastest CAGR of 24% during the forecast period of 2026 to 2033, driven by improving healthcare infrastructure, rising awareness, and increasing healthcare expenditure in countries such as China, Japan, and India. The region's growing focus on early diagnosis and cancer management, supported by government initiatives, is driving the adoption of melanoma treatments. Furthermore, as APAC strengthens its pharmaceutical manufacturing and clinical research capabilities, the accessibility and affordability of melanoma therapies are expanding to a wider patient population.

Japan Melanoma Market Insight

The Japan melanoma market is gaining momentum due to the country’s advanced healthcare system, aging population, and increasing focus on early cancer detection. The Japanese market places a significant emphasis on quality treatment and patient outcomes, and the adoption of melanoma therapies is driven by the rising prevalence of cancer and improved diagnostic technologies. The integration of advanced therapies with comprehensive care systems is fueling growth. Moreover, Japan's aging population is likely to spur demand for more effective and accessible melanoma treatment options in both hospital and specialized care settings.

India Melanoma Market Insight

The India melanoma market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s improving healthcare infrastructure, rising awareness of cancer, and increasing adoption of advanced treatment options. India is emerging as a key market for oncology therapies, and melanoma treatments are gaining traction across hospitals and specialty clinics. The push towards better cancer care services and the availability of cost-effective treatment options, alongside growing investments in healthcare, are key factors propelling the melanoma market in India.

Melanoma Market Share

The Melanoma industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Bristol-Myers Squibb Company (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- Amgen Inc. (U.S.)

- AstraZeneca PLC (U.K.)

- GSK plc (U.K.)

- Sanofi (France)

- Eli Lilly and Company (U.S.)

- Bayer AG (Germany)

- Takeda Pharmaceutical Company Limited (Japan)

- Boehringer Ingelheim International GmbH (Germany)

- Regeneron Pharmaceuticals, Inc. (U.S.)

- Incyte Corporation (U.S.)

- Exelixis, Inc. (U.S.)

- BeiGene, Ltd. (China)

- Daiichi Sankyo Company, Limited (Japan)

- Eisai Co., Ltd. (Japan)

- Iovance Biotherapeutics, Inc. (U.S.)

What are the Recent Developments in Global Melanoma Market?

- In February 2026, a Phase 2 clinical trial reported that neoadjuvant pembrolizumab achieved a 71% pathological complete response rate in patients with resectable desmoplastic melanoma, highlighting strong efficacy and safety outcomes. This development demonstrates the growing role of immunotherapy in early-stage melanoma treatment and supports further expansion of PD-1–based therapies in clinical practice

- In June 2025, results published in the New England Journal of Medicine showed that adding pembrolizumab to neoadjuvant and adjuvant regimens significantly improved efficacy outcomes in patients with locally advanced melanoma. This advancement reinforces the importance of combination immunotherapy strategies in improving long-term survival and disease management

- In February 2024, the U.S. Food and Drug Administration (FDA) granted accelerated approval to lifileucel (Amtagvi), the first tumor-infiltrating lymphocyte (TIL) cell therapy for patients with unresectable or metastatic melanoma. This milestone marks a major breakthrough in cell-based immunotherapy, offering a new treatment option for patients who have not responded to prior therapies

- In May 2023, findings from a clinical trial highlighted that pembrolizumab monotherapy showed strong effectiveness in treating desmoplastic melanoma, with a high response rate among patients, suggesting that single-agent immunotherapy could reduce the need for combination treatments and associated side effects. This development is reshaping treatment strategies toward more streamlined and tolerable approaches

- In December 2021, the FDA approved pembrolizumab (Keytruda) as an adjuvant treatment for stage IIB and IIC melanoma following complete surgical resection, based on improved recurrence-free survival outcomes in clinical trials. This approval expanded treatment options for earlier-stage melanoma patients and strengthened the role of immunotherapy in preventing disease recurrence

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.