Global Metastatic Cancer Drug Market

Market Size in USD Billion

CAGR :

%

USD

60.68 Billion

USD

104.25 Billion

2025

2033

USD

60.68 Billion

USD

104.25 Billion

2025

2033

| 2026 –2033 | |

| USD 60.68 Billion | |

| USD 104.25 Billion | |

| % | |

|

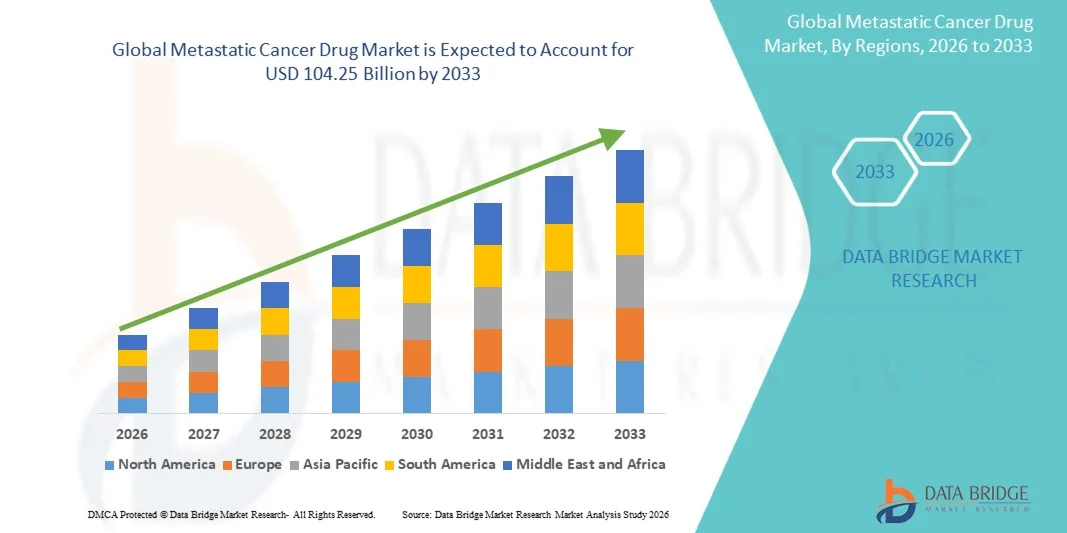

Metastatic Cancer Drug Market Size

- The global metastatic cancer drug market size was valued at USD 60.68 billion in 2025 and is expected to reach USD 104.25 billion by 2033, at a CAGR of 7.00% during the forecast period

- The market growth is largely fueled by the increasing prevalence of advanced-stage cancers, rising awareness about targeted therapies, and significant advancements in oncology drug development

- Furthermore, growing demand for personalized treatment options, coupled with technological progress in precision medicine and biologics, is establishing Metastatic Cancer Drugs as a critical solution in improving patient survival and quality of life. These converging factors are accelerating the uptake of Metastatic Cancer Drug solutions, thereby significantly boosting the industry's growth

Metastatic Cancer Drug Market Analysis

- Drugs for metastatic cancer, including targeted therapies and immuno-oncology agents, are increasingly critical in improving patient survival and quality of life in both advanced and refractory cancer cases due to their precision, efficacy, and ability to reduce systemic toxicity

- The escalating demand for metastatic cancer drugs is primarily fueled by the rising prevalence of late-stage cancers, growing awareness of personalized medicine, and the development of next-generation biologics and combination therapies

- North America dominated the metastatic cancer drug market with the largest revenue share of 42.5% in 2025, driven by advanced healthcare infrastructure, high patient awareness, strong reimbursement policies, and significant investment by key pharmaceutical companies in research and development

- Asia-Pacific is expected to be the fastest-growing region in the metastatic cancer drug market during the forecast period due to increasing cancer prevalence, expanding healthcare access, rising disposable incomes, and government initiatives supporting oncology care

- The Intravenous segment dominated the largest market revenue share of 56.2% in 2025, due to rapid bioavailability and precise dosing. Hospitals prefer IV for combination therapy regimens

Report Scope and Metastatic Cancer Drug Market Segmentation

|

Attributes |

Metastatic Cancer Drug Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

• Roche (Switzerland) |

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Metastatic Cancer Drug Market Trends

“Rising Adoption of Targeted and Personalized Therapies”

- A key trend in the global metastatic cancer drug market is the increasing shift toward targeted therapies and personalized treatment options. Advances in oncology research have enabled the development of drugs that are specifically designed for certain cancer subtypes, biomarker profiles, and patient genetic characteristics, thereby improving treatment efficacy and minimizing adverse effects

- For instance, in 2025, Pfizer introduced a biomarker-driven therapy for metastatic HER2-positive breast cancer patients, demonstrating significantly higher response rates than conventional chemotherapy. Similarly, Roche expanded its portfolio of targeted therapies for metastatic colorectal cancer by integrating KRAS mutation screening to optimize treatment outcomes

- Furthermore, combination therapies, including the pairing of immunotherapy with conventional chemotherapy, are gaining popularity to address drug resistance and late-stage metastatic progression. This approach is particularly being adopted in hospitals and specialty clinics across North America and Europe

- Another notable trend is the growing adoption of oral targeted therapies, which provide patients with the convenience of at-home treatment and improve adherence to treatment regimens. Pharmaceutical companies are increasingly investing in formulations that reduce hospitalization and frequent clinic visits

- The trend toward precision medicine is also accompanied by increased collaboration between pharmaceutical companies, research institutes, and healthcare providers to develop region-specific therapeutic solutions that address the genetic and epidemiological diversity of metastatic cancers globally

Metastatic Cancer Drug Market Dynamics

Driver

“Increasing Cancer Prevalence and Rising Healthcare Investments”

- The growing incidence of metastatic cancers worldwide, combined with higher healthcare expenditure and improved patient access to oncology care, is a major driver for the Metastatic Cancer Drug market. Governments and private healthcare institutions are prioritizing investments in advanced therapies to improve survival rates and patient quality of life

- For instance, in the U.S., the National Cancer Institute reported an increase in metastatic lung and colorectal cancer cases, driving demand for both branded and generic metastatic cancer drugs across hospitals, specialty clinics, and homecare services

- Furthermore, growing awareness of early diagnosis and treatment options is encouraging patients to seek more advanced therapeutic interventions, particularly among adult and geriatric populations. Pharmaceutical companies are actively expanding clinical trials and launching targeted therapies to meet this demand

- Another driver is the growing prevalence of companion diagnostics, which enable personalized treatment plans and enhance the effectiveness of metastatic cancer drugs. Hospitals and specialty clinics are increasingly adopting these diagnostics to optimize therapeutic outcomes

- Government initiatives, such as reimbursement schemes, patient assistance programs, and healthcare infrastructure expansion, particularly in North America and Europe, are facilitating broader adoption of advanced metastatic cancer therapies

- In addition, rising investments in oncology R&D by key pharmaceutical players are accelerating the introduction of innovative drugs, including biologics and small molecule inhibitors, which are transforming the standard of care for metastatic cancers globally

Restraint/Challenge

“High Treatment Costs and Stringent Regulatory Requirements”

- The high cost of innovative metastatic cancer drugs, coupled with complex and region-specific regulatory approval processes, poses a significant challenge to market expansion. These factors can limit patient access and delay the availability of new treatments in certain regions

- For instance, immunotherapy regimens for metastatic melanoma or advanced lung cancer can exceed tens of thousands of dollars per treatment cycle, making them unaffordable for price-sensitive patients, particularly in emerging economies

- In addition, regulatory hurdles, including extensive clinical trial requirements, stringent approval processes, and ongoing post-market surveillance mandates, can slow the introduction of novel therapies. This is particularly challenging for smaller pharmaceutical companies seeking to enter competitive markets

- Another challenge is the limited availability of healthcare infrastructure and oncology specialists in developing countries, which restricts access to advanced treatment options and limits the overall adoption of metastatic cancer drugs

- Patient adherence and compliance issues, especially for complex treatment regimens involving combination therapies or oral drugs, also impact market growth. Education and monitoring programs are necessary to ensure optimal treatment outcome

- Addressing these challenges requires strategies such as patient assistance programs, cost-reduction initiatives, faster regulatory approvals, and public-private partnerships to enhance accessibility and affordability, ensuring sustained growth of the Metastatic Cancer Drug market globally

Metastatic Cancer Drug Market Scope

The market is segmented on the basis of type, product, treatment, route of administration, dosage, end-users, and distribution channel.

• By Type

On the basis of type, the market is segmented into Prostate Cancer, Ovarian Cancer, Colorectal Cancer, Breast Cancer, Melanoma, Lung Cancer, and Others. The Prostate Cancer segment dominated the largest market revenue share of 28.6% in 2025, due to the high prevalence of prostate cancer in aging male populations and widespread adoption of targeted therapies. Hospitals and specialty clinics prefer combination treatment protocols, including chemotherapy and hormonal therapy. Early detection programs and routine screening have improved patient detection rates, supporting revenue growth. Insurance coverage and reimbursement policies reinforce adoption. Clinical evidence and physician preference maintain trust in treatment. Long-term therapy regimens provide recurring demand. Hospital pharmacies ensure steady drug supply. Patient adherence programs and monitoring improve outcomes. Supportive care enhances patient survival. R&D pipelines continue to expand indications. Government healthcare initiatives encourage broader access. The segment benefits from awareness campaigns and educational programs.

The Melanoma segment is expected to witness the fastest CAGR of 7.2% from 2026 to 2033, driven by increasing adoption of immunotherapies and checkpoint inhibitors. Rising incidence of skin cancers and growing awareness of early detection fuel market growth. Hospitals and specialty clinics integrate novel therapies into oncology care pathways. Clinical trial successes and new approvals accelerate adoption. Patient preference for targeted therapies due to reduced side effects supports expansion. Insurance coverage and reimbursement programs increase accessibility. Homecare and outpatient adoption enhance convenience. Pipeline innovations and R&D investments strengthen treatment options. Physician awareness campaigns boost adoption. Emerging markets show increased uptake. Real-world data supports efficacy and safety. Government initiatives promote early screening. Combination therapy regimens expand usage.

• By Product

On the basis of product, the market is segmented into Trastuzumab, Pertuzumab, and Trastuzumab Emtansine. The Trastuzumab segment dominated the largest market revenue share of 34.5% in 2025, supported by proven efficacy in HER2-positive metastatic cancers and widespread clinical adoption. Hospitals and specialty clinics rely on intravenous administration for precise dosing. Insurance coverage and reimbursement programs reinforce adoption. Established supply chains and hospital pharmacy integration ensure availability. Long-term therapy cycles provide recurring demand. Clinical guidelines and physician preference strengthen trust. Marketing campaigns and physician awareness improve uptake. Patient adherence programs enhance compliance. R&D pipelines for combination therapies expand indications. Specialty oncology centers manage infusion protocols. Clinical trial data support efficacy across multiple cancers. Patient education and follow-up improve outcomes.

The Pertuzumab segment is expected to witness the fastest CAGR of 6.8% from 2026 to 2033, driven by adoption in combination therapies with Trastuzumab and chemotherapy for HER2-positive cancers. Specialty clinics integrate dual HER2 blockade into standard care. Pipeline expansions and approvals increase physician confidence. Insurance coverage facilitates patient access. Clinical trials validate combination efficacy. Emerging market adoption supports growth. Homecare and outpatient administration improve convenience. Physician awareness and education campaigns drive adoption. Hospital pharmacies manage supply and adherence monitoring. Patients prefer combination therapy due to better outcomes. Adoption is supported by real-world clinical evidence. Telemedicine and remote follow-up enhance treatment continuity. Research into additional cancer indications sustains pipeline growth.

• By Treatment

On the basis of treatment, the market is segmented into Chemotherapy, Immunotherapy, Hormonal Therapy, Surgery, and Others. The Chemotherapy segment dominated the largest market revenue share of 41.7% in 2025, due to its established use as the backbone of metastatic cancer management. Hospitals administer systemic chemotherapy to control tumor progression. Physician familiarity and clinical guidelines support adoption. Insurance coverage enables patient access. Hospital pharmacy integration ensures immediate availability. Long-term therapy cycles provide recurring demand. Combination regimens maintain high prescription volumes. Advanced infusion facilities and trained oncologists reinforce efficacy. Patient adherence and outcome monitoring sustain revenue. Clinical evidence supports widespread use. Research continues to optimize dosing and reduce toxicity. Supportive care complements treatment.

The Immunotherapy segment is expected to witness the fastest CAGR of 7.5% from 2026 to 2033, driven by growing adoption of checkpoint inhibitors, CAR-T therapies, and personalized immune-oncology treatments. Hospitals and specialty clinics increasingly integrate immunotherapy into standard care. Clinical trials validate efficacy. Physician awareness campaigns support adoption. Insurance reimbursement policies improve access. Pipeline developments expand available therapies. Patient preference for targeted treatments reduces side effects. Emerging markets adopt immunotherapy programs. Homecare integration enhances adherence. Combination therapy with chemotherapy increases usage. Telemedicine supports outpatient administration. Educational campaigns improve patient awareness. Specialty clinics accelerate early-stage adoption.

• By Route of Administration

On the basis of route of administration, the market is segmented into Intravenous, Intramuscular, and Others. The Intravenous segment dominated the largest market revenue share of 56.2% in 2025, due to rapid bioavailability and precise dosing. Hospitals prefer IV for combination therapy regimens. Clinical guidelines support intravenous delivery for metastatic drugs. Hospital pharmacies ensure steady supply. Long-term therapy cycles reinforce demand. Physician familiarity improves adherence. Specialized infusion centers enable safe administration. Insurance coverage enhances accessibility. Combination therapies increase usage. Patient monitoring ensures safety. Advanced supportive care complements treatment. Clinical trials support ongoing IV adoption. Multidisciplinary teams facilitate therapy management.

The Intramuscular segment is expected to witness the fastest CAGR of 6.3% from 2026 to 2033, driven by patient-friendly formulations and outpatient adoption. IM injections reduce hospital visits and improve convenience. Specialty clinics and homecare integrate IM therapy. Clinical evidence supports efficacy. Emerging approvals expand usage. Telemedicine supports patient monitoring. Insurance coverage improves accessibility. Hospital pharmacies supply medications. Patient education encourages acceptance. Adoption grows in emerging markets. Pipeline R&D enhances therapy options. Convenience drives preference over IV therapy. Homecare services expand market reach. Multidisciplinary oversight ensures proper administration.

• By Dosage

On the basis of dosage, the market is segmented into Injection, Tablets, and Others. The Injection segment dominated the largest market revenue share of 53.4% in 2025, as injectable formulations ensure higher efficacy and compatibility with IV and IM administration. Hospitals manage dosing accuracy, adherence, and monitoring. Long-term treatment protocols maintain recurring demand. Physician trust reinforces adoption. Hospital pharmacies guarantee availability. Combination therapy increases usage. Patient safety and monitoring improve compliance. Clinical guidelines favor injections. Supportive care enhances outcomes. Research continues to optimize dosing schedules. Specialty oncology centers drive adoption. Clinical trial evidence supports treatment.

The Tablets segment is expected to witness the fastest CAGR of 6.9% from 2026 to 2033, driven by oral targeted therapies, convenience for homecare, and improved patient adherence. Outpatient clinics facilitate prescription and monitoring. Clinical evidence validates efficacy. Patient preference for non-invasive therapy supports growth. Specialty clinics adopt oral regimens. Insurance coverage improves access. Emerging markets contribute to adoption. Telemedicine integration enhances adherence. Education campaigns increase awareness. Pipeline innovations expand oral therapy options. Convenience and portability drive preference. Multidisciplinary monitoring ensures effectiveness.

• By End-Users

On the basis of end-users, the market is segmented into Hospitals, Specialty Clinics, and Others. The Hospitals segment dominated the largest market revenue share of 62.1% in 2025, supported by inpatient monitoring, centralized oncology care, and multidisciplinary treatment teams. Hospitals administer complex therapies and maintain specialized drug inventories. Clinical guidelines and physician preference reinforce adoption. Insurance coverage improves accessibility. Hospital pharmacies integrate with treatment protocols. Long-term adherence programs improve outcomes. Advanced hospital infrastructure enables infusion and monitoring. Research and clinical trials support hospital dominance. Patient follow-ups ensure therapy continuity. Specialty oncology centers reinforce leadership.

The Specialty Clinics segment is expected to witness the fastest CAGR of 7.4% from 2026 to 2033, driven by outpatient oncology services, personalized treatment plans, and early-stage intervention. Clinics integrate targeted therapies. Telemedicine supports patient adherence. Insurance coverage encourages utilization. Patient education increases adoption. Homecare integration enhances continuity. Pipeline drugs expand clinic offerings. Emerging markets drive growth. Physician awareness campaigns support use. Early detection programs increase patient throughput. Outpatient convenience improves preference. Combination therapy adoption grows. Multidisciplinary monitoring ensures safe therapy.

• By Distribution Channel

On the basis of distribution channel, the market is segmented into Hospital Pharmacy, Retail Pharmacy, and Others. The Hospital Pharmacy segment dominated the largest market revenue share of 58.7% in 2025, due to integration with treatment protocols, controlled drug dispensing, and immediate availability. Hospitals manage patient adherence and monitor therapy outcomes. Centralized pharmacy systems improve supply efficiency. Clinical guidelines favor hospital access. Long-term treatment programs sustain demand. Patient follow-up and monitoring reinforce therapy compliance. Specialty oncology centers reinforce adoption. Insurance coverage facilitates access. Multidisciplinary teams ensure proper dispensing. Clinical trials support hospital pharmacy adoption.

The Retail Pharmacy segment is expected to witness the fastest CAGR of 6.7% from 2026 to 2033, fueled by expanding pharmacy networks, patient preference for oral therapies, and homecare adoption. Retail pharmacies improve convenience and accessibility. Awareness campaigns boost adoption. Emerging markets show increased usage. Telemedicine supports remote prescription management. Insurance coverage facilitates growth. Patient education campaigns enhance compliance. Expansion of oral therapy options drives sales. Homecare preference supports segment growth. Accessibility in suburban and rural areas improves market penetration. Multidisciplinary oversight ensures proper dispensing.

Metastatic Cancer Drug Market Regional Analysis

- North America dominated the metastatic cancer drug market with the largest revenue share of 42.5% in 2025, driven by advanced healthcare infrastructure, high patient awareness, strong reimbursement policies, and significant investment by key pharmaceutical companies in research and development

- The market, pharmaceutical giants such as Pfizer, Roche, and Novartis have expanded their metastatic cancer drug portfolios with innovative targeted therapies and immunotherapies, improving patient outcomes and fostering clinical adoption

- The region’s high adoption of innovative therapies, robust oncology research, and well-established healthcare facilities are supporting widespread access to metastatic cancer treatments. Hospitals, specialty clinics, and homecare providers are increasingly utilizing oral, parenteral, and combination therapy regimens, enabling more personalized care

U.S. Metastatic Cancer Drug Market Insight

The U.S. metastatic cancer drug market accounted for the largest share within North America in 2025, driven by the high prevalence of metastatic cancers, patient access to advanced oncology care, and early adoption of novel therapies. For example, in 2025, the FDA approved multiple targeted therapies for metastatic breast and colorectal cancers, accelerating their integration into hospital and specialty clinic protocols. High R&D activity and investment by key pharmaceutical companies are leading to faster drug launches, clinical trials, and expanded indications for metastatic cancers, fueling growth across both branded and generic drug segments. In addition, the U.S. market benefits from strong healthcare reimbursement frameworks, patient assistance programs, and an increasing focus on precision medicine, allowing patients to access biomarker-guided therapies for better treatment outcomes.

Europe Metastatic Cancer Drug Market Insight

The Europe metastatic cancer drug market is projected to expand at a substantial CAGR over the forecast period, primarily driven by increasing cancer prevalence, stringent treatment guidelines, and government healthcare initiatives. For instance, Germany and France have implemented nationwide cancer screening programs and oncology funding schemes, which are improving early detection and enabling timely access to metastatic cancer therapies. Growing urbanization, the rising demand for specialized cancer care, and the integration of advanced treatment protocols in hospitals and specialty clinics are further supporting the adoption of metastatic cancer drugs. The region is also experiencing growth in multi-modal treatment strategies, combining chemotherapy, immunotherapy, and targeted therapy to optimize patient outcomes across both residential and hospital settings.

U.K. Metastatic Cancer Drug Market Insight

The U.K. metastatic cancer drug market is expected to grow steadily, driven by government support for oncology care, increased awareness among patients, and strong adoption of targeted therapies. For instance, NHS-funded programs are increasingly covering advanced metastatic cancer treatments such as PARP inhibitors for ovarian and breast cancer, enhancing accessibility for patients. The country’s well-established healthcare infrastructure and robust clinical research environment are encouraging faster adoption of innovative therapies across hospitals and specialty clinics. Patient awareness campaigns and improved insurance coverage are further driving the use of metastatic cancer drugs for both newly diagnosed and relapsed patients.

Germany Metastatic Cancer Drug Market Insight

The Germany metastatic cancer drug market is expected to expand at a considerable CAGR, fueled by high healthcare expenditure, advanced oncology infrastructure, and a focus on precision medicine. For instance, German hospitals and specialty clinics are actively adopting next-generation targeted therapies for metastatic lung and colorectal cancers, supported by reimbursement schemes and national treatment guidelines. The country’s emphasis on research, innovation, and sustainable healthcare solutions is encouraging the integration of novel therapies into standard care pathways, particularly in urban and technologically advanced regions.

Asia-Pacific Metastatic Cancer Drug Market Insight

Asia-Pacific metastatic cancer drug market is expected to be the fastest-growing region in the Metastatic Cancer Drug market during the forecast period due to increasing cancer prevalence, expanding healthcare access, rising disposable incomes, and government initiatives supporting oncology care. For instance, China, Japan, and India are witnessing government-backed programs to improve cancer diagnosis and treatment accessibility, along with investments in oncology hospitals and specialty clinics. The rising geriatric population and increasing awareness of early detection and personalized therapies are driving demand for advanced metastatic cancer drugs, including oral, injectable, and combination regimens. Furthermore, the growth of domestic pharmaceutical manufacturing in APAC is improving affordability and availability, expanding patient access to both branded and generic metastatic cancer drugs.

Japan Metastatic Cancer Drug Market Insight

The Japan Metastatic Cancer Drug market is gaining momentum due to the country’s aging population, high patient awareness, and strong focus on innovative oncology care. For instance, Japan has seen an increased adoption of immune checkpoint inhibitors and targeted therapies in hospitals and specialty clinics, particularly for lung, gastric, and colorectal cancers. The integration of advanced treatment protocols, early diagnosis initiatives, and government support for research and development is fueling growth in both adult and geriatric patient populations.

China Metastatic Cancer Drug Market Insight

The China metastatic cancer drug market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid urbanization, growing middle-class healthcare access, and high prevalence of cancer cases. For instance, national initiatives like the Healthy China 2030 plan are improving oncology infrastructure, enabling wider adoption of innovative metastatic cancer therapies in hospitals, specialty clinics, and homecare settings. The presence of strong domestic manufacturers, affordable generics, and increasing patient awareness of early detection and treatment options is further propelling market growth.

Metastatic Cancer Drug Market Share

The Metastatic Cancer Drug industry is primarily led by well-established companies, including:

• Roche (Switzerland)

• Novartis (Switzerland)

• Pfizer (U.S.)

• Merck & Co. (U.S.)

• Bristol-Myers Squibb (U.S.)

• Johnson & Johnson (U.S.)

• AstraZeneca (U.K.)

• Amgen (U.S.)

• AbbVie (U.S.)

• Takeda Pharmaceutical (Japan)

• Bayer (Germany)

• Eli Lilly and Company (U.S.)

• Sanofi (France)

• GlaxoSmithKline (U.K.)

• BeiGene (China)

• Regeneron Pharmaceuticals (U.S.)

• Daiichi Sankyo (Japan)

• Seattle Genetics (U.S.)

• Incyte Corporation (U.S.)

• Zai Lab (China)

Latest Developments in Global Metastatic Cancer Drug Market

- In December 2024, the U.S. Food and Drug Administration (FDA) approved zenocutuzumab (Bizengri) — the first systemic therapy for adults with advanced unresectable or metastatic non‑small cell lung cancer (NSCLC) or metastatic pancreatic adenocarcinoma harboring a neuregulin 1 (NRG1) gene fusion, representing a first‑in‑class targeted metastatic treatment

- In March 2025, the FDA approved pembrolizumab (Keytruda) with trastuzumab and chemotherapy for the first‑line treatment of adults with locally advanced unresectable or metastatic HER2‑positive gastric or gastroesophageal junction adenocarcinoma expressing PD‑L1 (CPS ≥1), expanding metastatic cancer treatment options

- In April 2025, the FDA approved nivolumab (Opdivo) with ipilimumab (Yervoy) for the first‑line treatment of adults with unresectable or metastatic hepatocellular carcinoma (HCC), marking an important advancement in combination immunotherapy for metastatic liver cancer

- In May 2025, the FDA approved retifanlimab‑dlwr (Zynyz) — both as a first‑line combination with carboplatin and paclitaxel and as a single agent — for adults with locally recurrent or metastatic squamous cell carcinoma of the anal canal (SCAC), providing a new metastatic treatment pathway

- In June 2025, the FDA approved taletrectinib (Ibtrozi) for adults with locally advanced or metastatic ROS1‑positive non‑small cell lung cancer (NSCLC), expanding targeted metastatic therapy for specific genetic subtypes of lung cancer

- In October 2025, the FDA expanded the indication for lurbinectedin, approving its use with atezolizumab or atezolizumab with hyaluronidase for maintenance therapy in adults with extensive‑stage small cell lung cancer (ES‑SCLC) whose disease has not progressed after first‑line treatment, broadening metastatic cancer care options

- In October 2025, the U.S. FDA approved imlunestrant (Inluriyo) for adults with ER‑positive, HER2‑negative, ESR1‑mutated advanced or metastatic breast cancer after at least one prior endocrine therapy, introducing a novel targeted oral therapy for metastatic breast cancer

- In October 2025, AstraZeneca Pharma India received regulatory approval from India’s CDSCO to market trastuzumab deruxtecan for unresectable or metastatic HER2‑positive solid tumors, marking the first antibody‑drug conjugate in India with a tumour‑agnostic indication

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.