Global Middle Ear Implants Market

Market Size in USD Million

CAGR :

%

USD

55.35 Million

USD

102.29 Million

2025

2033

USD

55.35 Million

USD

102.29 Million

2025

2033

| 2026 –2033 | |

| USD 55.35 Million | |

| USD 102.29 Million | |

| % | |

|

Middle Ear Implants Market Size

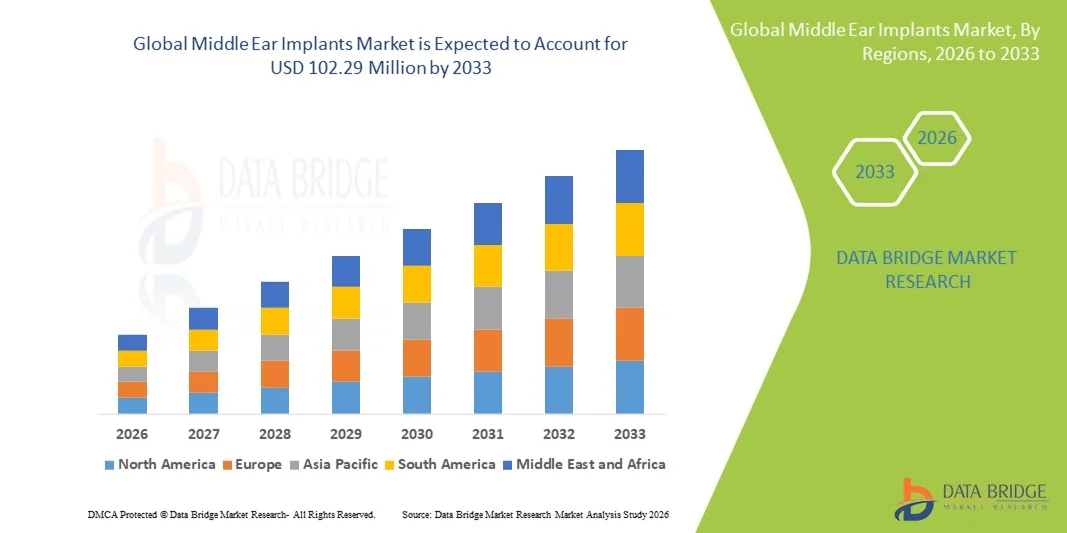

- The global middle ear implants market size was valued at USD 55.35 million in 2025 and is expected to reach USD 102.29 million by 2033, at a CAGR of 7.98% during the forecast period

- The market growth is largely fueled by the increasing prevalence of hearing disorders and hearing loss worldwide, particularly among the aging population, along with continuous technological advancements in implantable hearing devices that improve sound quality, comfort, and patient outcomes

- Furthermore, rising awareness of advanced hearing solutions over traditional aids, favorable reimbursement policies, expanding healthcare infrastructure in emerging economies, and growing demand for minimally invasive and digitally connected implants are driving adoption in both developed and developing regions. These converging factors are accelerating the uptake of middle ear implant solutions, thereby significantly boosting the industry’s growth

Middle Ear Implants Market Analysis

- Middle ear implants, providing surgical solutions to restore hearing by directly stimulating the ossicles or cochlea, are becoming increasingly vital for patients with moderate-to-severe hearing loss due to their improved sound quality, minimally invasive procedures, and compatibility with advanced digital hearing technologies

- The escalating demand for middle ear implants is primarily fueled by the growing prevalence of hearing loss worldwide, rising awareness of advanced hearing solutions over conventional hearing aids, and continuous technological advancements that enhance patient comfort and auditory outcomes

- North America dominated the middle ear implants market with the largest revenue share of 38.9% in 2025, characterized by advanced healthcare infrastructure, high per capita healthcare spending, and a strong presence of key implant manufacturers, with the U.S. experiencing substantial growth in implant procedures, particularly for cochlear and piezoelectric implants, driven by innovations in fully implantable systems and minimally invasive surgeries

- Asia-Pacific is expected to be the fastest-growing region in the middle ear implants market during the forecast period due to rising prevalence of hearing disorders, increasing healthcare access, urbanization, and growing disposable incomes in emerging economies such as China and India

- Cochlear Implants dominated the middle ear implants market with a market share of 45.2% in 2025, driven by their wide clinical applicability for sensorineural hearing loss, broad patient adoption, and continuous technological improvements that improve auditory outcomes

Report Scope and Middle Ear Implants Market Segmentation

|

Attributes |

Middle Ear Implants Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Middle Ear Implants Market Trends

Advancements in Fully Implantable and Digital Hearing Systems

- A significant and accelerating trend in the global middle ear implants market is the development of fully implantable devices and digital hearing solutions that enhance sound quality, reduce maintenance, and improve patient comfort

- For instance, Cochlear’s fully implantable system allows patients to hear without external components, offering discreet and convenient auditory restoration. Similarly, Med-El’s Vibrant Soundbridge provides seamless integration with external audio processors for improved hearing performance

- Digital signal processing in middle ear implants enables features such as adaptive frequency response, noise reduction, and personalized hearing profiles, improving patient satisfaction. For instance, Oticon Medical devices can automatically adjust sound amplification based on the surrounding environment for optimal auditory perception

- The integration of middle ear implants with smartphone apps and remote programming platforms allows audiologists to monitor patient performance and make real-time adjustments, enhancing usability and post-operative care

- Emerging AI-based algorithms in implant processors allow real-time environmental adaptation and predictive auditory enhancements, providing patients with a more natural hearing experience. For instance, some Cochlear models can detect speech in noisy environments and automatically optimize amplification

- This trend toward intelligent, customizable, and fully implantable hearing solutions is reshaping patient expectations for hearing rehabilitation. Consequently, companies such as MED-EL and Cochlear are advancing implant systems with enhanced connectivity and digital programmability

- The demand for middle ear implants offering fully implantable and digitally connected solutions is growing rapidly across both adult and pediatric populations, as patients increasingly prioritize convenience, aesthetic appeal, and improved hearing outcomes

Middle Ear Implants Market Dynamics

Driver

Rising Prevalence of Hearing Loss and Technological Advancements

- The increasing incidence of sensorineural and conductive hearing loss worldwide, coupled with ongoing innovations in implantable hearing devices, is a significant driver for the growing adoption of middle ear implants

- For instance, in March 2025, Cochlear introduced an upgraded cochlear implant system with enhanced sound processing and wireless connectivity, aiming to improve patient outcomes and usability

- As patients and healthcare providers become more aware of the limitations of conventional hearing aids, middle ear implants offer superior auditory restoration, improved speech perception, and long-term benefits, driving market growth

- Furthermore, growing access to advanced healthcare facilities and specialized audiology services is making middle ear implants more widely available, facilitating adoption in both developed and emerging markets

- Increasing government initiatives and reimbursement policies supporting advanced hearing solutions are encouraging hospitals and clinics to adopt middle ear implants. For instance, some European healthcare programs now cover implant surgeries for eligible patients

- Continuous R&D by leading manufacturers to improve device reliability, longevity, and patient comfort is expanding the implantable hearing solutions market. For instance, Med-El’s new processor reduces device replacement frequency, attracting more users

- The combination of technological improvements, expanding patient awareness, and increasing affordability is propelling the adoption of middle ear implants across hospitals, clinics, and surgical centers

Restraint/Challenge

Surgical Risks and High Cost of Advanced Devices

- Concerns regarding surgical complexity, potential complications, and the invasive nature of middle ear implant procedures pose a significant challenge to broader market adoption

- For instance, reports of post-operative infection or device failure have made some patients hesitant to opt for implant surgery over conventional hearing aids

- Addressing these concerns through minimally invasive surgical techniques, improved device reliability, and patient education is crucial for building trust and encouraging adoption

- In addition, the high cost of advanced middle ear implants, including fully implantable cochlear and bone-anchored hearing systems, can be a barrier for patients in price-sensitive or developing regions, limiting market penetration

- Lack of trained audiologists and specialized surgeons in emerging markets further restricts the adoption of middle ear implants, as proper implantation and post-operative care are critical for success

- Variations in regulatory approval processes across countries can delay product launches and market entry, affecting global expansion strategies for manufacturers

- Overcoming these challenges through surgical innovation, enhanced patient counseling, and the development of more cost-effective implant solutions will be vital for sustained growth in the middle ear implants market

Middle Ear Implants Market Scope

The market is segmented on the basis of transduction mode, product, application, and end use.

- By Transduction Mode

On the basis of transduction mode, the middle ear implants market is segmented into piezoelectric, electromagnetic, and electromechanical. The Piezoelectric segment dominated the market with the largest revenue share in 2025, driven by its high efficiency in sound transduction, reliability, and precise vibration control. Piezoelectric implants are widely preferred in clinical settings for their long-term stability and compatibility with both cochlear and middle ear implants. Surgeons favor piezoelectric devices for their minimal distortion and improved speech perception in patients with sensorineural hearing loss. The established track record of piezoelectric technology in implantable devices also makes it the preferred choice for hospitals and specialized clinics. In addition, continuous R&D has enhanced the durability and performance of piezoelectric transducers, supporting broader adoption.

The Electromagnetic segment is anticipated to witness the fastest growth from 2026 to 2033, driven by innovations in fully implantable systems and wireless connectivity. Electromagnetic transducers allow for better integration with digital processors and external audio devices, enabling adaptive sound amplification. Their growing use in bone-anchored and semi-implantable devices for diverse patient populations, including pediatric and elderly patients, supports rapid uptake. Electromagnetic implants are also gaining traction due to improvements in energy efficiency, reduced device size, and enhanced patient comfort, making them highly suitable for next-generation middle ear solutions.

- By Product

On the basis of product, the market is segmented into cochlear implants, bone-anchored hearing systems (BAHS), and auditory brainstem implants. The Cochlear Implants segment dominated the market with the largest market share of 45.2% in 2025, as these devices are widely used to treat severe to profound sensorineural hearing loss. Cochlear implants offer superior speech perception, improved auditory outcomes, and compatibility with advanced signal processing technologies. Their broad clinical acceptance, extensive post-operative support programs, and continuous innovation by companies such as Cochlear and MED-EL further drive their adoption. The devices are also preferred for both adults and children, enhancing their market dominance. The ability to integrate with smartphone apps and remote programming platforms adds convenience for patients and audiologists alike.

The Bone-Anchored Hearing Systems (BAHS) segment is expected to witness the fastest growth from 2026 to 2033, fueled by rising awareness of conductive and mixed hearing loss treatments. BAHS devices provide direct bone conduction stimulation, bypassing the middle ear, which is advantageous for patients with chronic otitis media or congenital ear malformations. Technological advancements in implant design, minimally invasive surgical procedures, and improved cosmetic appeal contribute to rapid adoption. In addition, increased reimbursement coverage and expansion into emerging markets are supporting the segment’s growth trajectory.

- By Application

On the basis of application, the market is segmented into sensorineural hearing loss, conductive hearing loss, and mixed hearing loss. The Sensorineural Hearing Loss segment dominated the market with the largest share in 2025, driven by the high global prevalence of sensorineural conditions, particularly among aging populations. Middle ear implants offer effective auditory restoration for patients with damaged hair cells or auditory nerves, improving speech recognition and quality of life. Advanced implantable technologies allow personalized sound mapping, noise reduction, and better speech perception even in noisy environments, enhancing patient satisfaction. Continuous awareness campaigns and government initiatives to support hearing rehabilitation further strengthen the adoption of implants in this patient group.

The Mixed Hearing Loss segment is expected to witness the fastest growth from 2026 to 2033, due to the increasing availability of hybrid implant solutions that can address both conductive and sensorineural deficits. Technological innovations allow simultaneous management of complex hearing impairments, which was previously challenging with conventional devices. Patients increasingly prefer these solutions for their dual functionality, non-invasiveness, and superior auditory outcomes. The growing adoption in pediatric populations with congenital malformations and expanding awareness among audiologists contribute to the rapid growth of this segment.

- By End Use

On the basis of end use, the market is segmented into hospitals & clinics, ambulatory surgical centers (ASCs), and others. The Hospitals & Clinics segment dominated the market with the largest share in 2025, as these facilities provide comprehensive surgical care, post-operative rehabilitation, and specialized audiology services required for middle ear implant procedures. Hospitals often serve as referral centers for complex cases, including cochlear and auditory brainstem implants, and possess the expertise and equipment for advanced implant surgeries. The presence of trained surgeons, rehabilitation support, and follow-up care makes hospitals the preferred choice for both adult and pediatric patients.

The Ambulatory Surgical Centers (ASCs) segment is expected to witness the fastest growth from 2026 to 2033, driven by the increasing trend of outpatient surgeries and minimally invasive implant procedures. ASCs offer cost-effective solutions, shorter recovery times, and convenience for patients, especially in regions with high patient inflow. Technological improvements in implant systems and growing insurance coverage for outpatient procedures further support the segment’s rapid adoption. Expansion of ASCs in emerging markets is also contributing to the growing preference for these facilities over traditional hospitals for implant procedures.

Middle Ear Implants Market Regional Analysis

- North America dominated the middle ear implants market with the largest revenue share of 38.9% in 2025, characterized by advanced healthcare infrastructure, high per capita healthcare spending, and a strong presence of key implant manufacturers

- Patients and healthcare providers in the region highly value the superior auditory outcomes, minimally invasive procedures, and post-operative rehabilitation support offered by middle ear implants, making them the preferred choice over conventional hearing aids

- This widespread adoption is further supported by well-established reimbursement policies, a technologically advanced medical ecosystem, and the presence of leading implant manufacturers, establishing middle ear implants as a standard solution for both adult and pediatric patients in hospitals and specialized clinics

U.S. Middle Ear Implants Market Insight

The U.S. middle ear implants market captured the largest revenue share of 82% in 2025 within North America, driven by advanced healthcare infrastructure, high awareness of hearing loss treatments, and early adoption of innovative implantable hearing devices. Patients increasingly prefer cochlear and piezoelectric implants due to their superior auditory outcomes, minimally invasive procedures, and compatibility with digital audiology platforms. The growing trend of outpatient and ambulatory surgeries, combined with the integration of fully implantable devices and remote programming apps, is further fueling market growth. In addition, government reimbursement programs and insurance coverage for implant procedures are supporting wider adoption. The U.S. continues to benefit from the presence of leading manufacturers such as Cochlear, MED-EL, and Oticon Medical, which actively introduce technological innovations to improve performance and patient comfort.

Europe Middle Ear Implants Market Insight

The Europe middle ear implants market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing awareness of hearing loss solutions, favorable reimbursement policies, and stringent healthcare quality standards. The growing prevalence of sensorineural and conductive hearing impairments, coupled with technological advancements in implant systems, is fostering adoption across hospitals and specialized clinics. European patients are also drawn to the aesthetic and functional advantages of fully implantable and digitally connected hearing devices. The region is witnessing significant growth across residential, pediatric, and geriatric applications, with implants being incorporated into both new treatment protocols and upgrades for existing hearing aid users.

U.K. Middle Ear Implants Market Insight

The U.K. middle ear implants market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by rising awareness of advanced hearing rehabilitation, increasing prevalence of hearing loss, and demand for high-quality audiology services. Concerns regarding long-term hearing deterioration encourage both adults and pediatric patients to opt for implantable solutions. The U.K.’s healthcare system, strong insurance coverage, and emphasis on patient education regarding implant options are expected to continue stimulating market growth. In addition, ongoing clinical trials and collaborations between implant manufacturers and NHS hospitals support the introduction of cutting-edge devices.

Germany Middle Ear Implants Market Insight

The Germany middle ear implants market is expected to expand at a considerable CAGR during the forecast period, fueled by technological innovation, increasing awareness of digital hearing solutions, and a growing geriatric population. Germany’s well-developed healthcare infrastructure, combined with its focus on precision medicine and rehabilitation, promotes the adoption of cochlear and bone-anchored hearing systems. Integration with tele-audiology platforms and digital programming systems is becoming increasingly prevalent, with a strong preference for reliable, minimally invasive, and patient-centric solutions. Government initiatives supporting early intervention for hearing loss further enhance market growth.

Asia-Pacific Middle Ear Implants Market Insight

The Asia-Pacific middle ear implants market is poised to grow at the fastest CAGR of 25% from 2026 to 2033, driven by rising prevalence of hearing disorders, urbanization, increasing disposable incomes, and growing access to advanced healthcare facilities in countries such as China, Japan, and India. The region’s expanding awareness of hearing rehabilitation, coupled with government initiatives promoting health technology adoption, is accelerating the uptake of middle ear implants. Furthermore, as APAC emerges as both a consumer and manufacturing hub for implantable devices, affordability and accessibility are improving, broadening the patient base.

Japan Middle Ear Implants Market Insight

The Japan middle ear implants market is gaining momentum due to the country’s advanced healthcare ecosystem, aging population, and demand for technologically sophisticated hearing solutions. Patients increasingly prefer fully implantable cochlear and piezoelectric systems for improved convenience, aesthetics, and auditory performance. Integration with remote programming and digital audiology tools is driving adoption in both residential and clinical settings. In addition, government programs supporting hearing care for elderly patients and ongoing collaborations between implant manufacturers and hospitals are further stimulating growth.

India Middle Ear Implants Market Insight

The India middle ear implants market accounted for the largest revenue share in Asia-Pacific in 2025, attributed to the country’s growing awareness of hearing loss solutions, rapid urbanization, and expanding healthcare infrastructure. India is emerging as a significant market for cochlear and bone-anchored hearing systems in both adults and pediatric populations. The push toward smart healthcare, rising affordability of implantable devices, and active presence of domestic and international manufacturers are key factors driving adoption. Increasing government and private initiatives to improve audiology services in urban and semi-urban regions are further propelling market growth.

Middle Ear Implants Market Share

The Middle Ear Implants industry is primarily led by well-established companies, including:

- Cochlear Limited (Australia)

- MED‑EL Medical Electronics (Austria)

- Sonova Holding AG (Switzerland)

- Advanced Bionics AG (Switzerland)

- Nurotron Biotechnology (China)

- Oticon Medical (Denmark)

- Envoy Medical Corporation (U.S.)

- SeboTek Hearing Systems, LLC (U.S.)

- Audina Hearing Instruments, Inc. (U.S.)

- Ototronix (U.S.)

- GN Store Nord (Denmark)

- Widex A/S (Denmark)

- Listent Medical Co., Ltd. (China)

- Rion Co., Ltd. (Japan)

- HearForm, Inc. (U.S.)

- InnerScope Hearing Technologies (U.S.)

- Advanced Sound Technologies (ASTi) (U.S.)

- Neurelec (France)

- HHTM (U.S.)

- Hearindaidssolution (U.S.)

What are the Recent Developments in Global Middle Ear Implants Market?

- In December 2025, MED‑EL’s cochlear implant became the only FDA‑approved option for children aged seven months and older with bilateral sensorineural hearing loss (SNHL), enabling earlier access to sound and critical speech development periods. This expanded pediatric indication significantly broadens access for infants previously not eligible for implant treatment

- In July 2025, Cochlear Limited announced the launch and FDA approval of its Nucleus® Nexa™ System, the first cochlear implant with upgradeable firmware, enabling recipients to access future technological improvements through implant updates rather than only via external processors. The system also features a smaller, lighter sound processor with all‑day battery life and internal memory to store a patient’s hearing settings, marking a significant innovation in implant tech

- In April 2025, MED‑EL USA presented its SONNET 3 audio processor at the American Cochlear Implant Association meeting, introducing integrated wireless connectivity, advanced audio processing, and IP68 waterproof design. This launch supports tailored solutions for conditions such as single‑sided deafness and strengthens the company’s clinical offering

- In November 2024, MED‑EL Corporation announced that the FDA approved expanded candidacy indications for its cochlear implant system, enabling adults with broader speech recognition deficits to qualify for implantation and granting the company the first FDA approval related to hearing preservation outcomes an important patient benefit indicating less residual hearing loss post‑implantation

- In July 2024, Oticon Medical announced that its Sentio™ System, an active transcutaneous bone conduction hearing implant, received U.S. FDA clearance and CE mark approval, offering the smallest transcutaneous bone conduction system available. The system enhances hearing options for individuals with conductive or mixed hearing loss without protruding abutments, improving comfort and cosmetic appeal

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.