Global Monogenic Disease Testing Market

Market Size in USD Billion

CAGR :

%

USD

3.60 Billion

USD

6.04 Billion

2025

2033

USD

3.60 Billion

USD

6.04 Billion

2025

2033

| 2026 –2033 | |

| USD 3.60 Billion | |

| USD 6.04 Billion | |

| % | |

|

Monogenic Disease Testing Market Overview

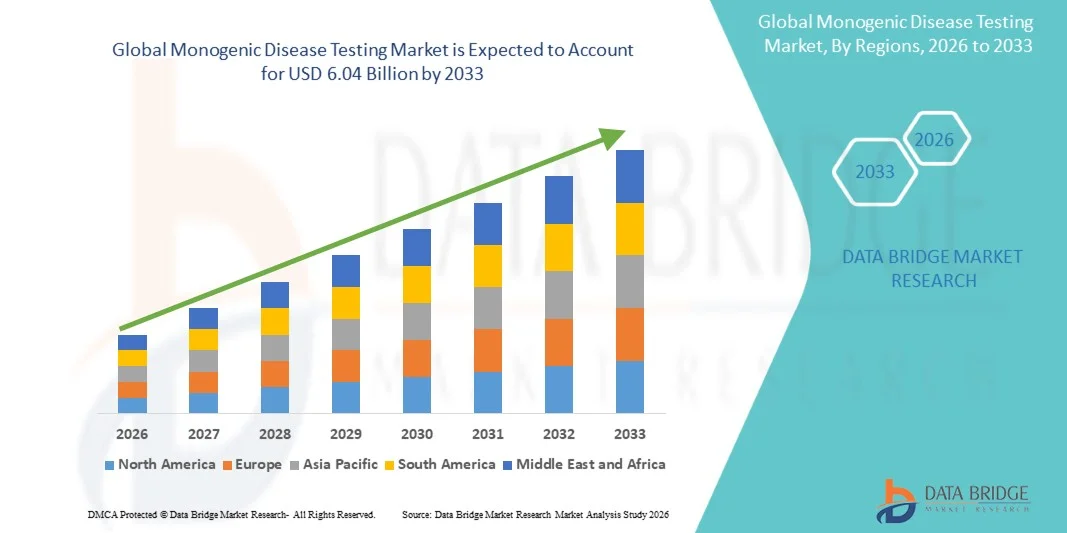

The global Monogenic Disease Testing market was valued at USD 3.60 billion in 2025 and is projected to reach USD 6.04 billion by 2033, growing at a CAGR of 6.70% from 2026 to 2033. The market is experiencing consistent growth driven by rising demand for early and accurate genetic diagnostics, rapid advancements in molecular testing technologies, and expanding applications of precision medicine across healthcare and research sectors.

The increasing prevalence of inherited genetic disorders globally, combined with growing awareness regarding preventive healthcare and newborn screening, is compelling hospitals, diagnostic laboratories, and research institutions to adopt advanced monogenic disease testing solutions. PCR-based assays, next-generation sequencing (NGS), and targeted gene panel testing technologies are increasingly replacing conventional diagnostic methods in many healthcare settings, offering faster, highly accurate, and cost-effective solutions for disease identification, carrier screening, prenatal testing, and personalized treatment planning.

Key Market Trends & Insights

- North America dominated the global Monogenic Disease Testing market with the largest revenue share of 37.24% in 2025, supported by advanced genetic testing infrastructure, high adoption of next-generation sequencing technologies, and increasing prevalence of inherited genetic disorders across the region

- The Diagnostic Testing segment led the market with a 38.67% share in 2025, driven by increasing utilization of genetic testing for early disease identification, precision medicine, and personalized treatment planning across hospitals and specialized diagnostic laboratories

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.8% from 2026 to 2033, fueled by rising healthcare expenditure, expanding newborn screening programs, and increasing awareness regarding genetic disorders across China, India, and Japan

- The Predictive and Pre-Symptomatic Testing segment is the fastest-growing test type, projected to register a CAGR of 7.5%, reflecting growing demand for early risk assessment, preventive healthcare strategies, and personalized genomic medicine

- The Familial Hypercholesterolemia segment dominates the disease type category with a 19.84% revenue share in 2025, led by increasing prevalence of inherited cardiovascular disorders and rising awareness regarding early genetic screening programs globally

- Hospitals account for 56.42% of the market, preferred for comprehensive genetic counseling, advanced diagnostic capabilities, and integration of precision medicine and molecular testing services within healthcare systems

- The Specialized Clinics segment is the fastest-growing end-use category, with a CAGR of 7.2%, driven by increasing demand for personalized genetic counseling, targeted diagnostic services, and specialized care for rare inherited disorders

- The Diagnostic Testing segment dominated the market with a share of 38.64% in 2025 due to its widespread adoption for confirming inherited genetic disorders, identifying disease-causing mutations, and supporting personalized treatment planning across hospitals and specialized genetic laboratories

Market Size & Forecast

- Global Market Value (2025): USD 3.60 Billion

- Expected Market Value (2033): USD 6.04 Billion

- Forecast CAGR (2026–2033): 6.70%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Global Monogenic Disease Testing Market Segmentation

|

Attributes |

Monogenic Disease Testing Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• F. Hoffmann-La Roche Ltd |

|

Market Opportunities |

· Increasing adoption of newborn screening and carrier testing programs across developing economies · Rising investments in precision medicine and personalized healthcare are generating strong demand for advanced monogenic disease testing solutions · The growing integration of AI-enabled genomic analysis platforms and next-generation sequencing technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Global Monogenic Disease Testing Market Trends

Trend: Rising Adoption of Precision Genetic Diagnostics and Newborn Screening Programs

Healthcare providers, diagnostic laboratories, and research institutions are increasingly adopting advanced Monogenic Disease Testing solutions to improve early disease detection, enable personalized treatment planning, and support preventive healthcare strategies. Next-generation sequencing (NGS), PCR-based assays, and targeted gene panel technologies are being widely utilized for the diagnosis of inherited disorders such as cystic fibrosis, sickle cell anemia, thalassemia, and Huntington’s disease. The growing implementation of nationwide newborn screening initiatives and carrier testing programs is significantly accelerating market demand. For instance, several countries across North America and Europe have expanded newborn genetic screening coverage to detect rare inherited disorders at early stages, improving treatment outcomes and reducing long-term healthcare costs. In addition, the integration of AI-enabled genomic analytics, cloud-based bioinformatics platforms, and automated genetic interpretation tools is enhancing testing accuracy, workflow efficiency, and clinical decision-making across precision medicine applications.

Global Monogenic Disease Testing Market Dynamics

Key Market Driver: Increasing Prevalence of Rare Genetic and Inherited Disorders

The rising global burden of inherited genetic disorders is significantly driving demand for Monogenic Disease Testing solutions worldwide. Conditions such as cystic fibrosis, sickle cell anemia, familial hypercholesterolemia, and thalassemia are witnessing increasing diagnosis rates due to growing awareness regarding genetic screening and advancements in molecular diagnostics. According to global health estimates, millions of newborns are affected annually by inherited disorders, increasing the need for early genetic testing and preventive healthcare interventions. Hospitals, specialized clinics, and diagnostic laboratories are increasingly investing in advanced genomic technologies to support accurate diagnosis, carrier screening, prenatal testing, and personalized treatment strategies. In addition, rising adoption of next-generation sequencing technologies, increasing government support for rare disease programs, and expanding precision medicine initiatives are contributing to strong market growth. The growing use of genetic testing in reproductive health, oncology, and pediatric disease management is further accelerating global adoption of monogenic disease testing solutions.

Key Restraint/Challenge: High Cost of Advanced Genetic Testing Technologies

A significant restraint in the global Monogenic Disease Testing market is the high cost associated with advanced genomic sequencing systems, bioinformatics platforms, and molecular diagnostic technologies. Modern genetic testing laboratories require substantial investment in sequencing instruments, automated sample preparation systems, specialized software, and highly trained personnel. In addition, recurring costs associated with reagents, genomic databases, data storage, quality assurance, and regulatory compliance increase the operational burden for healthcare providers and diagnostic laboratories. Smaller healthcare facilities and laboratories in developing economies often face budget constraints that limit access to advanced genetic testing infrastructure. Furthermore, the complexity of interpreting genetic variants and maintaining patient data privacy presents additional operational and regulatory challenges for market participants. The rapid expansion of precision medicine programs across developed healthcare systems highlights the increasing financial and technological requirements associated with advanced monogenic disease diagnostics.

Key Market Opportunity: Expansion of AI-Integrated Genomic Testing and Personalized Medicine

The integration of artificial intelligence and advanced bioinformatics platforms presents a significant growth opportunity for the Monogenic Disease Testing market. AI-enabled genomic analysis tools can improve mutation detection accuracy, automate variant interpretation, and accelerate clinical decision-making for inherited disease diagnosis. Increasing adoption of personalized medicine and targeted therapies is creating strong demand for comprehensive genetic testing solutions across hospitals, research institutes, and specialty clinics. In addition, expanding newborn screening initiatives, rising awareness regarding preventive healthcare, and growing investments in rare disease research across emerging economies such as China, India, Brazil, and Southeast Asia are generating substantial growth opportunities for market players. The development of cloud-connected genomic databases, portable sequencing platforms, and next-generation diagnostic technologies is further improving accessibility, efficiency, and scalability of monogenic disease testing services across global healthcare systems.

Global Monogenic Disease Testing Market Scope

The Monogenic Disease Testing market is segmented on the basis of test type, disease type, and end use.

- By Test Type

On the basis of test type, the global Monogenic Disease Testing market is segmented into carrier testing, diagnostic testing, new-born screening, predictive and pre-symptomatic testing, and prenatal testing. The Diagnostic Testing segment dominated the market with a share of 38.64% in 2025 due to its widespread adoption for confirming inherited genetic disorders, identifying disease-causing mutations, and supporting personalized treatment planning across hospitals and specialized genetic laboratories. Increasing prevalence of rare genetic disorders, growing awareness regarding early disease diagnosis, and rising utilization of next-generation sequencing (NGS) and PCR-based molecular testing technologies are significantly driving segment growth. In addition, expanding integration of AI-enabled genomic analysis platforms, automated molecular diagnostic systems, and high-throughput testing workflows is improving testing accuracy and operational efficiency. Healthcare providers are increasingly utilizing diagnostic genetic testing for conditions such as cystic fibrosis, Huntington’s disease, sickle cell anemia, and familial hypercholesterolemia. Rising government initiatives supporting early genetic screening programs and precision medicine adoption are further strengthening market demand. Furthermore, increasing investments in molecular diagnostics infrastructure, growing accessibility of genetic counseling services, and continuous advancements in bioinformatics technologies are reinforcing the dominance of the diagnostic testing segment in the global market.

The New-Born Screening segment is expected to witness the fastest CAGR of 7.6% from 2026 to 2033, driven by the increasing implementation of mandatory neonatal genetic screening programs across developed and emerging healthcare systems. Governments and healthcare organizations are expanding newborn screening initiatives to enable early detection of inherited metabolic disorders, immune deficiencies, and rare monogenic diseases before symptom onset. Advancements in multiplex PCR technologies, automated screening platforms, and rapid molecular diagnostic assays are significantly improving testing speed and sensitivity. In addition, rising awareness regarding preventive healthcare, improving healthcare infrastructure, and growing investments in pediatric genetic diagnostics are accelerating segment growth. Increasing adoption of point-of-care newborn testing devices and AI-integrated genomic analysis tools is also supporting faster and more accurate diagnosis. Countries across North America, Europe, and Asia-Pacific are expanding public health programs focused on early childhood disease detection, creating strong long-term opportunities for newborn genetic testing solutions globally.

- By Disease Type

On the basis of disease type, the global Monogenic Disease Testing market is segmented into cystic fibrosis, sickle cell anemia, severe combined immunodeficiency (SCID), Tay-Sachs disorder, polycystic kidney disorder, Gaucher's disease, Huntington's disease, neurofibromatosis, thalassaemia, and familial hypercholesterolemia. The Sickle Cell Anemia segment dominated the market with a share of 24.87% in 2025 due to the high global prevalence of hereditary blood disorders and increasing adoption of molecular diagnostic testing for early detection and disease management. Rising government initiatives for sickle cell screening, especially across Africa, the Middle East, and Asia-Pacific, are significantly contributing to market growth. Hospitals and diagnostic laboratories are increasingly adopting PCR-based assays, DNA sequencing technologies, and automated genetic testing systems to support accurate diagnosis and treatment monitoring. In addition, increasing awareness regarding inherited hematological disorders and growing investments in precision medicine programs are strengthening segment expansion. The widespread use of carrier screening and prenatal testing for sickle cell disease prevention is also driving testing volumes globally. Furthermore, advancements in CRISPR-based gene therapy research and rising clinical trials focused on genetic blood disorders are accelerating demand for advanced monogenic disease testing technologies.

The Severe Combined Immunodeficiency (SCID) segment is expected to witness the fastest CAGR of 7.8% from 2026 to 2033, driven by increasing newborn screening adoption and rising awareness regarding early immune disorder detection. Healthcare authorities worldwide are integrating SCID testing into national newborn screening panels to reduce infant mortality and improve treatment outcomes through early intervention. Advancements in molecular diagnostics, real-time PCR screening systems, and high-throughput genomic analysis technologies are enhancing detection accuracy and reducing turnaround time. In addition, increasing investments in pediatric genetic healthcare, expanding rare disease research initiatives, and growing accessibility of advanced immunological testing are supporting segment growth. The rising prevalence of inherited immune disorders and increasing clinical focus on stem cell transplantation and gene therapy are further accelerating adoption of SCID diagnostic testing globally. Emerging economies are also expanding neonatal screening infrastructure, creating significant opportunities for advanced monogenic disease testing providers.

- By End Use

On the basis of end use, the global Monogenic Disease Testing market is segmented into hospitals, ambulatory surgical centers, and specialized clinics. The Hospitals segment dominated the market with a share of 47.92% in 2025 due to the high volume of genetic diagnostic procedures, availability of advanced molecular diagnostic infrastructure, and increasing integration of precision medicine programs within hospital networks. Hospitals are extensively utilizing genetic testing platforms for diagnosis of inherited disorders, prenatal screening, oncology biomarker analysis, and neonatal disease detection. Growing adoption of automated molecular analyzers, next-generation sequencing systems, and AI-integrated laboratory information systems is significantly improving operational efficiency and diagnostic accuracy across hospital laboratories. In addition, rising healthcare expenditure, increasing prevalence of rare genetic diseases, and growing patient demand for personalized treatment solutions are supporting segment growth. Government support for genomic medicine initiatives and expansion of hospital-based genetic counseling services are further reinforcing the dominance of this segment. Furthermore, increasing collaborations between hospitals, biotechnology companies, and genomic research organizations are accelerating the implementation of advanced monogenic disease testing technologies worldwide.

The Specialized Clinics segment is expected to witness the fastest CAGR of 7.4% from 2026 to 2033, driven by the growing demand for personalized genetic counseling, targeted molecular diagnostics, and specialized rare disease management services. Specialized clinics are increasingly adopting advanced PCR-based testing systems, rapid sequencing technologies, and AI-supported genomic analysis tools to improve diagnostic precision and patient outcomes. Rising awareness regarding inherited disorders, expanding preventive healthcare initiatives, and increasing patient preference for specialized genetic care centers are accelerating market growth. In addition, the growing number of fertility clinics, prenatal diagnostic centers, and rare disease treatment facilities is increasing utilization of monogenic disease testing solutions globally. Expanding tele-genetics services and cloud-connected diagnostic platforms are also improving accessibility of specialized genetic testing in remote and underserved regions. Continuous advancements in precision medicine and personalized healthcare delivery models are expected to further support long-term growth of the specialized clinics segment.

Global Monogenic Disease Testing Market Regional Analysis

North America dominated the Monogenic Disease Testing market and accounted for the largest revenue share of 37.24% in 2025, supported by advanced genetic testing infrastructure, high adoption of next-generation sequencing (NGS) technologies, and increasing prevalence of inherited genetic disorders across the region. The region also benefits from strong healthcare expenditure, growing implementation of precision medicine programs, and rising availability of advanced molecular diagnostic laboratories. Increasing awareness regarding early genetic disease detection, expanding newborn screening initiatives, and continuous technological advancements in genomic analysis platforms are further strengthening North America’s leadership position in the global market.

U.S. Monogenic Disease Testing Market Insight

The U.S. Monogenic Disease Testing market is witnessing strong growth due to rising adoption of advanced genomic testing technologies, increasing prevalence of rare inherited disorders, and growing demand for personalized medicine solutions. The country’s highly developed healthcare infrastructure, strong presence of leading biotechnology companies, and increasing investments in molecular diagnostics research are driving market expansion. In addition, growing implementation of newborn screening programs, expanding utilization of next-generation sequencing platforms, and rising awareness regarding early disease detection are accelerating the adoption of monogenic disease testing across hospitals, specialized clinics, and research institutions.

Europe Monogenic Disease Testing Market Insight

The Europe Monogenic Disease Testing market remains a major contributor to global revenue, driven by strong government support for genetic screening programs, increasing investments in precision medicine, and growing adoption of advanced molecular diagnostic technologies. The widespread availability of genetic counseling services, rising awareness regarding inherited diseases, and increasing implementation of newborn screening initiatives are supporting market expansion across the region. In addition, advancements in genomic research, favorable healthcare policies, and expanding collaborations between research institutes and biotechnology companies continue to enhance the adoption of monogenic disease testing throughout Europe.

U.K. Monogenic Disease Testing Market Insight

The U.K. Monogenic Disease Testing market is experiencing steady growth, supported by rising investments in genomic medicine, expanding rare disease research programs, and increasing demand for early genetic disorder diagnosis. Growing implementation of national genome sequencing initiatives and increasing integration of AI-enabled diagnostic technologies are contributing to market growth. Furthermore, strong government focus on personalized healthcare, rising adoption of next-generation sequencing platforms, and increasing awareness regarding hereditary disease prevention are positioning the U.K. as a key innovation hub in the Monogenic Disease Testing industry.

Germany Monogenic Disease Testing Market Insight

The Germany Monogenic Disease Testing market is expanding steadily due to the country’s advanced healthcare infrastructure, strong biotechnology sector, and increasing adoption of precision diagnostic technologies. Hospitals, diagnostic laboratories, and research institutions are increasingly utilizing molecular genetic testing for early diagnosis of hereditary disorders and rare diseases. Continuous advancements in genomic sequencing technologies, automated molecular diagnostics, and AI-integrated laboratory systems, along with increasing government support for genetic research and personalized medicine initiatives, are further driving market growth in Germany.

Asia-Pacific Monogenic Disease Testing Market Insight

The Asia-Pacific Monogenic Disease Testing market is expected to witness rapid growth, recording the fastest CAGR of 7.8% from 2026 to 2033, driven by rising healthcare expenditure, expanding newborn screening programs, and increasing awareness regarding genetic disorders across China, India, and Japan. Growing investments in molecular diagnostic laboratories, increasing accessibility of genetic counseling services, and rising adoption of advanced genomic technologies are supporting regional market expansion. Additionally, improving healthcare infrastructure, increasing prevalence of inherited disorders, and growing government initiatives focused on early disease detection are accelerating the adoption of monogenic disease testing across the region.

Japan Monogenic Disease Testing Market Insight

The Japan Monogenic Disease Testing market is witnessing consistent growth due to rising investments in genomic medicine, advanced molecular diagnostics, and hereditary disease research. Healthcare providers and research institutes are increasingly adopting high-throughput sequencing technologies and automated genetic analysis platforms for accurate disease diagnosis and personalized treatment planning. Moreover, increasing government focus on precision healthcare, expanding newborn genetic screening programs, and rising awareness regarding rare inherited diseases are further contributing to market growth in Japan.

China Monogenic Disease Testing Market Insight

The China Monogenic Disease Testing market is growing rapidly, driven by expanding healthcare infrastructure, rising prevalence of inherited genetic disorders, and increasing government focus on genomic medicine and early disease detection. Growing adoption of next-generation sequencing technologies, AI-enabled molecular diagnostics, and automated laboratory systems across hospitals and diagnostic centers is significantly boosting market demand. In addition, rising investments in biotechnology research, expanding newborn screening initiatives, and increasing awareness regarding precision medicine are positioning China as one of the fastest-growing markets for Monogenic Disease Testing globally.

Global Monogenic Disease Testing Market Share

The Monogenic Disease Testing industry is primarily led by well-established companies, including:

- F. Hoffmann-La Roche Ltd

- Thermo Fisher Scientific Inc.

- Illumina Inc.

- QIAGEN N.V.

- Bio-Rad Laboratories Inc.

- Danaher Corporation

- Agilent Technologies Inc.

- PerkinElmer Inc.

- Abbott Laboratories

- Becton, Dickinson and Company

- Myriad Genetics Inc.

- Invitae Corporation

- Natera Inc.

- Eurofins Scientific

- Centogene N.V.

- Quest Diagnostics Incorporated

- Laboratory Corporation of America Holdings

- Exact Sciences Corporation

- SOPHiA GENETICS SA

- Guardant Health Inc.

- Fulgent Genetics Inc.

- Blueprint Genetics Oy

- Macrogen Inc.

- GeneDx Holdings Corp.

- Ambry Genetics Corporation

Latest Developments in Global Monogenic Disease Testing Market

- In March 2025, Illumina, Inc. announced expanded clinical adoption of its next-generation sequencing (NGS) platforms for rare and inherited disease testing, supporting faster and more comprehensive identification of monogenic disorders through enhanced whole-genome sequencing workflows and AI-powered variant interpretation tools

- In January 2025, F. Hoffmann-La Roche Ltd launched an upgraded digital PCR and molecular diagnostics portfolio designed to improve sensitivity and accuracy in genetic disease detection, enabling clinical laboratories to enhance testing efficiency for hereditary and rare disease applications

- In October 2024, Thermo Fisher Scientific Inc. introduced new genetic analysis solutions and automated workflow technologies for rare disease and monogenic disorder research, aimed at improving throughput, reducing turnaround times, and supporting precision medicine initiatives globally

- In June 2024, Quest Diagnostics Incorporated expanded its advanced genetic testing services for inherited disorders and carrier screening, strengthening its molecular diagnostics capabilities to support growing demand for early detection and personalized treatment planning

- In February 2024, QIAGEN N.V. announced enhancements to its QIAseq and QIAcuity digital PCR portfolio for rare disease and hereditary condition analysis, enabling highly sensitive detection of genetic mutations and supporting decentralized molecular testing laboratories

- In September 2023, Agilent Technologies, Inc. launched advanced genomic target enrichment and sequencing workflow solutions to improve the accuracy and scalability of monogenic disease research and clinical diagnostics applications

- In May 2023, Invitae Corporation expanded its inherited disease testing menu with enhanced whole-exome and carrier screening capabilities, supporting clinicians in diagnosing rare pediatric and adult-onset monogenic disorders more efficiently

- In January 2023, Bio-Rad Laboratories, Inc. introduced upgraded droplet digital PCR (ddPCR) systems for high-precision genetic mutation analysis, strengthening applications in rare disease diagnostics, oncology research, and inherited disorder testing

- In August 2022, PerkinElmer, Inc. expanded its newborn screening and genetic testing portfolio through advanced molecular diagnostic solutions focused on early identification of monogenic and metabolic disorders in infants

- In April 2022, Centogene N.V. announced strategic collaborations to accelerate rare disease diagnostics and genomic data analysis using AI-enabled bioinformatics platforms, supporting improved detection of inherited monogenic disorders globally

- In November 2021, Myriad Genetics, Inc. launched enhanced hereditary disease screening panels utilizing next-generation sequencing and advanced analytics technologies to improve detection accuracy for inherited genetic conditions and rare monogenic disorders

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.