Global Mucus Clearance Device Market

Market Size in USD Billion

CAGR :

%

USD

4.58 Billion

USD

7.29 Billion

2025

2033

USD

4.58 Billion

USD

7.29 Billion

2025

2033

| 2026 –2033 | |

| USD 4.58 Billion | |

| USD 7.29 Billion | |

| % | |

|

Mucus Clearance Device Market Overview

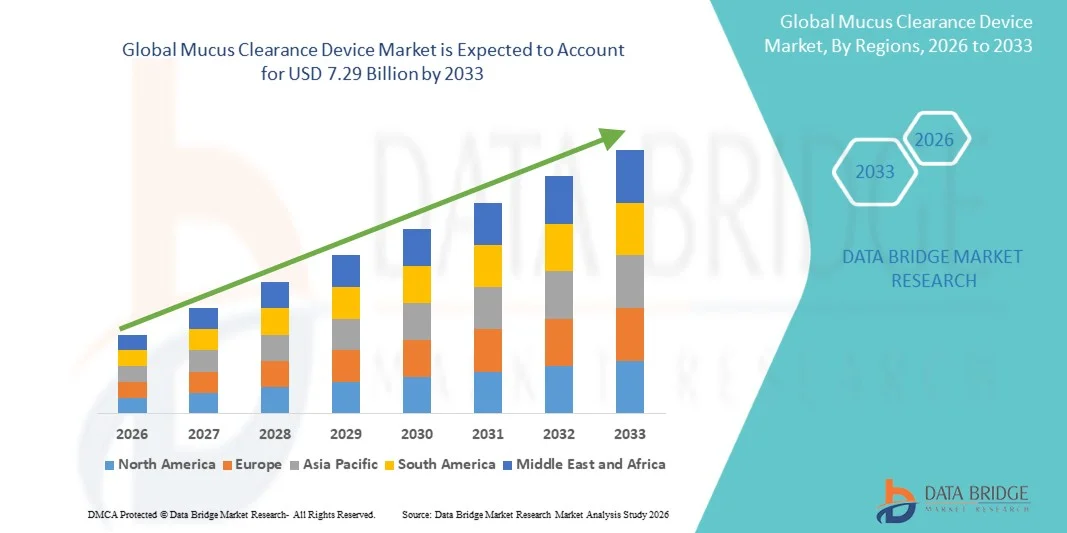

The Mucus Clearance Device Market was valued at USD 4.58 billion in 2025 and is projected to reach USD 7.29 billion by 2033, growing at a CAGR of 6.00% from 2026 to 2033 The market is experiencing consistent growth driven by rising prevalence of respiratory disorders such as chronic obstructive pulmonary disease (COPD), cystic fibrosis, asthma, and bronchiectasis, along with increasing demand for effective airway clearance and pulmonary hygiene solutions. Advancements in device design, including oscillatory positive expiratory pressure (OPEP) devices, high-frequency chest wall oscillation (HFCWO) systems, and mechanical insufflation-exsufflation devices, are significantly improving mucus clearance efficiency and patient comfort. Growing awareness of respiratory care management and expanding use of home healthcare solutions are further accelerating market adoption across both clinical and non-clinical settings.

The increasing burden of chronic respiratory diseases globally, combined with rising hospitalizations and post-operative pulmonary complications, is compelling hospitals, rehabilitation centers, and home care providers to adopt advanced mucus clearance technologies. These devices are increasingly being used to reduce airway obstruction, improve lung function, and lower the risk of respiratory infections. In addition, the shift toward portable, user-friendly, and non-invasive airway clearance devices is replacing traditional physiotherapy methods in many markets, offering cost-effective, convenient, and long-term respiratory management solutions for patients across developed and emerging regions.

Key Market Trends & Insights

- North America dominated the Mucus Clearance Device Market with the largest revenue share of 38.47% in 2025, supported by advanced respiratory care infrastructure, high prevalence of chronic respiratory diseases, and strong adoption of home healthcare and hospital-based airway clearance therapies. The region also benefits from well-established reimbursement frameworks, increasing awareness of pulmonary rehabilitation, and widespread availability of advanced mucus clearance technologies across hospitals, specialty clinics, and homecare settings. Growing demand for non-invasive respiratory support and portable airway clearance devices continues to strengthen North America’s leadership position in the global market.

- HFCWO Devices segment led the market with a 42.18% share in 2025, driven by strong clinical adoption in cystic fibrosis, COPD, and bronchiectasis management. These devices are widely used in hospital and homecare settings due to their proven effectiveness in mobilizing airway secretions and improving lung function. Increasing preference for high-frequency chest wall oscillation systems in long-term respiratory care and post-operative pulmonary therapy is further reinforcing segment dominance across developed healthcare markets.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 8.41% from 2026 to 2033, fueled by rising prevalence of chronic respiratory disorders, expanding healthcare infrastructure, and increasing healthcare expenditure across China, India, and Japan. Growing awareness of respiratory care management, improving access to advanced airway clearance devices, and rapid expansion of home healthcare services are further supporting regional market growth. In addition, rising air pollution levels and increasing hospital admissions for respiratory conditions are accelerating demand for mucus clearance solutions across emerging economies.

- OPEP Devices segment is expected to be the fastest-growing cycle type with a CAGR of 7.93% from 2026 to 2033, driven by their portability, affordability, and ease of use in both clinical and homecare environments. These devices are increasingly preferred for self-administered airway clearance therapy, especially among COPD and bronchiectasis patients. Growing adoption of patient-centric respiratory care solutions and increasing emphasis on reducing hospital dependency are further boosting demand for OPEP-based mucus clearance technologies globally.

- COPD indication segment dominated the market with a 39.62% revenue share in 2025, driven by the high global burden of chronic obstructive pulmonary disease and its strong association with mucus retention and airway obstruction. Increasing smoking prevalence, aging population, and rising exposure to environmental pollutants are contributing to higher COPD incidence rates worldwide. Continuous need for long-term respiratory management and frequent use of mucus clearance devices for symptom control are reinforcing segment leadership.

- Bronchiectasis segment is expected to be the fastest-growing indication with a CAGR of 8.12% from 2026 to 2033, driven by increasing diagnosis rates, improved imaging techniques, and rising awareness of chronic airway diseases. Patients with bronchiectasis require consistent airway clearance therapy, leading to higher adoption of advanced mucus clearance devices. Expanding access to specialized respiratory care and growing use of home-based treatment solutions are further accelerating segment growth.

- Hospitals segment dominated the end-user category with a 46.35% share in 2025, supported by high patient inflow, availability of advanced respiratory care equipment, and strong presence of trained healthcare professionals. Hospitals remain the primary setting for acute respiratory treatment, post-surgical recovery, and severe COPD management. Increasing integration of mucus clearance devices into pulmonary rehabilitation programs is further strengthening hospital dominance.

- The COPD segment dominated the market with a 42.37% revenue share in 2025, supported by the high global prevalence of chronic obstructive pulmonary disease and increasing need for long-term respiratory management solutions.

Market Size & Forecast

- Global Market Value (2025): USD 4.58 Billion

- Expected Market Value (2033): USD 7.29 Billion

- Forecast CAGR (2026–2033): 6.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Mucus Clearance Device Market Segmentation

|

Attributes |

Mucus Clearance Device Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Koninklijke Philips N.V. (Netherlands) |

|

Market Opportunities |

· Rising Adoption of Home-Based Respiratory Care Solutions · Increasing Burden of Chronic Respiratory Diseases and Aging Population · Technological Advancements and Integration of Smart Respiratory Devices |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Mucus Clearance Device Market Trends

Trend: Rising Adoption of Smart and Home-Based Respiratory Care Solutions

Patients and healthcare providers are increasingly adopting mucus clearance devices in homecare settings to improve long-term management of chronic respiratory diseases such as COPD, cystic fibrosis, and bronchiectasis. The integration of portable HFCWO and OPEP devices with digital monitoring systems is enabling better treatment adherence and reducing hospital dependency. Smart airway clearance devices equipped with Bluetooth connectivity and mobile app tracking are allowing physicians to monitor therapy outcomes remotely. For instance, companies like Koninklijke Philips N.V. and ResMed Inc. have expanded their respiratory care portfolios with connected airway clearance and ventilation support systems designed for home-based chronic disease management. Growing preference for outpatient care and aging-in-place healthcare models is significantly driving adoption across North America and Europe.

Mucus Clearance Device Market Dynamics

Key Market Driver: Rising Prevalence of Chronic Respiratory Diseases and Growing Geriatric Population

The increasing global burden of chronic respiratory conditions such as COPD, bronchiectasis, and cystic fibrosis is a major factor driving demand for mucus clearance devices. According to the World Health Organization (WHO), COPD alone affects hundreds of millions globally and remains a leading cause of morbidity and mortality. Aging populations, particularly in developed regions, are more vulnerable to reduced lung function and airway clearance complications, further increasing device adoption. Hospitals, rehabilitation centers, and homecare providers are increasingly using HFCWO, IPV, and PEP devices to improve lung function, reduce hospitalization rates, and enhance patient outcomes. In addition, rising awareness of early intervention in respiratory care is expanding diagnostic and treatment rates globally, especially across North America and Europe.

Key Restraint/Challenge: High Device Cost and Limited Accessibility in Emerging Markets

A significant challenge in the mucus clearance device market is the high cost of advanced airway clearance systems, including HFCWO vests, mechanical insufflation-exsufflation devices, and oscillatory positive expiratory pressure systems. The cost of devices, along with recurring expenses for accessories and maintenance, limits adoption in low- and middle-income regions. In addition, limited reimbursement coverage in several developing countries restricts patient access to advanced respiratory therapies. For example, full chest physiotherapy systems can require substantial investment, making them less accessible for smaller hospitals and homecare users. Furthermore, lack of awareness regarding airway clearance therapy and limited availability of trained respiratory therapists in rural areas continue to hinder widespread adoption.

Key Market Opportunity: Integration of Digital Health, Telemonitoring, and AI-Enabled Respiratory Therapy

The integration of digital health technologies into mucus clearance devices is creating strong growth opportunities in the global market. AI-enabled respiratory monitoring systems, cloud-based patient tracking platforms, and smart airway clearance devices are improving treatment efficiency and patient compliance. Companies are increasingly focusing on connected respiratory ecosystems that allow real-time data sharing between patients and healthcare providers. For instance, newer-generation devices from companies such as Baxter International Inc. and Philips include remote monitoring capabilities and data-driven therapy adjustments. In addition, the expansion of telehealth services and hospital-at-home programs is accelerating adoption of portable mucus clearance devices, particularly in North America and rapidly developing healthcare markets in Asia-Pacific.

Mucus Clearance Device Market Scope

The Mucus Clearance Device market is segmented on the basis of cycle type, indication, and end-user.

By Cycle Type

On the basis of cycle type, the Mucus Clearance Device Market is segmented into HFCWO Devices, OPEP Devices, MCA Devices, IPV Devices, and PEP Devices. The HFCWO Devices segment dominated the market with a 38.92% revenue share in 2025, driven by strong clinical adoption across chronic respiratory disease management, particularly in COPD, cystic fibrosis, and bronchiectasis care. These devices are widely used in hospitals, rehabilitation centers, and homecare settings due to their proven ability to enhance mucus clearance, improve lung function, and reduce hospitalization rates. Increasing physician preference for non-invasive, long-term airway clearance solutions and strong clinical guidelines supporting chest physiotherapy are further reinforcing segment dominance. High patient compliance and ease of home-use also contribute to sustained demand.

The IPV Devices segment is expected to witness the fastest growth at a CAGR of 8.1% from 2026 to 2033. This growth is driven by rising demand for advanced airway clearance solutions in intensive care units and emergency respiratory care settings. Increasing prevalence of severe pulmonary infections, post-operative complications, and ventilator-associated respiratory issues is significantly boosting adoption. Hospitals are increasingly integrating IPV systems with ventilatory support to improve mucus mobilization and oxygenation efficiency. Technological advancements in pressure-controlled and automated therapy systems are enhancing treatment precision and patient outcomes. Growing ICU admissions globally and expanding critical care infrastructure in emerging economies are further accelerating demand. Rising clinical preference for multifunctional respiratory support devices is strengthening market penetration. Expanding awareness among healthcare professionals regarding early intervention in severe respiratory conditions is also supporting growth. Increased healthcare spending and improved access to critical care technologies are expected to further drive segment expansion.

By Indication

On the basis of indication, the Mucus Clearance Device Market is segmented into Cystic Fibrosis, COPD, Bronchiectasis, and Others. The COPD segment dominated the market with a 42.37% revenue share in 2025, supported by the high global prevalence of chronic obstructive pulmonary disease and increasing need for long-term respiratory management solutions. Rising smoking rates, aging populations, and worsening air pollution levels are significantly contributing to disease burden worldwide. Hospitals and homecare providers are increasingly adopting mucus clearance devices to reduce exacerbations, improve oxygenation, and enhance patient quality of life. Strong awareness of early disease management and increasing diagnosis rates in developed regions further support growth.

The Bronchiectasis segment is expected to witness the fastest growth at a CAGR of 7.9% from 2026 to 2033. This growth is driven by rising disease detection through advanced imaging techniques such as high-resolution CT scans, leading to improved diagnosis rates globally. Increasing awareness among clinicians regarding long-term airway clearance therapy is boosting adoption of mucus clearance devices. Expanding respiratory care infrastructure in emerging markets is improving access to treatment. The chronic and progressive nature of bronchiectasis requires continuous airway clearance, supporting sustained device usage. Growing geriatric population and increasing comorbid respiratory conditions are further accelerating demand. Rising hospital admissions and pulmonary rehabilitation programs are contributing to segment expansion. Improved reimbursement policies in developed regions are also supporting adoption.

By End-User

On the basis of end-user, the Mucus Clearance Device Market is segmented into Direct/Patient, Hospitals, and Fertility Clinics and IVF Centres. The Hospitals segment dominated the market with a 46.58% revenue share in 2025, attributed to high patient inflow, availability of advanced respiratory care infrastructure, and widespread use of airway clearance devices in ICU, pulmonary care, and rehabilitation departments. Hospitals remain the primary point of care for acute and chronic respiratory conditions, ensuring consistent demand for HFCWO, IPV, and PEP devices. Increasing integration of respiratory therapy protocols in critical care units and strong reimbursement frameworks in developed regions further strengthen dominance.

The Direct/Patient segment is expected to witness the fastest growth at a CAGR of 8.4% from 2026 to 2033. This growth is driven by the rapid expansion of home healthcare services and increasing preference for self-managed chronic respiratory care. Rising availability of portable and user-friendly mucus clearance devices is enabling wider adoption among patients. Growing aging population and increasing prevalence of long-term respiratory diseases are further supporting demand. Expansion of telehealth platforms and remote patient monitoring systems is improving treatment adherence and clinical outcomes. Increasing healthcare awareness among patients is encouraging early adoption of airway clearance therapy. Lower hospital dependency and cost-effective home treatment options are accelerating market penetration. Technological advancements in compact, battery-operated devices are further enhancing usability and growth potential.

Mucus Clearance Device Market Regional Analysis

North America dominated the Mucus Clearance Device market and accounted for the largest revenue share of 38.47% in 2025, supported by advanced respiratory care infrastructure, high prevalence of chronic respiratory diseases, and strong adoption of hospital-based and home healthcare airway clearance therapies. The region benefits from well-established reimbursement frameworks that improve patient access to advanced treatment options, along with strong clinical adoption across hospitals, specialty respiratory clinics, and homecare settings. Increasing awareness regarding pulmonary rehabilitation and long-term respiratory disease management is further accelerating demand across healthcare systems. The widespread availability of advanced mucus clearance technologies such as HFCWO and OPEP devices is supporting clinical adoption. Growing preference for non-invasive respiratory therapies is improving patient compliance and treatment outcomes. Strong presence of leading medical device manufacturers is enhancing product innovation and accessibility. Rising hospitalization rates for COPD and bronchiectasis are contributing to consistent device utilization. Expansion of home healthcare services is further boosting demand for portable mucus clearance systems. Increasing geriatric population across the U.S. and Canada is significantly driving long-term care requirements. Technological advancements in wearable and battery-operated devices are improving mobility and ease of use. Integration of smart monitoring features is enhancing therapy effectiveness and patient adherence. Overall, strong healthcare infrastructure and clinical awareness continue to reinforce North America’s leadership position in the global market.

U.S. Mucus Clearance Device Market Insight

The U.S. Mucus Clearance Device market is witnessing strong growth due to rising prevalence of chronic respiratory conditions such as COPD, asthma, and bronchiectasis, along with increasing adoption of home-based respiratory care solutions. The country’s advanced healthcare ecosystem, supported by strong insurance coverage and reimbursement policies, is enabling wider access to mucus clearance therapies. Hospitals and respiratory care centers are increasingly integrating high-frequency chest wall oscillation (HFCWO) and oscillatory positive expiratory pressure (OPEP) devices into treatment protocols. Growing emphasis on reducing hospital readmissions is further encouraging home-based airway clearance adoption. Rising awareness of pulmonary rehabilitation programs is improving patient compliance and long-term outcomes. Strong presence of key manufacturers such as Baxter and Hill-Rom (now part of Baxter) is driving product innovation. Increasing geriatric population is contributing to higher demand for long-term respiratory care solutions. Expanding telehealth and remote monitoring integration is enhancing therapy management. Clinical adoption is also rising in post-acute care and rehabilitation centers. Technological advancements in portable and wearable devices are improving patient convenience. Growing healthcare expenditure is supporting adoption of advanced respiratory care technologies. Overall, strong clinical infrastructure continues to support sustained market expansion in the U.S.

Europe Mucus Clearance Device Market Insight

The Europe Mucus Clearance Device market remains a major contributor to global revenue, driven by strong healthcare systems, high awareness of respiratory diseases, and increasing adoption of advanced airway clearance technologies. The region benefits from supportive regulatory frameworks and reimbursement policies that facilitate access to respiratory care devices. Hospitals and specialty clinics across Germany, France, and the U.K. are widely adopting mucus clearance solutions for chronic respiratory disease management. Rising prevalence of COPD and cystic fibrosis is significantly driving demand across patient populations. Increasing focus on non-invasive respiratory therapies is supporting clinical adoption. Strong presence of leading manufacturers and R&D centers is enhancing product innovation. Growing geriatric population is increasing long-term care requirements. Expansion of home healthcare services is boosting adoption of portable devices. Integration of digital health technologies is improving treatment monitoring and patient adherence. Rising investments in pulmonary rehabilitation programs are strengthening clinical outcomes. Awareness campaigns by healthcare organizations are improving diagnosis and treatment rates. Overall, strong healthcare infrastructure and policy support continue to sustain Europe’s significant market share.

U.K. Mucus Clearance Device Market Insight

The U.K. Mucus Clearance Device market is experiencing steady growth, supported by increasing prevalence of chronic respiratory diseases and strong adoption of NHS-backed pulmonary care programs. Hospitals and community healthcare providers are increasingly using airway clearance devices to manage COPD and bronchiectasis patients. Rising focus on reducing hospital admissions and improving at-home care is driving demand for portable mucus clearance solutions. Growing integration of respiratory rehabilitation programs is enhancing patient outcomes. The presence of well-structured reimbursement systems is supporting wider device accessibility. Increasing adoption of OPEP and HFCWO devices is improving treatment effectiveness. Technological advancements in wearable respiratory devices are enhancing patient mobility. Expansion of home healthcare services is contributing to market growth. Rising awareness of early diagnosis and disease management is improving therapy adoption rates. Strong collaboration between healthcare providers and medical device companies is accelerating innovation. Increasing elderly population is further supporting demand for long-term respiratory care. Overall, the U.K. continues to emerge as a key innovation-driven market in Europe.

Germany Mucus Clearance Device Market Insight

The Germany Mucus Clearance Device market is expanding steadily due to strong healthcare infrastructure, high prevalence of chronic respiratory conditions, and increasing focus on advanced respiratory care solutions. Hospitals and rehabilitation centers are widely adopting mucus clearance devices for COPD and bronchiectasis management. The country’s strong medical device manufacturing base is supporting continuous innovation in airway clearance technologies. Rising awareness of pulmonary rehabilitation is driving higher adoption rates among patients. Increasing elderly population is contributing to long-term care demand. Strong insurance coverage and reimbursement support are improving patient access to therapies. Adoption of HFCWO and OPEP devices is growing across clinical settings. Expansion of home-based respiratory care is further boosting market penetration. Integration of digital monitoring systems is improving treatment compliance. Germany’s focus on clinical research is accelerating product development and validation. Increasing hospital investments in respiratory care units are strengthening adoption. Overall, strong healthcare standards and innovation ecosystem are driving sustained market growth.

Asia-Pacific Mucus Clearance Device Market Insight

The Asia-Pacific Mucus Clearance Device market is expected to witness rapid growth, recording a CAGR of 8.41% from 2026 to 2033, driven by rising prevalence of chronic respiratory diseases, expanding healthcare infrastructure, and increasing healthcare expenditure across emerging economies. Growing urbanization and rising air pollution levels are significantly increasing respiratory disease burden in countries such as China and India. Improving access to advanced healthcare facilities is supporting adoption of mucus clearance devices. Expansion of home healthcare services is further accelerating demand for portable airway clearance solutions. Rising awareness regarding respiratory disease management is improving diagnosis and treatment rates. Increasing hospital admissions for COPD and bronchiectasis are boosting device utilization. Government initiatives to strengthen respiratory care infrastructure are supporting market expansion. Growing medical tourism industry is also contributing to advanced therapy adoption. Presence of local manufacturers is improving affordability and accessibility. Rapid digital healthcare adoption is enhancing treatment monitoring and patient compliance. Increasing elderly population is further driving long-term care demand. Overall, Asia-Pacific is emerging as the fastest-growing regional market globally.

Japan Mucus Clearance Device Market Insight

The Japan Mucus Clearance Device market is witnessing steady growth due to increasing prevalence of respiratory diseases and strong healthcare system integration. Hospitals and rehabilitation centers are increasingly adopting advanced airway clearance technologies for COPD and bronchiectasis management. The country’s aging population is significantly driving demand for long-term respiratory care solutions. Strong focus on preventive healthcare and early disease management is improving device adoption rates. Increasing use of OPEP and HFCWO devices is enhancing clinical outcomes. Technological innovation in compact and portable devices is supporting homecare adoption. Integration of digital monitoring systems is improving therapy adherence. Strong healthcare funding and insurance coverage are supporting accessibility. Rising awareness of pulmonary rehabilitation programs is improving patient outcomes. Expansion of outpatient respiratory care services is contributing to market growth. Collaboration between medical device companies and healthcare institutions is fostering innovation. Overall, Japan’s advanced healthcare ecosystem is supporting consistent market expansion.

China Mucus Clearance Device Market Insight

The China Mucus Clearance Device market is growing rapidly, driven by rising prevalence of chronic respiratory diseases, increasing air pollution levels, and expanding healthcare infrastructure. Government focus on improving respiratory health awareness is supporting early diagnosis and treatment adoption. Hospitals are increasingly integrating mucus clearance devices into respiratory care protocols for COPD and bronchiectasis patients. Expanding home healthcare services are significantly boosting demand for portable airway clearance solutions. Rising healthcare expenditure is improving access to advanced respiratory therapies. Increasing urbanization and industrial pollution are contributing to higher disease burden. Growing adoption of OPEP and HFCWO devices is enhancing treatment effectiveness. Local manufacturing capabilities are improving affordability and availability of devices. Rapid expansion of hospital infrastructure is supporting clinical adoption. Increasing medical insurance coverage is improving patient access to therapies. Rising investments in respiratory care R&D are driving innovation. Overall, China is emerging as one of the fastest-growing markets globally for mucus clearance devices.

Mucus Clearance Device Market Share

The Mucus Clearance Device industry is primarily led by well-established companies, including:

- Koninklijke Philips N.V. (Netherlands)

- Hill-Rom Holdings, Inc. (U.S.)

- Baxter International Inc. (U.S.)

- Electromed, Inc. (U.S.)

- Monaghan Medical Corporation (U.S.)

- General Physiotherapy, Inc. (U.S.)

- Thayer Medical Corporation (U.S.)

- MGC Diagnostics Corporation (U.S.)

- Pari Medical Holding GmbH (Germany)

- Smiths Medical (U.S.)

- Vyaire Medical, Inc. (U.S.)

- Trudell Medical International (Canada)

- ResMed Inc. (U.S.)

- Allied Healthcare Products, Inc. (U.S.)

- Medline Industries, LP (U.S.)

- Dr. Trust (Nureca Ltd.) (India)

- CareFusion Corporation (U.S.)

- DeVilbiss Healthcare LLC (U.S.)

- Becton, Dickinson and Company (BD) (U.S.)

- Inogen, Inc. (U.S.)

- Aseptico, Inc. (U.S.)

- GCE Group (Sweden)

- Flexicare Medical Limited (U.K.)

- Hamilton Medical AG (Switzerland)

- Fukuda Denshi Co., Ltd. (Japan)

- Yuwell Medical Equipment & Supply Co., Ltd. (China)

- BPL Medical Technologies (India)

- Schiller AG (Switzerland)

- Drive DeVilbiss Healthcare (U.S.)

- Apex Medical Corp. (Taiwan)

- Sunrise Medical (Germany)

- Allied Medical Ltd. (New Zealand)

- ICU Medical, Inc. (U.S.)

Latest Developments in Mucus Clearance Device Market

- In March 2021, Electromed Inc. (U.S.), a leading airway clearance device manufacturer, expanded commercialization of its SmartVest Oscillatory Positive Expiratory Pressure (OPEP) system, strengthening its position in home-based high-frequency chest wall oscillation (HFCWO) therapy. The system is designed to improve airway clearance in patients with cystic fibrosis and COPD, reflecting growing demand for portable and homecare respiratory devices. This expansion highlights the increasing shift toward non-invasive, patient-centric respiratory therapy solutions

- In June 2022, Hillrom (now part of Baxter International Inc.) advanced its respiratory care portfolio by expanding adoption of its Vest Airway Clearance System across hospital and homecare settings, supporting chronic respiratory disease management. The system delivers high-frequency chest wall oscillation therapy to help mobilize mucus in patients with COPD, bronchiectasis, and neuromuscular disorders, reinforcing the trend toward hospital-to-home respiratory care transition. This development underscores increasing integration of airway clearance devices into long-term care pathways

- In September 2023, Koninklijke Philips N.V. (Netherlands) continued development of connected respiratory care solutions by enhancing digital health integration across airway clearance and respiratory therapy devices. These solutions aim to improve patient adherence through remote monitoring and data-driven respiratory management, supporting the broader shift toward smart, connected home healthcare systems. This development reflects the growing role of digital health in improving outcomes for chronic respiratory disease patients

- In February 2024, Baxter International Inc. expanded its respiratory care offerings following the continued integration of Hillrom’s airway clearance technologies, strengthening its portfolio in hospital-based and home-based mucus clearance therapies. The expansion focuses on improving clinical efficiency in treating COPD and cystic fibrosis patients using high-frequency chest wall oscillation systems. This move reflects consolidation trends in respiratory care device manufacturing and rising demand for advanced airway clearance technologies

- In May 2025, Monaghan Medical Corporation (U.S.), a key player in respiratory therapy devices, continued expansion of its Aerobika Oscillating Positive Expiratory Pressure (OPEP) device adoption in chronic respiratory disease management. The device is widely used for mucus mobilization in COPD and bronchiectasis patients and is increasingly incorporated into hospital discharge and homecare programs. This development reflects sustained growth in low-cost, effective OPEP-based airway clearance solutions

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.