Global Myelodysplastic Syndromes Market

Market Size in USD Billion

CAGR :

%

USD

3.60 Billion

USD

6.11 Billion

2025

2033

USD

3.60 Billion

USD

6.11 Billion

2025

2033

| 2026 –2033 | |

| USD 3.60 Billion | |

| USD 6.11 Billion | |

| % | |

|

Myelodysplastic Syndromes (MDS) Market Size

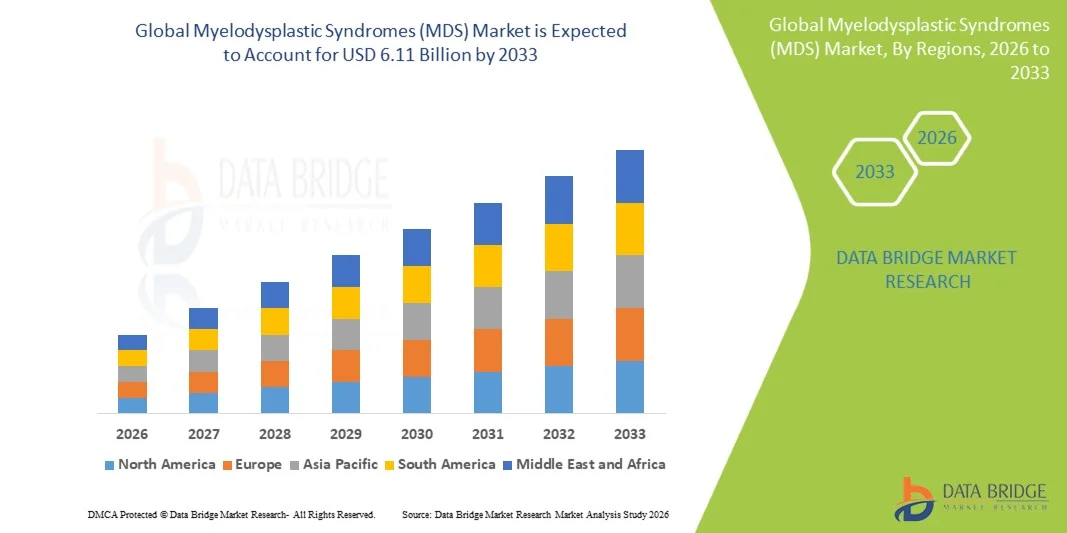

- The global Myelodysplastic Syndromes (MDS) market size was valued at USD 3.60 billion in 2025and is expected to reach USD 6.11 billion by 2033, at a CAGR of6.85% during the forecast period

- The market growth is largely fueled by the increasing prevalence of MDS particularly among the rapidly growing global geriatric population, accelerating FDA approvals of novel targeted therapies including imetelstat and luspatercept that are transforming lower-risk MDS management, and rising awareness of the syndrome among oncologists and hematologists enabling earlier diagnosis and treatment initiation.

- Furthermore, growing adoption of precision oncology approaches in MDS management, including molecular profiling-guided treatment selection and the integration of artificial intelligence in risk stratification, is establishing MDS-targeted therapies as the modern standard of hematological care. These converging factors are accelerating the uptake of MDS treatment solutions, thereby significantly boosting the industry's growth

Myelodysplastic Syndromes (MDS) Market Analysis

- Myelodysplastic syndromes, clonal hematopoietic disorders arising from abnormal bone marrow stem cell development characterized by ineffective hematopoiesis, peripheral cytopenias, and risk of transformation to acute myeloid leukemia, are increasingly recognized as a significant unmet need within hematology-oncology due to the limited curative treatment options available for the majority of affected patients

- The escalating demand for MDS therapies is primarily fueled by the rapidly aging global population with a higher burden of age-related clonal hematopoiesis, the landmark FDA approvals of luspatercept as first-line therapy and imetelstat as second-line therapy for lower-risk MDS in 2024, and the growing pipeline of targeted agents addressing specific mutational profiles across MDS subtypes

- North America dominated the MDS market with the largest revenue share of 39.40% in 2025, characterized by the highest incidence of MDS diagnosis with an estimated 10,000 to 30,000 new cases annually in the U.S., rapid uptake of newly approved therapies including imetelstat (Rytelo) and luspatercept (Reblozyl), robust reimbursement frameworks, and a strong presence of leading hematology companies including Bristol-Myers Squibb, Geron Corporation, and Takeda Pharmaceutical

- Asia-Pacific is expected to be the fastest growing region in the MDS market during the forecast period due to the rapidly expanding geriatric population, improving hematological diagnostic capabilities, and increasing adoption of innovative MDS treatment protocols at specialized oncology centers

- The oral segment dominated the largest market revenue share of 59.5% in 2025, driven by the widespread prescribing of oral agents including lenalidomide for del(5q) MDS, the growing adoption of INQOVI (oral decitabine/cedazuridine combination) that eliminates infusion center visits, and patient preference for oral administration that improves adherence and quality of life

Report Scope and Myelodysplastic Syndromes (MDS) Market Segmentation

|

Attributes |

Myelodysplastic Syndromes (MDS) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Bristol-Myers Squibb Company (U.S.) · Novartis AG (Switzerland) · Takeda Pharmaceutical Company (Japan) · Geron Corporation (U.S.) · Otsuka Holdings Co. Ltd. (Japan) · AbbVie Inc. (U.S.) · Jazz Pharmaceuticals (Ireland) · Rigel Pharmaceuticals (U.S.) · Astex Pharmaceuticals (U.S.) · Taiho Oncology (Japan) · Onconova Therapeutics (U.S.) · Syros Pharmaceuticals (U.S.) · FibroGen Inc. (U.S.) · Pfizer Inc. (U.S.) · Sanofi (France) · Medac (Germany) · Acceleron Pharma/Merck (U.S.) · Incyte Corporation (U.S.) · Lupin Limited (India) · Minovia Therapeutics (Israel) |

|

Market Opportunities |

· Expansion of Targeted Therapies for Mutational Subtype-Specific MDS · Growing Adoption of Oral Hypomethylating Agents |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Myelodysplastic Syndromes (MDS) Market Trends

“Precision Medicine and AI-Driven Risk Stratification Transforming MDS Management”

- A significant and accelerating trend in the global myelodysplastic syndromes market is the deepening integration of molecular profiling, next-generation sequencing, and artificial intelligence-powered risk stratification tools that are enabling more precise patient segmentation and treatment selection aligned with specific MDS mutational landscapes, transforming what was historically a broadly treated condition into a precision oncology target

- For instance, at the 2nd International Workshop on Myelodysplastic Syndromes and Myeloproliferative Neoplasms held in Boston in July 2024, leading hematologists highlighted the use of AI to improve risk stratification in MDS, demonstrating that machine learning algorithms analyzing mutational burden, cytogenetic data, and clinical parameters could predict disease trajectory with substantially greater accuracy than conventional IPSS-R scoring, enabling more personalized treatment selection

- AI integration in MDS management enables features such as automated bone marrow biopsy image analysis for morphological dysplasia grading, variant allele frequency tracking of clonal evolution across treatment cycles, and predictive modeling of AML transformation risk. In addition, the COMMANDS and IMerge trial data demonstrated that molecular markers such as SF3B1 mutation status and ring sideroblast presence are now being integrated into frontline treatment decision algorithms distinguishing luspatercept-appropriate from imetelstat-appropriate patient populations

- The seamless integration of molecular diagnostics with electronic health record systems and multidisciplinary hematology tumor board platforms is facilitating centralized, evidence-guided MDS management at comprehensive cancer centers. Through unified genomic data workflows, hematologists can coordinate targeted therapy selection, transfusion management, and stem cell transplant eligibility assessment within integrated care pathways

- This trend toward more intelligent, molecularly-guided, and personalized MDS management is fundamentally reshaping treatment paradigms across both lower-risk and higher-risk disease settings. Consequently, companies such as Syros Pharmaceuticals and Rigel Pharmaceuticals are developing mutation-specific targeted agents including tamibarotene and R289 that target the specific molecular pathways driving individual MDS subtypes

- The demand for precision medicine-based MDS management solutions incorporating molecular profiling, AI-driven risk stratification, and mutation-targeted therapeutic approaches is growing rapidly across both academic hematology centers and community oncology practices, as clinicians increasingly prioritize individualized care plans that optimize treatment outcomes and quality of life for MDS patients

Myelodysplastic Syndromes (MDS) Market Dynamics

Driver

“Landmark FDA Approvals and Expanding Targeted Therapy Pipeline Driving Market Growth”

- The accelerating regulatory approval of novel MDS therapies addressing previously unmet clinical needs, combined with the rapidly expanding pipeline of targeted agents addressing specific molecular drivers of MDS pathogenesis, is the primary driver for sustained market growth in the myelodysplastic syndromes space

- For instance, in June 2024, the FDA approved imetelstat (Rytelo), the first telomerase inhibitor for adults with transfusion-dependent anemia in low- to intermediate-1-risk MDS who have relapsed, are refractory to, or are ineligible for erythropoiesis-stimulating agents. The IMerge Phase 3 trial demonstrated statistically significant improvements in durable transfusion independence and hemoglobin response, establishing imetelstat as a mechanistically distinct disease-modifying therapy. Such approvals by key companies are expected to drive MDS market growth significantly throughout the forecast period

- As the FDA and EMA continue to grant breakthrough therapy, fast-track, and orphan drug designations to novel MDS candidates including bexmarilimab, R289, and other pipeline agents, pharmaceutical investment in MDS drug development is increasing substantially, creating a virtuous cycle of innovation that is expanding the treatment landscape and market value

- Furthermore, the full approval of luspatercept (Reblozyl) for first-line treatment of anemia in lower-risk MDS in patients without del(5q) following the positive COMMANDS trial data, combined with the growing adoption of oral hypomethylating agents such as INQOVI (decitabine/cedazuridine) that eliminate the need for infusion center visits, is substantially expanding the treated patient population and improving market penetration

- The growing recognition of MDS as a molecularly diverse group of disorders requiring subtype-specific treatment approaches, combined with improving diagnostic accuracy through next-generation sequencing, is expanding the diagnosed patient population and driving demand for a broader portfolio of targeted MDS therapies that address specific genetic vulnerabilities

Restraint/Challenge

“High Treatment Costs, Limited Curative Options, and Diagnostic Complexity”

- The high cost of novel MDS therapies including luspatercept, imetelstat, and stem cell transplantation combined with significant out-of-pocket expenses for long-term supportive care including red blood cell transfusions and growth factor injections represents a significant financial burden for patients and healthcare systems, particularly given that MDS predominantly affects elderly patients who may have limited economic resources

- For instance, the complex and heterogeneous nature of MDS with its multiple subtypes, overlapping morphological features with other hematological disorders, and requirement for specialized bone marrow biopsy interpretation with molecular profiling creates substantial diagnostic challenges that delay treatment initiation, particularly in community hospital settings without dedicated hematopathology expertise. Such diagnostic complexity contributes to treatment delays that worsen patient outcomes and limit market expansion in non-specialist settings

- Despite the recent approvals of imetelstat and luspatercept, the MDS treatment landscape remains characterized by a critical lack of curative options for the majority of patients, particularly those who are ineligible for allogeneic hematopoietic stem cell transplantation due to age, comorbidities, or lack of suitable donors. This unmet need drives patient and caregiver frustration and creates pressure for more effective disease-modifying therapies

- Companies such as Geron Corporation, Onconova Therapeutics, and FibroGen are investing in novel mechanisms of action including telomerase inhibition, kinase inhibition, and HIF-1alpha inhibition to address the therapeutic limitations of current MDS treatments and provide options for patients who have failed or are ineligible for existing approved therapies

- Overcoming these challenges through expanded reimbursement coverage, development of more effective and tolerable targeted agents, simplification of MDS diagnostic algorithms, and creation of accessible molecular profiling infrastructure across community hematology practices will be vital for sustained growth of the global MDS market

Myelodysplastic Syndromes (MDS) Market Scope

The market is segmented on the basis of type, therapeutic class, treatment, route of administration, end-user, and distribution channel.

- By Type

On the basis of type, the myelodysplastic syndromes market is segmented into Myelodysplastic Syndrome with Unilineage Dysplasia, Myelodysplastic Syndrome with Multilineage Dysplasia, Myelodysplastic Syndrome with Ring Sideroblasts, and Others. The MDS with multilineage dysplasia segment dominated the largest market revenue share of 20% in 2025, driven by its status as the most common MDS subtype affecting multiple hematopoietic cell lineages simultaneously, creating high transfusion requirements and symptom burden that necessitate pharmacological intervention. Patients with MDS-MLD frequently require both supportive care including regular red blood cell and platelet transfusions and active disease-modifying therapy with hypomethylating agents or erythropoiesis-stimulating agents, generating sustained demand for a broad portfolio of MDS treatment products. The segment benefits from the substantial clinical evidence base supporting azacitidine and decitabine in MDS-MLD patients across risk stratifications, providing well-established treatment algorithms that guide physician prescribing. In addition, the high prevalence of concurrent mutations in genes including DNMT3A, TET2, and ASXL1 in MDS-MLD patients is creating growing demand for molecularly targeted therapies that address the specific clonal drivers of multilineage dysplasia. Moreover, the growing adoption of molecular risk stratification tools in MDS-MLD management is enabling more precise therapy selection, further reinforcing dominant segment position.

The MDS with ring sideroblasts segment is anticipated to witness the fastest growth rate of 5.6% from 2026 to 2033, fueled by the landmark FDA approval of luspatercept as first-line therapy for anemia in lower-risk MDS patients including the SF3B1-mutated ring sideroblast subset, which has transformed treatment expectations and dramatically increased physician prescribing rates for this molecularly defined patient population. The COMMANDS trial demonstrating luspatercept's superiority over epoetin alfa in ESA-naive, transfusion-dependent lower-risk MDS with ring sideroblasts has established a new treatment standard that is driving substantial market expansion within this segment. In addition, the fastest growing CAGR reflects the expanding recognition of SF3B1 mutation as the key predictive biomarker for luspatercept response, creating a well-defined molecularly targeted patient population with strong commercial potential.

By Therapeutic Class

On the basis of therapeutic class, the MDS market is segmented into Hypomethylating Agents, Immunomodulatory Drugs, Anti-anemics, and Targeted Therapy. The hypomethylating agents segment dominated the largest market revenue share of 43.6% in 2025, driven by the widespread clinical adoption of azacitidine (Vidaza) and decitabine (Dacogen) as the established standard of care for higher-risk MDS patients ineligible for stem cell transplantation, supported by over two decades of clinical evidence demonstrating improvements in overall survival, hematological improvement, and quality of life compared to conventional care. Azacitidine and decitabine function by inhibiting DNA methyltransferases, reversing epigenetic silencing of tumor suppressor genes and enabling restoration of near-normal hematopoietic differentiation in a proportion of MDS patients. The segment further benefits from the commercial availability of oral hypomethylating formulations including INQOVI providing outpatient dosing convenience, growing generic competition improving cost accessibility for healthcare systems, and established physician familiarity across both academic and community hematology settings. In addition, the introduction of azacitidine-based combination regimens with venetoclax for higher-risk MDS patients ineligible for intensive chemotherapy is expanding the HMA segment's addressable population and revenue potential.

The targeted therapy segment is expected to witness the fastest CAGR of 12.4% from 2026 to 2033, driven by the landmark FDA approval of imetelstat (Rytelo) as a novel telomerase inhibitor providing durable transfusion independence in ESA-refractory lower-risk MDS, the expanding commercial uptake of luspatercept (Reblozyl) for ring sideroblast-positive and ESA-naive lower-risk MDS, and a rapidly expanding pipeline of mutation-specific targeted agents including IDH1/IDH2 inhibitors and IRAK1/IRAK4 dual inhibitors. In addition, a CAGR of 12.4% reflects the growing pharmaceutical recognition of MDS as a molecularly tractable precision oncology target amenable to targeted intervention across multiple specific mutational pathways.

- By Treatment

On the basis of treatment, the MDS market is segmented into Supportive Therapy, Growth Factors, Chemotherapy, Stem Cell Transplant, and Others. The stem cell transplant segment dominated the market with the largest revenue share of 38.7% in 2025, driven by its status as the only potentially curative treatment option for eligible MDS patients, typically younger patients or fit older patients with higher-risk disease, and the substantial healthcare costs associated with allogeneic hematopoietic stem cell transplantation including conditioning regimens, transplant procedures, graft-versus-host disease management, and extended follow-up care. The January 2025 FDA approval of GRAFAPEX (treosulfan) with fludarabine as a preparative conditioning regimen for alloHSCT in adult and pediatric MDS patients has expanded transplant eligibility to older and less fit patients, reinforcing the segment's dominant position. In addition, the high per-patient revenue contribution of stem cell transplant procedures, which can exceed USD 300,000 per case in the U.S., supports segment revenue dominance despite relatively lower patient volumes compared to drug-based treatment categories.

The growth factors segment is expected to witness the fastest CAGR during the forecast period, fueled by the growing clinical evidence supporting erythropoiesis-stimulating agents as foundational supportive care for lower-risk MDS and the increasing adoption of luspatercept as a next-generation erythropoiesis stimulatory agent providing superior transfusion independence rates versus conventional ESAs. The COMMANDS trial establishing luspatercept as superior to epoetin alfa in ESA-naive lower-risk MDS is dramatically shifting the growth factor treatment paradigm and driving accelerated adoption of novel erythropoietic agents. In addition, the expansion of luspatercept's clinical use through ongoing trials in newly defined MDS patient subpopulations is further supporting segment growth.

- By Route of Administration

On the basis of route of administration, the MDS market is segmented into Oral, Injectable, and Others. The oral segment dominated the largest market revenue share of 59.5% in 2025, driven by the widespread prescribing of oral agents including lenalidomide for del(5q) MDS, the growing adoption of INQOVI (oral decitabine/cedazuridine combination) that eliminates infusion center visits, and patient preference for oral administration that improves adherence and quality of life. The availability of oral MDS therapies provides substantial practical advantages for elderly patients with limited mobility, reduces healthcare resource utilization associated with intravenous infusions, and expands treatment access to community oncology settings. In addition, the growing development of oral targeted agents for MDS including investigational oral IDH inhibitors and oral telomerase inhibitor formulations is expected to further expand the oral segment's dominance through the forecast period.

The injectable segment is expected to witness the fastest CAGR during the forecast period, fueled by the market entry of luspatercept (subcutaneous injection) and imetelstat (intravenous infusion), both of which have achieved rapid commercial uptake following their 2024 approvals, and the growing adoption of subcutaneous azacitidine formulations providing more convenient administration compared to intravenous infusions. The immediate pharmacological action and predictable pharmacokinetics of injectable MDS agents continue to make them preferred for patients requiring urgent hematological improvement.

- By End-User

On the basis of end-user, the MDS market is segmented into Hospitals, Homecare, Specialty Centres, and Others. The hospitals segment accounted for the largest market revenue share of 48.6% in 2025, driven by their central role in bone marrow biopsy and molecular profiling for MDS diagnosis, transfusion services, stem cell transplantation programs, and administration of complex intravenous MDS therapies requiring clinical monitoring. Hospitals serve as the primary site of MDS diagnosis workup, risk stratification, treatment initiation, and management of treatment-related complications including cytopenias, infusion reactions, and disease progression. In addition, dedicated hematology units at major academic medical centers and comprehensive cancer centers function as the leading prescribers of novel targeted MDS therapies including imetelstat and luspatercept.

The specialty centres segment is expected to witness the fastest CAGR of 9.6% during the forecast period, fueled by the growing establishment of dedicated MDS clinics and hematology-oncology centers offering specialized outpatient MDS management. These specialized centers provide expert multidisciplinary care, access to clinical trials, molecular profiling services, and long-term follow-up programs that are essential for optimal MDS management. In addition, the adoption of oral hypomethylating agents and subcutaneous luspatercept is expanding MDS management beyond hospital infusion centers into community specialty clinic settings.

- By Distribution Channel

On the basis of distribution channel, the MDS market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 35% in 2025, driven by the predominant dispensing of complex MDS therapies including intravenous azacitidine, imetelstat, and luspatercept through hospital pharmacy systems that manage drug procurement, storage, preparation, and administration within clinical settings. Hospital pharmacies serve as the critical dispensing infrastructure for MDS therapies requiring controlled administration with clinical monitoring, and their established relationships with specialty pharmaceutical distributors support timely access to novel therapies including newly approved agents.

The online pharmacy segment is expected to witness the fastest CAGR of 5.5% during the forecast period, fueled by the growing adoption of specialty pharmacy home delivery services for oral MDS agents including lenalidomide and INQOVI, improving patient convenience and adherence for long-term maintenance therapy. Expanding telehealth platforms connecting MDS patients with specialized hematologists for prescription management and remote treatment monitoring are facilitating the growth of online pharmacy channels for MDS drug dispensing.

Myelodysplastic Syndromes (MDS) Market Regional Analysis

- North America dominated the MDS market with the largest revenue share of 39.40% in 2025, driven by the highest MDS diagnosis rates with an estimated 55,000 prevalent cases in the U.S., rapid commercial adoption of imetelstat and luspatercept following their landmark 2024 FDA approvals, and the presence of leading MDS pharmaceutical companies including Bristol-Myers Squibb, Geron Corporation, and Rigel Pharmaceuticals

- Consumers in the region benefit from favorable Medicare and commercial insurance reimbursement for approved MDS therapies, robust clinical trial infrastructure enabling early access to investigational agents, and highly developed hematology-oncology networks providing specialized MDS care at major academic medical centers

- This widespread adoption is further supported by high levels of MDS disease awareness among oncologists and hematologists, a technologically advanced diagnostic infrastructure including widespread access to next-generation sequencing for molecular profiling, and the growing preference for precision medicine approaches that align treatment selection with individual molecular disease characteristics

U.S. Myelodysplastic Syndromes (MDS) Market Insight

The U.S. MDS market captured the largest revenue share within North America in 2025, generating an estimated USD 1.1 billion, fueled by the rapid commercial uptake of imetelstat (Rytelo) and luspatercept (Reblozyl) following their FDA approvals in 2024, the January 2025 FDA approval of GRAFAPEX as a conditioning regimen for alloHSCT in MDS patients, and the September 2025 FDA approval of generic lenalidomide by Lupin expanding affordable access to immunomodulatory therapy. The U.S. benefits from both the American Cancer Society's growing public awareness programs for MDS and a strong clinical research network conducting pivotal trials of next-generation MDS therapies.

Europe Myelodysplastic Syndromes (MDS) Market Insight

The Europe MDS market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by the EMA regulatory pathway for luspatercept and imetelstat approvals, well-established national hematology guidelines supporting evidence-based MDS management, and significant clinical research activity at leading European hematology centers in Germany, France, the U.K., and Italy. The region benefits from broad universal healthcare coverage for MDS treatment and growing investment by European pharmaceutical companies and research institutions in novel MDS therapeutic development. In addition, the EORTC Leukemia Group and the European Leukemia Net are driving harmonized MDS treatment standards across member states.

U.K. Myelodysplastic Syndromes (MDS) Market Insight

The U.K. MDS market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by Blood Cancer UK reporting that over 2,000 people are diagnosed with MDS annually in the U.K., the NHS England's specialized blood cancer service networks providing access to expert multidisciplinary MDS care, and the growing availability of luspatercept and novel targeted MDS agents through NICE-approved treatment protocols. The U.K.'s Haematological Malignancy Research Network provides valuable real-world MDS epidemiology and outcomes data supporting treatment optimization.

Germany Myelodysplastic Syndromes (MDS) Market Insight

The Germany MDS market is expected to expand at a considerable CAGR during the forecast period, fueled by Germany's status as the highest MDS incident country within EU4 with the greatest number of diagnosed cases, the country's well-developed statutory health insurance coverage for novel MDS therapies including HMAs and targeted agents, and leading academic hematology centers in Leipzig, Dusseldorf, and Berlin contributing significantly to international MDS clinical research including the IMerge and COMMANDS trials.

Asia-Pacific Myelodysplastic Syndromes (MDS) Market Insight

The Asia-Pacific MDS market is poised to grow at the fastest CAGR of 10.9% during the forecast period of 2026 to 2033, driven by rapidly expanding geriatric populations across China, Japan, and India with higher MDS incidence, improving hematological diagnostic capabilities, increasing access to novel MDS therapies, and growing government investment in cancer care infrastructure. For instance, in December 2022, the Australian Leukaemia Foundation initiated clinical trials of new drugs for high-risk MDS, reflecting the region's expanding clinical research engagement with novel MDS treatment approaches. In addition, Japan's distinct MDS cytogenetics and lower median diagnosis age are driving localized research and clinical guideline development.

Japan Myelodysplastic Syndromes (MDS) Market Insight

The Japan MDS market is gaining momentum due to the country's highly developed hematology care network, well-established blood cancer clinical research infrastructure, and the Japanese Society of Hematology's active engagement in developing evidence-based MDS treatment guidelines incorporating newly approved agents. Japan's aging population with one of the world's highest proportions of elderly citizens is driving increasing MDS prevalence and demand for effective treatment options.

China Myelodysplastic Syndromes (MDS) Market Insight

The China MDS market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country's large aging patient population, rapidly expanding hematology-oncology care infrastructure, and increasing availability of generic HMAs and imported novel MDS therapies through China's accelerated drug approval pathways. The growing number of specialized blood cancer centers at major Chinese hospitals and increasing clinical trial activity for novel MDS agents are supporting market expansion.

Myelodysplastic Syndromes (MDS) Market Share

The Myelodysplastic Syndromes (MDS) industry is primarily led by well-established companies, including:

- Bristol-Myers Squibb Company (U.S.)

- Novartis AG (Switzerland)

- Takeda Pharmaceutical Company (Japan)

- Geron Corporation (U.S.)

- Otsuka Holdings Co. Ltd. (Japan)

- AbbVie Inc. (U.S.)

- Jazz Pharmaceuticals (Ireland)

- Rigel Pharmaceuticals (U.S.)

- Astex Pharmaceuticals (U.S.)

- Taiho Oncology (Japan)

- Onconova Therapeutics (U.S.)

- Syros Pharmaceuticals (U.S.)

- FibroGen Inc. (U.S.)

- Pfizer Inc. (U.S.)

- Sanofi (France)

- Medac (Germany)

- Acceleron Pharma/Merck (U.S.)

- Incyte Corporation (U.S.)

- Lupin Limited (India)

- Minovia Therapeutics (Israel)

Latest Developments in Global Myelodysplastic Syndromes (MDS) Market

- In February 2022, Syros Pharmaceuticals announced that the U.S. FDA granted Orphan Drug Designation to tamibarotene, a selective RAR-alpha agonist, for the treatment of MDS. This designation for the mutation-specific approach of targeting RARA-overexpressing MDS clones represented an early milestone in precision medicine-driven targeted therapy development for MDS, underscoring the growing pharmaceutical focus on molecularly defined MDS subtypes

- In April 2022, the U.S. FDA lifted its partial clinical hold on studies examining magrolimab in combination with azacitidine for the treatment of MDS, allowing the clinical evaluation of this anti-CD47 antibody combination to resume. This development highlighted the active investigation of novel immunotherapeutic approaches targeting the CD47 'don't eat me' signal in MDS, representing a mechanistically distinct pathway from conventional HMA therapy

- In June 2024, the FDA approved imetelstat (Rytelo), the first telomerase inhibitor, for adults with transfusion-dependent anemia in low- to intermediate-1-risk MDS who have relapsed, are refractory to, or are ineligible for erythropoiesis-stimulating agents. The Phase 3 IMerge trial demonstrated a statistically significant improvement in 24-week transfusion independence versus placebo, marking a transformative advance in second-line lower-risk MDS treatment with a mechanistically distinct disease-modifying approach

- In January 2025, the U.S. FDA approved GRAFAPEX (treosulfan) in combination with fludarabine as a preparative conditioning regimen for allogeneic hematopoietic stem cell transplantation in adult and pediatric patients with MDS, announced by Medexus. This approval expanded transplant eligibility to a broader population of MDS patients by providing a reduced-intensity conditioning option with a favorable toxicity profile, potentially increasing the number of patients eligible for the only curative treatment modality

- In March 2025, Faron Pharmaceuticals announced that the U.S. FDA granted Orphan Drug Designation to bexmarilimab, an anti-Clever-1 antibody, for the treatment of MDS. This designation for a novel immunotherapy approach targeting the macrophage immune checkpoint Clever-1 to promote anti-tumor immunity in MDS reflected the growing recognition of immune dysregulation as a key pathogenic driver amenable to therapeutic intervention

- In September 2025, Lupin received FDA approval for its generic lenalidomide capsules bioequivalent to Bristol-Myers Squibb's Revlimid for treatment of MDS and multiple myeloma, with manufacturing at its Pithampur facility in India. In addition, Minovia Therapeutics announced that the FDA granted Fast Track Designation to MNV-201 for treating MDS, reflecting continued regulatory momentum in advancing novel mechanism therapeutic candidates for this underserved hematological malignancy

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.