Global Myelofibrosis Mf Market

Market Size in USD Million

CAGR :

%

USD

655.12 Million

USD

896.57 Million

2025

2033

USD

655.12 Million

USD

896.57 Million

2025

2033

| 2026 –2033 | |

| USD 655.12 Million | |

| USD 896.57 Million | |

| % | |

|

Myelofibrosis (MF) Market Size

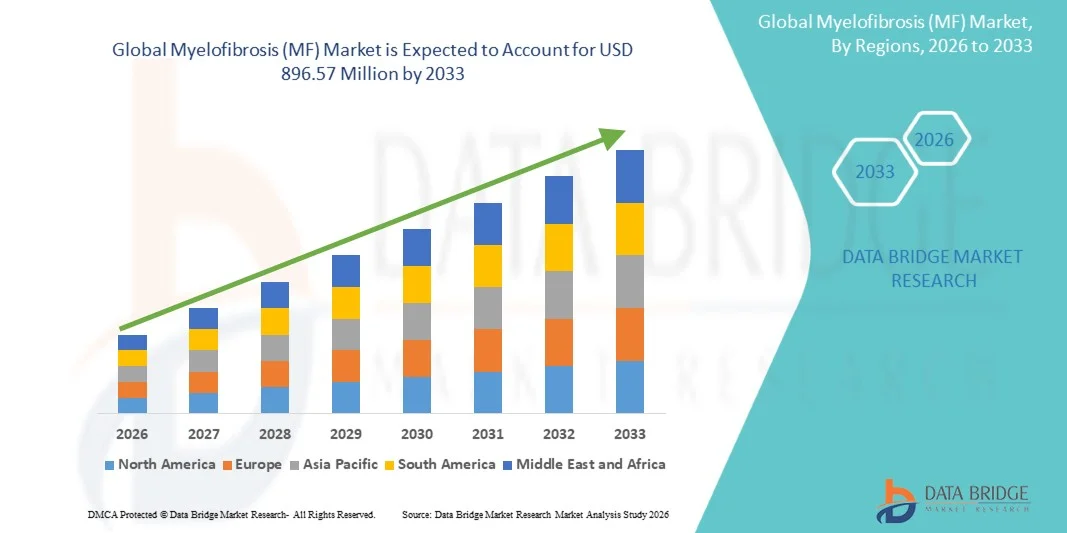

- The global Myelofibrosis (MF) market size was valued at USD 655.12 Million in 2025and is expected to reach USD 896.57 Million by 2033, at a CAGR of 4.00% during the forecast period

- The market growth is largely fueled by the rising prevalence of rare hematologic malignancies and continuous advancements in targeted oncology therapies, leading to increased adoption of innovative treatment solutions for myelofibrosis across hospitals, cancer centers, and specialty clinics worldwide. Growing investments in precision medicine and hematology research are further supporting market expansion

- Furthermore, rising patient demand for effective symptom management, improved survival outcomes, and personalized treatment options is establishing Myelofibrosis (MF) therapies as critical components of modern blood cancer care. These converging factors are accelerating the uptake of Myelofibrosis (MF) solutions, thereby significantly boosting the industry's growth

Myelofibrosis (MF) Market Analysis

- Myelofibrosis (MF), a rare chronic bone marrow disorder characterized by fibrosis, anemia, splenomegaly, and impaired blood cell production, is increasingly recognized as a critical segment within hematology and oncology care due to rising disease awareness, improved molecular diagnostics, and growing access to targeted treatment options

- The escalating demand for Myelofibrosis (MF) therapies is primarily fueled by increasing prevalence of myeloproliferative neoplasms, expanding use of JAK inhibitors, growing adoption of precision medicine, and rising need for therapies that improve symptom burden, spleen volume reduction, and overall survival outcomes

- North America dominated the myelofibrosis (MF) market with the largest revenue share of 41.30% in 2025, supported by advanced oncology infrastructure, favorable reimbursement systems, strong presence of leading pharmaceutical companies, and high adoption of innovative hematology treatments, with the U.S. witnessing substantial utilization of targeted therapies and stem cell transplant procedures

- Asia-Pacific is expected to be the fastest growing region in the myelofibrosis (MF) market during the forecast period due to improving hematology care infrastructure, rising healthcare expenditure, increasing diagnosis rates, and expanding access to specialty oncology therapies across countries such as China, India, Japan, and South Korea

- The Targeted Therapy segment dominated the largest market revenue share of 61.5% in 2025, driven by the widespread adoption of JAK inhibitors and other precision medicines that directly address disease pathways involved in myelofibrosis progression

Report Scope and Myelofibrosis (MF) Market Segmentation

|

Attributes |

Myelofibrosis (MF) Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Incyte Corporation (U.S.) · Novartis AG (Switzerland) · Bristol Myers Squibb (U.S.) · Pfizer Inc. (U.S.) · AbbVie Inc. (U.S.) · Merck & Co., Inc. (U.S.) · F. Hoffmann-La Roche Ltd. (Switzerland) · Johnson & Johnson (U.S.) · AstraZeneca plc (U.K.) · Eli Lilly and Company (U.S.) · GSK plc (U.K.) · Takeda Pharmaceutical Company Limited (Japan) · BeiGene Ltd. (China) · Teva Pharmaceutical Industries Ltd. (Israel) · Sun Pharmaceutical Industries Ltd. (India) · Dr. Reddy’s Laboratories Ltd. (India) · Cipla Limited (India) · Sierra Oncology, Inc. (U.S.) · CTI BioPharma Corp. (U.S.) |

|

Market Opportunities |

· Expansion of next-generation JAK inhibitors and combination therapies · Advancement in personalized medicine and molecular diagnostics |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Myelofibrosis (MF) Market Trends

“Advancements in Targeted Therapies and Precision Diagnostics”

- A significant and accelerating trend in the global Myelofibrosis (MF) market is the growing adoption of targeted therapies, molecular diagnostics, and personalized treatment strategies aimed at improving disease management and patient survival outcomes. This evolution is significantly enhancing treatment precision and long-term care standards

- For instance, JAK inhibitor therapies such as ruxolitinib and fedratinib are increasingly being used to reduce splenomegaly, improve constitutional symptoms, and enhance quality of life in patients with intermediate- and high-risk Myelofibrosis. Similarly, newer agents under development are targeting anemia and fibrosis progression

- Precision medicine integration enables features such as mutation profiling for JAK2, CALR, and MPL genes to support treatment selection and prognostic evaluation. For instance, advanced diagnostic panels help clinicians stratify patients more effectively and monitor therapeutic response over time. Furthermore, digital health platforms offer patients the ease of remote monitoring, allowing regular symptom tracking and follow-up management through connected healthcare systems

- The seamless integration of targeted drugs with supportive care therapies and broader oncology treatment pathways facilitates centralized management of complex patient needs. Through a single clinical framework, providers can address anemia, splenomegaly, thrombosis risk, and symptom burden, creating a more coordinated treatment experience

- This trend towards more intelligent, individualized, and outcome-focused treatment systems is fundamentally reshaping expectations for hematologic cancer care. Consequently, companies such as Novartis, Bristol Myers Squibb, and Incyte are developing next-generation therapies with improved efficacy and tolerability profiles for Myelofibrosis patients

- The demand for Myelofibrosis treatments that offer durable symptom relief, improved survival, and convenient administration is growing rapidly across hospitals and specialty cancer centers, as healthcare providers increasingly prioritize precision oncology solutions

Myelofibrosis (MF) Market Dynamics

Driver

“Growing Need Due to Rising Disease Burden and Expanding Access to Hematology Care”

- The increasing prevalence of myeloproliferative neoplasms among aging populations, coupled with the accelerating expansion of specialized hematology care services, is a significant driver for the heightened demand for Myelofibrosis therapies

- For instance, in April 2025, leading oncology centers expanded access programs for advanced bone marrow disorder treatments, focusing on broader availability of JAK inhibitors and molecular diagnostic testing. Such strategies by key healthcare providers are expected to drive the Myelofibrosis (MF) industry growth in the forecast period

- As patients become more aware of chronic blood cancer symptoms and seek earlier medical intervention, modern Myelofibrosis treatments offer advanced benefits such as spleen volume reduction, symptom improvement, and survival support, providing a compelling upgrade over conventional supportive care alone

- Furthermore, the growing popularity of precision medicine and the desire for individualized treatment pathways are making targeted therapies an integral component of hematology practice, offering seamless integration with diagnostics and long-term monitoring systems

- The convenience of oral therapies, improved access control through specialty pharmacies, and the ability to manage treatment through outpatient oncology settings are key factors propelling the adoption of Myelofibrosis therapies in both developed and emerging healthcare markets. The trend towards earlier diagnosis and the increasing availability of user-friendly treatment options further contribute to market growth

Restraint/Challenge

“Concerns Regarding High Treatment Costs and Limited Curative Options”

- Concerns surrounding the high cost of advanced therapies, including targeted drugs for Myelofibrosis, pose a significant challenge to broader market penetration. As many treatments require long-term use and specialist supervision, they can create financial burdens and access barriers, raising anxieties among patients about affordability and continuity of care

- For instance, high-priced branded JAK inhibitors and costly stem cell transplantation procedures have made some patients hesitant or unable to pursue optimal Myelofibrosis treatment solutions, particularly in lower-income regions

- Addressing these access concerns through reimbursement support, expanded insurance coverage, and regular introduction of lower-cost alternatives is crucial for building patient confidence. Companies such as Novartis and Incyte emphasize clinical value and long-term outcomes in their market strategies to reassure providers and payers

- In addition, the relatively high initial cost of some advanced Myelofibrosis treatment systems compared to supportive care can be a barrier to adoption for price-sensitive healthcare systems, particularly in developing regions or budget-constrained hospitals. While generic supportive medicines have become more affordable, premium targeted therapies or transplant procedures often come with a higher price tag

- While prices are gradually decreasing in some markets, the perceived premium for innovative hematology treatments can still hinder widespread adoption, especially for those who do not see an immediate need for advanced intervention

- Overcoming these challenges through enhanced reimbursement measures, patient education on treatment benefits, and the development of more affordable Myelofibrosis (MF) options will be vital for sustained market growth

Myelofibrosis (MF) Market Scope

The market is segmented on the basis of treatment type, route of administration, end-users, and distribution channel.

- By Treatment Type

On the basis of treatment type, the Myelofibrosis (MF) market is segmented into Targeted Therapy, Chemotherapy, and Others. The Targeted Therapy segment dominated the largest market revenue share of 61.5% in 2025, driven by the widespread adoption of JAK inhibitors and other precision medicines that directly address disease pathways involved in myelofibrosis progression. These therapies are preferred for reducing splenomegaly, symptom burden, fatigue, and inflammatory complications. Increasing clinical success of approved targeted drugs has significantly improved physician confidence. Growing diagnosis rates of primary and secondary myelofibrosis are supporting treatment demand. Pharmaceutical companies are actively investing in next-generation targeted pipelines. Better survival outcomes compared with conventional options further strengthen adoption. Rising awareness among hematologists regarding molecular testing also boosts segment growth. Availability through specialty oncology centers enhances accessibility. Supportive reimbursement in developed markets is another major driver. Combination regimens with anemia-focused agents are expanding usage. These factors collectively ensure dominance of the Targeted Therapy segment.

The Chemotherapy segment is expected to witness the fastest growth rate of 8.1% CAGR from 2026 to 2033, driven by increasing use in advanced-stage, refractory, or transformation-to-leukemia associated myelofibrosis cases. Chemotherapy remains relevant where rapid cytoreduction is clinically required. Growing demand for combination treatment protocols is supporting segment expansion. Physicians increasingly utilize chemotherapy in selected high-risk patients. Rising access to cancer care infrastructure in emerging economies further aids adoption. Availability of cost-effective generic cytotoxic agents supports market penetration. Increasing clinical trials evaluating combination regimens with targeted therapies also boost demand. Better supportive care management is improving treatment tolerability. Expanding hematology centers globally strengthen access. These factors position Chemotherapy as the fastest-growing treatment segment.

- By Route of Administration

On the basis of route of administration, the Myelofibrosis (MF) market is segmented into Oral, Parenteral, and Others. The Oral segment held the largest market revenue share of 58.9% in 2025, driven by the strong uptake of oral targeted therapies used as long-term disease management options. Patients prefer oral treatment due to convenience, reduced hospital visits, and easier chronic administration. Leading JAK inhibitors are commonly available in tablet formulations, supporting outpatient care. Growing preference for home-based oncology treatment is significantly aiding demand. Physicians favor oral regimens for continuous symptom control and patient adherence. Rising elderly patient populations further support non-invasive administration methods. Strong availability through specialty and retail pharmacies enhances accessibility. Improved compliance monitoring tools are also boosting usage. Expansion of oral oncology pipelines adds future growth potential. These factors maintain dominance of the Oral segment.

The Parenteral segment is expected to witness the fastest growth rate of 7.6% CAGR from 2026 to 2033, driven by increasing use of injectable supportive therapies, biologics, and hospital-administered treatment combinations. Patients with severe anemia, thrombocytopenia, or aggressive disease often require parenteral interventions. Growing use of transfusion support and injectable symptom-management drugs is supporting demand. Advances in biologic therapy development are further boosting market growth. Hospitals increasingly prefer monitored injectable treatment in complex cases. Rising investment in hematology infusion centers enhances accessibility. Better management of side effects is encouraging broader use. Increasing research into novel injectable agents supports future expansion. These factors make Parenteral the fastest-growing route of administration segment.

- By End-Users

On the basis of end-users, the Myelofibrosis (MF) market is segmented into Hospitals, Homecare, Specialty Clinics, and Others. The Hospitals segment accounted for the largest market revenue share of 46.8% in 2025, driven by the need for specialist diagnosis, bone marrow testing, imaging, transfusions, and multidisciplinary management of myelofibrosis patients. Hospitals remain the primary treatment centers for newly diagnosed and advanced-stage cases. Availability of hematologists, oncology pharmacists, and supportive care teams supports segment leadership. Patients requiring chemotherapy, transfusions, or emergency management are largely treated in hospitals. Rising incidence of rare blood cancers is increasing hospital admissions. Better reimbursement systems in developed countries further strengthen demand. Access to advanced laboratory infrastructure improves diagnostic confirmation. Increasing awareness among physicians is driving earlier referrals. Expansion of tertiary care cancer centers globally supports growth. These factors ensure Hospitals remain dominant.

The Specialty Clinics segment is expected to witness the fastest growth rate of 9.3% CAGR from 2026 to 2033, driven by the increasing establishment of dedicated hematology and oncology clinics worldwide. Patients prefer specialty clinics for faster appointments, focused expertise, and personalized disease monitoring. Long-term management of targeted therapy patients is increasingly shifting to outpatient specialty settings. Rising urbanization and healthcare accessibility support clinic growth. Availability of molecular diagnostics and follow-up care enhances treatment quality. Teleconsultation integration is improving patient convenience. Growing partnerships between hospitals and private clinics further aid expansion. Increasing demand for chronic cancer care outside hospitals supports revenue growth. These factors position Specialty Clinics as the fastest-growing end-user segment.

- By Distribution Channel

On the basis of distribution channel, the Myelofibrosis (MF) market is segmented into Hospital Pharmacy, Online Pharmacy, and Retail Pharmacy. The Hospital Pharmacy segment dominated the largest market revenue share of 51.7% in 2025, driven by the specialized nature of myelofibrosis therapies, many of which require monitored dispensing and oncology supervision. Hospital pharmacies are the primary source for newly initiated targeted therapies, chemotherapy, and supportive medicines. Complex dosing schedules often require pharmacist counseling. Strong linkage with hematology departments supports prescription volumes. Patients receiving inpatient or infusion-based care depend heavily on hospital pharmacy supply. Reimbursement handling and specialty procurement systems further strengthen dominance. Availability of cold-chain and high-value medicines also supports this channel. Growing tertiary hospital networks in emerging markets boost demand. These factors secure leadership of the Hospital Pharmacy segment.

The Online Pharmacy segment is expected to witness the fastest growth rate of 10.6% CAGR from 2026 to 2033, driven by growing digital healthcare adoption and increasing demand for convenient repeat dispensing of chronic oral therapies. Patients on long-term targeted therapy increasingly prefer doorstep medicine delivery. Secure e-prescriptions and tele-oncology consultations are accelerating channel adoption. Competitive pricing and subscription refill programs attract consumers. Rising smartphone penetration and improved digital trust further support growth. Better logistics for specialty medicine delivery are expanding reach. Patients in remote areas particularly benefit from online access. Integration with adherence reminders improves treatment continuity. Expanding regulatory acceptance of e-pharmacy platforms strengthens market potential. These factors collectively make Online Pharmacy the fastest-growing distribution channel segment.

Myelofibrosis (MF) Market Regional Analysis

- North America dominated the myelofibrosis (MF) market with the largest revenue share of 41.30% in 2025, supported by advanced oncology infrastructure, favorable reimbursement systems, strong presence of leading pharmaceutical companies, and high adoption of innovative hematology treatments. The region benefits from well-established cancer care networks, advanced diagnostic capabilities, and increasing access to specialty blood disorder treatment centers

- Healthcare providers and patients in the region highly value the availability of targeted therapies, JAK inhibitors, supportive care treatments, and stem cell transplant options for managing myelofibrosis. Growing focus on personalized medicine and long-term disease management is further strengthening market expansion

- This widespread adoption is further supported by high healthcare expenditure, active clinical research programs, and strong awareness of rare hematologic malignancies, establishing North America as a leading region in the Myelofibrosis (MF) market

U.S. Myelofibrosis (MF) Market Insight

The U.S. myelofibrosis (MF) market captured the largest revenue share within North America in 2025, driven by substantial utilization of targeted therapies and stem cell transplant procedures. The country benefits from leading cancer centers, broad access to hematologists, and rapid adoption of newly approved treatment options. Healthcare providers are increasingly focused on symptom control, spleen size reduction, anemia management, and improving quality of life through advanced treatment regimens. Strong clinical trial activity and ongoing drug innovation continue to support market growth in the U.S.

Europe Myelofibrosis (MF) Market Insight

The Europe myelofibrosis (MF) market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing prevalence of hematologic disorders, strong public healthcare systems, and growing access to advanced oncology care. The region is witnessing rising adoption of targeted therapies, transplant procedures, and supportive care treatments for rare blood cancers. Increasing research collaborations and regulatory support for orphan drugs are also contributing to market expansion across Europe.

U.K. Myelofibrosis (MF) Market Insight

The U.K. myelofibrosis (MF) market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by expanding access to hematology specialists and rising awareness of rare bone marrow disorders. Healthcare providers are increasingly emphasizing early diagnosis, precision treatment planning, and supportive management of chronic symptoms. Growth in specialty cancer centers and reimbursement support is expected to stimulate market demand in the U.K.

Germany Myelofibrosis (MF) Market Insight

The Germany myelofibrosis (MF) market is expected to expand at a considerable CAGR during the forecast period, fueled by advanced healthcare infrastructure, strong pharmaceutical presence, and growing demand for innovative oncology therapies. Germany’s established hematology treatment centers and emphasis on evidence-based medicine are promoting adoption of targeted treatments and transplant services. Rising elderly population levels are also supporting market growth.

Asia-Pacific Myelofibrosis (MF) Market Insight

The Asia-Pacific myelofibrosis (MF) market is poised to grow at the fastest CAGR during the forecast period due to improving hematology care infrastructure, rising healthcare expenditure, increasing diagnosis rates, and expanding access to specialty oncology therapies across countries such as China, India, Japan, and South Korea. Growing awareness of blood cancers, expanding tertiary hospitals, and better access to advanced diagnostics are significantly improving treatment opportunities across the region. Government healthcare reforms and oncology investments are further accelerating market growth.

Japan Myelofibrosis (MF) Market Insight

The Japan myelofibrosis (MF) market is gaining momentum due to the country’s advanced healthcare system, aging population, and strong focus on oncology innovation. Japanese healthcare providers increasingly emphasize precision medicine, supportive care, and long-term management of hematologic malignancies. Availability of modern targeted therapies and specialist treatment centers is further supporting market expansion.

China Myelofibrosis (MF) Market Insight

The China myelofibrosis (MF) market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s expanding healthcare infrastructure, growing oncology patient pool, and increasing awareness of rare blood disorders. China is witnessing rising adoption of specialty oncology drugs, improved access to hematology centers, and growing investment in cancer diagnostics. Government healthcare modernization efforts and broader availability of innovative therapies are key factors propelling the Myelofibrosis (MF) market in the country.

Myelofibrosis (MF) Market Share

The Myelofibrosis (MF) industry is primarily led by well-established companies, including:

- Incyte Corporation (U.S.)

- Novartis AG (Switzerland)

- Bristol Myers Squibb (U.S.)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Merck & Co., Inc. (U.S.)

- Hoffmann-La Roche Ltd. (Switzerland)

- Johnson & Johnson (U.S.)

- AstraZeneca plc (U.K.)

- Eli Lilly and Company (U.S.)

- GSK plc (U.K.)

- Takeda Pharmaceutical Company Limited (Japan)

- BeiGene Ltd. (China)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sun Pharmaceutical Industries Ltd. (India)

- Reddy’s Laboratories Ltd. (India)

- Cipla Limited (India)

- Sierra Oncology, Inc. (U.S.)

- CTI BioPharma Corp. (U.S.)

Latest Developments in Global Myelofibrosis (MF) Market

- In February 2021, Bristol Myers Squibb announced positive updated clinical data for Inrebic (fedratinib) in patients with intermediate-2 or high-risk myelofibrosis, demonstrating continued spleen volume reduction and symptom improvement in patients previously treated with ruxolitinib. This reinforced Inrebic’s growing role as a second-line therapy in the global myelofibrosis market

- In December 2021, Karyopharm Therapeutics presented Phase 1/2 clinical data for selinexor in combination with ruxolitinib for myelofibrosis at the American Society of Hematology (ASH) Annual Meeting. The study highlighted potential disease-modifying activity and symptom improvement, supporting development of novel combination therapies in myelofibrosis

- In June 2022, updated results from the Phase III MOMENTUM trial were presented at ASCO, showing that momelotinib significantly improved symptoms, spleen response, and transfusion independence versus danazol in symptomatic anemic myelofibrosis patients previously treated with a JAK inhibitor. The results positioned momelotinib as a promising new treatment option

- In September 2023, GSK announced that the U.S. Food and Drug Administration approved Ojjaara (momelotinib) for the treatment of intermediate or high-risk myelofibrosis in adults with anemia. Ojjaara became the first and only approved therapy specifically indicated for myelofibrosis patients with anemia, addressing splenomegaly, constitutional symptoms, and transfusion burden.

- In November 2023, GSK announced that the European Medicines Agency’s CHMP adopted a positive opinion recommending approval of momelotinib for myelofibrosis patients with moderate to severe anemia. This marked a major regulatory step toward commercialization across the European Union

- In January 2024, the European Commission granted marketing authorization for Omjjara (momelotinib) for adult patients with myelofibrosis and anemia, including both newly diagnosed and previously treated patients. The approval significantly expanded GSK’s presence in the international myelofibrosis treatment market

- In March 2024, Blood Cancer Journal published a major review titled Momelotinib for Myelofibrosis: Our 14 Years of Experience, highlighting long-term clinical benefits, anemia improvement, and the differentiated ACVR1/JAK inhibition mechanism of momelotinib. The publication strengthened physician awareness and confidence in the therapy

- In June 2024, GSK announced that Japan’s Ministry of Health, Labour and Welfare approved Omjjara (momelotinib) for the treatment of myelofibrosis. The approval marked the fourth major regulatory authorization for the therapy globally and expanded access across Asia-Pacific markets

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.