Global Natural Refrigerants Market

Market Size in USD Billion

CAGR :

%

USD

2.58 Billion

USD

6.44 Billion

2025

2033

USD

2.58 Billion

USD

6.44 Billion

2025

2033

| 2026 - 2033 | |

| USD 2.58 Billion | |

| USD 6.44 Billion | |

| % | |

|

Natural Refrigerants Market Overview

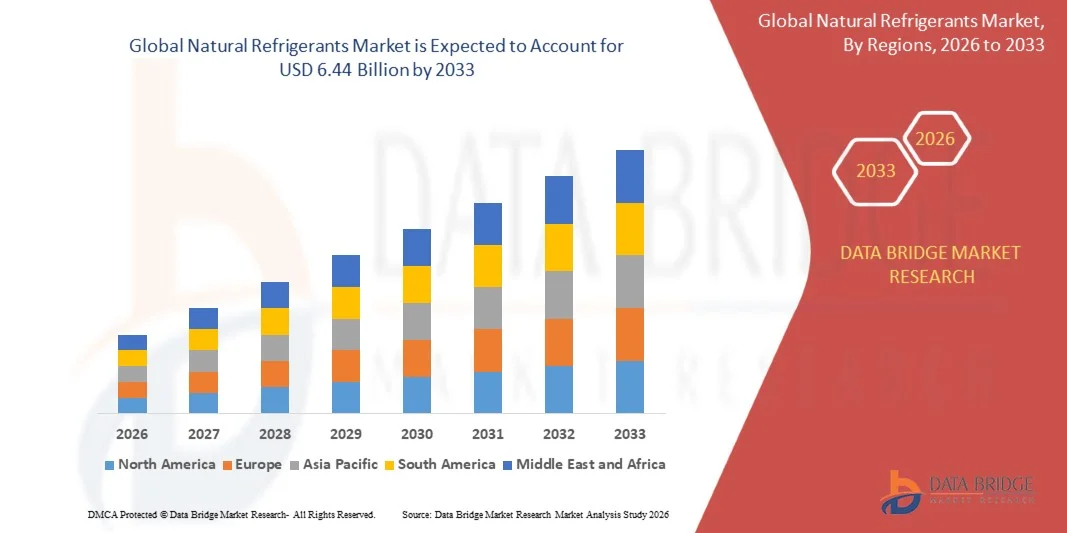

The Natural Refrigerants Market was valued at USD 2.58 billion in 2025 and is projected to reach USD 6.44 billion by 2033, growing at a CAGR of 12.10% from 2026 to 2033. The market is witnessing strong growth driven by rising environmental concerns, stringent regulations on high-GWP synthetic refrigerants, and increasing adoption of sustainable cooling solutions across commercial and industrial sectors.

The shift toward eco-friendly refrigeration technologies, including ammonia, carbon dioxide, and hydrocarbons, is accelerating as governments and industries prioritize carbon neutrality and energy efficiency. Expanding applications in food cold storage, supermarkets, industrial refrigeration, and HVAC systems are further supporting market expansion, as end users seek low-emission and cost-efficient cooling alternatives.

Key Market Trends & Insights

- North America dominated the natural refrigerants market with the largest revenue share of 39.8% in 2025, supported by strong regulatory pressure to reduce high-GWP refrigerants and increasing adoption of sustainable cooling technologies across commercial and industrial sectors.

- Asia-Pacific natural refrigerants market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, expanding cold chain infrastructure, and rising demand for energy-efficient cooling systems.

- The Ammonia Refrigerant segment held the largest market revenue share of approximately 38.6% in 2025, driven by its high energy efficiency, zero global warming potential, and extensive deployment in industrial refrigeration systems. It is widely used in cold storage warehouses, food processing plants, and large-scale refrigeration facilities due to its strong thermodynamic performance. Ammonia systems are particularly preferred in continuous heavy-duty operations where operational cost efficiency is critical. The segment also benefits from long lifecycle performance and low refrigerant cost compared to synthetic alternatives. Industrial expansion in food logistics and cold chain infrastructure continues to reinforce its dominance.

- The CO₂ Refrigerant segment is projected to register the fastest growth at a CAGR of 13.4% from 2026 to 2033, supported by increasing adoption in supermarket refrigeration systems and transcritical CO₂ Regulatory pressure under F-Gas norms in Europe and similar environmental policies in other regions are accelerating its adoption. CO₂ refrigerants are gaining traction in retail chains due to their low environmental impact and high safety profile. Technological improvements in cascade systems are further enhancing efficiency in warmer climates. Expanding retail infrastructure and sustainability commitments by global food retailers are significantly boosting demand.

- The Industrial Refrigeration segment held the largest market revenue share of approximately 34.9% in 2025, driven by strong demand from food processing units, cold storage facilities, and logistics warehouses. These systems require highly efficient and continuous cooling, making ammonia and CO₂-based solutions highly suitable. Industrial users prioritize energy efficiency and long-term operational cost savings, supporting sustained adoption. Expansion of global cold chain infrastructure is further strengthening this segment. Rising demand for processed and frozen food products continues to support growth.

- The Commercial Refrigeration segment accounted for approximately 29.7% market share in 2025, supported by strong deployment in supermarkets, hypermarkets, and retail chains. Regulatory mandates in Europe and North America are accelerating replacement of HFC-based systems with natural refrigerant alternatives. Retailers are increasingly adopting CO₂ transcritical systems for sustainability and compliance benefits. These systems also help reduce long-term energy consumption in large-scale refrigeration setups. Growing global grocery retail expansion is reinforcing steady segment growth.

Market Size & Forecast

- Global Market Value (2025): USD 2.58 Billion

- Expected Market Value (2033): USD 6.44 Billion

- Forecast CAGR (2026–2033): 12.10%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Natural Refrigerants Market Segmentation

|

Attributes |

Natural Refrigerants Key Market Insights |

|

Segments Covered |

· By Type: Ammonia Refrigerant, Hydrocarbon Refrigerant, CO2 Refrigerant, and Others Refrigerant · By Application: Commercial Refrigeration, Industrial Refrigeration, Domestic Refrigeration, Domestic Refrigeration, Stationary Air Conditioning, Mobile Air Conditioning, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• LG Electronics (South Korea) |

|

Market Opportunities |

· Increasing Adoption Of Eco-Friendly Cooling Technologies · Expansion Of Cold Chain Infrastructure In Emerging Economies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Natural Refrigerants Market Trends

Trend: Increasing Adoption Of Natural Refrigerants In Sustainable Cooling Systems

The global shift toward low-global-warming-potential (GWP) and zero-ozone-depletion refrigerants is accelerating as industries move away from synthetic hydrofluorocarbons (HFCs) due to environmental regulations and climate commitments. Natural refrigerants such as ammonia, carbon dioxide, hydrocarbons, and water-based systems are increasingly being deployed in commercial refrigeration, industrial cooling, and HVAC applications to reduce greenhouse gas emissions and improve long-term energy efficiency.

In commercial retail and food storage systems, supermarkets across Europe have rapidly adopted CO₂ transcritical systems, with countries such as Germany and the U.K. leading large-scale rollouts under F-Gas regulation compliance. For instance, CO₂-based refrigeration systems are increasingly replacing HFC-based units in grocery chains to achieve up to 20–30% lower lifecycle emissions while maintaining stable cooling performance in cold storage applications.

In industrial applications, ammonia-based refrigeration continues to gain traction in food processing plants, cold chain logistics hubs, and large-scale warehouses due to its high thermodynamic efficiency and zero direct global warming potential. In addition, hydrocarbon refrigerants such as propane (R290) are being integrated into compact refrigeration units and residential air conditioning systems in Asia-Pacific markets, particularly in India and China, where manufacturers are scaling production to meet rising domestic demand for energy-efficient appliances.

The rapid expansion of cold chain infrastructure in emerging economies is also strengthening demand for natural refrigerants, particularly in pharmaceuticals and perishable food transportation. In addition, data center cooling systems are beginning to experiment with low-GWP refrigerant blends and natural alternatives to reduce energy consumption and comply with sustainability targets set by global technology firms such as Microsoft and Google, which have committed to carbon neutrality across their supply chains.

Natural Refrigerants Market Dynamics

Key Market Driver: Stringent Environmental Regulations And Transition Toward Low-GWP Refrigeration Systems

Governments worldwide are enforcing strict regulations to phase down high-GWP refrigerants under frameworks such as the Kigali Amendment to the Montreal Protocol, compelling industries to adopt environmentally sustainable alternatives. Rising global temperatures and increasing carbon reduction targets are pushing commercial refrigeration and HVAC operators to transition toward natural refrigerants with minimal environmental impact.

Industrial and commercial sectors are increasingly deploying CO₂ and ammonia-based systems in supermarkets, cold storage warehouses, and industrial chillers to comply with regulatory mandates while improving energy efficiency. For instance, European Union F-Gas regulations are driving rapid replacement of HFC-based refrigeration systems, with CO₂ transcritical systems becoming standard in new retail installations across multiple countries.

Similarly, food and beverage companies and logistics providers are adopting ammonia-based refrigeration for large-scale cold storage facilities due to its high efficiency and cost-effectiveness in continuous operations. Real-world deployments in cold chain hubs across Germany and Japan have demonstrated significant reductions in energy consumption and operating costs compared to conventional synthetic refrigerant systems, supporting long-term sustainability goals.

Key Restraint/Challenge: Safety Concerns And Infrastructure Limitations In Handling Natural Refrigerants

Despite strong environmental advantages, natural refrigerants present operational challenges such as toxicity, flammability, and high-pressure system requirements, which limit their widespread adoption in certain applications. Ammonia-based systems require strict safety protocols due to toxicity risks, while hydrocarbon refrigerants pose flammability concerns in residential and small commercial environments.

In addition, the transition from conventional HFC-based systems requires significant infrastructure upgrades, specialized technician training, and redesign of existing refrigeration equipment, increasing initial capital costs for end users. Limited availability of compatible components and service expertise in developing regions further slows adoption rates.

Industry studies indicate that while natural refrigerant systems can reduce long-term operating costs, initial installation costs can be 15–40% higher compared to traditional HFC-based systems, creating affordability challenges for small and medium enterprises in emerging economies.

Key Market Opportunity: Expansion Of Energy-Efficient Cold Chain And Industrial Cooling Infrastructure

Rapid expansion of global cold chain logistics, pharmaceuticals storage, and processed food distribution is creating significant opportunities for natural refrigerants, particularly in developing economies across Asia-Pacific, Latin America, and Africa. Increasing demand for vaccine distribution infrastructure and perishable food transport is accelerating investments in sustainable refrigeration technologies.

Industrial operators are increasingly integrating CO₂ and ammonia-based systems into large-scale warehouses and processing plants to improve energy efficiency and reduce carbon footprints. For instance, India’s growing food processing sector and China’s expanding e-commerce cold chain logistics network are driving large-scale deployment of natural refrigerant-based refrigeration systems.

In addition, advancements in cascade refrigeration systems and hybrid CO₂-ammonia technologies are improving system efficiency and expanding applicability across medium and low-temperature cooling segments. Cold storage capacity expansions in Asia-Pacific during 2025 have shown significant adoption of natural refrigerant systems, with reported energy savings of approximately 15–25% compared to conventional refrigeration setups, reinforcing long-term growth potential across industrial and commercial applications.

Natural Refrigerants Market Scope

The market is segmented on the basis of type and application.

- By Type

On the basis of type, the natural refrigerants market is segmented into Ammonia Refrigerant, Hydrocarbon Refrigerant, CO₂ Refrigerant, and Others Refrigerant. The Ammonia Refrigerant segment held the largest market revenue share of approximately 38.6% in 2025, driven by its high energy efficiency, zero global warming potential, and extensive deployment in industrial refrigeration systems. It is widely used in cold storage warehouses, food processing plants, and large-scale refrigeration facilities due to its strong thermodynamic performance. Ammonia systems are particularly preferred in continuous heavy-duty operations where operational cost efficiency is critical. The segment also benefits from long lifecycle performance and low refrigerant cost compared to synthetic alternatives. Industrial expansion in food logistics and cold chain infrastructure continues to reinforce its dominance.

The CO₂ Refrigerant segment is projected to register the fastest growth at a CAGR of 13.4% from 2026 to 2033, supported by increasing adoption in supermarket refrigeration systems and transcritical CO₂ technologies. Regulatory pressure under F-Gas norms in Europe and similar environmental policies in other regions are accelerating its adoption. CO₂ refrigerants are gaining traction in retail chains due to their low environmental impact and high safety profile. Technological improvements in cascade systems are further enhancing efficiency in warmer climates. Expanding retail infrastructure and sustainability commitments by global food retailers are significantly boosting demand.

- By Application

On the basis of application, the natural refrigerants market is segmented into Commercial Refrigeration, Industrial Refrigeration, Domestic Refrigeration, Stationary Air Conditioning, Mobile Air Conditioning, and Others. The Industrial Refrigeration segment held the largest market revenue share of approximately 34.9% in 2025, driven by strong demand from food processing units, cold storage facilities, and logistics warehouses. These systems require highly efficient and continuous cooling, making ammonia and CO₂-based solutions highly suitable. Industrial users prioritize energy efficiency and long-term operational cost savings, supporting sustained adoption. Expansion of global cold chain infrastructure is further strengthening this segment. Rising demand for processed and frozen food products continues to support growth.

The Commercial Refrigeration segment accounted for approximately 29.7% market share in 2025, supported by strong deployment in supermarkets, hypermarkets, and retail chains. Regulatory mandates in Europe and North America are accelerating replacement of HFC-based systems with natural refrigerant alternatives. Retailers are increasingly adopting CO₂ transcritical systems for sustainability and compliance benefits. These systems also help reduce long-term energy consumption in large-scale refrigeration setups. Growing global grocery retail expansion is reinforcing steady segment growth.

Natural Refrigerants Market Regional Analysis

North America Natural Refrigerants Market Insight

North America dominated the natural refrigerants market with the largest revenue share of 39.8% in 2025, supported by strong regulatory pressure to reduce high-GWP refrigerants and increasing adoption of sustainable cooling technologies across commercial and industrial sectors. The region benefits from advanced cold chain infrastructure, high penetration of industrial refrigeration systems, and strong presence of major food processing and logistics companies. Growing investments in CO₂ and ammonia-based refrigeration systems in supermarkets and warehouses are further strengthening market demand. In addition, sustainability commitments from major corporations are accelerating the transition toward eco-friendly refrigerant alternatives, reinforcing regional leadership in the market.

U.S. Natural Refrigerants Market Insight

The U.S. natural refrigerants market captured the largest revenue share in North America in 2025, driven by rapid replacement of HFC-based systems with low-GWP alternatives across retail, industrial, and HVAC applications. Strong regulatory frameworks such as EPA SNAP guidelines and state-level climate policies are encouraging widespread adoption of natural refrigerants. Supermarket chains and cold storage operators are increasingly deploying CO₂ transcritical systems to improve energy efficiency and reduce emissions. In addition, rising demand from the food and beverage sector and expanding e-commerce cold chain logistics are further supporting market growth. Continuous technological advancements in refrigeration system design are enhancing efficiency and scalability.

Europe Natural Refrigerants Market Insight

The Europe natural refrigerants market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by stringent F-Gas regulations and aggressive decarbonization targets across the European Union. The region is rapidly transitioning away from synthetic refrigerants toward CO₂, ammonia, and hydrocarbon-based systems across commercial and industrial applications. Strong focus on sustainability, energy efficiency, and carbon neutrality is accelerating adoption across supermarkets, cold storage facilities, and industrial refrigeration plants. In addition, government incentives and green building initiatives are further promoting the use of natural refrigerants in HVAC systems and commercial infrastructure development.

U.K. Natural Refrigerants Market Insight

The U.K. natural refrigerants market is expected to witness steady growth from 2026 to 2033, driven by increasing regulatory pressure under F-Gas phase-down policies and growing demand for low-carbon cooling solutions. Retailers and food logistics providers are increasingly adopting CO₂-based refrigeration systems to meet sustainability targets and reduce operational emissions. Rising awareness of climate change and energy efficiency is also encouraging adoption in commercial and residential HVAC systems. In addition, modernization of cold chain infrastructure and expansion of supermarket networks are further supporting market penetration across the country.

Germany Natural Refrigerants Market Insight

The Germany natural refrigerants market is expected to witness strong growth from 2026 to 2033, supported by the country’s leadership in environmental sustainability and energy-efficient technologies. Germany has been an early adopter of ammonia and CO₂-based refrigeration systems in industrial and commercial applications. Strong regulatory enforcement, combined with advanced engineering capabilities, is accelerating the shift toward natural refrigerants. Increasing deployment in food processing industries and cold storage facilities is further driving demand. In addition, Germany’s focus on green building standards and industrial decarbonization is reinforcing long-term market expansion.

Asia-Pacific Natural Refrigerants Market Insight

The Asia-Pacific natural refrigerants market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid urbanization, expanding cold chain infrastructure, and rising demand for energy-efficient cooling systems. Countries such as China, India, and Japan are increasingly adopting natural refrigerants in commercial refrigeration, industrial cooling, and domestic appliances. Government initiatives promoting energy efficiency and environmental sustainability are further boosting adoption. In addition, the region’s strong manufacturing base for refrigeration equipment is improving accessibility and affordability of natural refrigerant systems across emerging economies.

Japan Natural Refrigerants Market Insight

The Japan natural refrigerants market is expected to witness steady growth from 2026 to 2033, driven by advanced technological adoption and strong focus on energy-efficient cooling systems. The country is actively transitioning toward CO₂-based refrigeration systems in supermarkets and convenience stores. High awareness of environmental sustainability and strict energy efficiency standards are supporting market expansion. In addition, integration of natural refrigerants in industrial refrigeration and HVAC systems is increasing. Japan’s emphasis on innovation and smart infrastructure development is further strengthening adoption across commercial and industrial sectors.

China Natural Refrigerants Market Insight

The China natural refrigerants market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by rapid urbanization, expanding retail infrastructure, and strong government support for green cooling technologies. China is witnessing large-scale deployment of CO₂ and hydrocarbon-based refrigeration systems across supermarkets, cold storage facilities, and industrial applications. The country’s strong manufacturing capabilities are enabling cost-effective production of natural refrigerant systems. In addition, rising demand from food processing and e-commerce logistics sectors is significantly boosting market growth. Government-led environmental policies are further accelerating the shift toward sustainable refrigeration solutions.

Natural Refrigerants Market Share

The Natural Refrigerants industry is primarily led by well-established companies, including:

• LG Electronics (South Korea)

• Haier Group (China)

• Sony Corporation (Japan)

• Sichuan Changhong Electronics Co. Ltd (China)

• Samsung Electronics Co. Ltd. (South Korea)

• Koninklijke Philips N.V. (Netherlands)

• Sharp Corporation (Japan)

• VIZIO Inc. (U.S.)

• Hisense Co., Ltd. (China)

• Panasonic Corporation (Japan)

Latest Developments in Natural Refrigerants Market

- In March 2023, Danfoss, acquisition initiative, acquired BOCK GmbH, a leading manufacturer of CO₂ and low-GWP compressors, to strengthen its natural refrigerant technology portfolio. The acquisition enables expansion of energy-efficient compressor solutions for hydrocarbons, CO₂ (R744), and other eco-friendly refrigerants. It is expected to accelerate the global transition toward sustainable cooling technologies and improve system efficiency across industrial refrigeration applications. The move strengthens Danfoss’ position in the natural refrigerants ecosystem and supports decarbonization goals across HVAC and refrigeration sectors. It also enhances innovation in low-emission compressor technologies for global markets

- In February 2023, Linde, strategic investment and supply agreement, signed a long-term contract and invested approximately USD 1.8 billion to supply clean hydrogen and nitrogen to OCI’s blue ammonia plant in Beaumont, Texas. The project aims to develop large-scale low-carbon ammonia production and strengthen the clean fuels value chain. It supports decarbonization in industrial gas applications and enhances the production of sustainable ammonia-based solutions. The investment significantly boosts the development of blue ammonia infrastructure and clean hydrogen ecosystems. It also strengthens the global shift toward low-emission energy and fertilizer production systems

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Natural Refrigerants Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Natural Refrigerants Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Natural Refrigerants Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.