Global Nucleic Acid Testing Nat Instrumentation Market

Market Size in USD Billion

CAGR :

%

USD

1.37 Billion

USD

2.19 Billion

2025

2033

USD

1.37 Billion

USD

2.19 Billion

2025

2033

| 2026 –2033 | |

| USD 1.37 Billion | |

| USD 2.19 Billion | |

| % | |

|

Nucleic Acid Testing-NAT Instrumentation Market Size

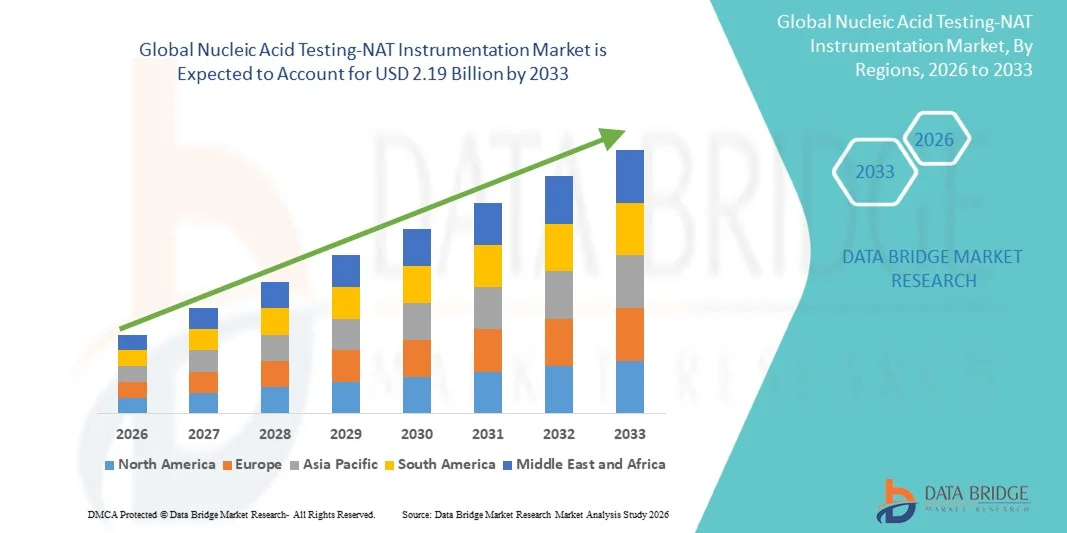

- The global nucleic acid testing-NAT instrumentation market size was valued at USD 1.37 billion in 2025 and is expected to reach USD 2.19 billion by 2033, at a CAGR of 6.05% during the forecast period

- The market growth is largely fueled by the increasing adoption of advanced molecular diagnostic technologies and ongoing technological innovations in automated nucleic acid testing platforms, leading to enhanced efficiency and accuracy in clinical diagnostics, blood screening, and infectious disease testing

- Furthermore, rising demand from healthcare providers, blood banks, and research laboratories for rapid, reliable, and high-throughput testing solutions is establishing NAT instrumentation as a critical component in modern diagnostic workflows. These converging factors are accelerating the uptake of nucleic acid testing solutions, thereby significantly boosting the market’s growth

Nucleic Acid Testing-NAT Instrumentation Market Analysis

- Nucleic Acid Testing (NAT) instrumentation, which enables rapid, sensitive, and high-throughput detection of pathogens and genetic material, is increasingly vital in blood screening, infectious disease diagnostics, and molecular research due to its accuracy, automation, and scalability

- The market growth is primarily driven by rising demand for reliable and fast diagnostic solutions, growing prevalence of infectious diseases, expansion of blood screening programs, and ongoing technological advancements in automated NAT platforms. These factors are accelerating the adoption of NAT instrumentation, thereby significantly boosting market growth

- North America dominated the nucleic acid testing NAT instrumentation market in 2025, accounting for approximately 41% of global revenue, supported by advanced healthcare infrastructure, widespread adoption of automated testing platforms, high government and private funding for diagnostics, and the presence of key industry players such as Roche, Abbott, and Qiagen

- Asia-Pacific is expected to be the fastest-growing region in the nucleic acid testing NAT instrumentation market during the forecast period, with a projected CAGR driven by expanding healthcare infrastructure, increasing infectious disease testing, rising awareness of molecular diagnostics, and growing government initiatives in countries like China, India, and Japan

- The disease diagnosis segment accounted for the largest market revenue share of 47.3% in 2025, driven by the global need for early and accurate detection of infectious diseases, genetic disorders, and cancer

Report Scope and Nucleic Acid Testing-NAT Instrumentation Market Segmentation

|

Attributes |

Nucleic Acid Testing-NAT Instrumentation Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Nucleic Acid Testing-NAT Instrumentation Market Trends

“Advancements in High-Throughput NAT Instrumentation and Workflow Efficiency”

- A significant and accelerating trend in the global nucleic acid testing (NAT) instrumentation market is the continuous innovation in high-throughput platforms that enable faster, more accurate detection of nucleic acids from clinical and research samples

- For instance, in July 2024, Roche launched the cobas 5800 system, offering automated sample processing with enhanced throughput and integrated quality control, supporting large-scale molecular diagnostics in hospitals and reference laboratories

- Manufacturers are increasingly focusing on automation, miniaturization, and multiplexing capabilities to reduce turnaround time, minimize human error, and support simultaneous detection of multiple pathogens or genetic targets

- Integration of robust data management and laboratory information systems (LIS) with NAT instrumentation is streamlining workflows, enabling seamless result reporting, traceability, and compliance with regulatory standards

- This trend toward higher efficiency, reliability, and automation is accelerating adoption in clinical diagnostics, blood screening, infectious disease testing, and research applications

- The growing emphasis on rapid, accurate, and scalable molecular diagnostics continues to drive investments in advanced NAT instrumentation across hospitals, diagnostic centers, and public health laboratories

Nucleic Acid Testing-NAT Instrumentation Market Dynamics

Driver

“Increasing Demand for Rapid and Accurate Molecular Diagnostics”

- The rising prevalence of infectious diseases, genetic disorders, and need for timely patient management is driving demand for nucleic acid testing solutions that offer high sensitivity and specificity

- For instance, in March 2025, Hologic expanded its Panther Fusion NAT platform to include new assays for respiratory viruses and sexually transmitted infections, reflecting growing demand for multi-target testing in clinical laboratories

- The increasing adoption of molecular diagnostics for early disease detection, pathogen surveillance, and personalized medicine is encouraging healthcare providers to invest in NAT instrumentation

- Furthermore, government initiatives and public health programs targeting infectious disease monitoring, blood screening, and pandemic preparedness are supporting market expansion

- The convenience of automated workflows, rapid turnaround times, and reliable results is driving adoption in both established and emerging markets, particularly in hospitals, diagnostic labs, and reference laboratories

Restraint/Challenge

“High Instrument Costs and Technical Complexity”

- The high initial investment required for NAT instrumentation, including equipment, reagents, and software, can restrict adoption among smaller clinics or laboratories with limited budgets

- For instance, in October 2023, several mid-sized laboratories in Southeast Asia reported delays in adopting fully automated NAT platforms due to high capital expenditure and operational costs

- Technical complexity and the need for trained personnel to operate sophisticated instruments and interpret results can hinder rapid deployment in resource-limited settings

- Regulatory requirements for clinical validation, quality control, and compliance with international standards add further operational challenges and cost implications

- Addressing these challenges through cost optimization, simplified workflows, operator training programs, and scalable solutions will be critical to sustaining market growth in the Nucleic Acid Testing-NAT Instrumentation segment

Nucleic Acid Testing-NAT Instrumentation Market Scope

The market is segmented on the basis of technology, application, and end users.

• By Technology

On the basis of technology, the Nucleic Acid Testing (NAT) Instrumentation market is segmented into Polymerase Chain Reaction (PCR), Ligase Chain Reaction (LCR), Transcription–mediated Amplification (TMA), Whole Genome Sequencing (WGS), and others. The Polymerase Chain Reaction (PCR) segment dominated the largest market revenue share of 41.7% in 2025, driven by its widespread adoption for accurate, sensitive, and rapid nucleic acid detection. PCR remains the gold standard for infectious disease diagnostics, oncology mutation profiling, and genetic testing due to its high specificity and established workflow in clinical laboratories. Hospitals and diagnostic centers prefer PCR for routine pathogen detection and disease surveillance. Technological advancements, such as real-time quantitative PCR (qPCR) and multiplex PCR, have further enhanced throughput and reliability. PCR assays are cost-effective and widely validated, supporting dominance in both emerging and developed markets. Integration with automated platforms improves workflow efficiency. Government and public health initiatives to strengthen infectious disease testing further accelerate adoption. The scalability of PCR enables use in small labs as well as large hospital networks. PCR’s versatility across multiple applications contributes to its leading revenue share.

The Whole Genome Sequencing (WGS) segment is expected to witness the fastest CAGR of 19.2% from 2026 to 2033, driven by increasing demand for precision medicine, genomics research, and comprehensive pathogen surveillance. WGS enables complete genomic profiling for personalized therapy, outbreak tracing, and advanced diagnostics. Falling sequencing costs, improved accuracy, and high-throughput capabilities make WGS increasingly accessible to hospitals, academic research centers, and biotech labs. WGS supports oncology, rare disease diagnostics, and infectious disease applications. Government-funded population genomics projects contribute to market growth. Integration with bioinformatics and AI-assisted analysis enhances data interpretation. Academic and clinical collaborations promote adoption in translational research. WGS allows simultaneous analysis of multiple pathogens or gene variants. Technological innovations in library preparation and sequencing chemistry improve efficiency. Expansion of genomic medicine programs in emerging markets accelerates growth. Demand for rapid pathogen variant detection in infectious disease outbreaks drives adoption. Overall, WGS represents the most dynamic and rapidly growing technology segment.

• By Application

On the basis of application, the NAT Instrumentation market is segmented into disease diagnosis, forensic testing, personalized medicine, and others. The disease diagnosis segment accounted for the largest market revenue share of 47.3% in 2025, driven by the global need for early and accurate detection of infectious diseases, genetic disorders, and cancer. PCR- and WGS-based diagnostics are widely used in hospitals, diagnostic centers, and government labs for rapid pathogen detection and epidemiological surveillance. Rising prevalence of viral outbreaks, such as COVID-19, influenza, and antibiotic-resistant infections, has accelerated adoption. Integration of NAT instruments with automated platforms and laboratory information systems improves workflow efficiency. Hospitals prioritize disease diagnosis applications for routine screening, outbreak monitoring, and clinical management. Public health programs and reimbursement support further enhance market dominance. NAT enables multiplex testing and rapid reporting, reducing diagnostic turnaround time. Disease diagnosis applications include both inpatient and outpatient settings. High adoption in emerging economies is fueled by government initiatives for infectious disease control. Accuracy, reliability, and scalability of NAT instruments strengthen their leadership in this segment.

The personalized medicine segment is expected to witness the fastest CAGR of 18.4% from 2026 to 2033, driven by the growing need for tailored therapeutics and precision oncology. NAT instruments, particularly WGS and PCR-based systems, enable identification of patient-specific genetic mutations for therapy selection. Adoption is increasing in oncology, rare disease treatment, and pharmacogenomics applications. Hospitals, specialty clinics, and research centers invest in NAT technologies to support individualized patient care. Integration with AI-assisted analysis platforms improves decision-making. Increasing government and private funding for precision medicine programs boosts growth. Personalized medicine also drives companion diagnostics development. Rising awareness of genomic-based therapy benefits among clinicians and patients accelerates adoption. Technological advancements reduce sample processing time and enhance throughput. Growing clinical trial activity in targeted therapies fuels demand. Personalized medicine applications are rapidly expanding in developed regions and emerging markets alike.

• By End Users

On the basis of end users, the NAT Instrumentation market is segmented into hospitals, specialty clinics, diagnostic centres, academic and research institutes, and others. The hospitals segment dominated the largest market revenue share of 49.6% in 2025, driven by high patient volumes and the integration of NAT instruments into routine diagnostics. Hospitals utilize NAT for infectious disease detection, genetic testing, and oncology applications. PCR remains widely implemented in clinical labs, while WGS and TMA are gaining traction for precision medicine programs. Large hospitals invest in automated and high-throughput systems to increase workflow efficiency. Hospitals benefit from government funding, reimbursement support, and public health initiatives to implement NAT testing. Multi-departmental usage increases instrument utilization. Integration with laboratory information management systems enhances reporting and clinical decision support. Hospitals prefer validated, reliable platforms with regulatory approvals. Growing patient awareness and preventive healthcare measures further encourage adoption. Hospitals remain the backbone of NAT instrumentation deployment worldwide.

The academic and research institutes segment is expected to witness the fastest CAGR of 17.9% from 2026 to 2033, driven by increased genomics research, population studies, and translational medicine projects. Research institutes use NAT instruments for molecular biology studies, drug discovery, and pathogen surveillance. Advancements in WGS, CRISPR-based detection, and TMA technologies support academic adoption. Government and private grants facilitate large-scale genomic research programs. Academic centers increasingly collaborate with biotechnology and pharmaceutical companies. Emerging research applications, such as single-cell genomics and metagenomics, drive instrument demand. Training and education in genomics enhance institutional adoption. Bioinformatics integration supports complex data analysis. Growth in molecular epidemiology studies accelerates adoption. Research institutes adopt flexible, high-throughput platforms for diverse experimental workflows. Overall, this segment represents the fastest-growing end-user category for NAT instrumentation globally.

Nucleic Acid Testing-NAT Instrumentation Market Regional Analysis

North America dominated the nucleic acid testing NAT instrumentation market in 2025, accounting for approximately 41% of global revenue. Market growth is supported by advanced healthcare infrastructure, widespread adoption of automated testing platforms, substantial government and private funding for diagnostics, and the presence of key industry players such as Roche, Abbott, and Qiagen. High diagnostic testing volumes in hospitals, reference laboratories, and blood screening facilities further strengthen the region’s market leadership.

U.S. Nucleic Acid Testing (NAT) Instrumentation Market Insight

The U.S. nucleic acid testing NAT instrumentation market captured the largest revenue share in North America in 2025, driven by early adoption of molecular diagnostic platforms and automated NAT systems across clinical laboratories, hospitals, and blood banks. The strong presence of major NAT instrument manufacturers and ongoing investments in genomic and infectious disease research contribute to sustained growth in the U.S. market.

Europe Nucleic Acid Testing (NAT) Instrumentation Market Insight

The Europe nucleic acid testing NAT instrumentation market is projected to grow steadily, supported by increasing adoption of NAT platforms in hospitals, diagnostic centers, and public health laboratories. Government-supported initiatives for infectious disease screening, blood safety, and molecular diagnostics are boosting demand, while regulatory frameworks encourage the use of validated NAT instrumentation for clinical applications.

U.K. Nucleic Acid Testing (NAT) Instrumentation Market Insight

The U.K. nucleic acid testing NAT instrumentation market is expected to grow at a moderate CAGR during the forecast period, driven by demand for high-throughput NAT instruments in hospitals and public health laboratories. Programs aimed at improving infectious disease detection and blood safety, coupled with private laboratory expansion, support market growth.

Germany Nucleic Acid Testing (NAT) Instrumentation Market Insight

Germany nucleic acid testing NAT instrumentation market is expected to witness steady growth, fueled by adoption of advanced molecular diagnostics and NAT platforms in hospital networks, blood banks, and research institutes. Increasing awareness of infectious disease monitoring and investments in automated diagnostic systems drive the market, particularly in clinical and public health settings.

Asia-Pacific Nucleic Acid Testing (NAT) Instrumentation Market Insight

Asia-Pacific nucleic acid testing NAT instrumentation market is expected to be the fastest-growing region in the NAT Instrumentation market during the forecast period, driven by expanding healthcare infrastructure, increasing infectious disease testing, rising awareness of molecular diagnostics, and growing government initiatives in countries such as China, India, and Japan. The rising number of public and private diagnostic laboratories, along with efforts to improve blood safety and infectious disease surveillance, is accelerating market adoption.

China Nucleic Acid Testing (NAT) Instrumentation Market Insight

China nucleic acid testing NAT instrumentation market accounted for the largest revenue share in Asia-Pacific in 2025, supported by increasing investment in molecular diagnostics, expansion of hospital and laboratory infrastructure, and growing demand for infectious disease testing. Government initiatives for blood safety and infectious disease monitoring, combined with strong domestic manufacturing capabilities for NAT instruments, are key factors propelling market growth.

Japan Nucleic Acid Testing (NAT) Instrumentation Market Insight

Japan’s nucleic acid testing NAT instrumentation market is gaining momentum due to rising adoption of molecular diagnostics in hospitals, research centers, and clinical laboratories. Government support for infectious disease detection and blood safety programs, along with increasing investment in advanced automation for NAT testing, is driving growth.

Nucleic Acid Testing-NAT Instrumentation Market Share

The Nucleic Acid Testing-NAT Instrumentation industry is primarily led by well-established companies, including:

- Roche Diagnostics (Switzerland)

- Abbott (U.S.)

- Qiagen N.V. (Netherlands)

- Hologic, Inc. (U.S.)

- bioMérieux S.A. (France)

- PerkinElmer, Inc. (U.S.)

- Siemens Healthineers (Germany)

- Danaher Corporation (U.S.)

- Thermo Fisher Scientific (U.S.)

- Becton, Dickinson and Company (U.S.)

- F. Hoffmann-La Roche Ltd (Switzerland)

- Hain Lifescience GmbH (Germany)

- GenMark Diagnostics, Inc. (U.S.)

- LumiraDx Ltd. (U.K.)

- BGI Genomics (China)

- CerTest Biotec (Spain)

- Seegene, Inc. (South Korea)

- Bio-Rad Laboratories, Inc. (U.S.)

- Mobidiag (Finland)

- Myriad Genetics, Inc. (U.S.)

Latest Developments in Global Nucleic Acid Testing-NAT Instrumentation Market

- In April 2021, Bio‑Rad Laboratories, Inc. launched its Reliance SARS‑CoV‑2 RT‑PCR Assay Kit with CE‑IVD marking for the European market, enabling high‑sensitivity nucleic acid detection for COVID‑19 and expanding access to reliable molecular testing in clinical laboratories across Europe. This release marked a significant contribution to NAT capabilities during the pandemic

- In May 2021, Thermo Fisher Scientific completed the acquisition of Mesa Biotech, a provider of advanced on‑site NAAT solutions, for up to $550 million, strengthening its molecular diagnostics portfolio and reinforcing its position in rapid NAT instrumentation and diagnostics worldwide

- In July 2021, bioMérieux launched EPISEQ SARS‑CoV‑2, a cloud‑based nucleic acid testing and genomic surveillance platform designed to track SARS‑CoV‑2 variants using NAAT data across multiple sequencing systems, enhancing public health response capabilities

- In November 2023, Roche Diagnostics announced the global launch of the LightCycler PRO System, a next‑generation qPCR instrument designed to advance clinical molecular diagnostics with improved performance, flexibility, and ease of use for both research and in‑vitro diagnostic workflows

- In March 2023, reports highlighted that Roche, Abbott, and Becton Dickinson were driving growth in automated molecular diagnostic systems integrating PCR‑based NAT workflows into broader clinical lab automation, boosting capacity and throughput for infectious disease testing

- In March 2025, Thermo Fisher Scientific received FDA 510(k) clearance for its Applied Biosystems TaqPath COVID‑19, Flu A, Flu B, RSV Select Panel, a multiplex real‑time PCR test designed for use on the QuantStudio 5 Dx system, enabling simultaneous detection of multiple respiratory pathogens

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.