Global Oilfield Scale Inhibitor Market

Market Size in USD Million

CAGR :

%

USD

900.00 Million

USD

1,439.22 Million

2025

2033

USD

900.00 Million

USD

1,439.22 Million

2025

2033

| 2026 - 2033 | |

| USD 900.00 Million | |

| USD 1,439.22 Million | |

| % | |

|

Oilfield Scale Inhibitor Market Overview

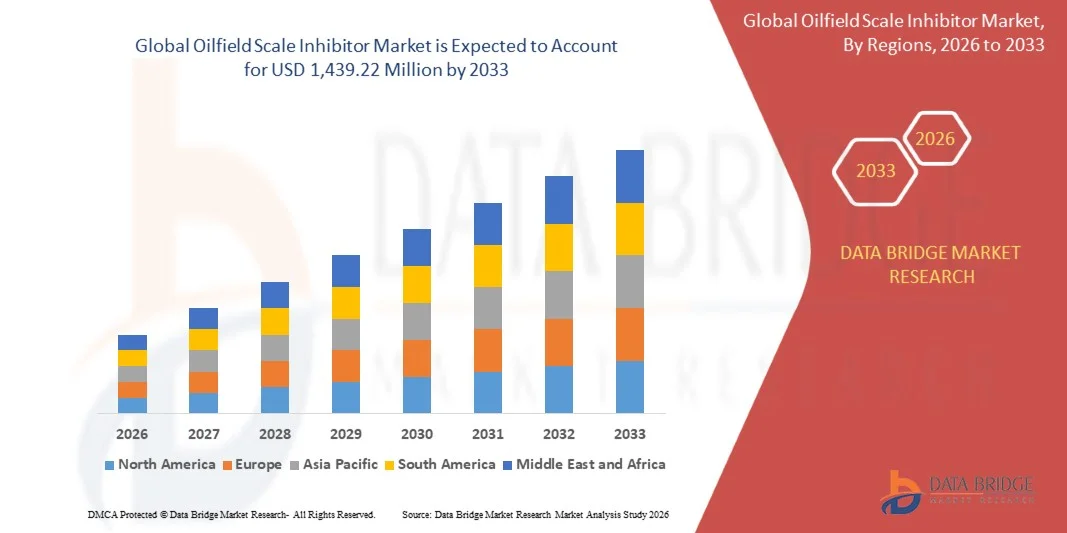

The Oilfield Scale Inhibitor Market was valued at USD 900.00 million in 2025 and is projected to reach USD 1,439.22 million by 2033, growing at a CAGR of 6.00% from 2026 to 2033. The market is experiencing stable growth driven by increasing oil and gas exploration activities, rising demand for enhanced oil recovery operations, and growing focus on maintaining production efficiency across mature and deepwater oilfields. Increasing operational challenges associated with mineral scale deposition in pipelines, wellbores, and production equipment are further accelerating adoption of advanced scale inhibition technologies across upstream oil and gas operations.

The increasing complexity of offshore drilling environments globally, combined with rising pressure to minimize equipment downtime and improve operational reliability, is compelling oilfield operators and service providers to deploy advanced chemical treatment solutions for scale management. Phosphonate- and polymer-based scale inhibitors are increasingly replacing conventional treatment approaches in many production systems, offering improved flow assurance, extended equipment lifespan, and reduced maintenance costs. In addition, expanding investments in unconventional oil and gas resources, including shale reservoirs and high-temperature high-pressure wells, are creating strong demand for highly efficient and thermally stable oilfield scale inhibitor formulations across global energy markets.

Key Market Trends & Insights

- North America dominated the oilfield scale inhibitor market with the largest revenue share of approximately 36.8% in 2025, supported by expanding hydraulic fracturing operations, strong upstream oil and gas investments, and increasing deployment of chemical enhanced oil recovery technologies across the U.S. and Canada.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of approximately 7.1% from 2026 to 2033. Growth is driven by rising offshore drilling projects, increasing domestic hydrocarbon production initiatives, and expanding refinery and upstream infrastructure investments across China, India, Indonesia, and Australia.

- The Phosphonates segment held the largest market revenue share of approximately 41.7% in 2025 driven by its high thermal stability, strong calcium carbonate inhibition performance, and widespread deployment across offshore drilling and enhanced oil recovery operations. Phosphonate-based inhibitors are widely preferred in high-pressure and high-temperature oilfield environments due to their effectiveness in preventing sulfate and carbonate scale formation across pipelines, injection systems, and production tubing.

- The Carboxylate/Acrylic segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by increasing demand for environmentally compliant and low-toxicity scale management solutions across offshore oilfields. Rising adoption of biodegradable polymer-based inhibitor chemistries and expanding regulatory pressure regarding phosphorous discharge limitations are accelerating segment expansion across North America and Europe.

- The Onshore Oilfield segment accounted for the largest market revenue share of approximately 62.9% in 2025 driven by increasing shale production activities, mature field optimization programs, and rising deployment of chemical enhanced oil recovery operations across major oil-producing economies. Onshore production facilities extensively utilize scale inhibitors to reduce mineral deposition in pipelines, separators, and water injection systems while improving production efficiency and reducing operational downtime.

- The Offshore Oilfield segment is projected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing deepwater and ultra-deepwater exploration projects across the Gulf of Mexico, Brazil, West Africa, and the North Sea. Rising operational complexity in subsea production systems and increasing demand for high-performance thermally stable inhibitor formulations are accelerating adoption across offshore drilling environments.

Market Size & Forecast

- Global Market Value (2025): USD 900.00 Million

- Expected Market Value (2033): USD 1,439.22 Million

- Forecast CAGR (2026–2033): 6.00%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Oilfield Scale Inhibitor Market Segmentation

|

Attributes |

Oilfield Scale Inhibitor Key Market Insights |

|

Segments Covered |

· By Type: Phosphonates, Carboxylate/Acrylic, Sulfonates, and Others · By Applications: Onshore Oilfield and Offshore Oilfield |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Halliburton Energy Services, Inc. (U.S.) |

|

Market Opportunities |

• Expansion Of Deepwater And Ultra-Deepwater Exploration Activities |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Oilfield Scale Inhibitor Market Trends

Trend: Increasing Adoption Of Environmentally Sustainable And High-Performance Oilfield Chemicals

Growing demand for operational efficiency, equipment protection, and environmentally compliant production chemicals is accelerating adoption of advanced oilfield scale inhibitors across upstream oil and gas operations. Conventional scale management approaches often result in production interruptions, equipment corrosion, and increased maintenance costs, encouraging operators to deploy highly efficient chemical inhibitor systems capable of improving flow assurance and extending asset life.

In offshore and unconventional oilfields, operators are increasingly integrating advanced phosphonate- and polymer-based scale inhibitors, For instance in subsea pipelines, injection wells, and enhanced oil recovery systems, to minimize calcium carbonate and sulfate scale deposition under high-pressure and high-temperature operating conditions. In mature oilfields, these inhibitors are being used to maintain reservoir productivity and reduce operational downtime associated with scaling in production tubing and surface equipment.

The rapid expansion of deepwater drilling projects and shale production activities is also increasing demand for thermally stable and environmentally sustainable inhibitor formulations capable of operating under chemically aggressive conditions. In addition, oilfield service companies are investing in biodegradable and low-toxicity chemical technologies to comply with tightening environmental regulations across offshore production markets. Field deployment studies conducted in the North Sea and Gulf of Mexico during 2025 demonstrated that advanced scale inhibitor treatment programs reduced unplanned production downtime by approximately 12–18% while extending equipment operational lifespan in offshore wells

Oilfield Scale Inhibitor Market Dynamics

Key Market Driver: Rising Expansion Of Deepwater And Enhanced Oil Recovery Operations

Oil and gas operators worldwide are increasingly investing in deepwater exploration, mature field optimization, and enhanced oil recovery activities to maintain hydrocarbon production and improve reservoir output. High salinity water conditions and mineral-rich reservoir environments significantly increase the risk of scale deposition within production systems, creating strong demand for advanced scale inhibitor technologies capable of maintaining uninterrupted flow operations.

Industries such as offshore drilling, shale production, and mature field operations are increasingly deploying oilfield scale inhibitors to reduce scale formation in pipelines, production tubing, separators, and injection systems. Energy companies are actively implementing continuous chemical injection systems, For instance in offshore platforms and subsea production infrastructure, to improve production reliability and minimize costly shutdowns associated with scaling-related blockages.

Similarly, enhanced oil recovery operations utilizing water flooding and chemical injection techniques are increasing dependence on scale inhibition technologies to maintain reservoir pressure and production efficiency. Offshore project assessments conducted in Brazil and the Middle East during 2024 indicated that advanced scale inhibitor deployment reduced scaling-related maintenance interventions by approximately 15–20% in high-temperature oil production environments

Key Restraint/Challenge: Environmental Compliance Pressure And Chemical Cost Volatility

Oilfield chemical manufacturers are facing increasing regulatory pressure regarding environmental toxicity, chemical discharge limitations, and sustainability compliance across offshore and onshore drilling activities. Conventional scale inhibitor chemistries containing phosphorous compounds and specialty additives are subject to stricter environmental monitoring, increasing product reformulation and compliance costs for manufacturers.

In addition, fluctuations in raw material pricing, specialty chemical availability, and transportation costs are increasing overall production expenses for oilfield service providers and chemical suppliers. Complex operational conditions in ultra-deepwater and high-pressure reservoirs further require customized inhibitor formulations, creating affordability concerns for smaller exploration operators and cost-sensitive oilfield projects.

Industrial benchmarking assessments conducted during 2024 indicated that specialty oilfield chemical prices experienced fluctuations of approximately 9–13% across major energy markets due to supply chain instability, feedstock cost increases, and tightening environmental compliance requirements, impacting procurement budgets for oilfield operators globally

Key Market Opportunity: Development Of Biodegradable And Smart Chemical Monitoring Technologies

Modern oilfield operations increasingly require environmentally sustainable and digitally optimized chemical treatment systems capable of improving operational reliability while minimizing ecological impact. Conventional monitoring approaches often provide limited real-time visibility into scaling behavior, creating opportunities for advanced inhibitor formulations integrated with intelligent monitoring technologies.

Oilfield service companies are increasingly exploring biodegradable inhibitor systems, For instance low-toxicity phosphonate alternatives and environmentally compliant polymer chemistries, to improve offshore regulatory compliance and reduce environmental discharge risks. In digital oilfield operations, operators are integrating real-time chemical monitoring sensors and predictive analytics platforms to optimize inhibitor dosing efficiency and reduce chemical wastage during production activities.

In addition, advancements in nanotechnology-based inhibitor formulations and automated injection systems are improving scale prevention efficiency across complex reservoir conditions, opening opportunities across offshore, shale, and enhanced oil recovery applications globally. Pilot digital oilfield projects conducted during 2025 across the U.S. shale sector and North Sea offshore operations reported chemical consumption optimization improvements of approximately 10–14% after integrating automated scale inhibitor monitoring and injection management systems.

Oilfield Scale Inhibitor Market Scope

The market is segmented on the basis of type and applications.

- By Type

On the basis of type, the oilfield scale inhibitor market is segmented into Phosphonates, Carboxylate/Acrylic, Sulfonates, and Others. The Phosphonates segment held the largest market revenue share of approximately 41.7% in 2025 driven by its high thermal stability, strong calcium carbonate inhibition performance, and widespread deployment across offshore drilling and enhanced oil recovery operations. Phosphonate-based inhibitors are widely preferred in high-pressure and high-temperature oilfield environments due to their effectiveness in preventing sulfate and carbonate scale formation across pipelines, injection systems, and production tubing.

The Carboxylate/Acrylic segment is projected to register the fastest growth at a CAGR of 6.8% from 2026 to 2033, driven by increasing demand for environmentally compliant and low-toxicity scale management solutions across offshore oilfields. Rising adoption of biodegradable polymer-based inhibitor chemistries and expanding regulatory pressure regarding phosphorous discharge limitations are accelerating segment expansion across North America and Europe.

- By Applications

On the basis of applications, the oilfield scale inhibitor market is segmented into Onshore Oilfield and Offshore Oilfield. The Onshore Oilfield segment accounted for the largest market revenue share of approximately 62.9% in 2025 driven by increasing shale production activities, mature field optimization programs, and rising deployment of chemical enhanced oil recovery operations across major oil-producing economies. Onshore production facilities extensively utilize scale inhibitors to reduce mineral deposition in pipelines, separators, and water injection systems while improving production efficiency and reducing operational downtime.

The Offshore Oilfield segment is projected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing deepwater and ultra-deepwater exploration projects across the Gulf of Mexico, Brazil, West Africa, and the North Sea. Rising operational complexity in subsea production systems and increasing demand for high-performance thermally stable inhibitor formulations are accelerating adoption across offshore drilling environments.

Oilfield Scale Inhibitor Market Regional Analysis

North America Oilfield Scale Inhibitor Market Insight

North America dominated the oilfield scale inhibitor market with the largest revenue share of 36.8% in 2025, supported by expanding shale oil and gas production activities, increasing enhanced oil recovery operations, and strong investments in upstream oilfield infrastructure. Oil and gas operators across the region highly prioritize production efficiency, flow assurance, and equipment reliability, increasing adoption of advanced scale inhibition technologies across onshore and offshore assets. Rising drilling activity in the Permian Basin and growing deployment of chemical injection systems are further strengthening market expansion across North America.

U.S. Oilfield Scale Inhibitor Market Insight

The U.S. oilfield scale inhibitor market captured the largest revenue share in 2025 within North America, fueled by rapid shale exploration activities, increasing hydraulic fracturing operations, and rising investments in mature well optimization programs. Oilfield operators are increasingly focusing on reducing production downtime and minimizing pipeline scaling through continuous chemical treatment technologies. In addition, rising crude oil output from unconventional reservoirs and increasing offshore exploration activity in the Gulf of Mexico are significantly contributing to market growth across the U.S. energy sector.

Europe Oilfield Scale Inhibitor Market Insight

The Europe oilfield scale inhibitor market is expected to witness stable growth from 2026 to 2033, primarily driven by increasing offshore drilling activities and rising investments in North Sea oilfield redevelopment projects. The growing emphasis on environmentally sustainable oilfield chemicals and stricter offshore environmental regulations are accelerating adoption of biodegradable and low-toxicity scale inhibitor formulations. The region is also experiencing increasing deployment of advanced chemical management systems across mature offshore production facilities and subsea infrastructure operations.

U.K. Oilfield Scale Inhibitor Market Insight

The U.K. oilfield scale inhibitor market is expected to witness steady growth from 2026 to 2033, driven by increasing investment in North Sea offshore production optimization and aging oilfield infrastructure management. Operators are increasingly deploying advanced scale inhibitor technologies to reduce maintenance costs and improve production continuity in mature offshore assets. In addition, increasing focus on environmentally compliant offshore chemical treatment systems is expected to support continued market expansion across the U.K. oil and gas industry.

Germany Oilfield Scale Inhibitor Market Insight

The Germany oilfield scale inhibitor market is expected to witness moderate growth from 2026 to 2033, fueled by increasing industrial research activities related to specialty oilfield chemicals and growing investments in sustainable industrial chemistry technologies. Germany’s strong engineering and chemical manufacturing capabilities support development of advanced polymer- and phosphonate-based inhibitor formulations for European energy markets. Rising focus on environmentally responsible chemical technologies is also encouraging innovation across industrial water treatment and oilfield chemical applications.

Asia-Pacific Oilfield Scale Inhibitor Market Insight

The Asia-Pacific oilfield scale inhibitor market is expected to witness the fastest growth rate from 2026 to 2033, supported by increasing offshore exploration projects, expanding refinery infrastructure, and rising oil and gas production activities across China, India, Indonesia, and Australia. The region’s growing energy demand and increasing investments in deepwater drilling operations are accelerating deployment of advanced oilfield production chemicals. Furthermore, increasing government support for domestic hydrocarbon production and upstream energy security initiatives is expanding market opportunities across Asia-Pacific.

Japan Oilfield Scale Inhibitor Market Insight

The Japan oilfield scale inhibitor market is expected to witness gradual growth from 2026 to 2033 due to increasing investments in advanced industrial chemical technologies and offshore energy infrastructure partnerships. Japanese companies are increasingly focusing on developing high-performance and environmentally sustainable specialty chemicals for energy and industrial applications. In addition, growing technological collaboration with offshore oilfield service providers is supporting adoption of efficient scale management solutions across regional offshore projects.

China Oilfield Scale Inhibitor Market Insight

The China oilfield scale inhibitor market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to the country’s expanding offshore drilling activities, rising unconventional gas exploration, and increasing investments in domestic oilfield chemical manufacturing. China continues to strengthen upstream production capabilities through large-scale shale gas and offshore exploration projects, increasing demand for advanced scale inhibition technologies across production systems and pipeline infrastructure. The rapid expansion of domestic energy companies and increasing focus on production efficiency optimization are key factors propelling market growth in China.

Oilfield Scale Inhibitor Market Share

The Oilfield Scale Inhibitor industry is primarily led by well-established companies, including:

- Halliburton Energy Services, Inc. (U.S.)

- Shell International B.V. (Netherlands)

- Schlumberger Limited (U.S.)

- Chevron Phillips Chemical Company LLC (U.S.)

- TechnipFMC plc (U.K.)

- NALCO India. (India)

- Baker Hughes Company (U.S.)

- TotalEnergies (France)

- Titan Oil Recovery (U.S.)

- Equinor ASA (Norway)

- A. HAMON (U.S.)

- CIC Group Inc (U.S.)

- Premier Energies Limited (U.S.)

- Vogt Power International (U.S.)

Latest Developments in Oilfield Scale Inhibitor Market

- In January 2025, SLB completed the acquisition of ChampionX Corporation in a transaction valued at approximately USD 7.8 billion to strengthen its integrated oilfield production and chemical management portfolio. The acquisition combines advanced digital monitoring technologies with large-scale oilfield chemical expertise, enabling predictive scale management and production optimization capabilities. This development is expected to improve operational efficiency, reduce intervention costs, and strengthen SLB’s competitive position within the global oilfield chemicals and production services market.

- In February 2024, BASF announced the expansion of its Basoflux paraffin inhibitor production capacity to address increasing demand from unconventional oil and gas production operations. The investment includes development of advanced solid inhibitor technologies capable of providing controlled and sustained chemical release without continuous injection systems. The expansion is expected to improve operational flexibility for upstream operators while supporting greater adoption of efficient flow assurance technologies across shale and unconventional resource markets.

- In September 2024, Schlumberger Limited launched an advanced digital oilfield platform focused on optimizing scale management operations through machine learning and predictive analytics technologies. The platform provides real-time monitoring of scale formation patterns and supports automated mitigation strategies to improve production continuity and reduce maintenance downtime. The launch reflects the growing industry transition toward digitally integrated oilfield chemical management systems and strengthens the company’s technology-driven service portfolio.

- In July 2024, Clariant AG expanded its Middle East operations through the establishment of a dedicated manufacturing facility for oilfield scale inhibitors designed specifically for regional geological and production conditions. The new facility enhances local production capabilities, improves supply chain responsiveness, and reduces delivery lead times for oilfield operators across the region. The expansion highlights the increasing trend of regionalized chemical manufacturing strategies aimed at improving operational efficiency and supporting rapidly growing Middle Eastern upstream energy projects.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Oilfield Scale Inhibitor Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Oilfield Scale Inhibitor Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Oilfield Scale Inhibitor Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.