Global Open Surgery Instruments Market

Market Size in USD Billion

USD

75.25 Billion

USD

117.42 Billion

2025

2033

USD

75.25 Billion

USD

117.42 Billion

2025

2033

| 2026 - 2033 | |

| USD 75.25 Billion | |

| USD 117.42 Billion | |

| % | |

|

Open Surgery Instruments Market Overview

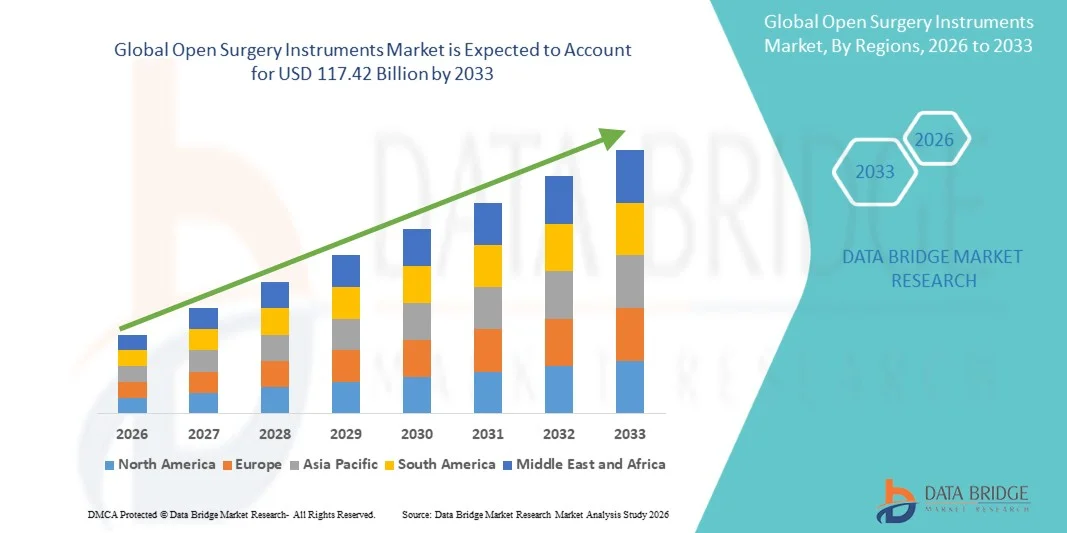

The Open Surgery Instruments Market was valued at USD 75.25 billion in 2025 and is projected to reach USD 117.42 billion by 2033, growing at a CAGR of 5.72% from 2026 to 2033. The market is experiencing consistent growth driven by the rising prevalence of chronic diseases requiring surgical interventions, increasing demand for minimally invasive and advanced surgical procedures, and continuous advancements in surgical instrument technologies. The expanding adoption of precision-based surgical tools, improved healthcare infrastructure, and growing investments in operating room modernization are further supporting market expansion across hospitals and surgical centers globally.

The increasing number of surgical procedures worldwide, combined with the growing burden of cardiovascular, orthopedic, gastrointestinal, and other chronic conditions, is encouraging healthcare providers to adopt advanced open surgery instruments that enhance accuracy, safety, and surgical outcomes. Traditional open surgical instruments continue to play a critical role in complex procedures, while innovations in ergonomic designs, energy-based devices, and high-performance surgical tools are improving efficiency and reducing procedure-related complications. In addition, rising demand for high-quality surgical equipment, increasing hospital capacity expansion, and advancements in surgical techniques are accelerating the adoption of open surgery instruments across developed and emerging markets.

.Key Market Trends & Insights

- North America dominated the Open Surgery Instruments Market with the largest revenue share of 34.26% in 2025, supported by the presence of advanced healthcare infrastructure, high surgical procedure volumes, strong adoption of technologically advanced surgical instruments, and increasing investments in minimally invasive and open surgical techniques.

- The Cardiothoracic Surgery segment dominated the market with a 31.6% share in 2025, supported by the increasing prevalence of cardiovascular diseases and the growing number of cardiac surgical procedures performed worldwide.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 6.9% from 2026 to 2033, fueled by rising healthcare expenditure, increasing surgical procedures, expanding hospital infrastructure, growing medical tourism, and improving access to advanced surgical instruments across China, India, and Japan.

- The Energy Systems segment is projected to be the fastest-growing product category, registering a CAGR of 7.4% during the forecast period, supported by increasing adoption of advanced electrosurgical technologies, improved surgical precision, reduced blood loss, and growing preference for efficient surgical workflows.

- Cardiothoracic Surgery dominated the application segment with a 28.67% revenue share in 2025, driven by the increasing prevalence of cardiovascular diseases, rising demand for complex surgical interventions, and growing utilization of specialized open surgery instruments in cardiac procedures.

- Hospitals accounted for the largest share in the end-user segment with 68.52% revenue share in 2025, supported by high surgical procedure volumes, availability of specialized surgical departments, greater adoption of advanced instruments, and increasing investments in hospital operating room infrastructure.

Market Size & Forecast

- Global Market Value (2025): USD 75.25 Billion

- Expected Market Value (2033): USD 117.42 Billion

- Forecast CAGR (2026–2033): 5.72%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Open Surgery Instruments Market Segmentation

|

Attributes |

Open Surgery Instruments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Johnson & Johnson MedTech (U.S.) |

|

Market Opportunities |

· Rising Number of Surgical Procedures Worldwide · Advancements in Surgical Instrument Technologies · Expansion of Healthcare Infrastructure in Emerging Market |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Open Surgery Instruments Market Trends

Trend: Increasing Adoption of Advanced Surgical Instruments and Precision-Based Surgical Technologies

Hospitals and surgical centers worldwide are increasingly adopting advanced open surgery instruments to improve procedural accuracy, enhance patient outcomes, and reduce surgical complications. The integration of ergonomic designs, advanced materials, energy-based technologies, and precision-engineered instruments is transforming traditional surgical workflows. Surgeons are increasingly utilizing advanced forceps, retractors, energy systems, staplers, and specialized instruments to improve efficiency across complex procedures such as cardiothoracic, orthopedic, and urologic surgeries. In addition, the growing emphasis on surgical safety, infection control, and minimally invasive approaches is encouraging manufacturers to develop next-generation open surgery instruments with improved functionality and reliability.

Open Surgery Instruments Market Dynamics

Key Market Driver: Rising Volume of Surgical Procedures and Increasing Demand for Advanced Surgical Instruments

The growing global burden of chronic diseases, including cardiovascular disorders, cancer, and orthopedic conditions, is significantly increasing the demand for surgical interventions and advanced open surgery instruments. Aging populations, rising healthcare access, and improvements in diagnostic capabilities are contributing to higher surgical procedure volumes worldwide.

Hospitals and ambulatory surgical centers are increasingly investing in advanced surgical tools such as energy systems, surgical staplers, and precision instruments to improve operating room efficiency and clinical outcomes. For instance, the increasing adoption of advanced surgical technologies in cardiac and orthopedic procedures is driving demand for specialized instruments that enable improved precision and reduced procedure time. Furthermore, healthcare modernization programs and increasing hospital infrastructure investments across emerging economies, particularly in Asia-Pacific and Latin America, are supporting market expansion.

Key Restraint/Challenge: High Cost of Advanced Surgical Instruments and Limited Access in Emerging Markets

A major challenge in the Open Surgery Instruments Market is the high cost associated with advanced surgical equipment and specialized instruments. Modern surgical technologies, including energy-based devices, powered instruments, and precision-engineered tools, require significant investment in procurement, sterilization, maintenance, and periodic replacement.

Smaller hospitals and healthcare facilities in developing regions often face budget limitations, restricting access to premium surgical instruments. In addition, variations in healthcare reimbursement policies, limited availability of skilled surgical professionals, and regulatory requirements across different countries create barriers to widespread adoption. The increasing complexity of surgical technologies also requires continuous training and skill development among healthcare professionals, adding to overall operational costs.

Key Market Opportunity: Integration of Robotic Surgery, Advanced Materials, and Smart Surgical Technologies

The integration of robotic-assisted surgery, artificial intelligence, and smart surgical technologies presents a significant growth opportunity for the Open Surgery Instruments market. Advanced instruments designed for robotic platforms and precision-based procedures are gaining traction due to their ability to improve surgical accuracy, enhance visualization, and support complex interventions. For instance, the growing adoption of robotic-assisted surgical systems by hospitals globally is creating demand for compatible advanced instruments, including specialized forceps, scissors, and energy devices. In addition, innovations in materials such as lightweight alloys, antimicrobial coatings, and reusable instrument technologies are improving durability and reducing infection risks. Leading healthcare markets, including North America and Europe, continue to invest heavily in surgical innovation, while countries such as China, India, and Japan are expanding healthcare infrastructure and adopting advanced surgical technologies. These developments are expected to create significant opportunities for manufacturers of open surgery instruments over the forecast period.

Open Surgery Instruments Market Scope

The Open Surgery Instruments market is segmented on the basis of product, application, and end user.

• By Product

On the basis of product, the Open Surgery Instruments Market is segmented into Scalpel, Scissors, Forceps, Clamps, Needles and Suture, Retractors, Suction, Staplers and Clips, Energy Systems, and Laparoscopic Instruments. The Forceps segment dominated the market with a 24.8% share in 2025, owing to its extensive use across a wide range of surgical procedures, including general surgery, cardiovascular surgery, orthopedic procedures, and gynecological interventions. Forceps are essential surgical tools used for grasping, holding, dissecting, and manipulating tissues during operations, making them a fundamental component of surgical instrument sets. Their widespread availability, reusable and disposable variants, and continuous improvements in ergonomic design are supporting segment growth. Increasing surgical volumes globally, rising demand for precision-based procedures, and expansion of hospital infrastructure are further contributing to the dominance of this segment. In addition, advancements in stainless steel quality, enhanced grip mechanisms, and lightweight designs are improving surgical efficiency and reducing surgeon fatigue, strengthening adoption across healthcare facilities.

The Energy Systems segment is expected to witness the fastest growth with a CAGR of 7.2% from 2026 to 2033, driven by increasing adoption of advanced surgical technologies that improve precision, reduce blood loss, and enhance procedural outcomes. Energy-based devices such as electrosurgical instruments, ultrasonic devices, and advanced vessel-sealing systems are gaining popularity due to their ability to provide accurate tissue cutting and coagulation. Growing preference for minimally invasive and precision-guided procedures, increasing surgical complexity, and rising demand for improved operating room efficiency are accelerating segment expansion. In addition, technological advancements in energy delivery systems, integration of smart surgical technologies, and increasing adoption across hospitals and ambulatory surgical centers are creating new growth opportunities. The rising focus on reducing surgery time and improving patient recovery outcomes is expected to further support the rapid growth of energy-based surgical instruments.

• By Application

On the basis of application, the Open Surgery Instruments Market is segmented into Cardiothoracic Surgery, Urologic Surgery, Orthopaedic Surgery, and Robot-Assisted Surgery. The Cardiothoracic Surgery segment dominated the market with a 31.6% share in 2025, supported by the increasing prevalence of cardiovascular diseases and the growing number of cardiac surgical procedures performed worldwide. Open surgery instruments play a critical role in complex heart and thoracic procedures requiring high precision, reliability, and surgical control. Rising cases of coronary artery disease, valve disorders, and other cardiovascular conditions are driving demand for advanced surgical instruments. In addition, increasing investments in specialized cardiac care centers, advancements in surgical techniques, and growing adoption of high-quality surgical tools are strengthening segment growth. The need for durable and precise instruments in critical procedures continues to support the leading position of cardiothoracic surgery applications.

The Robot-Assisted Surgery segment is expected to register the fastest growth with a CAGR of 8.5% from 2026 to 2033, driven by increasing adoption of robotic surgical platforms and growing demand for enhanced surgical accuracy and minimally invasive approaches. Although traditionally associated with minimally invasive procedures, robotic-assisted surgical systems increasingly rely on advanced surgical instruments and specialized tools to improve precision and control. Rising healthcare investments, increasing availability of robotic surgery systems, and growing surgeon preference for technology-assisted procedures are supporting segment expansion. Furthermore, advancements in robotic instrument design, improved visualization technologies, and increasing adoption in complex surgeries are accelerating market growth. The shift toward precision medicine and improved patient outcomes is expected to create significant opportunities for open surgery instrument manufacturers supporting robotic-assisted procedures.

• By End User

On the basis of end user, the Open Surgery Instruments Market is segmented into Hospitals, Ambulatory Surgery Centers, and Clinics. The Hospitals segment dominated the market with a 58.7% share in 2025, owing to the high volume of surgical procedures performed in hospital settings and the availability of advanced operating room infrastructure. Hospitals remain the primary users of open surgery instruments due to their ability to manage complex surgeries across multiple specialties, including cardiovascular, orthopedic, urological, and general surgery. Increasing healthcare expenditure, expansion of multispecialty hospitals, and growing demand for advanced surgical care are supporting segment dominance. In addition, hospitals maintain strong procurement networks and require continuous replacement and upgrading of surgical instruments, contributing to sustained demand. The growing number of surgical interventions and increasing focus on improving patient outcomes further reinforce the leading position of hospitals in the market.

The Ambulatory Surgery Centers segment is expected to witness the fastest growth with a CAGR of 7.8% from 2026 to 2033, driven by the increasing shift toward outpatient surgical procedures and cost-effective healthcare delivery models. Ambulatory surgery centers are gaining popularity due to shorter hospital stays, reduced healthcare costs, and improved patient convenience. Growing adoption of minimally invasive procedures, rising demand for same-day surgeries, and expansion of specialized surgical centers are supporting segment growth. In addition, increasing investments in healthcare infrastructure and the growing preference for efficient surgical care models are encouraging the adoption of advanced surgical instruments in ambulatory settings. The rising focus on reducing healthcare burden and improving operational efficiency is expected to accelerate the growth of this segment during the forecast period.

Open Surgery Instruments Market Regional Analysis

North America dominated the Open Surgery Instruments Market with the largest revenue share of 34.26% in 2025, supported by advanced healthcare infrastructure, high surgical procedure volumes, strong adoption of technologically advanced surgical instruments, and increasing investments in modern operating room technologies. The region benefits from the presence of leading medical device manufacturers, well-established hospital networks, and high adoption of advanced instruments such as energy systems, surgical staplers, precision forceps, and specialized retractors. Growing demand for complex surgical procedures, rising prevalence of chronic diseases, and increasing focus on improving surgical outcomes continue to strengthen North America’s leadership position in the global market.

U.S. Open Surgery Instruments Market Insight

The U.S. Open Surgery Instruments market is witnessing significant growth due to the country’s advanced healthcare ecosystem, increasing number of surgical procedures, and rapid adoption of innovative surgical technologies. Hospitals and ambulatory surgery centers are increasingly investing in advanced surgical instruments to enhance procedural efficiency, reduce complications, and improve patient outcomes. The presence of major medical device companies, strong research and development activities, and growing adoption of robotic-assisted and precision-based surgical technologies are further driving market expansion. In addition, increasing healthcare expenditure and demand for advanced surgical solutions across cardiothoracic, orthopedic, and urologic procedures are supporting market growth.

Europe Open Surgery Instruments Market Insight

The Europe Open Surgery Instruments market remains a major contributor to global revenue, driven by strong healthcare systems, technological innovation, and increasing demand for advanced surgical solutions. Countries across the region are witnessing higher adoption of precision surgical instruments, energy-based devices, and advanced operating room technologies due to rising surgical volumes and growing emphasis on patient safety. Government support for healthcare modernization, increasing investments in medical technology, and the presence of skilled healthcare professionals are enhancing the adoption of Open Surgery Instruments throughout Europe.

U.K. Open Surgery Instruments Market Insight

The U.K. Open Surgery Instruments market is experiencing steady growth, supported by increasing healthcare investments, rising surgical procedures, and growing adoption of advanced surgical technologies across hospitals and specialty care centers. The expansion of ambulatory surgical centers and modernization of healthcare facilities are contributing to demand for efficient and reliable surgical instruments. Furthermore, increasing focus on improving surgical outcomes, reducing hospital stays, and adopting innovative surgical techniques is supporting market growth in the U.K.

Germany Open Surgery Instruments Market Insight

The Germany Open Surgery Instruments market is expanding steadily due to the country’s strong healthcare infrastructure, advanced medical technology sector, and focus on surgical innovation. Hospitals and research institutions are increasingly adopting advanced surgical instruments to support complex procedures and improve clinical efficiency. Continuous advancements in surgical energy systems, precision instruments, and smart surgical technologies, combined with strong investment in healthcare research and development, are further driving market growth in Germany.

Asia-Pacific Open Surgery Instruments Market Insight

The Asia-Pacific Open Surgery Instruments market is expected to witness the fastest growth, registering a CAGR of 6.9% from 2026 to 2033, fueled by rising healthcare expenditure, increasing surgical procedures, expanding hospital infrastructure, growing medical tourism, and improving access to advanced surgical instruments across China, India, and Japan. The region is benefiting from rapid healthcare modernization, increasing investments in specialty hospitals, and growing demand for advanced surgical technologies. In addition, the rising burden of chronic diseases and improving healthcare accessibility are accelerating the adoption of open surgery instruments across emerging economies.

Japan Open Surgery Instruments Market Insight

The Japan Open Surgery Instruments market is witnessing consistent growth due to its advanced healthcare infrastructure, aging population, and increasing demand for high-precision surgical technologies. Hospitals and surgical centers are adopting advanced instruments to improve surgical accuracy, enhance patient outcomes, and support complex procedures. The country’s strong medical technology ecosystem, focus on healthcare innovation, and increasing adoption of advanced surgical solutions are contributing to market expansion.

China Open Surgery Instruments Market Insight

The China Open Surgery Instruments market is growing rapidly, driven by expanding healthcare infrastructure, increasing surgical procedure volumes, rising healthcare expenditure, and government initiatives to improve healthcare accessibility. The country is witnessing increasing adoption of advanced surgical instruments across hospitals and specialty care centers due to growing demand for improved surgical efficiency and outcomes. In addition, investments in medical device innovation, increasing hospital modernization, and the expansion of tertiary healthcare facilities are positioning China as one of the fastest-growing markets for Open Surgery Instruments globally.

Open Surgery Instruments Market Share

The Open Surgery Instruments industry is primarily led by well-established companies, including:

- Moog Inc. (U.S.)

- Dallara (Italy)

- Exail (France)

- IPG Automotive GmbH (Germany)

- aiMotive (Hungary)

- VI‑grade GmbH (Germany)

- Cruden B.V. (Netherlands)

- Dynisma Ltd. (UK)

- Applied Intuition Inc. (U.S.)

- rFpro (rFpro Limited) (England)

- Siemens AG (Germany)

- Dassault Systèmes SE (France)

- MTS Systems Corporation (U.S.)

- CAE Inc. (Canada)

- NVIDIA Corporation (U.S.)

- AB Dynamics PLC (U.K.)

- Forum8 (Japan)

- Mitsubishi Precision Co., Ltd. (Japan)

- FAAC Incorporated (U.S.)

- DriveSafety (U.S.)

- Simtec Simulation Technology GmbH (Germany)

- MB Dynamics Inc. (U.S.)

- Sanlab Simulation (India)

- SimCraft (U.S.)

- CXC Simulations (U.S.)

- XPI Simulation (United Kingdom)

- Tecknotrove Simulator Systems Pvt. Ltd. (India)

- Zhejiang Kechi Intelligent Technology Co., Ltd. (China)

- Shenzhen Zhongzhi Simulation (China)

- Hindustan Simulators (India)

- DriveSimSolutions (U.S.)

- Teksim Technologies (India)

- iMVR Inc. (U.S.)

- SimXperience (U.S.)

Latest Developments in Open Surgery Instruments Market

- In May 2022, Stryker, a leading medical technology company, announced the launch of its EasyFuse Dynamic Compression System for foot and ankle surgical applications. The system uses nitinol technology to provide improved compression strength, ease of use, and reduced surgical complexity. The launch expanded Stryker’s orthopedic surgical instrument portfolio by offering surgeons an advanced fixation solution designed to improve procedural efficiency and patient outcomes

- In September 2022, Stryker announced the launch of its Q Guidance System with Spine Guidance Software, designed to support computer-assisted open and minimally invasive spine procedures. The system combines advanced optical tracking technology with surgical planning capabilities to improve intraoperative guidance, accuracy, and workflow efficiency. This development highlights the growing integration of digital navigation technologies with surgical instruments to enhance precision during complex procedures

- In May 2023, Stryker introduced the Ortho Q Guidance System with Ortho Guidance Software, expanding its advanced surgical navigation solutions for orthopedic procedures. The platform was developed to support hip and knee surgeries by providing improved surgical planning and intraoperative guidance through advanced tracking and software capabilities. The launch reflects the increasing adoption of technology-enabled surgical instruments and navigation systems in orthopedic surgery

- In July 2024, Ethicon, a Johnson & Johnson MedTech company, announced the launch of the ECHELON 3000 Stapler, a next-generation digitally enabled surgical stapling device. The instrument features one-handed powered articulation designed to improve access and control during surgical procedures, with enhanced jaw aperture and articulation capabilities. The launch demonstrates the continued advancement of surgical staplers and instrument technologies aimed at improving precision in both open and minimally invasive procedures

- In May 2024, Ethicon announced the U.S. launch of the ECHELON LINEAR Cutter, an advanced surgical stapling solution incorporating 3D-Stapling Technology and Gripping Surface Technology (GST). The device was developed to improve staple line security and provide surgeons with greater control during tissue management procedures. This innovation highlights the industry trend toward next-generation stapling instruments designed to reduce surgical risks and improve clinical outcomes

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.