Global Orthopedic Surgical Energy Devices Market

Market Size in USD Billion

CAGR :

%

USD

1.18 Billion

USD

2.15 Billion

2025

2033

USD

1.18 Billion

USD

2.15 Billion

2025

2033

| 2026 –2033 | |

| USD 1.18 Billion | |

| USD 2.15 Billion | |

| % | |

|

Global Orthopedic Surgical Energy Devices Market Overview

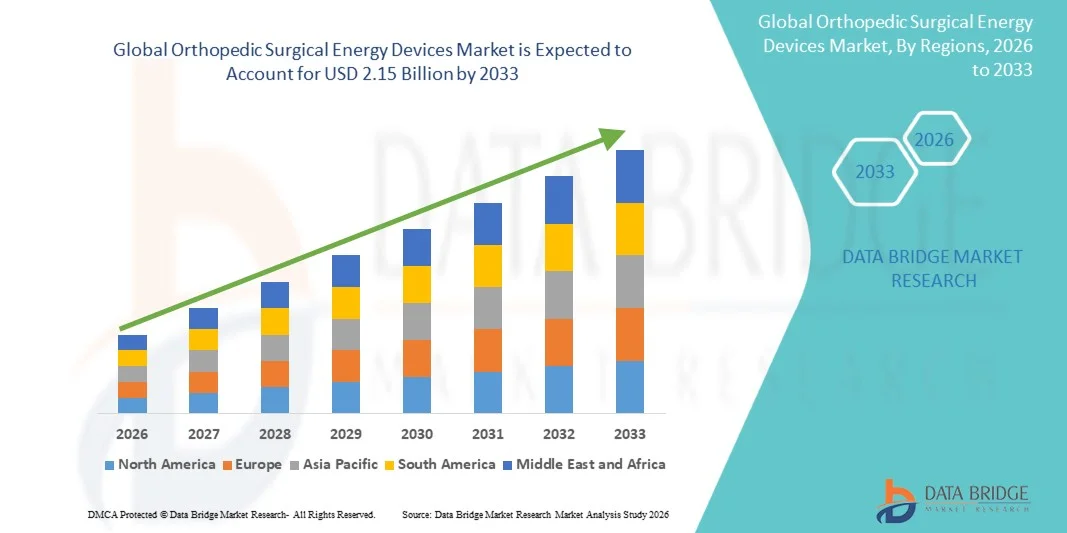

The global orthopedic surgical energy devices market was valued at USD 1.18 billion in 2025 and is projected to reach USD 2.15 billion by 2033, growing at a CAGR of 7.80% from 2026 to 2033. The market is witnessing steady expansion driven by increasing volume of orthopedic surgical procedures, rising prevalence of musculoskeletal disorders, and growing demand for minimally invasive surgical techniques that improve precision and reduce recovery time. Technological advancements in energy-based surgical platforms such as radiofrequency, ultrasonic, and advanced electrosurgical systems are further supporting market adoption across hospitals and ambulatory surgical centers.

The rising burden of osteoarthritis, sports injuries, trauma cases, and an aging global population is significantly increasing the need for orthopedic interventions worldwide. In addition, healthcare providers are increasingly adopting advanced energy devices to enhance surgical accuracy, reduce intraoperative blood loss, and improve patient outcomes. The integration of smart energy systems, improved ergonomic handpieces, and compatibility with robotic-assisted surgical platforms is further accelerating market penetration, particularly in developed healthcare systems with strong investment in surgical innovation and operating room modernization.

Key Market Trends & Insights

- North America dominated the global orthopedic surgical energy devices market with the largest revenue share of 36.28% in 2025, supported by advanced healthcare infrastructure, high adoption of minimally invasive orthopedic procedures, and strong presence of leading medical device companies.

- The Radiofrequency segment led the market by technology with a 39.1% share in 2025, driven by its widespread use in precise tissue cutting, coagulation, and reduced intraoperative blood loss during orthopedic procedures.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.6% from 2026 to 2033, fueled by rising orthopedic procedure volumes, expanding hospital infrastructure, and increasing adoption of advanced surgical technologies in China, India, and Japan.

- The Ultrasound segment is the fastest-growing technology segment, projected to register a CAGR of 7.5%, owing to its ability to enable highly precise cutting with minimal thermal damage and improved post-operative recovery outcomes.

- The Knee application segment dominates the application category with a 42.3% revenue share in 2025, driven by increasing prevalence of osteoarthritis, sports injuries, and rising demand for knee replacement procedures globally.

- Handpieces segment accounts for 61.4% the market in 2025, preferred by recurring usage demand, surgical precision requirements, and continuous innovation in ergonomic and high-performance energy delivery systems.

- The Hip segment is the fastest-growing application category, with a CAGR of 7.2% from 2026 to 2033, driven by growing geriatric population and increasing hip reconstruction surgeries.

Market Size & Forecast

- Global Market Value (2025): USD 1.18 Billion

- Expected Market Value (2033): USD 2.15 Billion

- Forecast CAGR (2026–2033): 7.80%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Global Orthopedic Surgical Energy Devices Market Segmentation

|

Attributes |

Orthopedic Surgical Energy Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Stryker (U.S.) · Medtronic (Ireland) · Johnson & Johnson Services, Inc. (U.S.) · Smith & Nephew (U.K.) · Olympus Corporation (Japan) · B. Braun SE (Germany) · CONMED Corporation (U.S.) · Zimmer Biomet. (U.S.) · Boston Scientific Corporation (U.S.) · Karl Storz SE & Co. KG (Germany) · Erbe Elektromedizin GmbH (Germany) · KLS Martin Group (Germany) · Aesculap AG (Germany) · Applied Medical Resources Corporation (U.S.) · Integra LifeSciences Holdings Corporation (U.S.) · Richard Wolf GmbH (Germany) · Apyx Medical Corporation (U.S.) · BOWA-electronic GmbH & Co. KG (Germany) · Misonix, Inc. (U.S.) · De Soutter Medical (U.K.) |

|

Market Opportunities |

· Rising demand for minimally invasive orthopedic procedures · Increasing adoption of hybrid energy platforms combining radiofrequency and ultrasound technologies · Expansion of ambulatory surgical centers (ASCs) is driving demand for compact, cost-efficient orthopedic surgical energy devices |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Global Orthopedic Surgical Energy Devices Market Trends

Trend: Rising Adoption of Minimally Invasive and Precision Orthopedic Surgeries

Orthopedic surgeons are increasingly adopting energy-based surgical devices such as radiofrequency and ultrasonic systems to perform minimally invasive procedures with higher precision and reduced tissue trauma. These technologies enable accurate soft tissue dissection, improved hemostasis, and faster patient recovery, making them widely used in knee and hip replacement surgeries. For instance, ultrasonic systems such as Stryker’s Sonicision™ and Smith+Nephew’s energy platforms are commonly used in arthroscopic procedures for soft tissue management. Integration with advanced imaging systems and smart surgical handpieces is further enhancing procedural control and outcomes in complex orthopedic interventions.

Global Orthopedic Surgical Energy Devices Market Dynamics

Key Market Driver: Growing Burden of Musculoskeletal Disorders and Rising Surgical Volumes

The increasing prevalence of osteoarthritis, sports injuries, and age-related bone degeneration is significantly driving demand for orthopedic surgical interventions. As the global geriatric population expands, hospitals and surgical centers are performing a higher number of knee and hip replacement procedures, fueling adoption of advanced energy devices. For example, knee arthroplasty procedures using energy-assisted tools are rising in high-volume centers such as the Hospital for Special Surgery (HSS) in the U.S. These systems improve surgical efficiency, reduce intraoperative complications, and support faster postoperative recovery, making them essential tools in modern orthopedic operating rooms.

Key Restraint/Challenge: High Initial Investment Cost of Advanced Simulators

A key restraint in the orthopedic surgical energy devices market is the high acquisition and maintenance cost of advanced systems, particularly ultrasonic and integrated energy platforms. These devices require significant capital investment, along with ongoing costs for consumables, servicing, and staff training. As a result, smaller hospitals and emerging healthcare facilities in cost-sensitive regions face challenges in adopting these technologies despite their clinical advantages. In addition, budget constraints in public healthcare systems further limit widespread penetration.

For instance, advanced ultrasonic surgical handpieces and integrated energy platforms can cost several thousand dollars per unit, while full OR integration systems can require substantial hospital infrastructure upgrades. As a result, smaller hospitals in price-sensitive markets such as rural India or parts of Southeast Asia often rely on conventional electrosurgical tools instead of advanced energy systems. In addition, budget constraints in public healthcare systems further limit widespread penetration.

Key Market Opportunity: Integration of Smart Energy Platforms and Robotic-Assisted Orthopedic Surgery

The integration of intelligent energy modulation systems with robotic-assisted orthopedic surgery presents a major growth opportunity. Platforms such as Stryker’s Mako SmartRobotics and Zimmer Biomet’s ROSA Knee System are increasingly being combined with advanced energy devices to improve surgical precision and consistency. AI-enabled surgical systems can provide real-time tissue feedback, optimize energy delivery, and enhance procedural accuracy during complex joint reconstruction procedures. The growing adoption of digital operating rooms and connected surgical ecosystems is expected to accelerate innovation, enabling safer, more standardized, and highly efficient orthopedic surgeries across developed and emerging markets.

Global Orthopedic Surgical Energy Devices Market Scope

The Orthopedic Surgical Energy Devices market is segmented on the basis of product, technology, application, end user, and distribution channel.

- By Product

On the basis of product, the global orthopedic surgical energy devices market is segmented into handpieces and accessories. The Handpieces segment dominated the market in 2025 with a 61.4% share, owing to their critical role in delivering precise energy during orthopedic procedures such as tissue cutting, coagulation, and ablation. These devices are widely used in knee arthroscopy and hip replacement surgeries, where surgical accuracy and control are essential. Increasing adoption of minimally invasive orthopedic procedures and rising surgical volumes in hospitals are further supporting demand for advanced reusable and disposable handpieces. Manufacturers such as Stryker, Medtronic, and Johnson & Johnson (Ethicon) are continuously innovating ergonomic and smart handpiece systems to improve surgical efficiency and reduce operative time. Integration with energy platforms and compatibility with robotic-assisted surgery systems is further strengthening this segment’s dominance.

The Accessories segment is the fastest-growing, projected to register a CAGR of 7.8% from 2026 to 2033, driven by increasing consumption of single-use components such as electrodes, tips, cables, and probes. The shift toward infection control, sterility standards, and disposable surgical tools is significantly boosting accessory demand across hospitals and ambulatory surgical centers. Rising surgical procedure volumes, particularly in orthopedic trauma and sports injury cases, are further accelerating recurring revenue generation from accessories. In addition, advancements in precision-designed consumables that enhance energy delivery efficiency are expanding their clinical adoption. Emerging markets are also witnessing strong growth due to increasing hospital infrastructure expansion and rising orthopedic surgical capacity.

- By Technology

On the basis of technology, the market is segmented into radiation, radiofrequency, ultrasound, microwave, and others. The Radiofrequency segment dominated the market in 2025 with a 39.1% share, due to its widespread use in soft tissue dissection, hemostasis, and controlled thermal ablation during orthopedic procedures. RF-based systems are highly preferred in knee and hip surgeries for their precision and ability to minimize blood loss. Their compatibility with minimally invasive techniques and proven clinical reliability has made them a standard in modern orthopedic operating rooms. Companies such as Medtronic and Ethicon have strong portfolios of RF-based surgical platforms, further reinforcing market leadership.

The Ultrasound segment is the fastest-growing, projected to register a CAGR of 7.5% from 2026 to 2033, driven by increasing adoption of ultrasonic bone cutting and soft tissue management technologies. Ultrasonic devices provide high precision with minimal thermal damage, making them ideal for complex orthopedic procedures. Growing preference for faster recovery times and reduced postoperative complications is accelerating adoption in hospitals and specialized orthopedic centers. Technological advancements in ultrasonic energy modulation and integration with smart surgical systems are further expanding their clinical applications. Rising use in arthroscopy and minimally invasive joint surgeries is also contributing to strong growth momentum.

- By Application

On the basis of application, the market is segmented into hip and knee. The Knee segment dominated the market in 2025 with a 42.3% share, driven by the high global prevalence of osteoarthritis, sports injuries, and aging-related joint degeneration. Knee replacement and arthroscopic procedures extensively utilize energy-based surgical devices for precise tissue handling and improved surgical outcomes. Hospitals worldwide, including high-volume orthopedic centers such as Hospital for Special Surgery (HSS) in the U.S., report increasing adoption of energy devices in knee procedures. The growing number of partial and total knee arthroplasty procedures is further strengthening segment dominance.

The Hip segment is the fastest-growing, projected to register a CAGR of 7.2% from 2026 to 2033, supported by rising geriatric population and increasing incidence of hip fractures and degenerative hip disorders. Advanced energy devices are increasingly used in hip reconstruction and replacement surgeries to enhance precision and reduce surgical trauma. Improvements in implant technologies and rising surgical accessibility in emerging economies are driving procedure growth. In addition, faster recovery expectations and minimally invasive hip surgery techniques are boosting adoption. Expanding orthopedic infrastructure in Asia-Pacific is further accelerating this segment’s growth.

- By End User

On the basis of end user, the market is segmented into hospitals & clinics, ambulatory surgical centers (ASCs), and others. The Hospitals & Clinics segment dominated the market in 2025 with a 64.7% share, due to high patient inflow, availability of advanced surgical infrastructure, and presence of specialized orthopedic surgeons. Hospitals are the primary centers for complex orthopedic surgeries such as joint replacement and trauma care, where energy devices are extensively used. Strong procurement capabilities and integration of advanced operating room technologies further reinforce this segment’s dominance. Large healthcare networks and academic medical centers are also driving consistent demand.

The Ambulatory Surgical Centers (ASCs) segment is the fastest-growing, projected to register a CAGR of 8.1% from 2026 to 2033, driven by the shift toward outpatient and cost-effective surgical care. ASCs increasingly perform minimally invasive orthopedic procedures that rely on energy devices for precision and reduced recovery time. Lower hospitalization costs, faster patient turnover, and improved surgical efficiency are key growth drivers. Increasing insurance coverage for outpatient orthopedic procedures is also supporting adoption. Expansion of ASC infrastructure in developed markets such as the U.S. is significantly accelerating segment growth.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into direct tender and third-party distributors. The Direct Tender segment dominated the market in 2025 with a 58.9% share, as large hospitals and government healthcare systems prefer direct procurement from manufacturers for cost efficiency, bulk purchasing, and long-term supply agreements. This channel ensures better pricing control and technical support, especially for high-value surgical energy systems. Leading companies such as Stryker and Medtronic actively engage in direct hospital contracts and institutional tenders.

The Third-Party Distributors segment is the fastest-growing, projected to register a CAGR of 7.9% from 2026 to 2033, driven by increasing penetration in emerging markets and smaller healthcare facilities. Distributors play a key role in expanding access to advanced surgical technologies in regions with limited direct manufacturer presence. They provide localized support, faster logistics, and flexible purchasing options for hospitals and clinics. Growth in private healthcare infrastructure across Asia-Pacific, Latin America, and the Middle East is further strengthening this distribution channel.

Global Orthopedic Surgical Energy Devices Market Regional Analysis

North America dominated the global orthopedic surgical energy devices market with the largest revenue share of 36.28% in 2025, supported by advanced healthcare infrastructure, high adoption of minimally invasive orthopedic procedures, and strong presence of leading medical device companies. The region also benefits from a high volume of knee and hip replacement surgeries, strong reimbursement frameworks, and early adoption of advanced surgical technologies such as radiofrequency and ultrasonic energy systems. Increasing integration of robotic-assisted orthopedic platforms and smart surgical energy devices in hospitals further strengthens North America’s leadership position in the global market.

U.S. Orthopedic Surgical Energy Devices Market Insight

The U.S. orthopedic surgical energy devices market is witnessing strong growth due to rising volumes of orthopedic procedures, increasing prevalence of osteoarthritis, and high adoption of minimally invasive surgical techniques. The country’s advanced healthcare infrastructure, strong reimbursement systems, and presence of leading medical device manufacturers such as Stryker, Medtronic, and Johnson & Johnson (Ethicon) are driving market expansion. Increasing integration of radiofrequency and ultrasonic energy systems in knee and hip replacement surgeries, along with growing adoption of robotic-assisted orthopedic platforms, is further accelerating demand across hospitals and ambulatory surgical centers.

Europe Orthopedic Surgical Energy Devices Market Insight

The Europe orthopedic surgical energy devices market remains a major contributor to global revenue, driven by strong healthcare systems, high orthopedic surgical volumes, and increasing adoption of advanced energy-based surgical technologies. The widespread use of minimally invasive orthopedic procedures across Germany, France, and the U.K. is supporting market expansion. Growing investment in surgical innovation, coupled with rising geriatric population and strict clinical standards, continues to enhance adoption of radiofrequency and ultrasonic devices across hospitals and specialized orthopedic centers.

U.K. Orthopedic Surgical Energy Devices Market Insight

The U.K. orthopedic surgical energy devices market is experiencing steady growth, supported by increasing demand for joint replacement procedures and rising adoption of advanced surgical technologies in the National Health Service (NHS) and private hospitals. Growing use of energy-based systems in knee arthroscopy and hip surgeries is improving surgical precision and reducing recovery times. Furthermore, integration of minimally invasive techniques and expanding adoption of robotic-assisted orthopedic platforms are strengthening market growth across the country.

Germany Orthopedic Surgical Energy Devices Market Insight

The Germany orthopedic surgical energy devices market is expanding steadily due to the country’s strong orthopedic care infrastructure, high surgical innovation, and advanced medical device adoption. German hospitals and orthopedic centers are increasingly utilizing radiofrequency and ultrasonic energy systems for complex joint reconstruction and trauma surgeries. Strong focus on clinical efficiency, precision surgery, and aging population-driven demand for hip and knee replacements is further supporting market growth in the country.

Asia-Pacific Orthopedic Surgical Energy Devices Market Insight

The Asia-Pacific orthopedic surgical energy devices market is expected to witness rapid growth, driven by rising orthopedic disease burden, expanding healthcare infrastructure, and increasing adoption of minimally invasive surgical technologies. Countries such as China, India, and Japan are experiencing strong growth in knee and hip replacement procedures. Growing investments in hospital modernization, rising medical tourism, and increasing availability of advanced surgical systems are supporting regional market expansion across both public and private healthcare sectors.

Japan Orthopedic Surgical Energy Devices Market Insight

The Japan orthopedic surgical energy devices market is witnessing consistent growth due to its rapidly aging population, high prevalence of musculoskeletal disorders, and strong focus on advanced surgical care. Japanese hospitals and orthopedic specialists are increasingly adopting ultrasonic and radiofrequency devices for precise, minimally invasive procedures. Integration of robotic-assisted surgery systems and continuous innovation in surgical technologies are further contributing to market expansion across the country.

China Orthopedic Surgical Energy Devices Market Insight

The China orthopedic surgical energy devices market is growing rapidly, driven by rising healthcare investments, increasing orthopedic surgical volumes, and expanding hospital infrastructure. Growing prevalence of osteoarthritis and sports-related injuries is boosting demand for knee and hip procedures. Strong government focus on healthcare modernization, increasing adoption of advanced surgical technologies, and rapid expansion of domestic medical device manufacturing capabilities are positioning China as one of the fastest-growing markets globally.

Global Orthopedic Surgical Energy Devices Market Share

The Orthopedic Surgical Energy Devices industry is primarily led by well-established companies, including:

- Stryker (U.S.)

- Medtronic (Ireland)

- Johnson & Johnson Services, Inc. (U.S.)

- Smith & Nephew (U.K.)

- Olympus Corporation (Japan)

- B. Braun SE (Germany)

- CONMED Corporation (U.S.)

- Zimmer Biomet. (U.S.)

- Boston Scientific Corporation (U.S.)

- Karl Storz SE & Co. KG (Germany)

- Erbe Elektromedizin GmbH (Germany)

- KLS Martin Group (Germany)

- Aesculap AG (Germany)

- Applied Medical Resources Corporation (U.S.)

- Integra LifeSciences Holdings Corporation (U.S.)

- Richard Wolf GmbH (Germany)

- Apyx Medical Corporation (U.S.)

- BOWA-electronic GmbH & Co. KG (Germany)

- Misonix, Inc. (Bioventus Inc.) (U.S.)

- De Soutter Medical (U.K.)

Latest Developments in Global Orthopedic Surgical Energy Devices Market

- In March 2025, researchers developed a pulsating fluid jet system for minimally invasive bone cement removal in orthopedic surgery. The system uses controlled fluid energy to precisely remove bone cement during revision hip and knee procedures, reducing mechanical stress on surrounding bone and soft tissue. It integrates real-time monitoring and adaptive control mechanisms to improve surgical accuracy and safety. This innovation highlights the growing shift toward energy-assisted and non-mechanical approaches in complex orthopedic revisions. The study demonstrates improved procedural efficiency and reduced tissue damage compared to conventional techniques

- In October 2024, researchers introduced an ultrasonic implant monitoring system designed for orthopedic joint replacements. The technology leverages ultrasonic energy signals to assess implant stability and detect early-stage loosening in hip and knee prosthetics. It enables continuous, non-invasive post-surgical monitoring, reducing the risk of late-stage implant failure. This development expands the application of ultrasonic technology beyond surgical use into orthopedic diagnostics. It has potential to significantly reduce revision surgery rates and improve long-term patient outcomes

- In April 2024, Medtronic expanded the deployment of its Valleylab™ FT10 energy platform across healthcare facilities in India. The system enhances surgical energy control, safety, and precision across multiple procedures, including orthopedic surgeries requiring coagulation and soft tissue dissection. It supports minimally invasive techniques widely used in knee and hip procedures. The expansion reflects increasing penetration of advanced electrosurgical systems in emerging markets. It also strengthens Medtronic’s position in energy-based surgical device adoption globally

- In July 2023, Smith+Nephew continued expansion of its advanced energy-based surgical portfolio, including ultrasonic and RF systems used in orthopedic arthroscopy. These systems are widely used for soft tissue management in knee and shoulder procedures, enabling precise dissection with reduced thermal damage. The company’s focus on minimally invasive orthopedic solutions supports faster recovery and improved surgical outcomes. Increasing adoption of these platforms reflects growing demand for precision-driven orthopedic procedures. The development reinforces Smith+Nephew’s leadership in sports medicine and orthopedic surgical technologies

- In May 2022, Stryker advanced its integrated surgical ecosystem by enhancing energy-enabled instruments used in orthopedic operating rooms. The development focused on improving efficiency in joint replacement and arthroscopic procedures through better energy control and instrument ergonomics. These enhancements support high-precision tissue cutting and coagulation during complex knee and hip surgeries. The initiative aligns with broader adoption of smart operating room technologies and robotic-assisted surgery. It further strengthens Stryker’s portfolio in orthopedic surgical energy and minimally invasive systems.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.