Global Orthotic Devices Market

Market Size in USD Billion

CAGR :

%

USD

3.06 Billion

USD

4.57 Billion

2025

2033

USD

3.06 Billion

USD

4.57 Billion

2025

2033

| 2026 - 2033 | |

| USD 3.06 Billion | |

| USD 4.57 Billion | |

| % | |

|

Orthotic Devices Market Overview

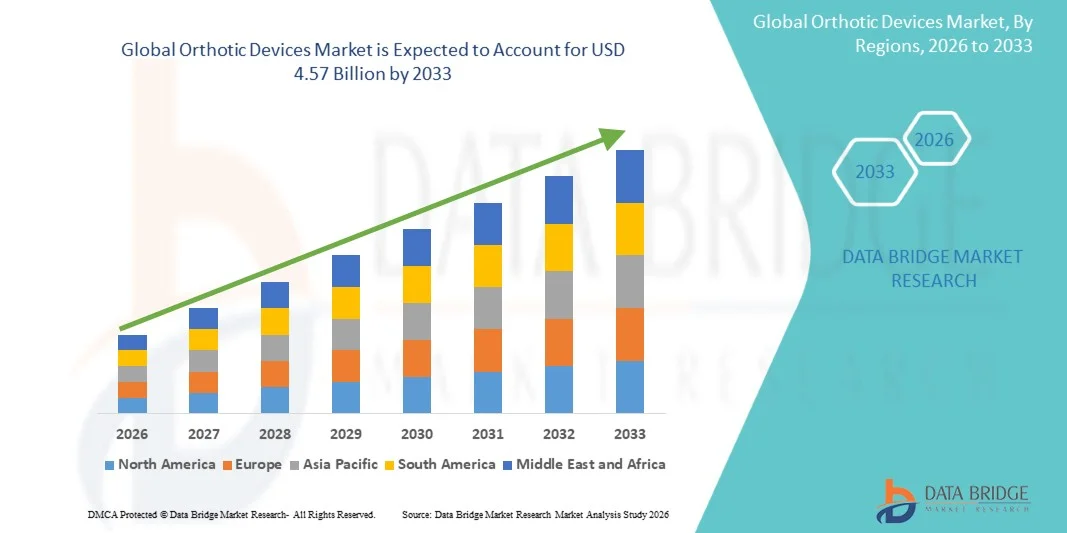

The Orthotic Devices Market was valued at USD 3.06 billion in 2025 and is projected to reach USD 4.57 billion by 2033, growing at a CAGR of 5.15% from 2026 to 2033. The market is witnessing steady growth driven by the rising prevalence of musculoskeletal disorders, increasing incidence of sports injuries, and growing demand for non-invasive treatment solutions for mobility and posture correction.

The expanding geriatric population worldwide, coupled with the increasing burden of conditions such as osteoarthritis, diabetes-related foot complications, and spinal disorders, is accelerating the adoption of advanced orthotic devices. Technological advancements in lightweight materials, 3D printing, and customized orthotic designs are enhancing patient comfort and treatment outcomes. In addition, growing awareness of preventive healthcare, improved access to rehabilitation services, and increasing investments in orthopedic care are supporting market expansion across hospitals, clinics, rehabilitation centers, and home healthcare settings.

Key Market Trends & Insights

- North America dominated the Orthotic Devices Market with the largest revenue share of 36.42% in 2025, supported by advanced healthcare infrastructure, high adoption of orthopedic care solutions, and favorable reimbursement policies.

- The Surgical Devices segment led the market with a 68.42% share in 2025, driven by the increasing number of orthopedic procedures, trauma surgeries, and corrective interventions performed globally.

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 7.4% from 2026 to 2033, fueled by a rapidly aging population, improving healthcare access, and increasing awareness of orthopedic rehabilitation in China, India, and Japan.

- Accessories are the fastest-growing product, projected to register a CAGR of 7.3%, reflecting the surge in demand for supportive components that enhance orthotic functionality and patient comfort.

- The Static Orthotic Devices segment dominated the posture category with a 61.35% revenue share in 2025, led by its extensive use in immobilization, injury recovery, and post-operative support applications.

- Lower Extremity Orthotics accounted for 49.63% of the market, preferred by the rising incidence of lower limb disorders, mobility impairments, diabetic complications, and age-related musculoskeletal conditions.

- The Leather segment is the fastest-growing material category, with a CAGR of 6.9%, driven by rising demand for premium orthotic products offering improved comfort, flexibility, and aesthetic appeal.

Market Size & Forecast

- Global Market Value (2025): USD 3.06 Billion

- Expected Market Value (2033): USD 4.57 Billion

- Forecast CAGR (2026–2033): 5.15%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Orthotic Devices Market Segmentation

|

Attributes |

Orthotic Devices Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Ottobock SE & Co. KGaA (Germany) · Össur hf. (Iceland) · Bauerfeind AG (Germany) · Hanger, Inc. (U.S.) · Enovis Corporation (U.S.) · Blatchford Limited (U.K.) · Thuasne Group (France) · medi GmbH & Co. KG (Germany) · Breg, Inc. (U.S.) · DeRoyal Industries, Inc. (U.S.) · Aspen Medical Products LLC (U.S.) · Fillauer LLC (U.S.) · Orthomerica Products, Inc. (U.S.) · Trulife (Ireland) · Becker Orthopedic (U.S.) · OPTEC USA (U.S.) · Spinal Technology, Inc. (U.S.) · Allard International (Sweden) · Nippon Sigmax Co., Ltd. (Japan) · Tynor Orthotics Pvt. Ltd. (India) |

|

Market Opportunities |

· Expansion of personalized 3D-printed orthotic devices · Rising demand for orthotic support among the aging population · Growing integration of smart sensors and digital monitoring technologies |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Orthotic Devices Market Trends

Trend: Growth in Personalized and 3D-Printed Orthotic Solutions

Healthcare providers and orthopedic specialists are increasingly adopting customized orthotic devices to improve patient comfort, mobility, and treatment effectiveness while reducing fitting errors associated with standard products. The integration of 3D scanning, digital modeling, and additive manufacturing enables precise fabrication tailored to individual anatomical requirements. Hospitals, rehabilitation centers, and specialty clinics are similarly utilizing personalized orthoses to address complex musculoskeletal conditions through data-driven treatment approaches, while advanced materials create lightweight designs that closely match patient-specific functional needs.

For instance, in January 2025, Materialise expanded its patient-specific orthopedic and orthotic solutions portfolio by enhancing digital workflows and 3D printing capabilities for customized mobility support devices.

Orthotic Devices Market Dynamics

Key Market Driver: Rising Prevalence of Musculoskeletal Disorders and Mobility Impairments

The increasing incidence of musculoskeletal disorders and mobility-related conditions has created substantial demand for advanced orthotic devices that can support joint stability, correct biomechanical alignment, and improve functional movement across diverse patient populations. Healthcare providers, rehabilitation centers, and orthopedic clinics are prescribing orthoses as a core component of treatment pathways, reducing complications, accelerating recovery timelines, and enhancing long-term patient outcomes. Growing cases of osteoarthritis, diabetic foot disorders, and sports injuries continue to strengthen demand for clinically effective orthotic interventions worldwide. For instance, in March 2024, Össur introduced new orthopedic bracing and support technologies designed to improve mobility management and rehabilitation outcomes for patients with musculoskeletal conditions.

Key Restraint/Challenge: High Cost of Customized and Advanced Orthotic Devices

A significant restraint in the Orthotic Devices Market is the high cost associated with customized and technologically advanced orthotic solutions. Modern products incorporate precision scanning systems, specialized materials, and individualized manufacturing processes, requiring considerable expenditure for production, fitting, and ongoing clinical adjustments. The overall cost burden extends to follow-up consultations, replacement requirements, and reimbursement limitations, making access challenging for patients in cost-sensitive regions and underfunded healthcare systems. These affordability concerns continue to restrict broader adoption despite the proven clinical benefits of advanced orthotic technologies.

For instance, in 2024, several healthcare providers across developing markets reported reimbursement and affordability barriers for custom orthoses, highlighting ongoing challenges related to patient access and treatment costs.

Key Market Opportunity: Integration of Smart Sensors and Digital Monitoring Technologies

The integration of smart technologies in orthotic devices presents a significant market opportunity. Sensor-enabled platforms can monitor gait patterns, track rehabilitation progress, and provide real-time performance insights while supporting data-driven clinical decision-making. The development of connected orthotic solutions and remote patient monitoring capabilities is further enhancing treatment effectiveness, opening growth opportunities across orthopedic care, rehabilitation services, and home healthcare settings. Advancements in wearable healthcare technologies are also enabling continuous assessment of patient outcomes and personalized therapy optimization. For instance, in September 2024, Ottobock continued expanding its digitally connected orthopedic technologies, supporting data-driven rehabilitation and improved patient mobility management through smart assistive solutions.

Orthotic Devices Market Scope

The orthotic devices market is segmented on the basis of product, posture, product type, device type, manufacturing method, materials, application, end user, and distribution channel.

- By Product

On the basis of product, the Orthotic Devices Market is segmented into surgical devices and accessories. The Surgical Devices segment dominated the market with a 68.42% share in 2025, owing to the increasing number of orthopedic procedures, trauma surgeries, and corrective interventions performed globally. These devices play a critical role in stabilizing musculoskeletal structures and supporting post-surgical rehabilitation. Growing prevalence of degenerative bone disorders and sports injuries continues to drive demand. Healthcare providers increasingly utilize advanced surgical orthotic solutions to improve treatment outcomes and patient recovery rates. Technological advancements in orthopedic surgery are further strengthening adoption. Strong hospital-based utilization continues to support the segment’s leading position.

The Accessories segment is projected to witness the fastest growth at a CAGR of 7.3% from 2026 to 2033, driven by increasing demand for supportive components that enhance orthotic functionality and patient comfort. Accessories such as liners, straps, padding systems, and adjustment components are gaining wider adoption. Growing awareness regarding long-term orthotic maintenance is supporting demand. Manufacturers are introducing advanced materials to improve durability and usability. Rising use of customized orthotic systems is further creating opportunities for accessory sales. Increasing replacement frequency also contributes to strong segment growth.

- By Posture

On the basis of posture, the Orthotic Devices Market is segmented into dynamic orthotic devices and static orthotic devices. The Static Orthotic Devices segment dominated the market with a 61.35% share in 2025, owing to its extensive use in immobilization, injury recovery, and post-operative support applications. These devices provide stability and structural alignment, making them suitable for managing fractures, joint disorders, and musculoskeletal injuries. Healthcare professionals frequently prescribe static orthoses for controlled healing and pain reduction. Their relatively simple design and broad clinical applicability support widespread adoption. Cost-effectiveness compared to advanced dynamic systems further strengthens demand. The segment continues to benefit from growing orthopedic patient volumes globally.

The Dynamic Orthotic Devices segment is expected to register the fastest growth at a CAGR of 7.6% from 2026 to 2033, driven by rising demand for mobility-enhancing and function-restoring orthopedic solutions. These devices enable controlled movement while supporting affected joints and muscles. Technological advancements in smart materials and biomechanical engineering are improving performance and patient outcomes. Dynamic orthoses are increasingly utilized in neurological rehabilitation and sports medicine applications. Growing focus on active recovery approaches is supporting adoption. Rising demand for personalized mobility solutions is expected to accelerate segment expansion.

- By Product Type

On the basis of product type, the Orthotic Devices Market is segmented into ankle braces and supports, foot insoles, knee braces and supports, orthopaedic braces and support, orthotic splints, spinal braces and supports, and upper extremity braces and supports. The Knee Braces and Supports segment dominated the market with a 27.84% share in 2025, owing to the high prevalence of osteoarthritis, ligament injuries, sports-related trauma, and post-operative rehabilitation requirements worldwide. These devices are extensively prescribed to improve joint stability, reduce pain, and enhance mobility among patients of all age groups. Growing participation in sports and physical activities has increased the incidence of knee injuries, supporting demand for preventive and recovery-focused solutions. Hospitals and orthopedic clinics widely utilize knee braces as part of conservative treatment approaches. Technological advancements in lightweight and adjustable brace designs have improved patient comfort and compliance. Their broad clinical applicability continues to make this segment the leading revenue contributor globally.

The Foot Insoles segment is projected to register the fastest growth at a CAGR of 7.8% from 2026 to 2033, driven by increasing awareness regarding foot health, diabetic foot management, and biomechanical correction. These products are increasingly used to address plantar fasciitis, flat feet, heel pain, and posture-related disorders. Rising demand for customized insoles manufactured through digital scanning and 3D printing technologies is accelerating adoption. The growing diabetic population is further creating demand for pressure-relieving and protective insole solutions. Expanding availability through retail and online channels is improving accessibility. Increasing focus on preventive healthcare and daily mobility enhancement is expected to sustain strong growth throughout the forecast period.

- By Device Type

On the basis of device type, the Orthotic Devices Market is segmented into upper extremity orthotics, lower extremity orthotics, and cervical/spinal orthotics. The Lower Extremity Orthotics segment dominated the market with a 49.63% share in 2025, driven by the rising incidence of lower limb disorders, mobility impairments, diabetic complications, and age-related musculoskeletal conditions. These devices are commonly prescribed for the management of ankle, foot, knee, and leg abnormalities. Growing numbers of orthopedic surgeries and rehabilitation procedures continue to support segment demand. Lower extremity orthotics play a critical role in restoring gait function and improving patient independence. Healthcare providers increasingly recommend these products as non-invasive treatment alternatives. Their widespread use across hospitals, rehabilitation centers, and specialty clinics reinforces their market leadership.

The Cervical/Spinal Orthotics segment is expected to witness the fastest growth at a CAGR of 7.4% from 2026 to 2033, supported by increasing cases of spinal disorders, poor posture-related conditions, and degenerative spine diseases. Growing sedentary lifestyles and prolonged screen exposure are contributing to rising demand for spinal support solutions. Technological advancements have enabled the development of more comfortable and anatomically optimized spinal braces. These devices are increasingly utilized during post-surgical recovery and chronic pain management programs. Rising awareness regarding spinal health and early intervention is encouraging adoption. Expanding rehabilitation services globally are further supporting market growth.

- By Manufacturing Method

On the basis of manufacturing method, the Orthotic Devices Market is segmented into custom orthotic devices, custom-fitted orthotic devices, and pre-fabricated orthotic devices. The Custom Orthotic Devices segment dominated the market with a 45.28% share in 2025, owing to its superior fit, enhanced therapeutic effectiveness, and ability to address complex patient-specific conditions. These devices are designed using detailed biomechanical assessments and advanced imaging technologies. Healthcare professionals increasingly prefer customized solutions for chronic orthopedic disorders and rehabilitation programs. Improved patient comfort and better clinical outcomes are strengthening demand across multiple applications. Advancements in digital design software and additive manufacturing technologies have streamlined production processes. The segment continues to benefit from growing emphasis on personalized healthcare solutions.

The Custom-Fitted Orthotic Devices segment is projected to register the fastest growth at a CAGR of 7.5% from 2026 to 2033, driven by the balance it offers between personalization, affordability, and faster delivery timelines. These products can be adjusted according to patient anatomy without requiring fully customized manufacturing. Increasing demand for cost-effective orthopedic care solutions is supporting adoption. Healthcare facilities are increasingly utilizing custom-fitted devices to improve treatment accessibility. Advancements in fitting technologies are enhancing precision and patient satisfaction. Growing demand across emerging economies is expected to contribute significantly to future growth.

- By Material

On the basis of materials, the Orthotic Devices Market is segmented into polypropylene and leather. The Polypropylene segment dominated the market with a 71.56% share in 2025, due to its lightweight properties, durability, affordability, and versatility in orthotic manufacturing. The material offers excellent structural support while maintaining patient comfort during extended use. Polypropylene is widely utilized in lower limb orthoses, spinal braces, and customized orthopedic devices. Its ease of molding and modification supports efficient fabrication processes. Manufacturers favor this material because it enables mass production without compromising functionality. Continuous improvements in polymer technology are further enhancing product performance and durability.

The Leather segment is anticipated to witness the fastest growth at a CAGR of 6.9% from 2026 to 2033, driven by rising demand for premium orthotic products offering improved comfort, flexibility, and aesthetic appeal. Leather-based orthoses are often preferred in applications requiring prolonged wear and enhanced patient acceptance. Increasing consumer preference for durable and breathable materials is supporting adoption. Specialty orthopedic clinics continue to utilize leather in selected support and rehabilitation products. Product innovations combining leather with advanced cushioning materials are improving functionality. Growing demand for patient-centric orthopedic solutions is expected to support future growth.

- By Application

On the basis of application, the Orthotic Devices Market is segmented into chronic diseases, cranio-maxillofacial (CMF), dental, disabilities, hip, injuries, knee, pediatrics, spine, sports injuries, and extremities and trauma (SET). The Knee segment dominated the market with a 24.91% share in 2025, driven by the growing prevalence of osteoarthritis, ligament injuries, and age-related degenerative joint conditions. Knee orthotic devices are extensively used for pain management, rehabilitation, and mobility enhancement. Increasing sports participation and rising obesity rates have contributed to higher incidences of knee disorders globally. Healthcare professionals frequently recommend orthotic interventions as non-surgical treatment options. Technological advancements in brace design and support mechanisms are improving treatment effectiveness. The large patient population continues to sustain strong demand within this segment.

The Sports Injuries segment is expected to register the fastest growth at a CAGR of 7.9% from 2026 to 2033, owing to increasing participation in recreational and professional sports activities worldwide. Athletes increasingly utilize orthotic devices for injury prevention, performance enhancement, and recovery support. Growing awareness regarding sports medicine and rehabilitation is encouraging wider adoption. Technological innovations are enabling the development of lightweight and activity-specific orthoses. Rising investments in fitness and wellness activities are also contributing to segment expansion. The growing emphasis on active lifestyles is expected to maintain strong growth momentum.

- By End User

On the basis of end user, the Orthotic Devices Market is segmented into ambulatory surgical centers, hospitals, and specialty clinics. The Hospitals segment dominated the market with a 58.74% share in 2025, supported by high patient volumes, advanced diagnostic capabilities, and comprehensive orthopedic treatment services. Hospitals serve as primary centers for orthopedic surgeries, trauma care, and rehabilitation programs. They provide access to multidisciplinary teams capable of evaluating and prescribing appropriate orthotic solutions. Increasing orthopedic procedure volumes continue to strengthen demand for orthotic devices within hospital settings. Hospitals also benefit from favorable reimbursement frameworks in several developed markets. Their central role in musculoskeletal care contributes significantly to segment dominance.

The Specialty Clinics segment is projected to witness the fastest growth at a CAGR of 7.2% from 2026 to 2033, driven by increasing demand for specialized orthopedic, rehabilitation, and sports medicine services. These facilities offer focused expertise and personalized treatment approaches for musculoskeletal conditions. Patients increasingly prefer specialty clinics due to shorter waiting times and customized care pathways. Growing availability of advanced fitting and diagnostic technologies is improving treatment outcomes. Expansion of outpatient orthopedic services is supporting market penetration. Rising awareness regarding early intervention and preventive care is further accelerating growth.

- By Distribution Channel

On the basis of distribution channel, the Orthotic Devices Market is segmented into retail outlets, pharmacies, online sales, and orthotic clinics. The Orthotic Clinics segment dominated the market with a 44.37% share in 2025, owing to the specialized assessment, fitting, customization, and follow-up services provided through these facilities. Patients often require professional evaluation to ensure optimal orthotic selection and effectiveness. Orthotic clinics offer access to trained practitioners capable of delivering individualized treatment plans. The increasing demand for customized and complex orthotic devices continues to support clinic-based distribution. Strong integration with rehabilitation and orthopedic care services further enhances their importance. Their ability to provide end-to-end patient support maintains segment leadership.

The Online Sales segment is expected to be the fastest-growing distribution channel at a CAGR of 8.1% from 2026 to 2033, driven by increasing digital healthcare adoption and expanding e-commerce penetration globally. Consumers are increasingly purchasing standardized orthotic products through online platforms due to convenience and product accessibility. Digital channels offer broader product selections and competitive pricing compared to traditional outlets. Manufacturers are investing heavily in direct-to-consumer sales strategies to strengthen market reach. Improved online fitting tools and virtual consultations are enhancing customer confidence. The continued expansion of digital healthcare ecosystems is expected to accelerate segment growth.

Orthotic Devices Market Regional Analysis

North America dominated the Orthotic Devices Market with the largest revenue share of 36.42% in 2025, supported by advanced healthcare infrastructure, high adoption of orthopedic care solutions, and favorable reimbursement policies. The region also benefits from favorable reimbursement policies, increasing prevalence of musculoskeletal disorders, and growing demand for customized and technologically advanced orthotic products. Rising geriatric population levels, strong awareness regarding mobility management, and expanding utilization of orthotic devices across hospitals, rehabilitation centers, and specialty clinics continue to support market growth. Increasing focus on personalized patient care and digital orthotic manufacturing technologies further strengthens North America’s leadership position in the global market.

U.S. Orthotic Devices Market Insight

The U.S. orthotic devices market is witnessing strong growth due to rising prevalence of musculoskeletal disorders, increasing demand for personalized orthopedic care, and growing adoption of advanced rehabilitation technologies. The country’s well-established healthcare infrastructure, along with increasing utilization of custom orthotics, 3D-printed devices, and digital fitting solutions, is driving demand across hospitals, specialty clinics, and rehabilitation centers. In addition, growing emphasis on mobility enhancement and improving patient outcomes is accelerating orthotic device adoption across healthcare providers and orthopedic specialists.

Europe Orthotic Devices Market Insight

The Europe orthotic devices market remains a major contributor to global revenue, driven by strong healthcare systems, technological innovation, and high demand for advanced mobility support solutions. The widespread use of orthotic devices in rehabilitation programs, orthopedic care, and chronic disease management is supporting market expansion across the region. Increasing investments in personalized orthotic technologies, coupled with growing geriatric populations and rising musculoskeletal disorder prevalence, continue to enhance the adoption of orthotic devices throughout Europe.

U.K. Orthotic Devices Market Insight

The U.K. orthotic devices market is experiencing steady growth, supported by rising adoption of advanced orthopedic care solutions, rehabilitation services, and customized orthotic technologies. Increasing investments in digital healthcare infrastructure and growing demand for cost-effective, non-invasive treatment options are contributing to market growth. Furthermore, integration of 3D scanning, additive manufacturing, and biomechanical assessment technologies is improving orthotic performance and patient outcomes, positioning the U.K. as a key innovation hub in the orthotic devices industry.

Germany Orthotic Devices Market Insight

The Germany orthotic devices market is expanding steadily due to the country’s strong healthcare system, advanced manufacturing capabilities, and increasing adoption of next-generation orthopedic technologies. Healthcare providers, rehabilitation centers, and orthopedic specialists are increasingly utilizing orthotic devices for mobility support, injury management, and post-surgical rehabilitation. Continuous advancements in customized orthotic design, lightweight materials, and digital production technologies, along with strong government focus on healthcare quality and patient mobility, are further driving market growth in Germany.

Asia-Pacific Orthotic Devices Market Insight

The Asia-Pacific orthotic devices market is expected to witness rapid growth, driven by increasing aging populations, expanding healthcare infrastructure, and rising investments in orthopedic treatment services across countries such as China, India, and Japan. Growing awareness regarding mobility management, rising adoption of advanced orthotic technologies, and increasing demand for affordable and effective rehabilitation solutions are supporting regional market expansion. In addition, the growing prevalence of chronic musculoskeletal disorders and improving access to healthcare services are accelerating orthotic device adoption across medical and rehabilitation sectors.

Japan Orthotic Devices Market Insight

The Japan orthotic devices market is witnessing consistent growth due to rising investments in rehabilitation technologies, orthopedic innovation, and elderly care services. Healthcare providers, rehabilitation facilities, and orthopedic specialists are increasingly adopting advanced orthotic devices for mobility enhancement, functional recovery, and long-term musculoskeletal management. Moreover, increasing integration of digital manufacturing technologies and the country’s focus on healthy aging and independent living are further contributing to market growth.

China Orthotic Devices Market Insight

The China orthotic devices market is growing rapidly, driven by increasing healthcare expenditure, expanding rehabilitation infrastructure, and rising government focus on disability support and musculoskeletal healthcare. Growing adoption of customized and technologically advanced orthotic devices across hospitals, rehabilitation centers, and specialty clinics is significantly boosting market demand. In addition, rising investments in healthcare modernization, increasing awareness regarding mobility assistance solutions, and rapid technological advancements are positioning China as one of the fastest-growing markets for orthotic devices globally.

Orthotic Devices Market Share

The orthotic devices industry is primarily led by well-established companies, including:

- Ottobock SE & Co. KGaA (Germany)

- Össur hf. (Iceland)

- Bauerfeind AG (Germany)

- Hanger, Inc. (U.S.)

- Enovis Corporation (U.S.)

- Blatchford Limited (U.K.)

- Thuasne Group (France)

- medi GmbH & Co. KG (Germany)

- Breg, Inc. (U.S.)

- DeRoyal Industries, Inc. (U.S.)

- Aspen Medical Products LLC (U.S.)

- Fillauer LLC (U.S.)

- Orthomerica Products, Inc. (U.S.)

- Trulife (Ireland)

- Becker Orthopedic (U.S.)

- OPTEC USA (U.S.)

- Spinal Technology, Inc. (U.S.)

- Allard International (Sweden)

- Nippon Sigmax Co., Ltd. (Japan)

- Tynor Orthotics Pvt. Ltd. (India)

Latest Developments in Orthotic Devices Market

- In June 2025, Ottobock, a global leader in prosthetics, orthotics, and mobility solutions, announced the presentation of new orthotic and neuro-orthotic innovations at the I.S.P.O. World Congress 2025 in Stockholm. The company showcased advanced digital fitting solutions, smart orthopedic technologies, and next-generation mobility support products designed to improve patient outcomes and rehabilitation efficiency. The development highlights the growing integration of digital healthcare technologies within the orthotic devices market

- In March 2025, Surestep, a provider of pediatric orthotic solutions, announced the launch of Sprout3D™, a first-of-its-kind 3D-printed cranial remolding orthosis designed to treat plagiocephaly and brachycephaly. The device utilizes advanced 3D fabrication technologies and extensive clinical data to deliver improved precision, comfort, and treatment effectiveness. This launch reflects the increasing adoption of additive manufacturing and patient-specific orthotic solutions across the healthcare industry

- In March 2025, SUITX by Ottobock, a subsidiary focused on wearable support technologies, introduced the IX BACK VOLTON, an intelligent exoskeleton designed to assist workers in physically demanding industrial and logistics environments. The AI-enabled system provides adaptive power support, helping reduce musculoskeletal strain and workplace injury risks. The launch demonstrates the expanding role of advanced orthotic and wearable assistive technologies beyond traditional healthcare applications

- In August 2024, Össur, a global orthotics and prosthetics company, announced the launch of EmpowerX, an AI-integrated DMEPOS practice and workflow management platform for orthopedic clinics and hospital systems. The solution automates inventory management, insurance verification, product dispensing, and procurement processes to improve operational efficiency and patient care delivery. The development highlights the growing digital transformation trend across the orthotic devices ecosystem

- In October 2023, Blatchford, a leading manufacturer of prosthetic and orthotic technologies, announced the launch of Tectus®, a lightweight microprocessor-controlled orthotic device for individuals with partial lower limb paralysis. The intelligent knee-ankle-foot orthosis (KAFO) incorporates sensor-based technology and advanced gait-support features to improve walking efficiency, comfort, and safety. This innovation reflects the increasing integration of smart technologies into orthotic device development

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.