Global Ovulation Inducing Drugs Market

Market Size in USD Billion

CAGR :

%

USD

4.82 Billion

USD

7.68 Billion

2025

2033

USD

4.82 Billion

USD

7.68 Billion

2025

2033

| 2026 –2033 | |

| USD 4.82 Billion | |

| USD 7.68 Billion | |

| % | |

|

Ovulation Inducing Drugs Market Size

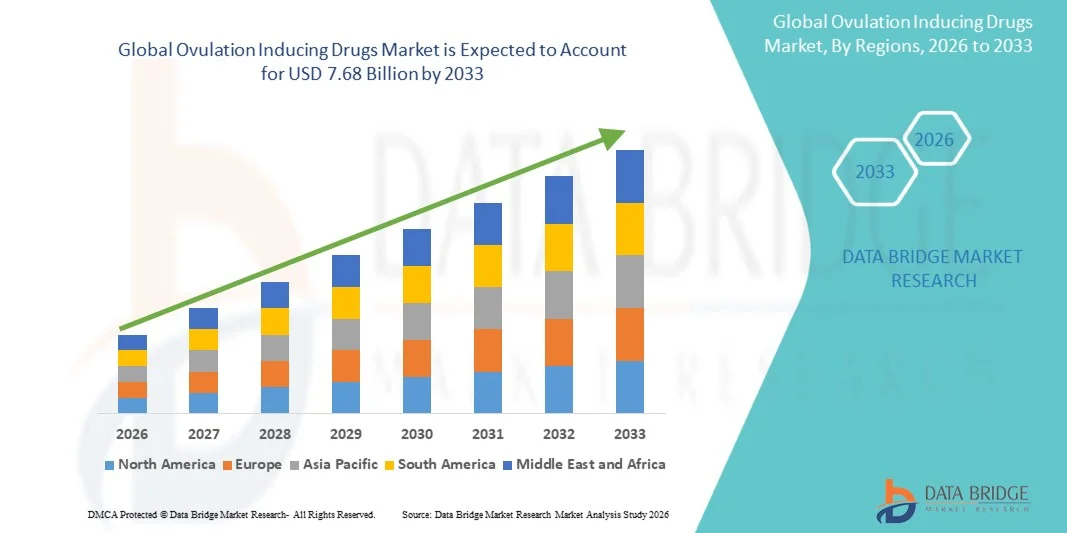

- The global ovulation inducing drugs market size was valued at USD 4.82 billion in 2025and is expected to reach USD 7.68 billion by 2033, at a CAGR of 6.00% during the forecast period

- The market growth is largely fueled by the rising prevalence of infertility cases, delayed pregnancies, and hormonal disorders such as polycystic ovary syndrome (PCOS), which are increasing the demand for ovulation-stimulating therapies across fertility clinics and healthcare systems

- Furthermore, growing awareness regarding assisted reproductive technologies (ART), improved access to fertility treatments, and expanding healthcare infrastructure in emerging economies are driving adoption of ovulation inducing drugs, thereby significantly boosting the industry's growth

Ovulation Inducing Drugs Market Analysis

- Ovulation inducing drugs, used to stimulate ovulation and improve fertility outcomes, are increasingly important in reproductive healthcare settings as they play a key role in treating infertility caused by hormonal imbalance, anovulation, and conditions such as PCOS, while being widely integrated into assisted reproductive technology (ART) protocols

- The escalating demand for ovulation inducing drugs is primarily fueled by rising infertility rates, delayed pregnancies, lifestyle changes affecting hormonal health, and growing acceptance and awareness of fertility treatments including IVF and ovulation induction therapies

- North America dominated the ovulation inducing drugs market with the largest revenue share of 38.7% in 2025, supported by advanced fertility clinic infrastructure, high healthcare expenditure, and strong adoption of reproductive treatment options, with the U.S. leading usage due to well-established ART practices and continuous clinical advancements in fertility management

- Asia-Pacific is expected to be the fastest growing region in the ovulation inducing drugs market during the forecast period due to increasing infertility burden, expanding access to fertility care, rising medical tourism for reproductive treatments, and improving awareness of reproductive health solutions across developing economies

- Parenteral segment dominated the ovulation inducing drugs market with a market share of 54.6% in 2025, driven by its higher clinical efficacy in controlled ovarian stimulation and strong physician preference in assisted reproductive procedures

Report Scope and Ovulation Inducing Drugs Market Segmentation

|

Attributes |

Ovulation Inducing Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

· Expanding adoption of fertility preservation techniques such as egg freezing · Increasing integration of personalized hormone therapy |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Ovulation Inducing Drugs Market Trends

“Rising Adoption of Advanced ART Protocols and Personalized Fertility Treatments”

- A significant and accelerating trend in the global ovulation inducing drugs market is the increasing integration of advanced assisted reproductive technology (ART) protocols and personalized fertility treatment approaches based on hormonal profiling and patient-specific ovulation patterns

- For instance, the use of clomiphene citrate and letrozole in tailored ovulation induction cycles is being widely adopted in fertility clinics to improve ovulation response rates and pregnancy outcomes

- Integration of diagnostic tools such as anti-Müllerian hormone (AMH) testing and ultrasound monitoring is enabling clinicians to optimize drug dosing and timing, thereby improving treatment precision and success rates in infertility management

- Furthermore, combination therapy approaches using gonadotropins with oral ovulation agents are increasingly being utilized to enhance follicular development and maximize reproductive efficiency in complex infertility cases

- Growing use of digital fertility tracking tools and AI-assisted cycle monitoring is further enhancing treatment planning accuracy and improving patient outcomes in ovulation induction therapies

- This shift toward more individualized and protocol-driven fertility treatment strategies is reshaping clinical practice standards and improving overall success rates of ovulation induction therapies

- The growing demand for evidence-based, customized fertility solutions is rapidly expanding across both developed and emerging healthcare markets, as patients increasingly seek higher success rates in conception treatments

Ovulation Inducing Drugs Market Dynamics

Driver

“Rising Infertility Rates and Expanding Fertility Treatment Accessibility”

- The increasing prevalence of infertility cases driven by lifestyle changes, delayed pregnancies, and hormonal disorders such as PCOS is a major factor driving demand for ovulation inducing drugs globally

- For instance, growing utilization of ovulation induction therapies in fertility clinics and hospitals is being supported by expanding reimbursement coverage and improved access to reproductive healthcare services

- As more couples seek medical assistance for conception, ovulation inducing drugs are becoming a first-line treatment option in early-stage infertility management protocols

- Furthermore, increasing awareness campaigns and government initiatives promoting reproductive health are encouraging early diagnosis and treatment of ovulatory disorders

- Expansion of telemedicine-based fertility consultations is also improving access to ovulation induction treatments in remote and underserved regions

- Rising investment in reproductive healthcare infrastructure in emerging economies is further strengthening availability and adoption of fertility drugs worldwide

- The rising establishment of specialized fertility centers in urban and semi-urban regions is further strengthening accessibility and adoption of these drugs across diverse populations

- The growing acceptance of medical intervention for infertility is significantly contributing to sustained market expansion across global healthcare systems

Restraint/Challenge

“Adverse Hormonal Side Effects and Regulatory Approval Complexity”

- Concerns related to hormonal side effects such as ovarian hyperstimulation syndrome (OHSS), mood fluctuations, and multiple pregnancy risks pose a significant challenge to the broader adoption of ovulation inducing drugs

- For instance, the clinical monitoring requirements associated with gonadotropin-based therapies increase treatment complexity and limit their unsupervised or widespread use

- Strict regulatory approval processes and variability in drug approval timelines across different countries also delay the introduction of newer fertility-enhancing therapeutics into the market

- Furthermore, high treatment costs associated with repeated ovulation induction cycles can limit accessibility for patients in low- and middle-income regions

- Limited awareness and stigma associated with infertility treatments in certain developing regions can also reduce early adoption of ovulation induction therapies

- Dependence on repeated clinical visits and ultrasound monitoring increases patient burden and reduces convenience compared to other long-term therapeutic options

- The need for continuous medical supervision and diagnostic monitoring adds to the overall treatment burden, reducing patient compliance in long-term therapy cycles

- Addressing safety concerns through improved drug formulations, better clinical guidelines, and enhanced affordability will be critical for sustained market growth

Ovulation Inducing Drugs Market Scope

The market is segmented on the basis of drug class, route of administration, end-users, and distribution channel.

- By Drug Class

On the basis of drug class, the ovulation inducing drugs market is segmented into hormones and therapeutics drugs. The hormones segment dominated the market with the largest market revenue share of 61.3% in 2025, driven by their critical role in regulating ovarian function and stimulating follicular development in infertility treatments. Hormonal agents such as gonadotropins and selective estrogen receptor modulators are widely used in clinical practice due to their high efficacy in controlled ovulation induction protocols. The segment also benefits from strong clinical validation and standardized treatment guidelines across fertility clinics and hospitals. In addition, increasing prevalence of PCOS and anovulation disorders continues to support consistent demand for hormone-based therapies. Growing physician preference for predictable outcomes in assisted reproductive procedures further reinforces segment dominance. Expanding accessibility of hormonal fertility drugs in emerging markets is also contributing to sustained revenue growth.

The therapeutics drugs segment is anticipated to witness the fastest growth rate of 9.8% from 2026 to 2033, fueled by increasing development of novel non-hormonal and adjunct fertility treatment options. Rising research into safer alternatives with fewer side effects is encouraging adoption of therapeutic drugs in infertility management. These drugs are increasingly being used in combination therapies to enhance ovulation response and improve pregnancy success rates. Furthermore, growing demand for personalized fertility treatment is accelerating innovation in targeted therapeutic approaches. Expanding clinical trials and pipeline drug development activities are strengthening future market prospects. Increasing patient preference for lower-risk treatment options is also supporting rapid segment expansion.

- By Route of Administration

On the basis of route of administration, the ovulation inducing drugs market is segmented into oral, parenteral, and others. The parenteral segment dominated the market with a market share of 54.6% in 2025, driven by its high clinical effectiveness in controlled ovarian stimulation and its essential role in advanced fertility treatments such as IVF and IUI procedures. Injectable therapies, particularly gonadotropins, are widely preferred by fertility specialists due to their ability to provide precise hormonal control and predictable ovarian response. The segment is strongly supported by increasing adoption of assisted reproductive technologies globally, where injectable drugs are considered standard in stimulation protocols. Rising success rates associated with parenteral administration further reinforce physician preference in complex infertility cases

The oral segment is expected to witness the fastest growth rate of 10.5% from 2026 to 2033, driven by its non-invasive nature, affordability, and widespread use as first-line therapy in early-stage infertility treatment. Oral drugs such as clomiphene citrate and letrozole are increasingly preferred for initial ovulation induction due to ease of administration and minimal clinical supervision requirements. Growing awareness of infertility treatment options and early diagnosis of ovulatory disorders is supporting increased adoption of oral therapies. Expanding access through retail and hospital pharmacies further strengthens market penetration

- By End-Users

On the basis of end-users, the ovulation inducing drugs market is segmented into hospitals, homecare, specialty clinics, and others. The specialty clinics segment dominated the market with the largest market revenue share of 47.2% in 2025, driven by the high concentration of assisted reproductive procedures performed in fertility-focused centers. Specialty clinics offer advanced diagnostic capabilities and personalized treatment protocols, making them the primary setting for ovulation induction therapies. Increasing number of IVF cycles and fertility consultations is further strengthening demand in this segment. Availability of trained reproductive endocrinologists enhances treatment outcomes and patient trust. Growing patient preference for specialized fertility care over general hospitals is also contributing to dominance. Expanding network of fertility clinics in urban regions is supporting continued market leadership.

The homecare segment is anticipated to witness the fastest growth rate of 11.2% from 2026 to 2033, fueled by increasing adoption of self-administered oral therapies and rising preference for convenient treatment options. Patients undergoing early-stage ovulation induction are increasingly managing therapy at home under medical guidance. Advancements in telemedicine and remote fertility monitoring are supporting this shift. Growing awareness of at-home fertility management is improving treatment accessibility in remote areas. Reduced hospital visits and lower overall treatment burden are key factors driving adoption. Increasing availability of patient-friendly drug formulations is further accelerating segment growth.

- By Distribution Channel

On the basis of distribution channel, the ovulation inducing drugs market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with the largest market revenue share of 49.5% in 2025, driven by the high volume of prescriptions generated through fertility clinics and hospital-based reproductive units. Hospital pharmacies ensure controlled dispensing of hormonal and injectable fertility drugs under medical supervision. Strong integration with assisted reproductive procedures supports consistent demand in this channel. Availability of specialist guidance within hospitals enhances patient compliance and treatment accuracy. Increasing number of fertility treatments performed in hospital settings further strengthens this segment. Established procurement systems and drug availability also contribute to market leadership.

The online pharmacy segment is expected to witness the fastest growth rate of 13.4% from 2026 to 2033, driven by rising digital healthcare adoption and increasing preference for convenient drug delivery services. Patients are increasingly purchasing fertility medications through verified e-pharmacy platforms due to ease of access and privacy considerations. Growth of teleconsultation services is further supporting online prescription fulfillment. Expanding internet penetration and smartphone usage are boosting digital healthcare adoption in emerging markets. Competitive pricing and doorstep delivery services are also encouraging consumer shift toward online channels. Strengthening regulatory frameworks for online drug sales is further supporting segment expansion.

Ovulation Inducing Drugs Market Regional Analysis

- North America dominated the ovulation inducing drugs market with the largest revenue share of 38.7% in 2025, supported by advanced fertility clinic infrastructure, high healthcare expenditure, and strong adoption of reproductive treatment options

- Patients and healthcare providers in the region increasingly prefer ovulation inducing drugs due to their proven clinical effectiveness, widespread availability, and integration into standardized fertility treatment protocols across specialty clinics and hospitals

- This widespread adoption is further supported by high healthcare expenditure, strong insurance coverage for fertility treatments in several cases, and a technologically advanced clinical ecosystem enabling precise diagnosis and treatment of ovulatory disorders, establishing the region as a key hub for fertility drug utilization

U.S. Ovulation Inducing Drugs Market Insight

The U.S. ovulation inducing drugs market captured the largest revenue share within North America in 2025, driven by rapid adoption of advanced fertility treatments and a high incidence of infertility linked to lifestyle changes, delayed pregnancies, and hormonal disorders. Patients in the country increasingly rely on ovulation induction therapies as a first-line and adjunct treatment in assisted reproductive procedures such as IVF and IUI. Strong presence of leading fertility clinics and continuous innovation in reproductive endocrinology are further supporting market growth. In addition, high awareness of fertility preservation options and favorable insurance coverage in select cases are enhancing accessibility to treatment. The integration of digital health tools and precision medicine approaches is also improving treatment outcomes and expanding adoption of ovulation inducing drugs.

Europe Ovulation Inducing Drugs Market Insight

The Europe ovulation inducing drugs market is projected to expand at a steady CAGR throughout the forecast period, primarily driven by rising infertility rates, delayed childbearing trends, and increasing acceptance of assisted reproductive technologies. Strong regulatory frameworks and well-established healthcare systems are supporting safe and standardized use of fertility drugs across the region. Growing government initiatives promoting reproductive health awareness are further encouraging early diagnosis and treatment of ovulatory disorders. In addition, increasing availability of fertility clinics and rising demand for ART procedures are contributing to sustained market growth across both Western and Eastern Europe.

U.K. Ovulation Inducing Drugs Market Insight

The U.K. ovulation inducing drugs market is anticipated to grow at a notable CAGR during the forecast period, driven by increasing infertility cases and rising demand for assisted reproductive treatments. Strong presence of specialized fertility centers and publicly supported healthcare access are facilitating wider adoption of ovulation induction therapies. Growing awareness of reproductive health and increasing preference for early-stage fertility intervention are further supporting market expansion. In addition, lifestyle-related hormonal imbalances and delayed pregnancies are contributing to higher demand for ovulation inducing drugs in the country.

Germany Ovulation Inducing Drugs Market Insight

The Germany ovulation inducing drugs market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of infertility treatments and strong demand for advanced reproductive healthcare solutions. The country’s well-developed healthcare infrastructure and focus on clinical precision are supporting widespread adoption of hormone-based fertility therapies. Rising cases of age-related infertility and delayed parenthood are further contributing to market growth. In addition, strong emphasis on regulated and evidence-based treatment approaches is enhancing patient confidence in ovulation induction therapies.

Asia-Pacific Ovulation Inducing Drugs Market Insight

The Asia-Pacific ovulation inducing drugs market is poised to grow at the fastest CAGR of 11.6% from 2026 to 2033, driven by rising infertility rates, increasing urbanization, and improving access to fertility healthcare services in countries such as China, India, and Japan. Growing awareness of reproductive health and expanding acceptance of assisted reproductive technologies are significantly boosting market demand. Rapid development of healthcare infrastructure and rising medical tourism for fertility treatments are further accelerating growth. In addition, government initiatives supporting maternal and reproductive health are enhancing adoption of ovulation inducing drugs across the region.

Japan Ovulation Inducing Drugs Market Insight

The Japan ovulation inducing drugs market is gaining momentum due to declining birth rates, delayed pregnancies, and increasing reliance on assisted reproductive technologies. The country’s advanced healthcare system and strong focus on precision medicine are supporting widespread adoption of fertility treatments. Growing use of hormonal therapies in IVF cycles and fertility preservation procedures is further driving market expansion. In addition, increasing awareness of reproductive health and integration of advanced diagnostic tools are improving treatment outcomes in the country.

India Ovulation Inducing Drugs Market Insight

The India ovulation inducing drugs market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rising infertility rates, rapid urbanization, and increasing awareness of fertility treatments. Expanding fertility clinic networks and improving access to reproductive healthcare services are significantly driving market growth. Increasing prevalence of lifestyle-related hormonal disorders is further boosting demand for ovulation induction therapies. In addition, availability of cost-effective treatment options and growing adoption of assisted reproductive technologies are strengthening market penetration across urban and semi-urban regions.

Ovulation Inducing Drugs Market Share

The Ovulation Inducing Drugs industry is primarily led by well-established companies, including:

- Merck & Co., Inc. (U.S.)

- Ferring Pharmaceuticals (Switzerland)

- Bayer AG (Germany)

- Novartis AG (Switzerland)

- Pfizer Inc. (U.S.)

- AbbVie Inc. (U.S.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Sanofi (France)

- AstraZeneca (U.K.)

- Sun Pharmaceutical Industries Ltd. (India)

- Dr. Reddy’s Laboratories Ltd. (India)

- Cipla Limited (India)

- Zydus Lifesciences Limited (India)

- Lupin Limited (India)

- Glenmark Pharmaceuticals Ltd. (India)

- Abbott (U.S.)

- Endo International plc (Ireland)

- Organon & Co. (U.S.)

- Serono Inc. (Switzerland)

- Eli Lilly and Company (U.S.)

What are the Recent Developments in Global Ovulation Inducing Drugs Market?

- In January 2026, ESHRE (European Society of Human Reproduction and Embryology) updated its ovarian stimulation guidelines, reinforcing the use of individualized gonadotropin-based protocols for controlled ovarian stimulation in IVF cycles. The updated recommendations emphasize personalized dosing strategies to improve follicular response while minimizing risks such as ovarian hyperstimulation syndrome (OHSS)

- In June 2025, new clinical evidence published in peer-reviewed reproductive medicine journals reaffirmed that letrozole demonstrates higher ovulation and live birth rates compared to clomiphene citrate in women with polycystic ovary syndrome (PCOS). The findings also highlighted reduced risk of multiple pregnancies, strengthening letrozole’s position as a first-line oral ovulation inducing drug

- In March 2025, a large-scale systematic review and meta-analysis reported that combination therapy using letrozole and clomiphene citrate significantly improves ovulation and pregnancy rates in patients with clomiphene-resistant PCOS. The study indicated that dual therapy enhances follicular development and overall reproductive outcomes compared to monotherapy approaches.

- In September 2024, a comprehensive review involving more than 75,000 patients confirmed that letrozole outperforms clomiphene citrate in terms of ovulation induction success rates and pregnancy outcomes. The analysis also highlighted improved endometrial receptivity associated with letrozole use, supporting its growing global preference in infertility treatments

- In May 2021, randomized controlled clinical trials demonstrated that letrozole is more effective than clomiphene citrate for inducing ovulation in women with PCOS, resulting in higher ovulation rates and improved pregnancy outcomes. These findings played a key role in changing clinical practice trends toward aromatase inhibitors as preferred ovulation inducing agents

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.