Global Personal Health Apps Market

Market Size in USD Billion

CAGR :

%

USD

26.70 Billion

USD

64.24 Billion

2025

2033

USD

26.70 Billion

USD

64.24 Billion

2025

2033

| 2026 –2033 | |

| USD 26.70 Billion | |

| USD 64.24 Billion | |

| % | |

|

Personal Health Apps Market Overview

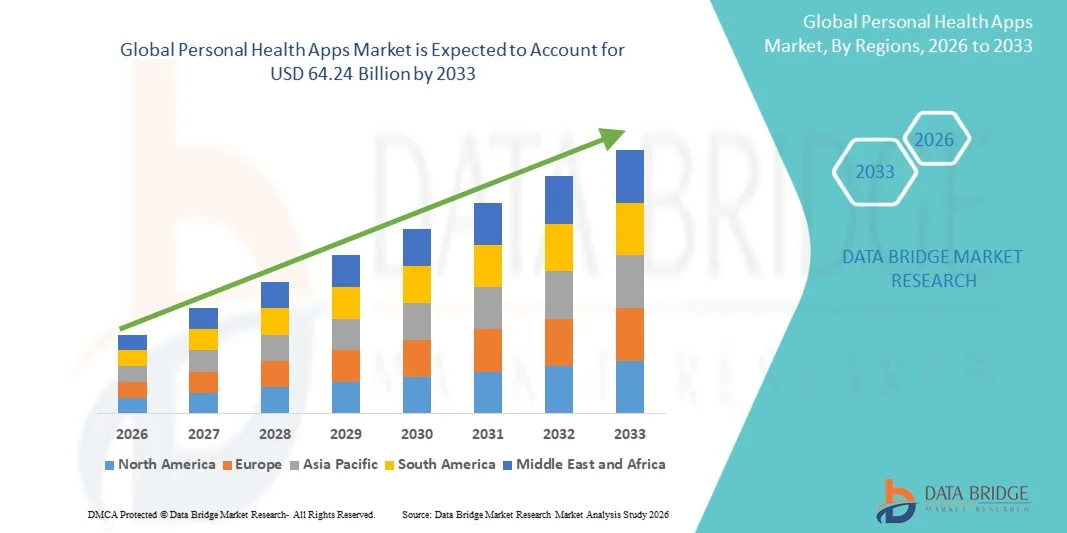

The global personal health apps market was valued at USD 26.70 billion in 2025 and is projected to reach USD 64.24 billion by 2033, growing at a CAGR of 11.6% from 2026 to 2033. The market is experiencing consistent growth driven by rising consumer focus on preventive healthcare, increasing smartphone penetration, and the rapid adoption of digital wellness and fitness tracking solutions across global populations.

The growing prevalence of chronic diseases, combined with a shift toward self-managed healthcare and remote monitoring, is accelerating the adoption of personal health applications. Integration of AI, wearable devices, and cloud-based health platforms is further enhancing real-time health tracking, personalized insights, and user engagement. In addition, increasing awareness of mental health, fitness management, and lifestyle optimization is supporting widespread usage across both developed and emerging markets.

Key Market Trends & Insights

- North America dominated the global personal health apps market with the largest revenue share of 38.42% in 2025, supported by high smartphone penetration, advanced digital health infrastructure, and strong adoption of fitness and chronic care management apps.

- The Fitness Apps segment led the market with a 44.18% share in 2025, driven by rising health awareness, increasing adoption of wearable devices, and growing demand for daily activity tracking and lifestyle management solutions

- Asia-Pacific is expected to be the fastest-growing region at a CAGR of 13.4% from 2026 to 2033, fueled by rapid digitalization, expanding middle-class population, and increasing adoption of mobile-based preventive healthcare solutions in India, China, and Southeast Asia.

- Medical Apps are the fastest-growing app type, projected to register a CAGR of 13.8%, reflecting the surge in demand for chronic disease management, telehealth integration, and remote patient monitoring solutions.

- The Fitness Solutions segment dominated the application category with a 42.65% revenue share in 2025, led by growing consumer focus on physical activity tracking, calorie management, and personalized workout programs.

- Google Play Store accounted for 57.36% of the market, preferred by widespread Android smartphone penetration, affordability of devices, and strong user base across emerging economies.

- The Monitoring Services segment is the fastest-growing application category, with a CAGR of 14.5%, driven by rising demand for continuous health tracking and early detection of health abnormalities.

Market Size & Forecast

- Global Market Value (2025): USD 26.70 Billion

- Expected Market Value (2033): USD 64.24 Billion

- Forecast CAGR (2026–2033): 11.6%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia Pacific

Report Scope and Global Personal Health Apps Market Segmentation

|

Attributes |

Personal Health Apps Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· MyFitnessPal, Inc. (U.S.) · Fitbit LLC (U.S.) · Apple Inc. (U.S.) · Samsung Electronics Co., Ltd. (South Korea) · Google LLC (U.S.) · Strava, Inc. (U.S.) · Headspace Health, Inc. (U.S.) · Calm.com, Inc. (U.S.) · Flo Health, Inc. (U.K.) · Noom, Inc. (U.S.) · Oura Health Ltd (Finland) · WHOOP, Inc. (U.S.) · Nike, Inc. (U.S.) · Garmin Ltd. (Switzerland) · Withings (France) · Lifesum AB (Sweden) · Sleep Cycle AB (Sweden) · Zwift, Inc. (U.S.) · WW International, Inc. (U.S.) · MyNetDiary Inc. (U.S.) |

|

Market Opportunities |

· Integration with wearable ecosystems and IoT health devices · Expansion of AI-driven preventive healthcare models is enabling predictive risk scoring and early intervention features · Growing adoption of employer-sponsored wellness programs |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Global Personal Health Apps Market Trends

Trend: Rise of AI-Driven Personalized Health and Continuous Wellness Tracking

Personal health apps are increasingly leveraging artificial intelligence and connected wearable devices to deliver real-time, highly personalized health insights across fitness, nutrition, sleep, and mental wellness domains. These platforms continuously process user-generated biometric and behavioral data to offer adaptive recommendations, predictive health alerts, and automated wellness coaching experiences. For instance, platforms such as Apple Health, Fitbit, and Samsung Health are integrating AI-driven insights to create seamless, always-on digital health monitoring ecosystems for users.

Global Personal Health Apps Market Dynamics

Key Market Driver: Growing Shift Toward Preventive and Self-Managed Healthcare

The increasing global focus on preventive healthcare and self-directed wellness management is driving strong adoption of personal health apps as users seek convenient tools for tracking fitness, chronic conditions, and overall lifestyle health. Rising healthcare costs and limited access to traditional healthcare services in many regions are further accelerating reliance on mobile-based health monitoring and digital wellness solutions. For instance, widely used applications such as MyFitnessPal, Google Fit, and Flo Health support users in managing daily health routines, nutrition, and condition-specific tracking.

Key Restraint/Challenge: Data Privacy Risks and Regulatory Compliance Complexity

A key challenge in the personal health apps market is the growing concern over data privacy, cybersecurity risks, and stringent regulatory frameworks governing sensitive health and biometric information. Increasing scrutiny from regulators and users regarding data collection, storage, and third-party sharing practices is creating compliance burdens for app developers and limiting trust in digital health platforms. For instance, several health app providers operating under GDPR and HIPAA frameworks face restrictions and audits that impact feature expansion and cross-border data utilization.

Key Market Opportunity: Expansion of AI-Enabled Preventive Care and Employer Wellness Ecosystems

The integration of AI-driven predictive analytics and preventive care models presents a strong opportunity for personal health apps to shift from reactive tracking to early disease risk detection and continuous health optimization. At the same time, increasing adoption of employer-sponsored wellness programs and insurance-linked digital health platforms is creating large-scale B2B growth avenues for user engagement and long-term retention. For instance, corporate wellness platforms integrated with apps such as Virgin Pulse and Fitbit Health Solutions are being widely used to improve employee productivity, reduce healthcare costs, and support personalized preventive health management.

Global Personal Health Apps Market Scope

The Personal Health Apps market is segmented on the basis of app type, application, and platform.

- By App Type

On the basis of app type, the global personal health apps market is segmented into medical apps and fitness apps. The Fitness Apps segment dominated the market with a 44.18% share in 2025, driven by rising health awareness, increasing adoption of wearable devices, and growing demand for daily activity tracking and lifestyle management solutions. These apps are widely used for weight management, exercise tracking, and nutrition planning across both developed and emerging economies. Integration with smartwatches and fitness bands has significantly improved user engagement and retention rates. Continuous gamification features and AI-based coaching are further strengthening adoption. Expanding corporate wellness programs are also boosting usage among working populations. The segment benefits from strong consumer preference for preventive and non-clinical health management tools.

The Medical Apps segment is expected to witness the fastest growth at a CAGR of 13.8% from 2026 to 2033, driven by increasing demand for chronic disease management, telehealth integration, and remote patient monitoring solutions. These apps support users in tracking conditions such as diabetes, hypertension, and cardiovascular disorders. Rising healthcare digitization and physician adoption of mobile health tools are further accelerating growth. Integration with electronic health records and connected medical devices is enhancing clinical utility. Increasing aging population and chronic disease burden are key demand drivers. The segment is also benefiting from regulatory support for digital health solutions across multiple regions.

- By Application

On the basis of application, the global personal health apps market is segmented into monitoring services, fitness solutions, diagnostic services, treatment services, and others. The Fitness Solutions segment dominated the market with a 42.65% share in 2025, supported by growing consumer focus on physical activity tracking, calorie management, and personalized workout programs. These solutions are widely integrated with wearable devices and mobile platforms, enabling continuous health tracking and behavioral insights. Increasing adoption of AI-based fitness coaching and virtual training programs is further enhancing user engagement. Social fitness communities and gamified challenges are also driving higher retention rates. Rising obesity levels and sedentary lifestyles are contributing significantly to demand. The segment benefits from strong consumer-driven adoption across global markets.

The Monitoring Services segment is projected to witness the fastest growth at a CAGR of 14.5% from 2026 to 2033, driven by rising demand for continuous health tracking and early detection of health abnormalities. These services enable real-time monitoring of vital signs such as heart rate, sleep patterns, blood pressure, and glucose levels. Increasing integration with IoT-enabled medical devices and wearables is improving data accuracy and usability. Growing focus on preventive healthcare and remote patient monitoring is further accelerating adoption. Healthcare providers are increasingly leveraging monitoring apps for post-treatment care and chronic disease management. The segment is also supported by advancements in cloud-based health data analytics.

- By Platform

On the basis of platform, the global personal health apps market is segmented into Google Play Store, Apple Store, and others. The Google Play Store segment dominated the market with a 57.36% share in 2025, driven by widespread Android smartphone penetration, affordability of devices, and strong user base across emerging economies. The platform hosts a large variety of health and fitness applications catering to diverse consumer needs. Developers prefer Android due to lower entry barriers and broader market reach. Increasing adoption of low-cost smartphones in Asia-Pacific and Latin America is further strengthening this dominance. Continuous app innovation and frequent updates are enhancing user engagement. The segment benefits from strong ecosystem expansion in price-sensitive markets.

The Apple Store segment is expected to witness the fastest growth at a CAGR of 12.9% from 2026 to 2033, driven by high-income user base, strong ecosystem integration, and premium adoption of health tracking technologies. Apple’s HealthKit and wearable ecosystem enable seamless data synchronization and advanced health analytics. Increasing focus on data privacy and security is encouraging users to adopt iOS-based health applications. Rising penetration of Apple Watch and connected health devices is further accelerating growth. Developers are increasingly targeting Apple users due to higher monetization potential. The segment benefits from strong demand for premium digital health experiences and advanced wellness features.

Global Personal Health Apps Market Regional Analysis

North America dominated the global personal health apps market with the largest revenue share of 38.42% in 2025, supported by high smartphone penetration, advanced digital health infrastructure, and strong adoption of fitness and chronic care management apps. The region also benefits from rising consumer awareness regarding preventive healthcare, increasing prevalence of chronic diseases, and widespread use of AI-powered fitness and monitoring platforms. Strong presence of leading technology companies and health app developers further accelerates innovation and market penetration. Expanding employer-sponsored wellness programs and insurance-linked digital health solutions continue to strengthen North America’s leadership position in the global market.

U.S. Personal Health Apps Market Insight

The U.S. personal health apps market is witnessing strong growth due to rising consumer awareness of preventive healthcare, increasing prevalence of lifestyle diseases, and widespread adoption of digital wellness ecosystems. The country’s advanced digital health infrastructure, along with high smartphone and wearable penetration, is driving demand across fitness, mental wellness, and chronic disease management applications. In addition, strong presence of technology giants and health startups, combined with employer-sponsored wellness programs and insurance-linked incentives, is accelerating adoption of AI-powered, subscription-based health platforms across diverse user groups. In addition, strong investments from technology companies and healthcare organizations are enabling continuous product innovation, particularly in AI-based analytics and predictive health insights. This is further strengthening the region’s leadership in the global personal health apps landscape.

Europe Personal Health Apps Market Insight

The Europe personal health apps market remains a major contributor to global revenue, driven by strong regulatory frameworks, rising health consciousness, and increasing adoption of preventive healthcare solutions. The widespread use of fitness tracking, nutrition monitoring, and mental wellness applications is supporting market expansion across the region. Increasing integration of health apps with public healthcare systems, along with strong emphasis on data privacy and digital security, continues to enhance user trust and adoption throughout Europe. Consumers in Europe are increasingly adopting fitness, nutrition, and mental wellness applications as part of daily lifestyle management. Integration of health apps with public healthcare systems and wearable technologies is improving accessibility and continuity of care.

U.K. Personal Health Apps Market Insight

The U.K. personal health apps market is experiencing steady growth, supported by rising digital healthcare adoption, increasing focus on mental well-being, and strong penetration of mobile-based wellness applications. Government-backed digital health initiatives and growing integration of apps with NHS-supported platforms are contributing to market expansion. Furthermore, increasing demand for fitness tracking, stress management, and virtual consultation services is strengthening the use of AI-enabled and personalized health applications across the country. Mental health awareness is a particularly strong driver in the U.K., with growing adoption of apps focused on anxiety management, mindfulness, and behavioral therapy. In addition, fitness and lifestyle applications are gaining traction among younger populations seeking personalized health optimization tools.

Germany Personal Health Apps Market Insight

The Germany personal health apps market is expanding steadily due to strong healthcare infrastructure, rising health awareness, and increasing adoption of digital fitness and chronic disease management solutions. Consumers are increasingly using mobile applications for preventive care, nutrition tracking, and lifestyle monitoring. Continuous advancements in data protection, AI-driven health analytics, and integration with wearable medical devices are further improving app functionality and driving sustained market growth in Germany. Germany’s emphasis on data security and healthcare digitization is driving the development of highly secure and compliant health platforms. Integration with electronic health records and medical-grade wearable devices is improving the clinical usefulness of personal health apps.

Asia-Pacific Personal Health Apps Market Insight

The Asia-Pacific personal health apps market is expected to witness rapid growth, driven by increasing smartphone penetration, rising digital health awareness, and expanding middle-class population across emerging economies. Growing burden of chronic diseases and increasing focus on preventive healthcare are supporting strong demand for fitness, wellness, and monitoring applications. In addition, rapid digital transformation and expansion of mobile-first healthcare ecosystems in countries such as China, India, and Southeast Asia are accelerating regional market adoption. Consumers in the region are increasingly adopting fitness, nutrition, and preventive healthcare apps as part of daily lifestyle management. The growing burden of chronic diseases such as diabetes and hypertension is further driving the need for continuous health monitoring tools.

Japan Personal Health Apps Market Insight

The Japan personal health apps market is witnessing consistent growth due to a rapidly aging population, strong focus on preventive healthcare, and increasing adoption of wearable-integrated digital health solutions. Consumers are increasingly relying on mobile applications for fitness tracking, chronic disease monitoring, and elderly care support. Moreover, integration of AI, IoT, and advanced analytics in health platforms is enhancing personalized care and improving long-term health management outcomes across the population. Integration of advanced technologies such as AI, IoT, and wearable health devices is enhancing the accuracy and usability of personal health apps. These solutions are particularly valuable in managing age-related health conditions and supporting independent living for elderly populations.

China Personal Health Apps Market Insight

The China personal health apps market is growing rapidly, driven by expanding digital healthcare infrastructure, rising health awareness, and strong adoption of mobile-first wellness ecosystems. Increasing prevalence of chronic diseases and lifestyle-related disorders is boosting demand for self-monitoring and preventive health solutions. In addition, strong domestic technology ecosystem, integration with super apps, and rapid advancements in AI-driven health analytics are positioning China as one of the fastest-growing markets for personal health apps globally. Increasing prevalence of chronic diseases and lifestyle disorders is encouraging consumers to adopt self-monitoring and preventive healthcare solutions. Fitness tracking, nutrition management, and telehealth applications are becoming increasingly popular across urban populations.

Global Personal Health Apps Market Share

The Personal Health Apps industry is primarily led by well-established companies, including:

- MyFitnessPal, Inc. (U.S.)

- Fitbit LLC (U.S.)

- Apple Inc. (U.S.)

- Samsung Electronics Co., Ltd. (South Korea)

- Google LLC (U.S.)

- Strava, Inc. (U.S.)

- Headspace Health, Inc. (U.S.)

- com, Inc. (U.S.)

- Flo Health, Inc. (U.K.)

- Noom, Inc. (U.S.)

- Oura Health Ltd (Finland)

- WHOOP, Inc. (U.S.)

- Nike, Inc. (U.S.)

- Garmin Ltd. (Switzerland)

- Withings (France)

- Lifesum AB (Sweden)

- Sleep Cycle AB (Sweden)

- Zwift, Inc. (U.S.)

- WW International, Inc. (U.S.)

- MyNetDiary Inc. (U.S.)

Latest Developments in Global Personal Health Apps Market

- In October 2025, the World Health Organization (WHO) expanded its digital health initiatives by releasing updated global guidance for mobile health (mHealth) applications and personal health tracking systems, focusing on the safe and effective use of digital tools for chronic disease management, mental health support, and preventive care. The framework encourages governments and healthcare systems to integrate validated digital health applications into national healthcare strategies to improve accessibility and patient outcomes. This development highlights growing institutional support for regulated and evidence-based personal health app adoption worldwide

- In November 2024, Apple introduced significant updates to its Apple Health ecosystem, adding enhanced mental health features such as mood tracking, emotional state logging, and deeper behavioral insights integrated with Apple Watch biometric data. The update enables users to monitor stress levels, sleep patterns, and overall wellness in a more holistic manner through a unified health dashboard. This advancement reflects Apple’s growing emphasis on combining physical and mental health monitoring within its digital health platform

- In March 2023, Google and Samsung expanded the Health Connect platform, enabling secure interoperability between more than 500 health and fitness applications across Android devices. The platform allows seamless sharing of health data such as steps, sleep, heart rate, and nutrition metrics across apps such as Fitbit, MyFitnessPal, and Samsung Health. This development significantly improves fragmentation issues in the personal health apps ecosystem and strengthens cross-platform digital health integration

- In January 2023, Google officially launched Health Connect, a unified API platform designed to standardize health data sharing across Android-based fitness and wellness applications. The platform provides users with centralized control over their health data permissions while enabling developers to integrate consistent health metrics across apps. This launch marked a key step toward building a more interoperable and secure personal health data ecosystem in the mobile health industry

- In September 2021, WHO released its Global Strategy on Digital Health 2020–2025 implementation updates, emphasizing the rapid adoption of digital health tools including mobile health applications for improving healthcare delivery and patient engagement. The strategy highlights the importance of scaling digital health solutions to support universal health coverage and strengthen health systems globally. This initiative played a foundational role in accelerating global adoption of personal health apps and digital wellness platforms.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.