Global Pharmaceutical Isolator Market

Market Size in USD Billion

CAGR :

%

USD

4.21 Billion

USD

12.26 Billion

2025

2033

USD

4.21 Billion

USD

12.26 Billion

2025

2033

| 2026 –2033 | |

| USD 4.21 Billion | |

| USD 12.26 Billion | |

| % | |

|

Pharmaceutical Isolator Market Size

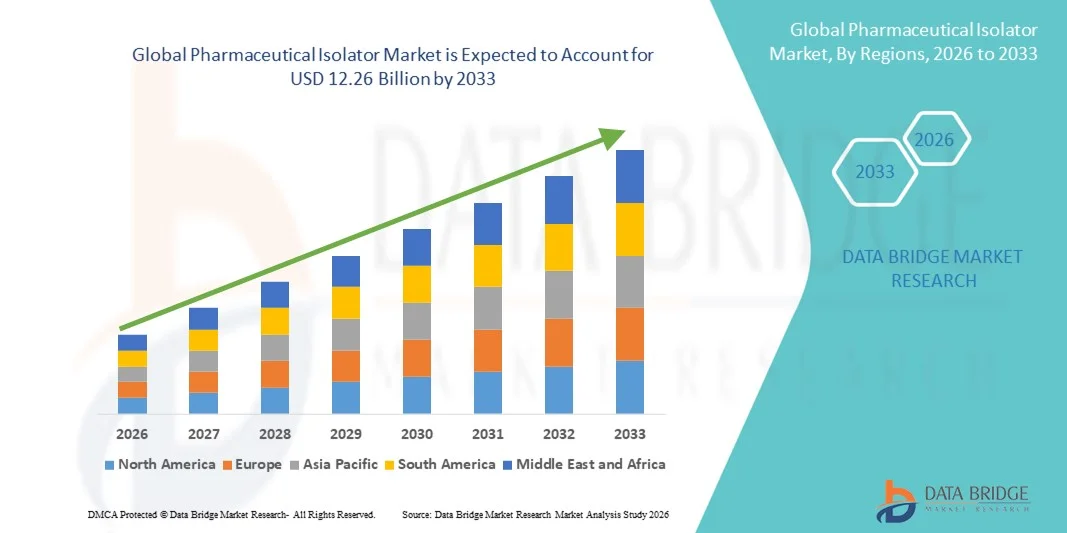

- The global Pharmaceutical Isolator market size was valued at USD 4.21 billion in 2025 and is expected to reach USD 12.26 billion by 2033, at a CAGR of 14.30% during the forecast period

- The market growth is largely fueled by the increasing emphasis on sterile drug manufacturing, stringent regulatory requirements for contamination control, and continuous technological advancements in aseptic processing and cleanroom systems within pharmaceutical and biotechnology facilities

- Furthermore, rising demand for safe, contamination-free handling of hazardous drugs, growing production of biologics and high-potency active pharmaceutical ingredients (HPAPIs), and increasing focus on operator and product protection are establishing pharmaceutical isolators as critical components in modern manufacturing and laboratory environments. These converging factors are accelerating the uptake of Pharmaceutical Isolator solutions, thereby significantly boosting the industry's growth

Pharmaceutical Isolator Market Analysis

- Pharmaceutical isolators, designed to provide a sterile and contamination-free environment for handling potent compounds and aseptic drug manufacturing, are increasingly vital components of modern pharmaceutical and biotechnology facilities due to their high-level product protection, operator safety, and compliance with stringent regulatory standards

- The escalating demand for pharmaceutical isolators is primarily fueled by the growing production of biologics and high-potency active pharmaceutical ingredients (HPAPIs), rising emphasis on contamination control, and increasing regulatory requirements for sterile drug manufacturing processes

- North America dominated the Pharmaceutical Isolator market with the largest revenue share of 39.2% in 2025, characterized by advanced pharmaceutical manufacturing infrastructure, strong presence of leading biopharmaceutical companies, high R&D investments, and strict regulatory compliance standards. The U.S. accounts for a substantial share of regional installations, driven by expanding biologics production and aseptic processing facilities

- Asia-Pacific is expected to be the fastest-growing region in the Pharmaceutical Isolator market during the forecast period, expanding at a CAGR of 9.4% from 2026 to 2033, due to increasing pharmaceutical manufacturing capacity, rising investments in biotechnology, growing generic drug production, and strengthening regulatory frameworks across emerging economies

- The closed system segment held the largest market revenue share of 62.4% in 2025, attributed to its superior contamination control capabilities and complete environmental isolation

Report Scope and Pharmaceutical Isolator Market Segmentation

|

Attributes |

Pharmaceutical Isolator Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Pharmaceutical Isolator Market Trends

Technological Advancements and Automation in Contamination Control

- A significant and accelerating trend in the global Pharmaceutical Isolator market is the increasing integration of advanced automation, robotics, and digital monitoring systems within isolator units to enhance sterility assurance and operational efficiency

- Manufacturers are focusing on minimizing human intervention in critical processes by incorporating automated glove testing, robotic material transfer systems, and real-time environmental monitoring technologies. This evolution is significantly improving contamination control while ensuring compliance with stringent global regulatory standards

- For instance, leading pharmaceutical equipment manufacturers are introducing isolators equipped with integrated vaporized hydrogen peroxide (VHP) bio-decontamination systems and automated pressure control mechanisms that maintain consistent aseptic conditions throughout production cycles. Similarly, advanced isolator platforms now feature touchscreen interfaces and data logging systems that support digital batch recording and audit readiness

- The adoption of Industry 4.0 principles within pharmaceutical manufacturing facilities is further enhancing isolator performance. Smart sensors embedded within isolator chambers continuously monitor airflow velocity, particle counts, temperature, humidity, and differential pressure to ensure stable and validated operating conditions. These systems enable predictive maintenance and reduce downtime by identifying potential deviations before they escalate into compliance risks

- The seamless integration of isolators with centralized manufacturing execution systems (MES) and quality management platforms allows pharmaceutical companies to maintain comprehensive traceability and documentation. Through a unified digital interface, operators can oversee production parameters, environmental conditions, and validation records, strengthening regulatory compliance and operational transparency

- This shift toward intelligent, automated, and digitally connected isolator systems is fundamentally reshaping pharmaceutical manufacturing environments. Companies are prioritizing modular automation-ready isolators capable of supporting biologics, cell and gene therapies, and high-potency drug production with minimal contamination risks

- The demand for technologically advanced pharmaceutical isolators is growing rapidly across both developed and emerging markets, as manufacturers increasingly prioritize sterility assurance, operator safety, and long-term cost efficiency in highly regulated production environments

Pharmaceutical Isolator Market Dynamics

Driver

Rising Demand for Sterile Pharmaceuticals and Regulatory Compliance Requirements

- The increasing global demand for sterile injectable drugs, biologics, vaccines, and high-potency compounds is a significant driver fueling the growth of the Pharmaceutical Isolator market

- As pharmaceutical pipelines become more complex, manufacturers require highly controlled environments to ensure product integrity and patient safety

- For instance, the rapid expansion of biologics manufacturing facilities and vaccine production units worldwide has necessitated the installation of advanced aseptic and containment isolator systems to meet regulatory sterility standards. Strategic investments by pharmaceutical companies in new sterile production lines are expected to drive market expansion during the forecast period

- As regulatory authorities intensify inspections and enforce stricter Good Manufacturing Practice (GMP) guidelines, pharmaceutical manufacturers are compelled to adopt isolator systems that provide validated contamination control and operator protection. Isolators significantly reduce the risk of product recalls, batch failures, and cross-contamination incidents

- Furthermore, the growing production of oncology drugs and high-potency active pharmaceutical ingredients (HPAPIs) requires containment isolators to safeguard personnel and the external environment from hazardous exposure. Rising awareness regarding occupational safety standards further strengthens demand

- The expansion of contract manufacturing organizations (CMOs) and contract research organizations (CROs) is also contributing to market growth, as these facilities increasingly rely on isolators to maintain high sterility and safety benchmarks while serving multiple pharmaceutical clients

Restraint/Challenge

High Capital Investment and Complex Validation Procedures

- The high initial cost associated with pharmaceutical isolator systems poses a significant challenge to widespread adoption, particularly for small and mid-sized pharmaceutical companies operating with limited capital budgets. Advanced isolators equipped with automation, decontamination systems, and digital monitoring technologies require substantial upfront investment

- For instance, installation of a fully integrated aseptic isolator line in a sterile manufacturing facility involves not only equipment procurement costs but also infrastructure modifications, HVAC upgrades, and validation expenses, increasing overall project expenditure

- In addition, the validation and qualification processes for isolator systems are complex and time-consuming, requiring extensive documentation, performance testing, and regulatory approvals. Companies must conduct installation qualification (IQ), operational qualification (OQ), and performance qualification (PQ) procedures before commercial production can commence

- Maintenance requirements, periodic revalidation, and operator training further add to operational costs. Any deviation from validated parameters can lead to production delays and compliance risks, increasing financial burdens for manufacturers

- Overcoming these challenges will require cost-optimized system designs, streamlined validation protocols, and supportive regulatory guidance. Manufacturers focusing on modular, scalable, and energy-efficient isolator solutions are expected to mitigate some of these constraints and sustain long-term market growth

Pharmaceutical Isolator Market Scope

The market is segmented on the basis of type, system type, pressure, configuration, application, end user, and distribution channel.

- By Type

On the basis of type, the Global Pharmaceutical Isolator market is segmented into Aseptic Isolators, Containment Isolators, Bio Isolators, Sampling and Weighing Isolators, Active Pharmaceutical Ingredient (API) Manufacturing Isolators, Radiopharmaceutical Isolators, Production Isolators, and Others. The aseptic isolators segment dominated the largest market revenue share of 34.6% in 2025, primarily driven by the increasing global demand for sterile injectable drugs, biologics, and vaccines that require highly controlled environments to prevent contamination. These isolators create a fully enclosed, decontaminated workspace that significantly reduces human intervention, thereby minimizing microbial risks. Pharmaceutical companies are increasingly adopting aseptic isolators to comply with stringent Good Manufacturing Practice (GMP) guidelines and regulatory mandates related to sterility assurance. The rapid expansion of biologics pipelines, monoclonal antibody production, and advanced cell and gene therapies has further strengthened demand. Aseptic isolators also improve operational efficiency by enabling automated filling and compounding processes. In addition, rising hospital compounding activities and outsourcing to contract manufacturing organizations support steady adoption. Continuous technological advancements, including integrated vaporized hydrogen peroxide (VHP) systems, further enhance segment dominance.

The containment isolators segment is anticipated to witness the fastest CAGR of 8.9% from 2026 to 2033, fueled by the growing production of high-potency active pharmaceutical ingredients (HPAPIs) and cytotoxic drugs that require strict operator protection. These systems are specifically designed to prevent hazardous drug exposure and environmental contamination, ensuring worker safety. Increasing oncology drug development and expansion of targeted therapies are significantly boosting demand. Regulatory authorities are enforcing tighter occupational safety standards, compelling manufacturers to invest in advanced containment technologies. Rising awareness regarding cross-contamination risks in multiproduct facilities is further driving adoption. Containment isolators also enhance product integrity while maintaining negative pressure environments for safe handling. The expansion of pharmaceutical manufacturing in emerging markets contributes to sustained growth.

- By System Type

On the basis of system type, the market is segmented into Closed System and Open System. The closed system segment held the largest market revenue share of 62.4% in 2025, attributed to its superior contamination control capabilities and complete environmental isolation. Closed systems create a sealed barrier between the internal working area and the external environment, ensuring maximum sterility and operator safety. These systems are widely preferred in aseptic drug manufacturing, sterile compounding, and vaccine production. Their ability to maintain consistent environmental parameters such as airflow, pressure, and humidity enhances compliance with global regulatory standards. Increasing automation in pharmaceutical facilities further supports closed system integration. In addition, pharmaceutical companies favor closed systems for long-term cost efficiency due to reduced product loss and contamination risks. The rising complexity of biologic drug manufacturing continues to reinforce this segment’s dominance.

The open system segment is expected to witness a CAGR of 7.8% from 2026 to 2033, driven by flexibility, ease of installation, and cost-effectiveness for non-critical applications. Open isolators are commonly used in research settings and lower-risk processing environments where complete enclosure may not be mandatory. Their adaptability for small-scale production and academic research supports steady adoption. Growing pharmaceutical R&D activities globally are expected to stimulate demand. In addition, increasing early-stage drug development projects and pilot-scale manufacturing activities are contributing to higher utilization of open isolator systems. These systems also offer easier maintenance and faster validation processes, making them attractive for institutions operating under budget constraints. Furthermore, expanding collaborations between academic institutes and biotechnology startups are expected to create sustained demand for flexible and economical isolator solutions.

- By Pressure

On the basis of pressure, the pharmaceutical isolator market is segmented into Positive Pressure and Negative Pressure. The positive pressure segment accounted for the largest revenue share of 55.1% in 2025, primarily due to its extensive use in sterile drug manufacturing environments where product protection is critical. Positive pressure systems ensure that any potential leakage occurs outward, preventing contaminants from entering the sterile workspace. These isolators are widely implemented in injectable drug production, vaccine filling lines, and sterile compounding pharmacies. The rapid increase in demand for biologics and parenteral formulations has significantly boosted segment growth. Pharmaceutical companies are prioritizing positive pressure isolators to achieve higher sterility assurance levels and regulatory compliance. Furthermore, technological integration with automated decontamination cycles enhances reliability and efficiency.

The negative pressure segment is projected to grow at a CAGR of 9.3% from 2026 to 2033, driven by the rising handling of hazardous compounds, oncology drugs, and HPAPIs. Negative pressure isolators protect operators and the surrounding environment by containing harmful substances within the chamber. Increasing awareness of occupational safety regulations and worker protection standards significantly supports demand. Expansion of cancer drug manufacturing facilities globally is expected to accelerate adoption. In addition, the growing pipeline of antibody-drug conjugates (ADCs) and other highly potent targeted therapies is further increasing the requirement for advanced containment systems. Pharmaceutical manufacturers are also investing in upgraded negative pressure technologies to meet stricter environmental and occupational health compliance standards. Furthermore, rising inspections and regulatory audits across global manufacturing sites are compelling facilities to adopt high-performance containment isolators to minimize contamination risks and ensure long-term operational safety.

- By Configuration

On the basis of configuration, the market is segmented into Floor Standing, Modular, Mobile, Compact, Table Top, Portable, and Others. The floor standing segment dominated the market with a revenue share of 39.7% in 2025, supported by its extensive deployment across large-scale pharmaceutical and biotechnology manufacturing facilities worldwide. These systems are specifically engineered for high-volume production environments where continuous processing, sterility assurance, and regulatory compliance are critical. Floor-standing isolators provide superior structural integrity and are capable of integrating seamlessly with automated filling lines, robotic arms, conveyor systems, and decontamination units. Their ability to accommodate complex equipment configurations makes them highly suitable for biologics, vaccine, and injectable drug manufacturing. Pharmaceutical companies prefer these systems for long-term operational stability and scalability within fixed production infrastructures. In addition, their compatibility with advanced airflow management and environmental monitoring systems strengthens contamination control. Growing investments in greenfield manufacturing plants and expansion of contract manufacturing organizations (CMOs) have further accelerated adoption. The segment also benefits from strong demand in developed markets where regulatory compliance standards are stringent.

The modular segment is expected to register the fastest CAGR of 9.6% during the forecast period, driven by increasing demand for flexible, scalable, and cost-efficient production solutions. Modular isolators are designed with interchangeable units that allow manufacturers to expand, relocate, or reconfigure production layouts with minimal disruption. This adaptability is particularly valuable for multiproduct facilities handling diverse drug portfolios, including biologics and high-potency compounds. As pharmaceutical pipelines evolve rapidly, companies seek infrastructure that can adjust to fluctuating production volumes. Modular systems reduce capital expenditure risks by enabling phased investments rather than large upfront costs. They are also gaining popularity in emerging markets where pharmaceutical infrastructure is still developing. In addition, modular designs support faster installation timelines and easier validation processes. Increasing emphasis on lean manufacturing and operational efficiency further contributes to their rapid adoption across global markets.

- By Application

On the basis of application, the market is segmented into Sterility Testing, Manufacturing, Sampling/Weighing/Distribution, and Medical Device Manufacturing. The manufacturing segment held the largest market revenue share of 41.3% in 2025, primarily due to the expanding global production of sterile pharmaceuticals, injectable therapies, vaccines, and advanced biologics. Isolators play a pivotal role in maintaining contamination-free environments during critical processes such as aseptic filling, compounding, capping, and packaging. With the rapid growth of biologics and personalized medicines, manufacturers require highly controlled environments to ensure product integrity. Stringent regulatory frameworks from global health authorities mandate robust sterility standards, reinforcing reliance on isolator technology. In addition, increasing outsourcing of production to CMOs has amplified demand for large-scale isolator integration. The rising prevalence of chronic diseases and growing immunization programs further stimulate production volumes. Pharmaceutical companies are investing heavily in automated isolator systems to improve throughput and minimize human error. Continuous innovation in integrated decontamination technologies also enhances the operational reliability of manufacturing isolators.

The sterility testing segment is projected to grow at a CAGR of 8.7% from 2026 to 2033, driven by intensifying regulatory scrutiny and mandatory quality validation requirements prior to product release. Every batch of sterile pharmaceutical product must undergo rigorous sterility testing, significantly boosting demand for controlled testing environments. The surge in biologics production, which requires higher sterility assurance levels, further strengthens this segment. Growing adoption of rapid microbiological testing methods within isolator systems enhances operational efficiency. Increasing quality control investments by pharmaceutical firms globally also contribute to expansion. In addition, the development of advanced cell and gene therapies necessitates more frequent sterility validation procedures. As regulatory agencies continue tightening inspection protocols, pharmaceutical manufacturers are prioritizing advanced sterility testing isolators to avoid compliance risks and product recalls.

- By End User

On the basis of end user, the market is segmented into Hospitals, Diagnostic Laboratories, Academic and Research Institutes, Pharmaceutical and Biotechnology Companies, Contract Research Organizations, and Others. Pharmaceutical and biotechnology companies dominated the largest revenue share of 48.9% in 2025, owing to their extensive reliance on isolators for sterile manufacturing, research and development, and handling of high-potency compounds. These companies operate large-scale production facilities that require strict contamination control and operator safety standards. The rapid expansion of biologics, biosimilars, and oncology drug pipelines significantly fuels demand within this segment. Increasing global drug approvals and pipeline advancements are encouraging facility upgrades and modernization initiatives. Pharmaceutical firms also prioritize isolator systems to enhance efficiency, reduce product loss, and maintain consistent quality standards. Continuous technological integration, including automated monitoring and digital validation systems, further strengthens segment leadership. Rising investments in vaccine production and advanced therapeutic development add to the sustained growth trajectory.

Contract Research Organizations (CROs) are expected to witness the fastest CAGR of 9.1% from 2026 to 2033, supported by increasing outsourcing of clinical research, drug discovery, and early-stage manufacturing activities. Pharmaceutical companies are partnering with CROs to reduce operational costs and accelerate time-to-market for new therapies. As CROs expand their service portfolios, they are investing in advanced isolator infrastructure to meet regulatory and client requirements. Growing small and mid-sized biotech firms rely heavily on CROs for specialized sterile handling capabilities. The expansion of global clinical trial activities further stimulates demand for isolator-equipped laboratories. Increasing cross-border collaborations and research initiatives also contribute to rising infrastructure investments.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into Direct Tender, Retail Sales, and Third Party Distributors. The direct tender segment accounted for the largest revenue share of 57.8% in 2025, driven by bulk procurement agreements between isolator manufacturers and pharmaceutical companies, hospitals, and government healthcare institutions. Large-scale facility expansion projects typically involve centralized procurement processes through long-term contracts. Direct tenders ensure competitive pricing, product customization, and after-sales service agreements, making them highly attractive for high-value capital equipment purchases. Governments and public health institutions also prefer direct procurement for infrastructure modernization initiatives. Pharmaceutical manufacturers favor this channel for tailored solutions aligned with regulatory requirements. In addition, strategic vendor partnerships and framework agreements further reinforce segment dominance.

The third-party distributors segment is projected to grow at a CAGR of 8.4% during the forecast period, fueled by expanding global supply chains and increasing penetration into emerging markets. Distributors play a crucial role in reaching small and mid-sized pharmaceutical firms that may not engage in direct procurement contracts. They provide localized technical support, installation services, and maintenance assistance. Growing pharmaceutical infrastructure development in Asia-Pacific, Latin America, and the Middle East enhances distributor-based sales opportunities. Furthermore, partnerships between global manufacturers and regional distributors are strengthening market reach and accelerating adoption across developing economies.

Pharmaceutical Isolator Market Regional Analysis

- North America dominated the pharmaceutical isolator market with the largest revenue share of 39.2% in 2025, characterized by advanced pharmaceutical manufacturing infrastructure, a strong presence of leading biopharmaceutical companies, substantial R&D investments, and strict regulatory compliance standards governing sterile drug production

- The region benefits from well-established aseptic processing facilities, high adoption of containment technologies, and continuous upgrades of cleanroom environments to meet evolving GMP and FDA requirements

- The U.S. accounts for a substantial share of regional installations, driven by expanding biologics production, rising demand for sterile injectables, and the increasing implementation of advanced barrier systems in large-scale manufacturing plants

U.S. Pharmaceutical Isolator Market Insight

The U.S. pharmaceutical isolator market captured the largest revenue share within North America in 2025, supported by the country’s extensive biologics manufacturing base and rapid expansion of aseptic fill-finish operations. The presence of major biopharmaceutical companies and contract development and manufacturing organizations (CDMOs) is accelerating the adoption of closed and open isolator systems. Stringent regulatory oversight by the U.S. FDA encourages manufacturers to implement high-containment solutions to minimize contamination risks and ensure product sterility. Growing investments in cell and gene therapy production facilities are further driving demand for advanced isolator technologies. In addition, continuous modernization of legacy pharmaceutical plants and the rising need for operator safety in handling potent compounds are strengthening market growth across the country.

Europe Pharmaceutical Isolator Market Insight

The Europe pharmaceutical isolator market is projected to expand at a steady CAGR throughout the forecast period, driven by strong regulatory frameworks, increasing biologics production, and rising emphasis on contamination control in sterile manufacturing. The region is characterized by the presence of established pharmaceutical hubs and advanced cleanroom infrastructure. Compliance with EU GMP Annex 1 revisions is prompting manufacturers to upgrade conventional cleanroom setups with modern isolator systems. Growing demand for high-potency active pharmaceutical ingredients (HPAPIs) and sterile injectables is further accelerating adoption. Moreover, increased outsourcing to CDMOs and investments in vaccine manufacturing facilities are supporting consistent regional growth.

U.K. Pharmaceutical Isolator Market Insight

The U.K. pharmaceutical isolator market is anticipated to grow at a noteworthy CAGR during the forecast period, supported by strong pharmaceutical R&D activities and expanding biologics manufacturing capabilities. The country’s focus on advanced therapy medicinal products (ATMPs), including cell and gene therapies, is driving demand for highly controlled aseptic environments. Regulatory alignment with international quality standards ensures continued investment in contamination control technologies. In addition, increasing partnerships between research institutions and pharmaceutical companies are fostering innovation in sterile production processes. The modernization of manufacturing facilities and emphasis on operator safety are also contributing to steady market expansion.

Germany Pharmaceutical Isolator Market Insight

The Germany pharmaceutical isolator market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s robust pharmaceutical manufacturing sector and strong emphasis on engineering excellence. Germany’s well-developed industrial infrastructure and leadership in precision equipment manufacturing support the adoption of technologically advanced isolator systems. Increasing production of biologics, biosimilars, and sterile injectable drugs is creating sustained demand for aseptic containment solutions. Strict adherence to EU regulatory standards and a focus on automation in pharmaceutical production are further strengthening market growth. In addition, investments in sustainable and energy-efficient cleanroom technologies are aligning with Germany’s broader industrial priorities.

Asia-Pacific Pharmaceutical Isolator Market Insight

The Asia-Pacific pharmaceutical isolator market is expected to be the fastest-growing region, expanding at a CAGR of 9.4% from 2026 to 2033, driven by rapidly increasing pharmaceutical manufacturing capacity and rising investments in biotechnology. Countries such as China, India, Japan, and South Korea are strengthening their regulatory frameworks and upgrading production facilities to meet international quality standards. The region’s growing generic drug production, expanding vaccine manufacturing capabilities, and increasing exports of sterile formulations are significantly boosting demand for isolator systems. Furthermore, favorable government initiatives supporting domestic pharmaceutical production and foreign direct investments are accelerating infrastructure development. Cost advantages in manufacturing and the rising presence of global CDMOs are also contributing to strong regional growth momentum.

Japan Pharmaceutical Isolator Market Insight

The Japan pharmaceutical isolator market is gaining traction due to the country’s advanced healthcare infrastructure, strong regulatory environment, and focus on high-quality pharmaceutical manufacturing. Japan’s leadership in biologics research and regenerative medicine is driving the need for sophisticated aseptic processing technologies. Pharmaceutical manufacturers are increasingly investing in automated and high-containment isolator systems to ensure product integrity and operator protection. The modernization of aging manufacturing facilities and compliance with global GMP standards are further stimulating demand. In addition, Japan’s emphasis on innovation and precision engineering supports the integration of advanced isolator technologies in both commercial production and research settings.

China Pharmaceutical Isolator Market Insight

China pharmaceutical isolator market accounted for the largest market revenue share in Asia-Pacific in 2025, attributed to rapid expansion of pharmaceutical production capacity, growing biotechnology investments, and strengthening regulatory oversight. The country’s expanding middle class and increasing healthcare expenditure are driving higher demand for sterile and high-quality pharmaceutical products. Government initiatives aimed at improving GMP compliance and promoting domestic drug manufacturing are accelerating the adoption of isolator systems. The presence of large-scale pharmaceutical manufacturing clusters and rising exports of active pharmaceutical ingredients and finished formulations are further propelling market growth. In addition, increasing collaborations with global pharmaceutical firms are enhancing technological advancements and boosting installations of modern containment solutions across China.

Pharmaceutical Isolator Market Share

The Pharmaceutical Isolator industry is primarily led by well-established companies, including:

- Getinge AB (Sweden)

- SKAN AG (Switzerland)

- COMECER S.p.A. (Italy)

- Extract Technology Ltd. (U.K.)

- Azbil Telstar, S.L. (Spain)

- Germfree Laboratories, Inc. (U.S.)

- Laminar Air Flow Systems (U.S.)

- Hosokawa Micron Ltd. (U.K.)

- IsoTech Design (U.K.)

- NuAire, Inc. (U.S.)

- The Baker Company, Inc. (U.S.)

- Terra Universal, Inc. (U.S.)

- Weiss Technik (Germany)

- Chiyoda Corporation (Japan)

- Fedegari Autoclavi S.p.A. (Italy)

- Munters Group (Sweden)

- Mikron Corporation (U.S.)

- Howorth Air Technology (U.K.)

- Envair Technology (U.K.)

- Bioquell (U.K.)

Latest Developments in Global Pharmaceutical Isolator Market

- In July 2023, Metall+Plastic launched a new state-of-the-art pharmaceutical isolator system designed to create a safer and more secure controlled environment for drug manufacturing, integrating advanced automation features that reduce contamination risk and improve operator safety. This development reflects the broader industry drive toward more automated and efficient aseptic processing

- In March 2023, SKAN AG introduced an advanced isolator system featuring innovative filtration technology that increases air purity levels within containment environments by approximately 30 %, enhancing sterility assurance for critical pharmaceutical applications such as aseptic fill-finish operations

- In October 2023, Getinge AB announced the launch of ISOPRIME — a low-cost rigid-wall pharmaceutical isolator built for common aseptic procedures, lowering entry barriers for firms needing compliant isolator solutions while maintaining high sterility performance

- In March 2024, Telstar unveiled a dual-mode isolator system at the Pharma Congress in Wiesbaden capable of performing both containment and aseptic operations. This versatile design allows companies to use a single isolator for multiple sterile processing needs, reducing both footprint and capital expenditure

- In January 2025, Getinge AB launched a new line of automated transfer isolators specifically designed to integrate with robotic aseptic filling lines, enhancing throughput and reducing manual touchpoints in sterile drug production — an important innovation for high-volume biologics and injectable drug manufacturing

- In February 2025, Skan AG announced a partnership with a major European contract development and manufacturing organization (CDMO) to implement fully integrated isolator systems for the sterile production of next-generation cell and gene therapies, highlighting the trend toward specialized isolators for advanced biologic manufacturing

- In January 2025, Comecer S.p.A. introduced a new hydrogen peroxide vapor (HPV) decontamination system for its isolator range, delivering faster cycle times and improved compatibility with sensitive materials — addressing critical operational efficiency and reliability needs in modern aseptic processing facilities

- In October 2025, Jubilant HollisterStier LLC launched a new third sterile fill & finish line at its Spokane facility (USA), featuring advanced isolator technology that enhances sterility assurance, throughput, and precision for complex injectable drug programs. The $132 million project significantly increases the company’s sterile manufacturing capacity and supports global supply needs for high-value therapeutics

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.