Global Photodiode Sensors Market

Market Size in USD Billion

CAGR :

%

USD

1.45 Billion

USD

2.54 Billion

2025

2033

USD

1.45 Billion

USD

2.54 Billion

2025

2033

| 2026 –2033 | |

| USD 1.45 Billion | |

| USD 2.54 Billion | |

| % | |

|

Photodiode Sensors Market Size

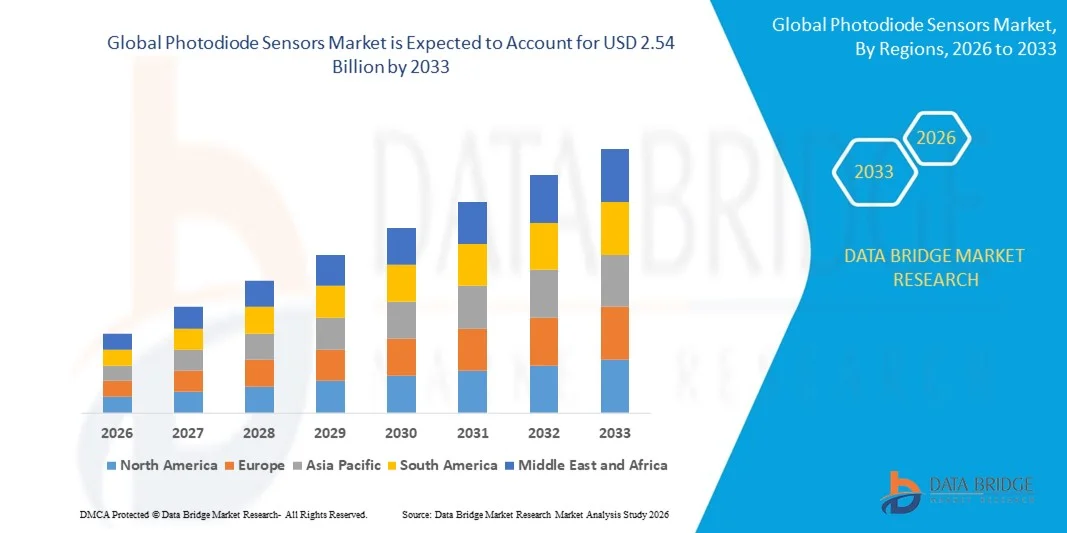

- The global photodiode sensors market size was valued at USD 1.45 billion in 2025 and is expected to reach USD 2.54 billion by 2033, at a CAGR of 7.20% during the forecast period

- The market growth is largely fueled by the rapid expansion of fiber optic communication networks, increasing deployment of high-speed data transmission systems, and continuous advancements in optoelectronic technologies, leading to stronger integration of photodiode sensors across telecommunications, industrial automation, and healthcare applications

- Furthermore, rising demand for high-sensitivity light detection in applications such as LiDAR, medical imaging, environmental monitoring, and consumer electronics is positioning photodiode sensors as critical components in next-generation sensing systems. These converging factors are accelerating technological innovation and large-scale deployment, thereby significantly boosting the growth of the photodiode sensors market

Photodiode Sensors Market Analysis

- Photodiode sensors, which convert light into electrical signals for precise optical detection, are increasingly vital components in modern communication systems, medical diagnostic devices, automotive safety technologies, and industrial automation due to their high sensitivity, fast response time, compact size, and energy efficiency

- The escalating demand for photodiode sensors is primarily fueled by the expansion of 5G infrastructure, rising adoption of advanced driver-assistance systems and LiDAR technologies, growing use of non-invasive medical monitoring equipment, and increasing integration of optical sensing solutions in smart manufacturing and consumer electronics

- North America dominated the photodiode sensors market with a share of 46.01% in 2025, due to strong demand across optical communication, aerospace and defense, and advanced healthcare diagnostics sectors

- Asia-Pacific is expected to be the fastest growing region in the photodiode sensors market during the forecast period due to rapid urbanization, expanding telecommunications infrastructure, and strong semiconductor manufacturing capabilities in countries such as China, Japan, and South Korea

- PIN photodiode segment dominated the market with a market share of 41.92% in 2025, due to its superior sensitivity, fast response time, and low noise performance compared to standard PN photodiodes. Its wide depletion region enhances light absorption efficiency, making it highly suitable for optical communication systems, medical instrumentation, and industrial sensing applications. The strong adoption of fiber optic networks and high-speed data transmission systems further supports the demand for PIN photodiodes

Report Scope and Photodiode Sensors Market Segmentation

|

Attributes |

Photodiode Sensors Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, geographically represented company-wise production and capacity, network layouts of distributors and partners, detailed and updated price trend analysis and deficit analysis of supply chain and demand. |

Photodiode Sensors Market Trends

Increasing Integration of Photodiode Sensors in LiDAR and 3D Sensing Applications

- A significant trend in the photodiode sensors market is the rising integration of photodiode technologies into LiDAR and advanced 3D sensing systems, driven by growing demand for precise depth detection and real-time environmental mapping across automotive and industrial sectors. This integration is strengthening the role of photodiodes as core components in next-generation sensing architectures

- For instance, Sony Semiconductor Solutions introduced its IMX479 stacked SPAD depth sensor for automotive LiDAR applications, enabling long-range detection and enhanced photon efficiency. Such developments enhance object recognition accuracy and support safer autonomous driving capabilities

- The adoption of avalanche photodiodes and SPAD arrays in advanced driver-assistance systems is expanding as these sensors provide high sensitivity and fast response time under low-light conditions. This is positioning photodiode sensors as critical enablers of reliable perception systems in intelligent mobility platforms

- Industrial automation is increasingly utilizing photodiode-based time-of-flight sensors to enable accurate 3D mapping and robotic navigation in manufacturing environments. This trend is supporting the shift toward smart factories that rely on stable and high-speed optical detection systems

- Healthcare imaging and diagnostic equipment are incorporating compact photodiode arrays to improve optical signal detection and enhance imaging precision. This integration is accelerating advancements in non-invasive diagnostic systems that require high-performance light sensing components

- The market is witnessing sustained innovation in solid-state LiDAR and depth-sensing modules where photodiodes form the foundation of signal reception and conversion. This rising incorporation across automotive, robotics, and imaging applications is reinforcing the transition toward intelligent sensing ecosystems built on high-efficiency photodiode technologies

Photodiode Sensors Market Dynamics

Driver

Rapid Expansion of Fiber Optic Communication Infrastructure

- The rapid expansion of fiber optic communication networks across global telecommunications infrastructure is driving strong demand for photodiode sensors that convert optical signals into electrical signals with high precision and speed. These components are essential for maintaining signal integrity and supporting high-bandwidth data transmission

- For instance, Hamamatsu Photonics supplies high-speed PIN photodiodes widely used in optical receivers for fiber optic communication systems. These devices enable accurate light detection and stable performance across long-distance data transmission networks

- The deployment of 5G networks and hyperscale data centers is increasing the need for high-sensitivity photodiodes capable of handling faster data rates and lower latency requirements. This strengthens the role of photodiode sensors in supporting next-generation communication infrastructure

- Telecommunication operators are investing heavily in optical transceivers and receiver modules that depend on reliable photodiode components for signal conversion. This investment is accelerating production volumes and technological refinement within the photodiode market

- The continued global expansion of broadband access and cloud-based services is strengthening this growth driver. The need for faster, more energy-efficient, and high-accuracy optical receivers continues to influence technological advancement and long-term market expansion

Restraint/Challenge

High Manufacturing Complexity and Cost of Advanced Photodiode Technologies

- The photodiode sensors market faces challenges due to the complex fabrication processes required to produce high-performance photodiodes, particularly avalanche photodiodes and SPAD arrays that demand precision semiconductor engineering. These processes involve specialized materials, advanced wafer processing, and strict environmental controls, increasing overall production costs

- For instance, OSRAM Opto Semiconductors GmbH employs advanced compound semiconductor fabrication techniques to manufacture high-sensitivity photodiodes for automotive and industrial use. Such intricate production requirements elevate capital investment and operational expenditure for manufacturers

- Manufacturing advanced photodiodes requires stringent quality control standards to ensure low noise, high quantum efficiency, and long-term stability under demanding operating conditions. These requirements extend development cycles and increase testing and validation costs

- The reliance on compound semiconductor materials and specialized packaging technologies introduces supply chain complexity and cost variability. Maintaining consistent performance while managing material expenses presents ongoing challenges for producers

- These combined factors place pressure on industry participants to optimize fabrication efficiency and reduce cost structures while sustaining high-performance standards. The need to balance innovation with economic feasibility continues to shape competitive dynamics within the photodiode sensors market

Photodiode Sensors Market Scope

The market is segmented on the basis of photodiode type, wavelength, and end-use industry.

- By Photodiode Type

On the basis of photodiode type, the photodiode sensors market is segmented into PN photodiode, PIN photodiode, avalanche photodiode, and Schottky photodiode. The PIN photodiode segment dominated the market with the largest revenue share of 41.92% in 2025, driven by its superior sensitivity, fast response time, and low noise performance compared to standard PN photodiodes. Its wide depletion region enhances light absorption efficiency, making it highly suitable for optical communication systems, medical instrumentation, and industrial sensing applications. The strong adoption of fiber optic networks and high-speed data transmission systems further supports the demand for PIN photodiodes. In addition, their cost-effectiveness and operational stability across varying environmental conditions strengthen their position in both commercial and industrial deployments.

The avalanche photodiode segment is anticipated to witness the fastest growth rate from 2026 to 2033, fueled by rising demand for high-gain and high-sensitivity detection in low-light environments. Avalanche photodiodes provide internal signal amplification through impact ionization, enabling precise detection in long-distance optical communication, LiDAR systems, and advanced defense applications. Increasing deployment of autonomous systems and advanced driver-assistance technologies is accelerating their integration into sensing modules. Their ability to detect weak optical signals with improved signal-to-noise ratio makes them highly attractive for next-generation photonic and imaging solutions.

- By Wavelength

On the basis of wavelength, the photodiode sensors market is segmented into ultra violet (UV) spectrum, visible spectrum, near infrared (NIR) spectrum, and infrared (IR) spectrum. The near infrared (NIR) spectrum segment dominated the market in 2025, driven by its extensive use in fiber optic communication, biomedical monitoring, and industrial automation systems. NIR photodiodes offer deeper material penetration and stable performance, making them suitable for non-invasive medical diagnostics and proximity sensing applications. The expansion of high-speed internet infrastructure and data centers significantly contributes to the sustained demand for NIR-based photodiode sensors. In addition, their compatibility with silicon-based detector technologies enhances manufacturing scalability and cost efficiency.

The infrared (IR) spectrum segment is projected to witness the fastest growth from 2026 to 2033, supported by increasing adoption in thermal imaging, motion detection, and remote sensing applications. IR photodiodes are widely utilized in security systems, environmental monitoring, and aerospace technologies due to their ability to detect heat signatures and operate in low-visibility conditions. Growing investments in smart surveillance systems and industrial safety solutions are further propelling demand. Their expanding role in automotive sensing and defense-grade imaging systems strengthens long-term growth prospects.

- By End-Use Industry

On the basis of end-use industry, the photodiode sensors market is segmented into telecommunication, health care, consumer electronics, aerospace and defense, and others. The telecommunication segment dominated the market with the largest revenue share in 2025, driven by rapid global expansion of fiber optic networks and increasing data traffic. Photodiodes play a critical role in optical receivers, converting light signals into electrical signals with high precision and speed. The continuous deployment of 5G infrastructure and data center interconnect solutions significantly supports demand. In addition, the need for reliable high-bandwidth communication systems reinforces the dominance of this segment.

The health care segment is expected to witness the fastest growth rate from 2026 to 2033, fueled by rising adoption of photodiode-based sensors in medical imaging, pulse oximetry, and diagnostic equipment. Photodiodes enable accurate light detection in non-invasive monitoring devices, supporting real-time patient data analysis. Increasing demand for portable and wearable medical devices is accelerating integration of compact and energy-efficient photodiode sensors. Technological advancements in biomedical optics and growing focus on preventive healthcare further drive segment expansion.

Photodiode Sensors Market Regional Analysis

- North America dominated the photodiode sensors market with the largest revenue share of 46.01% in 2025, driven by strong demand across optical communication, aerospace and defense, and advanced healthcare diagnostics sectors

- The region benefits from the rapid deployment of fiber optic networks, high investment in R&D activities, and early adoption of advanced sensing technologies across industrial and commercial applications

- This widespread adoption is further supported by the presence of leading semiconductor manufacturers, robust data center infrastructure, and continuous innovation in LiDAR, medical imaging, and automation systems, establishing photodiode sensors as critical components in high-performance electronic systems

U.S. Photodiode Sensors Market Insight

The U.S. photodiode sensors market captured the largest revenue share within North America in 2025, fueled by extensive expansion of high-speed communication networks and strong defense modernization programs. Increasing investments in 5G infrastructure and data centers are accelerating demand for high-sensitivity optical detectors. The growing integration of photodiodes in medical devices, autonomous vehicles, and industrial automation systems further propels market growth. Moreover, technological advancements in semiconductor fabrication and optoelectronics strengthen domestic production capabilities and innovation leadership.

Europe Photodiode Sensors Market Insight

The Europe photodiode sensors market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by increasing focus on industrial automation, renewable energy systems, and advanced automotive technologies. Rising adoption of optical sensing in manufacturing and smart mobility solutions is fostering regional growth. European industries emphasize precision, energy efficiency, and regulatory compliance, which supports the deployment of reliable photodiode-based detection systems. Growth is evident across telecommunications, aerospace, and medical device manufacturing sectors.

U.K. Photodiode Sensors Market Insight

The U.K. photodiode sensors market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by expanding investments in research institutions, healthcare technology, and next-generation communication systems. The country’s strong semiconductor research ecosystem encourages innovation in optoelectronic components. Increasing adoption of optical sensors in biomedical applications and environmental monitoring further stimulates demand. The growing emphasis on digital infrastructure and high-speed connectivity continues to support market expansion.

Germany Photodiode Sensors Market Insight

The Germany photodiode sensors market is expected to expand at a considerable CAGR during the forecast period, fueled by the country’s strong industrial base and leadership in automotive engineering. The integration of photodiode sensors in advanced driver-assistance systems, industrial robotics, and precision manufacturing equipment significantly contributes to demand. Germany’s emphasis on Industry 4.0 and smart factory initiatives accelerates adoption of high-performance optical sensing technologies. Continuous innovation in automotive LiDAR and automation solutions further reinforces growth prospects.

Asia-Pacific Photodiode Sensors Market Insight

The Asia-Pacific photodiode sensors market is poised to grow at the fastest CAGR during the forecast period of 2026 to 2033, driven by rapid urbanization, expanding telecommunications infrastructure, and strong semiconductor manufacturing capabilities in countries such as China, Japan, and South Korea. Increasing production of consumer electronics and rising deployment of fiber optic networks are major growth catalysts. Government initiatives promoting digitalization and domestic chip manufacturing further strengthen regional demand. The expanding role of APAC as a global electronics manufacturing hub enhances large-scale adoption of photodiode sensors.

Japan Photodiode Sensors Market Insight

The Japan photodiode sensors market is gaining momentum due to the country’s advanced electronics industry and strong focus on precision engineering. High adoption of photodiodes in imaging systems, robotics, and medical devices supports steady growth. Japan’s leadership in optical technologies and sensor miniaturization drives innovation in high-performance detection systems. The increasing development of smart infrastructure and next-generation automotive technologies further accelerates market expansion.

China Photodiode Sensors Market Insight

The China photodiode sensors market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to rapid expansion of telecommunications networks and large-scale electronics manufacturing. China’s strong domestic semiconductor ecosystem supports high-volume production of optoelectronic components. Growing demand for consumer electronics, industrial automation, and surveillance systems significantly propels adoption. The country’s investments in smart cities, 5G infrastructure, and advanced manufacturing technologies continue to strengthen its dominant regional position.

Photodiode Sensors Market Share

The photodiode sensors industry is primarily led by well-established companies, including:

- Everlight Electronics Co., Ltd. (Taiwan)

- OSRAM Opto Semiconductors GmbH (Germany)

- ROHM CO., LTD. (Japan)

- Hamamatsu Photonics K.K. (Japan)

- Thorlabs, Inc. (U.S.)

- TT electronics (U.K.)

- First Sensor AG (Germany)

- Edmund Optics Inc. (U.S.)

- Semiconductor Components Industries, LLC (U.S.)

- Global Communication Semiconductors, LLC (U.S.)

- KYOTO SEMICONDUCTOR Co., Ltd. (Japan)

- Vishay Intertechnology, Inc. (U.S.)

- Centronic (U.K.)

- APIC Corporation (Japan)

- Diodes Incorporated (U.S.)

- Agilent Technologies, Inc. (U.S.)

- New Japan Radio Co., Ltd. (Japan)

- LuxNet Corporation (Japan)

- Central Semiconductor Corp. (U.S.)

Latest Developments in Global Photodiode Sensors Market

- In December 2025, Imec demonstrated the integration of colloidal quantum-dot photodiodes on 300 mm CMOS wafers, advancing scalable short-wave infrared (SWIR) sensing technology for high-volume semiconductor manufacturing. This development is expected to significantly reduce production costs while improving sensitivity and resolution in SWIR photodiode sensors. The innovation strengthens commercial viability across automotive LiDAR, industrial inspection, environmental monitoring, and smart agriculture applications. By enabling compatibility with standard CMOS processes, it accelerates broader adoption of advanced infrared photodiode sensors in mass-market electronics

- In June 2025, Sony Semiconductor Solutions introduced the IMX479 stacked SPAD depth sensor designed for automotive LiDAR systems, delivering a detection range of up to 300 meters with enhanced photon-detection efficiency. This advancement supports higher precision object recognition and long-range depth mapping in advanced driver-assistance systems and autonomous vehicles. The improved efficiency enhances performance in low-light and high-speed driving environments, strengthening the competitiveness of SPAD-based photodiode architectures. As automotive manufacturers increasingly prioritize safety and automation, such innovations drive substantial growth opportunities in the photodiode sensors market

- In May 2025, Lawrence Livermore National Laboratory unveiled an electrophoretic quantum-dot deposition method that enhances near-infrared detector performance on textured and non-planar substrates. This technique improves light absorption efficiency and uniformity, which can significantly enhance sensitivity in near-infrared photodiode sensors. The breakthrough supports advancements in telecommunications, biomedical imaging, and spectroscopy applications requiring high-precision optical detection. By enabling improved detector fabrication on complex surfaces, the development expands design flexibility and performance capabilities within the photodiode sensor industry

- In April 2025, TDK demonstrated the world’s first Spin Photo Detector capable of achieving tenfold data-rate improvements compared to conventional photodetectors. This innovation introduces a new approach to high-speed optical data conversion, particularly benefiting AI accelerator interconnects and high-bandwidth computing environments. The increased transmission speed and signal efficiency support the growing demand for faster data processing in data centers and advanced computing systems. Such advancements reinforce the expanding role of next-generation photodiode technologies in high-performance communication infrastructure

- In March 2025, onsemi launched the Hyperlux ID real-time indirect time-of-flight sensor capable of depth sensing up to 30 meters for industrial environments. This solution enhances precision 3D sensing capabilities in factory automation, robotics, and machine vision systems. By delivering improved depth accuracy and reliability in challenging lighting conditions, it strengthens the integration of photodiode-based sensing modules in industrial automation platforms. The launch contributes to rising demand for advanced optical sensing solutions in smart manufacturing and industrial digitalization initiatives

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Photodiode Sensors Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Photodiode Sensors Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Photodiode Sensors Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.