Global Plaque Psoriasis Market

Market Size in USD Billion

CAGR :

%

USD

1.20 Billion

USD

1.98 Billion

2025

2033

USD

1.20 Billion

USD

1.98 Billion

2025

2033

| 2026 –2033 | |

| USD 1.20 Billion | |

| USD 1.98 Billion | |

| % | |

|

Plaque Psoriasis Market Size

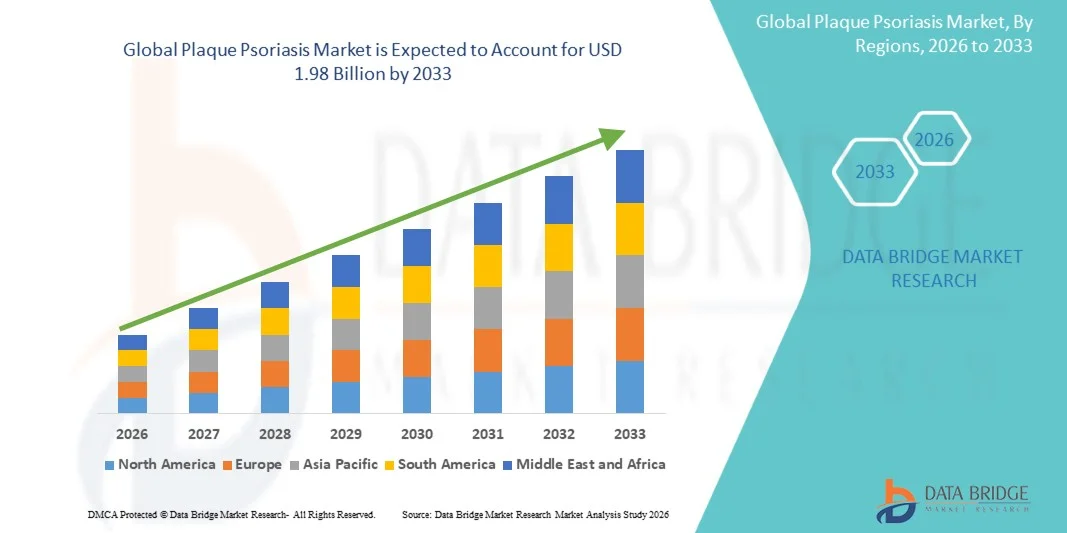

- The global plaque psoriasis market size was valued at USD 1.20 billion in 2025 and is expected to reach USD 1.98 billion by 2033, at a CAGR of 6.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of plaque psoriasis, rising awareness regarding skin health, and continuous advancements in dermatological treatments, leading to improved diagnosis and management across both clinical and homecare settings

- Furthermore, growing patient demand for effective, safe, and long-term treatment options, along with increasing adoption of biologics, targeted therapies, and advanced topical formulations, is establishing modern psoriasis treatments as the standard of care. These converging factors are accelerating the uptake of plaque psoriasis solutions, thereby significantly boosting the industry’s growth

Plaque Psoriasis Market Analysis

- Plaque psoriasis, a chronic autoimmune skin disorder, is increasingly a focus of modern dermatology due to its rising prevalence, impact on quality of life, and demand for effective and safe treatment options. The market is driven by the introduction of biologics, targeted therapies, and advanced topical formulations that improve patient outcomes and adherence

- The growing demand for plaque psoriasis therapies is primarily fueled by increasing awareness of skin health, expanding access to dermatology clinics, and rising investment in clinical trials and research for novel treatments. The market is also benefiting from digital platforms that enhance patient monitoring and education

- North America dominated the plaque psoriasis market with the largest revenue share of approximately 41.3% in 2025, supported by the presence of major pharmaceutical companies, advanced research infrastructure, and strong healthcare spending in the U.S.

- Asia-Pacific is expected to be the fastest-growing region in the plaque psoriasis market, with a projected CAGR of 9.5%, driven by increasing urbanization, rising healthcare awareness, expanding access to dermatology services, and growing investments in clinical research in countries such as China and India

- The injectable segment dominated the largest market revenue share of 52.3% in 2025, primarily due to the prevalence of biologic therapies administered via subcutaneous or intravenous injections

Report Scope and Plaque Psoriasis Market Segmentation

|

Attributes |

Plaque Psoriasis Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Plaque Psoriasis Market Trends

“Rising Prevalence of Autoimmune and Chronic Skin Disorders”

- Plaque psoriasis is increasingly recognized as a chronic autoimmune disorder affecting skin and overall quality of life, driving global market demand for effective treatments

- For instance, in 2024, AbbVie reported a surge in Humira prescriptions globally, reflecting rising diagnosis and treatment rates of moderate-to-severe plaque psoriasis

- The prevalence of psoriasis is higher in North America and Europe, with approximately 2–3% of the population affected, indicating a persistent market opportunity

- Advances in biologics, oral systemic therapies, and phototherapy are enabling personalized treatment approaches, improving patient adherence

- Healthcare systems are emphasizing early diagnosis and integrated dermatology care, including patient counseling and education

- Increased awareness campaigns by patient advocacy groups are contributing to higher diagnosis rates and better treatment compliance

- Technological advancements in diagnostic tools, such as digital skin imaging and AI-assisted disease monitoring, support timely and accurate disease assessment

- The growth of telemedicine platforms has improved access to dermatological consultations, especially in remote or underserved regions

- Chronic nature of the disease encourages long-term therapy adherence, providing recurring demand for both biologic and non-biologic treatments

- Global research focus on understanding genetic and immunological mechanisms of psoriasis is supporting pipeline development and innovative therapies

Plaque Psoriasis Market Dynamics

Driver

“Expanding Biologic and Targeted Therapy Adoption”

- Rapid adoption of biologics and targeted therapies with better efficacy and safety profiles is a major driver for market growth

- For instance, in 2025, Janssen Pharmaceuticals expanded U.S. distribution of Tremfya (guselkumab) following FDA approval for moderate-to-severe plaque psoriasis, improving patient access

- Availability of insurance coverage and reimbursement programs in developed countries encourages higher adoption of high-cost therapies

- Emergence of biosimilars in both developed and emerging markets is improving affordability and increasing patient access

- Increasing physician awareness about the benefits of targeted therapies is driving more prescriptions over conventional systemic treatments

- Expanding clinical trial activity globally is accelerating approval of novel therapies and encouraging adoption

- Pharmaceutical companies are investing in patient support programs, including financial assistance and adherence initiatives

- Rising prevalence of moderate-to-severe psoriasis cases is shifting treatment patterns towards advanced therapies

- Collaboration between biotech companies and healthcare providers is enhancing access to cutting-edge therapies and boosting market penetration

- Growing patient preference for therapies with fewer side effects and convenient administration methods is positively influencing market growth

Restraint/Challenge

“High Treatment Costs and Limited Access in Developing Regions”

- High cost of biologics and advanced therapies is a major restraint, limiting access for price-sensitive patients in low- and middle-income countries

- For instance, the average annual cost of biologic treatment in the U.S. exceeds USD50,000, restricting adoption for uninsured or underinsured populations

- Inconsistent healthcare infrastructure in developing regions reduces availability of advanced therapies

- Limited number of dermatology specialists in certain regions delays diagnosis and treatment initiation

- Regulatory hurdles in emerging markets slow the approval and availability of new therapies

- Patient adherence challenges, due to side effects or complicated dosing schedules, can limit treatment effectiveness and market growth

- High out-of-pocket costs for combination therapies pose additional challenges for patients requiring multiple treatments

- Lack of awareness about modern therapies among patients and healthcare providers in some regions limits market penetration

- Distribution and supply chain limitations affect availability of biologics in remote or rural areas

- Addressing these challenges requires expansion of insurance coverage, development of cost-effective biosimilars, patient education, and strategic policy interventions to improve access and affordability

Plaque Psoriasis Market Scope

The market is segmented on the basis of treatment, route of administration, end users, and distribution channel.

- By Treatment

On the basis of treatment, the Plaque Psoriasis market is segmented into topical therapy, phototherapy, systemic agents, biologic therapies, and others. The biologic therapies segment dominated the largest market revenue share of 44.5% in 2025, driven by its high efficacy in moderate-to-severe plaque psoriasis cases and targeted action on specific immune pathways. Patients and dermatologists prefer biologics due to their sustained clinical response and reduced systemic side effects. Rapid adoption in hospitals and specialty centers further boosts the segment’s share. Continuous R&D and the approval of next-generation biologics enhance market penetration. Pharmaceutical companies focus on developing biosimilars, increasing accessibility. Growing awareness of disease management and patient support programs accelerates adoption. Biologics benefit from insurance coverage in developed markets. Integration with digital patient monitoring and adherence programs enhances uptake. High prevalence of chronic plaque psoriasis globally supports demand. Expanding pipelines in North America and Europe sustain revenue dominance. Technological advancements in drug formulation improve safety and patient convenience. Government incentives for innovative therapies further strengthen growth.

The systemic agents segment is expected to witness the fastest CAGR of 19.2% from 2026 to 2033, driven by increasing adoption for moderate-to-severe cases where topical therapies are insufficient. Growth is supported by the rising prevalence of psoriasis and the need for combination therapy. Development of novel small molecules with improved safety profiles accelerates adoption. Expansion of hospital and specialty center networks enables broader patient access. Pharmaceutical research focuses on personalized therapy and targeted treatments. Increasing patient awareness and education programs enhance uptake. Systemic agents offer flexible dosing and route options, promoting compliance. Insurance coverage and reimbursement policies in developed regions facilitate market penetration. Clinical guidelines recommending systemic therapy for severe cases support growth. Emerging markets in Asia-Pacific show rapid adoption due to improving healthcare infrastructure. Continuous innovation in oral and injectable systemic formulations drives market momentum. Collaboration between manufacturers and healthcare providers accelerates distribution.

- By Route of Administration

On the basis of route of administration, the Plaque Psoriasis market is segmented into oral and injectable. The injectable segment dominated the largest market revenue share of 52.3% in 2025, primarily due to the prevalence of biologic therapies administered via subcutaneous or intravenous injections. Injectable treatments are preferred for their precision, efficacy, and long dosing intervals, improving patient adherence. Hospitals and specialty centers often recommend injectables for moderate-to-severe cases. Technological advances in auto-injectors and prefilled syringes enhance patient convenience. Biologic therapies delivered via injections maintain higher clinical outcomes, driving adoption. Expanding insurance coverage for injectable therapies supports market dominance. Physicians prioritize injectables due to predictable pharmacokinetics and safety profiles. Global awareness campaigns for psoriasis management encourage injectable use. R&D pipelines focused on innovative injectable formulations sustain growth. Integration with patient support and monitoring programs enhances adherence. Regulatory approvals of new injectable biologics boost revenue. Expanding distribution networks in developed and emerging markets further strengthen adoption.

The oral segment is expected to witness the fastest CAGR of 17.8% from 2026 to 2033, driven by the development of novel small-molecule drugs and JAK inhibitors suitable for oral administration. Oral therapies offer convenience, improved patient compliance, and reduced need for clinic visits. Rising adoption in emerging markets with growing healthcare infrastructure supports growth. Pharmaceutical companies invest in research to improve oral bioavailability and minimize adverse effects. Increasing prevalence of chronic plaque psoriasis globally contributes to market expansion. Collaboration between manufacturers and specialty pharmacies enhances accessibility. Oral administration is particularly preferred for patients averse to injections. Health insurance coverage and reimbursement policies for oral drugs facilitate adoption. Clinical trials exploring combination oral therapies accelerate innovation. Patient education on oral therapies improves adherence and acceptance. Expansion of online pharmacies and telemedicine channels boosts oral therapy reach. Emerging technology in drug delivery systems enhances therapeutic outcomes.

- By End Users

On the basis of end users, the market is segmented into hospitals, homecare, specialty centers, and others. The hospitals segment dominated the largest market revenue share of 48.7% in 2025, driven by widespread access to dermatology departments, experienced medical staff, and advanced treatment facilities. Hospitals provide both biologic and systemic therapies with proper monitoring and support. Adoption is fueled by rising prevalence of moderate-to-severe plaque psoriasis and patient trust in clinical expertise. Integration with patient assistance programs and insurance coverage strengthens hospital utilization. Ongoing research collaborations and clinical trials in hospital settings enhance treatment options. Hospitals provide comprehensive care including combination therapies and long-term management. Technological advancements in hospital-based administration of biologics support patient compliance. Government and private healthcare initiatives increase patient inflow. Hospitals are preferred for monitoring adverse events and therapeutic outcomes. Partnerships with pharmaceutical companies enable access to innovative therapies. Expansion of hospital networks in emerging markets drives further adoption. Continuous training and clinical updates for dermatologists improve service quality.

The homecare segment is expected to witness the fastest CAGR of 16.9% from 2026 to 2033, driven by increasing preference for self-administration of biologics and oral therapies at home. Growth is supported by patient awareness programs and digital health monitoring tools. Telemedicine and homecare services provide guidance on dosage, adherence, and side-effect management. Rising patient preference for convenience and reduced hospital visits accelerates adoption. Healthcare providers encourage home-based therapy for mild-to-moderate cases. Emerging markets show increasing uptake of homecare solutions due to limited hospital access. Collaboration between pharmaceutical companies and homecare service providers expands market reach. Innovative devices like auto-injectors improve patient confidence and safety. Insurance coverage for homecare administration supports growth. Continuous patient education on self-administration enhances compliance. Homecare adoption reduces healthcare system burden while improving patient satisfaction. Digital apps and remote monitoring platforms reinforce rapid uptake. Expansion in specialty pharmacies enables wider distribution of homecare therapies.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, online pharmacy, and retail pharmacy. The hospital pharmacy segment dominated the largest market revenue share of 54.2% in 2025, driven by direct availability of biologics and systemic agents at hospitals. Hospitals ensure proper storage, handling, and administration of complex therapies. Direct engagement with patients improves adherence and clinical outcomes. Pharmaceutical companies collaborate with hospital pharmacies for clinical trial integration and patient support programs. Hospital pharmacies benefit from insurance coverage and reimbursement for high-cost therapies. Established hospital networks facilitate accessibility and continuous supply. Professional guidance and monitoring enhance patient trust in medications. Integration with hospital electronic medical records improves treatment tracking. Patient education and counseling programs strengthen segment adoption. Expansion of hospital pharmacies in emerging regions supports market penetration. Availability of advanced formulations like prefilled syringes increases preference. Hospital pharmacies provide bundled therapies and monitoring services to improve outcomes. Continuous growth of hospital infrastructure globally reinforces revenue dominance.

The online pharmacy segment is expected to witness the fastest CAGR of 18.5% from 2026 to 2033, driven by the rise of e-commerce platforms and telemedicine services enabling remote access to therapies. Online pharmacies offer convenience, privacy, and doorstep delivery for chronic therapy patients. Digital platforms facilitate prescription verification and patient counseling. Adoption is fueled by growing internet penetration and smartphone usage, particularly in emerging markets. Partnerships with pharmaceutical companies and logistics providers improve availability and reliability. Online channels reduce geographical barriers to therapy access. Patient awareness and educational campaigns enhance acceptance of online pharmacies. Advanced inventory management and tracking systems ensure timely supply. Integration with mobile applications enables therapy reminders and monitoring. Increasing insurance coverage for online orders supports growth. Telehealth services complement online pharmacy adoption for continuous care. Expansion of online specialty pharmacies boosts global reach and accessibility.

Plaque Psoriasis Market Regional Analysis

- North America dominated the plaque psoriasis market with the largest revenue share of approximately 41.3% in 2025, supported by the presence of major pharmaceutical companies, advanced research infrastructure, and strong healthcare spending in the U.S. For instance, in 2024, AbbVie reported a significant increase in Humira and Skyrizi prescriptions in the U.S., reflecting high adoption of biologic therapies for moderate-to-severe plaque psoriasis

- High patient awareness and strong dermatologist networks in the region contribute to early diagnosis and treatment uptake. Robust insurance coverage and reimbursement policies encourage the use of advanced therapies. North America benefits from extensive clinical trial activity, supporting the launch of innovative therapies and pipeline growth

- Rising prevalence of autoimmune disorders and chronic skin conditions drives sustained demand for effective plaque psoriasis management. Pharmaceutical companies are increasingly introducing patient support programs to improve therapy adherence. Education campaigns and digital health platforms enhance awareness and facilitate remote monitoring of patient treatment outcomes. Strong government initiatives and private investments in dermatology research further support market expansion. Preference for combination therapies and newer biologics with improved safety profiles continues to propel regional market growth

U.S. Plaque Psoriasis Market Insight

The U.S. plaque psoriasis market captured the largest revenue share in 2025 within North America, driven by advanced R&D, early adoption of biologics, and strong healthcare infrastructure. For instance, Janssen Pharmaceuticals expanded distribution of Tremfya (guselkumab) in 2025 after FDA approval, reflecting high patient demand for targeted therapies. High healthcare expenditure and well-established dermatology clinics ensure accessibility of advanced treatments. The prevalence of moderate-to-severe psoriasis cases promotes adoption of biologics over traditional systemic therapies. Increasing patient awareness of long-term treatment benefits is driving adherence and prescription growth. Biosimilar introductions are gradually improving affordability while maintaining efficacy standards. Active patient support programs and co-pay assistance encourage therapy continuity. Strong physician engagement and treatment guideline adherence improve therapy uptake. The growing use of digital platforms and teledermatology supports remote care and chronic condition monitoring. Expanding clinical trial networks in the U.S. continue to introduce innovative treatment options, fueling market growth.

Europe Plaque Psoriasis Market Insight

The Europe plaque psoriasis market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by regulatory support, advanced healthcare infrastructure, and increasing patient awareness. For instance, Novartis launched Cosentyx campaigns across Germany and France in 2024, enhancing accessibility of biologic treatments for severe plaque psoriasis patients. Growing urbanization and an aging population contribute to rising prevalence. Rising investment in dermatology research and healthcare IT supports early diagnosis. Increasing adoption of biologics and combination therapies enhances patient outcomes. Healthcare reimbursement policies and government funding encourage therapy accessibility. Expansion of clinical centers and specialized dermatology clinics improves treatment reach. Patient education initiatives strengthen therapy adherence. High prevalence of moderate-to-severe psoriasis promotes long-term treatment uptake. Development of national psoriasis registries supports epidemiological research and market growth.

U.K. Plaque Psoriasis Market Insight

The U.K. plaque psoriasis market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing patient awareness and access to dermatology services. For instance, in 2023, Sandoz introduced biosimilar adalimumab widely across NHS hospitals, improving affordability and access. Increasing demand for biologics in moderate-to-severe cases drives market expansion. Robust healthcare infrastructure ensures therapy availability and patient adherence. Growing adoption of digital patient monitoring systems enhances chronic care management. Healthcare funding programs support biologic therapy uptake. E-commerce and pharmacy networks improve distribution of topical treatments. Clinical trial activity encourages early adoption of innovative therapies. Rising prevalence of comorbidities like psoriatic arthritis increases treatment demand. Physician education programs promote guideline-based therapy selection.

Germany Plaque Psoriasis Market Insight

Germany’s plaque psoriasis market is expanding at a considerable CAGR, fueled by advanced healthcare infrastructure and high R&D investment. For instance, Boehringer Ingelheim conducted extensive outreach for its Cosentyx biologic in 2024, enhancing patient access to targeted therapy. Increasing patient awareness and preventive dermatology programs support early intervention. Growing prevalence of chronic skin disorders increases therapy demand. Government reimbursement policies ensure access to biologics. High physician engagement improves adoption of advanced therapies. Clinical research initiatives support launch of new treatments. Patient support programs enhance adherence and long-term treatment outcomes. Integration of digital health solutions improves remote patient monitoring. Focus on sustainable healthcare and eco-conscious drug production aligns with market trends.

Asia-Pacific Plaque Psoriasis Market Insight

Asia-Pacific plaque psoriasis market is expected to be the fastest-growing region in the Plaque Psoriasis market, with a projected CAGR of 9.5%, driven by increasing urbanization, rising healthcare awareness, and expanding dermatology services. For instance, in 2025, Novartis and Pfizer expanded biologic therapy access in China and India, improving treatment options for moderate-to-severe psoriasis. Increasing investments in healthcare infrastructure support greater therapy access. Rising disposable incomes enable patients to afford advanced therapies. Growing clinical research activity promotes introduction of innovative treatments. Expanding biotech and CRO infrastructure accelerates therapy adoption. Increasing physician awareness encourages guideline-based prescribing. Teledermatology adoption improves access in rural areas. National psoriasis awareness campaigns support early diagnosis and treatment. Emergence of urban hospitals and specialty clinics improves patient outreach.

Japan Plaque Psoriasis Market Insight

Japan’s plaque psoriasis market is growing due to rising healthcare awareness, urbanization, and demand for advanced therapies. For instance, Eli Lilly expanded Taltz biologic access across Japanese dermatology centers in 2024, enhancing treatment availability. Aging population increases the need for user-friendly therapies. High insurance coverage improves affordability for patients. Strong physician networks ensure early intervention. Rising adoption of combination therapies supports treatment efficacy. Expansion of clinical trial programs introduces new biologics. Telemedicine platforms support remote patient management. Increasing digital monitoring improves adherence. Government initiatives support chronic disease management.

China Plaque Psoriasis Market Insight

China plaque psoriasis market accounted for the largest market revenue share in Asia-Pacific in 2025, driven by growing healthcare access, urbanization, and patient awareness. For instance, Janssen and Novartis launched educational programs in 2024, increasing awareness of biologic treatment options in major Chinese cities. Rising middle-class population increases affordability of advanced therapies. Government support for chronic disease management improves treatment access. Expansion of dermatology specialty hospitals enhances patient care. Growing clinical trial activity supports new drug introductions. Increasing use of digital health solutions enables remote monitoring. Physician education programs improve guideline-based therapy adoption. Biologic and biosimilar therapy availability increases treatment penetration. Urbanization and higher patient awareness contribute to long-term market growth.

Plaque Psoriasis Market Share

The Plaque Psoriasis industry is primarily led by well-established companies, including:

- AbbVie (U.S.)

- Johnson & Johnson (U.S.)

- Novartis (Switzerland)

- Amgen (U.S.)

- Pfizer (U.S.)

- Boehringer Ingelheim (Germany)

- Eli Lilly (U.S.)

- Sun Pharma (India)

- Valeant Pharmaceuticals (Canada)

- Celgene (U.S.)

- GSK (U.K.)

- Dermira (U.S.)

- Leo Pharma (Denmark)

- Sanofi (France)

- Horizon Therapeutics (U.S.)

- Mylan (U.S.)

- Ferring Pharmaceuticals (Switzerland)

- Bristol-Myers Squibb (U.S.)

- UCB Pharma (Belgium)

- Lundbeck (Denmark)

Latest Developments in Global Plaque Psoriasis Market

- In October 2023, the BIMZELX biologic therapy was approved by the U.S. Food and Drug Administration for the treatment of moderate‑to‑severe plaque psoriasis, offering a new IL‑17A and IL‑17F dual inhibitor option with strong clinical efficacy demonstrated in multiple Phase III studies

- In July 2023, Janssen Pharmaceuticals announced positive topline results from its Phase IIb FRONTIER 1 clinical trial evaluating the novel oral interleukin‑23 receptor antagonist JNJ‑2113 in adult patients with moderate‑to‑severe plaque psoriasis, marking advancement toward an oral biologic approach

- In March 2025, Johnson & Johnson reported comprehensive Phase III data for icotrokinra (JNJ‑2113) showing that the once‑daily oral IL‑23 receptor‑blocking peptide achieved co‑primary endpoints and was superior to deucravacitinib in moderate‑to‑severe plaque psoriasis, reinforcing the potential future shift toward effective oral therapies for psoriasis

- In July 2025, Johnson & Johnson submitted a New Drug Application (NDA) to the U.S. Food and Drug Administration seeking approval of icotrokinra, the first‑in‑class targeted oral peptide IL‑23 receptor antagonist for both adults and adolescents with moderate‑to‑severe plaque psoriasis based on strong Phase III evidence

- In February 2025, Teva Pharmaceuticals in partnership with Alvotech launched SELARSDI (ustekinumab‑aekn) in the United States, a biosimilar to Stelara, for treating plaque psoriasis, psoriatic arthritis, Crohn’s disease, and ulcerative colitis, offering more affordable access to established biologic therapy for patients

- In May 2025, the ZORYVE topical cream (0.3 %) was approved by the U.S. Food and Drug Administration for plaque psoriasis treatment in patients aged 6 years and older, expanding options for pediatric and adult topical therapy

- In September 2025, the TREMFYA IL‑23 inhibitor received FDA approval for the treatment of pediatric moderate‑to‑severe plaque psoriasis and active psoriatic arthritis in children aged 6 years and older, marking the first IL‑23 biologic approved for this younger patient population

- In December 2025, Sun Pharmaceutical Industries launched ILUMYA (tildrakizumab) in India to treat moderate‑to‑severe plaque psoriasis, bringing a globally well‑established IL‑23 inhibitor biologic to the Indian market after successful international adoption and strong clinical outcomes

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.