Global Plasmapheresis Periprocedural Care Equipments Market

Market Size in USD Billion

CAGR :

%

USD

1.76 Billion

USD

2.64 Billion

2025

2033

USD

1.76 Billion

USD

2.64 Billion

2025

2033

| 2026 - 2033 | |

| USD 1.76 Billion | |

| USD 2.64 Billion | |

| % | |

|

Plasmapheresis Periprocedural Care Equipments Market Size

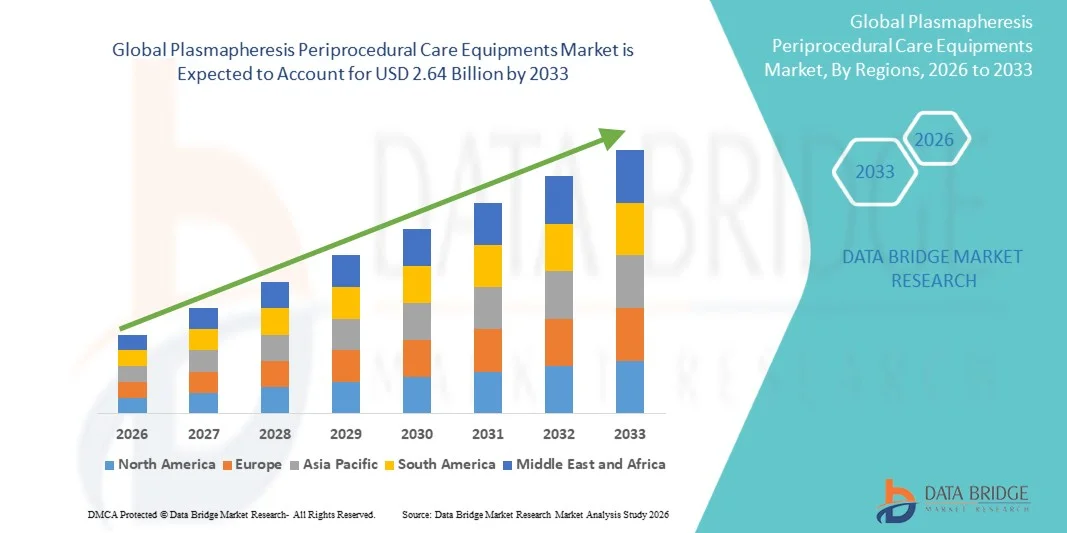

- The global plasmapheresis periprocedural care equipments market size was valued at USD 1.76 billion in 2025 and is expected to reach USD 2.64 billion by 2033, at a CAGR of 5.20% during the forecast period

- The market growth is largely fueled by the rising prevalence of chronic autoimmune, neurological, and hematological disorders, which are increasing the demand for advanced therapeutic plasmapheresis procedures in critical care and hospital settings

- Furthermore, increasing technological advancements in apheresis systems, membrane filtration, and centrifugation technologies are enhancing treatment efficiency, safety, and precision, thereby accelerating adoption across healthcare facilities

Plasmapheresis Periprocedural Care Equipments Market Analysis

- Plasmapheresis periprocedural care equipment, used for separating and removing plasma components from blood for therapeutic purposes, is becoming increasingly essential in modern healthcare systems due to its effectiveness in treating life-threatening immune and blood-related disorders

- The escalating demand for these systems is primarily driven by the growing burden of chronic diseases, expanding use in emergency and intensive care treatments, and continuous improvements in blood purification technologies that enhance procedural outcomes and patient safety

- North America dominated the plasmapheresis periprocedural care equipments market with a share of8% in 2025, due to high prevalence of autoimmune and hematological disorders along with advanced healthcare infrastructure

- Asia-Pacific is expected to be the fastest growing region in the plasmapheresis periprocedural care equipments market during the forecast period due to rising healthcare expenditure, expanding patient pool, and increasing awareness of advanced therapeutic procedures

- Centrifugation segment dominated the market with a market share of 62.6% in 2025, due to its high efficiency in separating plasma components based on density differences. It is widely preferred in clinical settings due to its reliability and ability to process larger blood volumes effectively. Centrifugation-based systems are extensively integrated into hospital workflows for both therapeutic and donation-based procedures

Report Scope and Plasmapheresis Periprocedural Care Equipments Market Segmentation

|

Attributes |

Plasmapheresis Periprocedural Care Equipments Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

· Asahi Kasei Kuraray Medical Co Ltd (Japan) · Terumo BCT Inc. (U.K.) · Fenwal (U.S.) · Haemonetics Corporation (U.S.) · Octapharma AG (Switzerland) · Therakos Ltd. (U.S.) · Grifols, S.A. (Spain) · B. Braun Melsungen AG (Germany) · Hemacare Corporation (U.S.) · Kawasumi Laboratories (Japan) · Fresenius Kabi AG (Germany) |

|

Market Opportunities |

· Expansion of Plasma-Derived Therapeutics Applications · Growth in Emerging Healthcare Infrastructure |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework. |

Plasmapheresis Periprocedural Care Equipments Market Trends

“Rising Adoption of Automated Apheresis Systems”

- A significant trend in the plasmapheresis periprocedural care equipments market is the increasing adoption of automated apheresis systems, driven by the need for improved procedural efficiency, accuracy, and patient safety in therapeutic blood purification processes. This automation is enhancing workflow consistency and reducing manual intervention in critical care environments

- For instance, Terumo BCT Inc. and Haemonetics Corporation provide advanced automated apheresis platforms widely used in hospitals and blood collection centers for plasma separation and therapeutic procedures. These systems improve processing speed and ensure standardized clinical outcomes across high-volume healthcare settings

- The integration of digital monitoring and real-time data tracking in apheresis systems is strengthening procedural control and enabling better patient-specific treatment adjustments. This is improving overall clinical decision-making and enhancing the reliability of plasmapheresis procedures

- Hospitals and specialized care centers are increasingly adopting automated systems to manage rising patient volumes requiring plasma exchange therapies. This shift is reducing operational burden on healthcare staff while improving treatment efficiency and safety standards

- The growing use of closed-system disposable kits alongside automated devices is improving infection control and reducing contamination risks during procedures. This is further supporting the transition toward fully integrated and safer plasmapheresis workflows

- The market is witnessing increased preference for automation-driven solutions as healthcare providers focus on improving procedural accuracy, reducing human error, and optimizing treatment time. This trend is significantly shaping the modernization of plasmapheresis care infrastructure globally

Plasmapheresis Periprocedural Care Equipments Market Dynamics

Driver

“Increasing Prevalence of Blood and Autoimmune Disorders”

- The plasmapheresis periprocedural care equipments market is primarily driven by the rising prevalence of autoimmune, neurological, and hematological disorders, which require plasma exchange therapies as part of critical treatment protocols. This growing disease burden is significantly increasing demand for advanced plasmapheresis procedures in hospital and intensive care settings

- For instance, Grifols S.A. and Octapharma AG are actively involved in plasma-based therapeutic ecosystems supporting treatments for conditions such as Guillain-Barré syndrome and myasthenia gravis, which rely on plasmapheresis procedures. Their involvement strengthens the clinical adoption of plasma separation technologies in disease management

- The increasing incidence of chronic inflammatory disorders is expanding the use of plasmapheresis as a supportive therapy to remove harmful antibodies from the bloodstream. This is driving consistent utilization of apheresis equipment across tertiary care hospitals

- Neurological complications requiring emergency plasma exchange are further contributing to higher procedural volumes in critical care units. This is reinforcing the need for reliable and high-performance periprocedural equipment

- The continuous growth in patient populations requiring advanced blood purification therapies is strengthening long-term demand for plasmapheresis equipment. This driver is playing a key role in sustaining market expansion across global healthcare systems

Restraint/Challenge

“High Cost and Operational Complexity of Equipment”

- The plasmapheresis periprocedural care equipments market faces significant challenges due to the high cost of advanced apheresis systems and the operational complexity involved in their usage. These factors limit adoption, particularly in small and resource-constrained healthcare facilities

- For instance, Fresenius Kabi AG and B. Braun Melsungen AG provide advanced blood management and apheresis systems that require specialized training and infrastructure for efficient operation. The complexity of these systems increases dependency on skilled professionals and elevates operational costs

- High initial investment costs associated with purchasing and installing plasmapheresis machines restrict their deployment in developing regions. This creates disparities in access to advanced therapeutic blood purification technologies

- Maintenance requirements and the need for regular calibration of precision-based systems further add to operational expenses for healthcare providers. This increases the overall cost burden on hospitals and clinics

- The combined effect of high equipment costs, maintenance needs, and operational complexity continues to restrain widespread adoption. This challenge remains a key barrier to broader market penetration despite rising clinical demand

Plasmapheresis Periprocedural Care Equipments Market Scope

The market is segmented on the basis of product, application, technology, procedure, and end use.

- By Product

On the basis of product, the plasmapheresis periprocedural care equipment market is segmented into disposable apheresis kits and apheresis machines. The disposable apheresis kits segment dominated the market with the largest revenue share in 2025, driven by rising emphasis on infection control and patient safety during blood separation procedures. Healthcare providers prefer disposable kits due to reduced risk of cross-contamination and simplified workflow in clinical settings. Increasing procedural volumes in hospitals further supports the demand for single-use consumables as they ensure consistent performance and regulatory compliance. The cost efficiency in sterilization and maintenance also strengthens their adoption across high-throughput facilities.

The apheresis machines segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by technological advancements in automated blood processing systems. These machines enable higher precision in plasma separation and improved patient monitoring during procedures. Rising investments in advanced therapeutic apheresis platforms across developed healthcare systems are accelerating adoption. The integration of digital controls and real-time data tracking further enhances procedural efficiency and clinical outcomes. Increasing demand for personalized treatment approaches also supports the expansion of this segment.

- By Application

On the basis of application, the market is segmented into renal disease, neurology, and hematology. The hematology segment dominated the market with the largest revenue share in 2025, driven by the high prevalence of blood-related disorders such as autoimmune conditions and clotting abnormalities. Plasmapheresis is widely used in hematological treatments to remove harmful antibodies and plasma components. Hospitals frequently adopt these procedures for managing severe and chronic cases requiring rapid therapeutic intervention. Growing awareness among clinicians regarding early intervention benefits further supports segment dominance.

The neurology segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing use of plasmapheresis in neurological disorders such as Guillain-Barré syndrome and multiple sclerosis. The therapy helps in reducing circulating antibodies that affect nerve function, improving patient recovery outcomes. Rising incidence of autoimmune neurological diseases is expanding clinical adoption globally. Advancements in neuro-therapeutic care protocols are further strengthening procedure acceptance. Expanding neurological treatment infrastructure in emerging healthcare systems is also contributing to growth.

- By Technology

On the basis of technology, the market is segmented into membrane filtration and centrifugation. The centrifugation segment dominated the market with the largest revenue share of 62.6% in 2025, driven by its high efficiency in separating plasma components based on density differences. It is widely preferred in clinical settings due to its reliability and ability to process larger blood volumes effectively. Centrifugation-based systems are extensively integrated into hospital workflows for both therapeutic and donation-based procedures. Their established clinical performance and adaptability across multiple indications further reinforce market leadership.

The membrane filtration segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing adoption of selective plasma separation techniques. This technology enables more targeted removal of plasma components while preserving essential blood elements. Growing preference for minimally invasive and patient-friendly procedures is accelerating its usage. Continuous improvements in membrane materials are enhancing filtration efficiency and reducing procedure time. Expanding use in specialized therapeutic applications is further supporting segment growth.

- By Procedure

On the basis of procedure, the market is segmented into photopheresis, LDL apheresis, plateletpheresis, leukapheresis, and erythrocytapheresis. The leukapheresis segment dominated the market with the largest revenue share in 2025, driven by its critical role in managing hematological malignancies and extreme leukocyte counts. It is widely used in emergency and oncology care settings to rapidly reduce white blood cell levels. Hospitals prioritize leukapheresis due to its life-saving application in acute conditions. Increasing cancer burden globally further strengthens its procedural demand.

The LDL apheresis segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by rising prevalence of cardiovascular diseases and familial hypercholesterolemia. The procedure effectively removes low-density lipoprotein cholesterol from the bloodstream, reducing long-term cardiac risks. Growing focus on preventive cardiovascular care is supporting adoption in both developed and emerging markets. Advances in selective adsorption technologies are improving treatment efficiency. Expanding clinical guidelines recommending LDL reduction therapies are further accelerating growth.

- By End Use

On the basis of end use, the market is segmented into hospitals and clinics, biopharmaceutical companies, and others. The hospitals and clinics segment dominated the market with the largest revenue share in 2025, driven by high patient inflow and availability of advanced therapeutic infrastructure. These settings serve as primary centers for plasmapheresis procedures due to access to trained professionals and critical care facilities. Increasing hospitalization rates for chronic and autoimmune diseases further support demand. Integration of advanced apheresis systems into hospital workflows strengthens segment leadership.

The biopharmaceutical companies segment is anticipated to witness the fastest growth rate from 2026 to 2033, driven by increasing use of plasmapheresis in plasma-derived drug production and research applications. Companies rely on plasma collection for developing immunoglobulins and other therapeutic proteins. Rising investments in biologics and plasma-based therapies are accelerating demand. Expanding clinical research activities and donor collection programs further support growth. Increasing focus on advanced biologic drug pipelines continues to drive segment expansion.

Plasmapheresis Periprocedural Care Equipments Market Regional Analysis

- North America dominated the plasmapheresis periprocedural care equipments market with the largest revenue share of 40.8% in 2025, driven by high prevalence of autoimmune and hematological disorders along with advanced healthcare infrastructure

- The region benefits from strong adoption of therapeutic apheresis procedures supported by well-established hospital systems and skilled clinical professionals. Increasing investments in advanced blood purification technologies and strong reimbursement frameworks further enhance market penetration

- Widespread availability of technologically advanced apheresis machines and consumables continues to support consistent procedural demand, establishing North America as the leading regional market

U.S. Plasmapheresis Periprocedural Care Equipments Market Insight

The U.S. plasmapheresis periprocedural care equipments market captured the largest revenue share in North America in 2025, driven by rising incidence of neurological and renal disorders requiring plasmapheresis treatments. The country benefits from early adoption of advanced therapeutic technologies and strong presence of key medical device manufacturers. Increasing clinical use of plasmapheresis in intensive care and emergency settings is further accelerating demand. Expanding healthcare expenditure and strong integration of advanced apheresis systems in hospitals continue to support market growth across the U.S.

Europe Plasmapheresis Periprocedural Care Equipments Market Insight

The Europe plasmapheresis periprocedural care equipments market is projected to expand at a substantial CAGR during the forecast period, supported by rising awareness of advanced blood purification therapies and structured healthcare systems. Increasing prevalence of chronic autoimmune conditions is driving higher adoption of plasmapheresis procedures across hospitals. Strong regulatory frameworks and emphasis on patient safety further support the use of advanced disposable kits and machines. Growing investments in hospital modernization and therapeutic innovations are enhancing procedural adoption across key European countries.

U.K. Plasmapheresis Periprocedural Care Equipments Market Insight

The U.K. plasmapheresis periprocedural care equipments market is anticipated to grow at a notable CAGR during the forecast period, driven by increasing cases of neurological disorders and expanding use of therapeutic apheresis. Rising focus on improving critical care infrastructure is supporting adoption of advanced plasmapheresis systems in hospitals. The presence of a well-developed public healthcare system ensures wider accessibility to advanced treatment procedures. Growing clinical awareness and preference for minimally invasive blood purification techniques are further supporting market expansion.

Germany Plasmapheresis Periprocedural Care Equipments Market Insight

The Germany plasmapheresis periprocedural care equipments market is expected to expand at a considerable CAGR during the forecast period, fueled by strong healthcare infrastructure and high adoption of advanced medical technologies. Increasing focus on precision medicine and immunotherapy treatments is driving demand for plasmapheresis procedures. The country’s emphasis on high-quality clinical standards supports the use of technologically advanced apheresis machines and consumables. Rising cases of chronic inflammatory and autoimmune diseases continue to strengthen market growth across Germany.

Asia-Pacific Plasmapheresis Periprocedural Care Equipments Market Insight

The Asia-Pacific plasmapheresis periprocedural care equipments market is poised to grow at the fastest CAGR from 2026 to 2033, driven by rising healthcare expenditure, expanding patient pool, and increasing awareness of advanced therapeutic procedures. Rapid urbanization and improving hospital infrastructure are supporting wider adoption of plasmapheresis technologies. Government initiatives focused on strengthening healthcare systems are further accelerating market penetration. Increasing availability of cost-effective apheresis solutions is expanding access across emerging economies in the region.

Japan Plasmapheresis Periprocedural Care Equipments Market Insight

The Japan plasmapheresis periprocedural care equipments market is gaining momentum due to high prevalence of autoimmune and neurological disorders and strong technological healthcare integration. The country’s advanced hospital infrastructure supports widespread use of sophisticated apheresis machines for therapeutic applications. Increasing aging population is further driving demand for plasma-based treatments. Strong focus on clinical precision and patient safety continues to support adoption of advanced plasmapheresis systems in both public and private healthcare facilities.

China Plasmapheresis Periprocedural Care Equipments Market Insight

The China plasmapheresis periprocedural care equipments market accounted for the largest revenue share in Asia-Pacific in 2025, driven by rapid healthcare infrastructure expansion and rising burden of chronic diseases. Increasing government support for healthcare modernization and hospital upgrades is boosting adoption of advanced apheresis systems. Growing awareness of blood purification therapies in tertiary care centers is further supporting demand. Strong domestic manufacturing capabilities and availability of cost-effective equipment continue to accelerate market growth across China.

Plasmapheresis Periprocedural Care Equipments Market Share

The plasmapheresis periprocedural care equipments industry is primarily led by well-established companies, including:

- Asahi Kasei Kuraray Medical Co Ltd (Japan)

- Terumo BCT Inc. (U.K.)

- Fenwal (U.S.)

- Haemonetics Corporation (U.S.)

- Octapharma AG (Switzerland)

- Therakos Ltd. (U.S.)

- Grifols, S.A. (Spain)

- B. Braun Melsungen AG (Germany)

- Hemacare Corporation (U.S.)

- Kawasumi Laboratories (Japan)

- Fresenius Kabi AG (Germany)

Latest Developments in Global Plasmapheresis Periprocedural Care Equipments Market

- In 2026, CytoSorbents expanded its extracorporeal blood purification portfolio through HotSwap launch and Aferetica partnership renewal, strengthening procedural efficiency in critical care plasmapheresis systems. This development enhances workflow efficiency in therapeutic blood purification by simplifying adsorber exchange processes during treatment. It improves procedural continuity and reduces operational complexity in intensive care settings. The strengthened collaboration with Aferetica supports innovation in extracorporeal therapy platforms, improving clinical adoption across hospitals. Overall, it reinforces the market shift toward integrated and simplified periprocedural care solutions

- In 2026, Haemonetics received FDA clearance for its NexSys PCS plasma collection system with Persona PLUS technology, advancing personalized plasma separation procedures. This approval strengthens market adoption of high-efficiency plasma collection systems by enabling donor-specific customization and improved plasma yield. It enhances operational productivity in plasma collection centers and supports rising demand for plasma-derived therapies. The innovation improves procedural flexibility while maintaining safety standards in large-scale blood processing environments. It further accelerates modernization of plasma separation infrastructure across developed healthcare markets

- In 2025, Fresenius Kabi introduced adaptive nomogram technology for its Aurora Xi plasmapheresis system, improving precision in plasma collection procedures. This advancement enhances market efficiency by optimizing plasma yield per donor and improving procedural accuracy in therapeutic and donation-based apheresis. It reduces variability in plasma collection outcomes, strengthening clinical reliability. The technology supports higher throughput in blood collection centers while maintaining donor safety. It reinforces the trend toward data-driven and patient-specific plasmapheresis systems

- In 2025, Terumo BCT expanded digital integration across its plasmapheresis platforms, enabling cloud-based monitoring and real-time device performance tracking. This development improves market operational efficiency by enabling remote monitoring and predictive maintenance of apheresis systems. It reduces downtime and enhances workflow management in hospitals and blood centers. Real-time analytics support better clinical decision-making during procedures. The integration of digital technologies strengthens adoption of connected plasmapheresis ecosystems globally

- In 2023, Asahi Kasei advanced modular multi-therapy apheresis platforms supporting procedures such as LDL apheresis and photopheresis within a single system. This innovation strengthens market flexibility by enabling multiple therapeutic applications on a unified platform. It reduces equipment dependency and improves cost efficiency for healthcare providers. Hospitals benefit from streamlined procedural workflows and enhanced treatment versatility. The development supports broader adoption of multi-functional plasmapheresis systems in advanced clinical settings

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.