Global Polymer Filler Market

Market Size in USD Billion

CAGR :

%

USD

62.36 Billion

USD

87.34 Billion

2025

2033

USD

62.36 Billion

USD

87.34 Billion

2025

2033

| 2026 –2033 | |

| USD 62.36 Billion | |

| USD 87.34 Billion | |

| % | |

|

Polymer Filler Market Overview

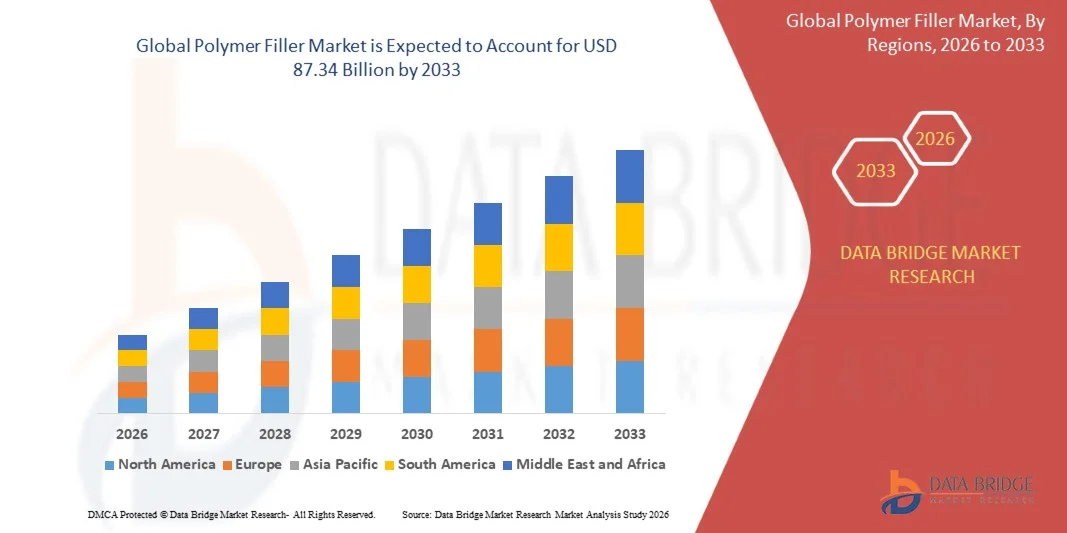

The Polymer Filler Market was valued at USD 62.36 billion in 2025 and is projected to reach USD 87.34 billion by 2033, growing at a CAGR of 4.30% from 2026 to 2033. The market is witnessing steady growth driven by increasing demand for lightweight and cost-effective polymer materials, rising utilization of fillers across packaging, automotive, construction, and electrical industries, and growing advancements in high-performance composite manufacturing technologies.

The expanding use of polymer fillers to improve mechanical strength, thermal stability, impact resistance, and dimensional stability in plastic products is encouraging manufacturers to increasingly incorporate mineral and specialty fillers into polymer formulations. Calcium carbonate, talc, silica, glass fibers, and carbon-based fillers are being widely adopted to enhance product durability and processing efficiency while reducing raw material costs across industrial manufacturing applications. In addition, rising demand for lightweight automotive components, increasing construction activities, and growing adoption of sustainable and recyclable polymer materials are further supporting market expansion globally.

Key Market Trends & Insights

- North America dominated the polymer filler market with the largest revenue share of 34.2% in 2025, supported by strong demand from automotive, packaging, and construction industries along with increasing adoption of advanced composite manufacturing technologies.

- Asia-Pacific is expected to be the fastest-growing region, recording a CAGR of 5.2% from 2026 to 2033. Growth is driven by rapid industrialization, expanding automotive production, rising infrastructure development activities, and increasing plastics manufacturing across China, India, Japan, and South Korea.

- The Inorganic segment held the largest market revenue share of approximately 72.4% in 2025 driven by its extensive use in automotive, construction, packaging, and industrial plastic applications. Inorganic fillers such as calcium carbonate, talc, silica, glass fibers, and mica are widely preferred due to their superior mechanical strength, thermal stability, dimensional rigidity, and cost-effectiveness in high-volume polymer manufacturing processes.

- The Organic segment is projected to register the fastest growth at a CAGR of 5.1% from 2026 to 2033, driven by increasing demand for lightweight, sustainable, and bio-based polymer composite materials across packaging and consumer goods industries. Rising focus on recyclable materials and environmentally friendly manufacturing processes is accelerating adoption of organic filler technologies globally.

- The Building and Construction segment accounted for the largest market revenue share of nearly 31.8% in 2025 driven by growing utilization of filled polymer materials in pipes, insulation systems, flooring products, cables, and structural components. Increasing infrastructure development activities and rising demand for durable, lightweight, and cost-efficient construction materials continue to support strong segment growth globally.

- The Automobile segment is expected to witness the fastest CAGR of 5.4% from 2026 to 2033 driven by rising demand for lightweight vehicle components, fuel-efficient automotive systems, and electric vehicle manufacturing applications. Automotive manufacturers are increasingly utilizing polymer fillers in dashboards, bumpers, interior trims, and battery housing systems to improve strength, reduce weight, and optimize production efficiency across modern vehicle platforms.

Market Size & Forecast

- Global Market Value (2025): USD 62.36 Billion

- Expected Market Value (2033): USD 87.34 Billion

- Forecast CAGR (2026–2033): 4.30%

- Leading Region in 2025: North America

- Fastest Growing Region: Asia-Pacific

Report Scope and Polymer Filler Market Segmentation

|

Attributes |

Polymer Filler Key Market Insights |

|

Segments Covered |

· By Type: Organic and Inorganic · By Application: Automobile, Electrical and Electronics, Building and Construction, Industrial, Packaging, and Others |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

• Trelleborg (Sweden) |

|

Market Opportunities |

• Rising Adoption Of Lightweight Polymer Composites In Automotive And Aerospace Industries |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Polymer Filler Market Trends

Trend: Rising Adoption Of Sustainable And High-Performance Polymer Composite Materials

Increasing demand for lightweight, durable, and cost-efficient polymer materials across automotive, construction, packaging, and consumer goods industries is accelerating the adoption of advanced polymer fillers globally. Conventional polymers often face limitations related to mechanical strength, thermal stability, dimensional rigidity, and processing efficiency, encouraging manufacturers to incorporate mineral and specialty fillers to improve overall material performance while reducing production costs.

In modern automotive manufacturing, companies are increasingly integrating fillers such as talc, calcium carbonate, silica, and glass fibers into polypropylene and engineering plastics, For instance for interior panels, dashboards, bumpers, and lightweight structural components, to reduce vehicle weight and improve fuel efficiency. In construction applications, polymer fillers are being utilized to enhance impact resistance, durability, and thermal insulation properties in pipes, cables, flooring, and insulation materials while optimizing raw material utilization and lowering manufacturing expenses.

The rapid expansion of flexible packaging, electric vehicles, and advanced infrastructure development projects is also increasing demand for high-performance polymer composites capable of delivering superior mechanical and barrier properties. In addition, growing regulatory focus on sustainable manufacturing and recyclable materials is encouraging adoption of bio-based and recycled fillers in polymer processing operations. Industry validation through automotive lightweighting programs during 2025 demonstrated that mineral-filled polypropylene composites reduced component weight by nearly 10–15% while improving stiffness and dimensional stability in selected vehicle interior applications.

Polymer Filler Market Dynamics

Key Market Driver: Rising Demand For Lightweight And Cost-Efficient Polymer Materials

Industries worldwide are increasingly focusing on reducing material costs, improving energy efficiency, and enhancing product durability across large-scale manufacturing operations. Conventional polymers often require performance enhancement to meet evolving industrial standards related to strength, thermal resistance, and structural stability, creating strong demand for filler materials capable of improving polymer functionality while optimizing production economics.

Industries such as automotive, packaging, construction, and electrical manufacturing are increasingly deploying polymer fillers to improve mechanical performance, reduce polymer consumption, and enhance processing efficiency in high-volume applications. Automotive manufacturers are actively utilizing fillers, For instance talc-filled polypropylene and glass fiber-reinforced plastics, to reduce vehicle weight and support fuel efficiency and emission reduction targets without compromising structural integrity.

Similarly, packaging manufacturers are integrating calcium carbonate and silica fillers into plastic films and rigid packaging products to improve stiffness, barrier properties, and cost competitiveness while reducing resin dependency. Real-world industrial deployments across Asia-Pacific and Europe during 2024 integrating mineral-filled polymer compounds into automotive and construction applications demonstrated raw material cost reductions of approximately 8–12% in selected high-volume manufacturing operations.

Key Restraint/Challenge: Processing Complexity And Performance Limitations In High-Load Applications

Polymer fillers can create processing challenges related to dispersion uniformity, compatibility, and flow behavior during large-scale polymer manufacturing operations. Poor filler distribution and inadequate bonding between filler particles and polymer matrices can negatively affect mechanical strength, surface finish, and long-term durability in high-performance applications.

In addition, certain specialty fillers and reinforcement materials involve high processing costs, complex compounding requirements, and specialized surface treatment technologies, increasing overall manufacturing expenses for advanced polymer composites. Excessive filler loading may also reduce flexibility, transparency, and impact resistance in selected packaging and consumer product applications, limiting broader commercial adoption in performance-sensitive industries.

Commercial manufacturing assessments indicate that high filler loading levels exceeding 40–50% in selected thermoplastic applications can reduce elongation performance and increase brittleness, while advanced engineered fillers and coupling agents may increase compound production costs by approximately 15–20% compared to standard polymer formulations.

Key Market Opportunity: Expanding Applications In Electric Vehicles And Sustainable Packaging

Modern electric vehicles, renewable energy systems, and advanced packaging solutions increasingly require lightweight, durable, and environmentally sustainable polymer materials capable of delivering superior performance characteristics under demanding operating conditions. Conventional plastic materials often face limitations related to thermal management, dimensional stability, and recyclability, creating strong demand for advanced polymer filler technologies with enhanced multifunctional properties.

Automotive companies are increasingly exploring polymer fillers, For instance glass fibers, nanoclays, and conductive carbon-based fillers, to improve EV battery housing performance, lightweight structural components, and thermal insulation systems without increasing manufacturing complexity. In packaging applications, rising demand for recyclable and sustainable materials is accelerating utilization of bio-based fillers and calcium carbonate compounds in flexible and rigid packaging products to reduce virgin plastic consumption and improve environmental performance.

In addition, advancements in nanotechnology, surface modification technologies, and hybrid composite development are improving filler compatibility and multifunctional performance, opening opportunities across aerospace, renewable energy, and electronics manufacturing sectors in Asia-Pacific and North America. EV component testing programs conducted during 2025 across China and Germany reported stiffness improvements of approximately 12–18% and weight reduction benefits of nearly 10% after integrating advanced mineral-filled polymer composites into selected battery enclosure and interior component applications.

Polymer Filler Market Scope

The market is segmented on the basis of type and application.

- By Type

On the basis of type, the polymer filler market is segmented into Organic and Inorganic. The Inorganic segment held the largest market revenue share of approximately 72.4% in 2025 driven by its extensive use in automotive, construction, packaging, and industrial plastic applications. Inorganic fillers such as calcium carbonate, talc, silica, glass fibers, and mica are widely preferred due to their superior mechanical strength, thermal stability, dimensional rigidity, and cost-effectiveness in high-volume polymer manufacturing processes.

The Organic segment is projected to register the fastest growth at a CAGR of 5.1% from 2026 to 2033, driven by increasing demand for lightweight, sustainable, and bio-based polymer composite materials across packaging and consumer goods industries. Rising focus on recyclable materials and environmentally friendly manufacturing processes is accelerating adoption of organic filler technologies globally.

- By Application

On the basis of application, the polymer filler market is segmented into Automobile, Electrical and Electronics, Building and Construction, Industrial, Packaging, and Others. The Building and Construction segment accounted for the largest market revenue share of nearly 31.8% in 2025 driven by growing utilization of filled polymer materials in pipes, insulation systems, flooring products, cables, and structural components. Increasing infrastructure development activities and rising demand for durable, lightweight, and cost-efficient construction materials continue to support strong segment growth globally.

The Automobile segment is expected to witness the fastest CAGR of 5.4% from 2026 to 2033 driven by rising demand for lightweight vehicle components, fuel-efficient automotive systems, and electric vehicle manufacturing applications. Automotive manufacturers are increasingly utilizing polymer fillers in dashboards, bumpers, interior trims, and battery housing systems to improve strength, reduce weight, and optimize production efficiency across modern vehicle platforms.

Polymer Filler Market Regional Analysis

North America Polymer Filler Market Insight

North America dominated the polymer filler market with the largest revenue share of 34.2% in 2025, supported by strong demand from automotive, packaging, and construction industries, along with increasing adoption of lightweight polymer composite materials. Manufacturers across the region are increasingly utilizing mineral and specialty fillers to improve material durability, thermal stability, and processing efficiency while reducing production costs. The region also benefits from advanced polymer manufacturing infrastructure, high investments in sustainable material technologies, and rising demand for recyclable plastic solutions across industrial and consumer applications.

U.S. Polymer Filler Market Insight

The U.S. polymer filler market captured the largest revenue share in 2025 within North America, fueled by growing demand for lightweight automotive components, advanced packaging materials, and high-performance construction products. Manufacturers are increasingly integrating fillers such as calcium carbonate, talc, and glass fibers into polymer compounds to improve mechanical performance and optimize raw material utilization. The growing adoption of electric vehicles, coupled with increasing investments in sustainable packaging and infrastructure modernization projects, is further propelling market expansion. Moreover, advancements in polymer processing technologies and composite material innovation are significantly contributing to industry growth.

Europe Polymer Filler Market Insight

The Europe polymer filler market is expected to witness significant growth from 2026 to 2033, primarily driven by stringent environmental regulations and rising demand for sustainable and recyclable polymer materials across automotive, packaging, and industrial sectors. European manufacturers are increasingly adopting advanced filler technologies to improve product performance while reducing carbon emissions and material consumption. The region is experiencing strong demand for lightweight composites in electric vehicles and energy-efficient building materials. Increasing investments in circular economy initiatives and bio-based material innovation are also supporting continued market expansion.

U.K. Polymer Filler Market Insight

The U.K. polymer filler market is expected to witness steady growth from 2026 to 2033, driven by rising utilization of filled polymer materials in packaging, construction, and consumer goods applications. Increasing focus on sustainable packaging regulations and recyclable plastic solutions is encouraging manufacturers to adopt high-performance filler technologies for material optimization and cost reduction. In addition, growing investments in infrastructure renovation and lightweight industrial materials are expected to continue stimulating market demand across the country.

Germany Polymer Filler Market Insight

The Germany polymer filler market is expected to witness strong growth from 2026 to 2033, fueled by increasing demand for lightweight engineering plastics and advanced automotive composite materials. Germany’s strong automotive manufacturing base and industrial processing capabilities are promoting large-scale adoption of polymer fillers in electric vehicles, industrial machinery, and high-performance construction applications. The country’s emphasis on sustainability, material efficiency, and advanced manufacturing technologies is further supporting adoption of innovative filler-enhanced polymer compounds across industrial sectors.

Asia-Pacific Polymer Filler Market Insight

The Asia-Pacific polymer filler market is expected to witness the fastest growth rate from 2026 to 2033, supported by rapid industrialization, expanding construction activities, and increasing automotive and packaging manufacturing across countries such as China, India, Japan, and South Korea. Rising demand for affordable and durable polymer materials is accelerating filler utilization across consumer goods, infrastructure, and industrial applications. Furthermore, the region’s growing role as a global manufacturing hub for plastics and polymer compounds is improving filler accessibility and production scalability across emerging economies.

Japan Polymer Filler Market Insight

The Japan polymer filler market is expected to witness strong growth from 2026 to 2033 due to increasing demand for high-performance engineering plastics, lightweight automotive materials, and advanced electronic components. Japanese manufacturers are increasingly integrating specialty fillers into polymers to improve dimensional stability, heat resistance, and durability across automotive and electronics applications. The country’s strong focus on technological innovation and advanced material science is also supporting development of next-generation polymer composite technologies for industrial and consumer applications.

China Polymer Filler Market Insight

The China polymer filler market accounted for the largest market revenue share in Asia Pacific in 2025, attributed to the country’s massive plastics manufacturing industry, rapid infrastructure development, and strong automotive and packaging production capabilities. China has emerged as one of the leading consumers and producers of polymer filler materials due to increasing demand for lightweight and cost-efficient plastic products across industrial and consumer sectors. The growing adoption of electric vehicles, expansion of construction activities, and rising investments in sustainable packaging manufacturing are further propelling market growth across the country.

Polymer Filler Market Share

The Polymer Filler industry is primarily led by well-established companies, including:

• Trelleborg (Sweden)

• Shin-Etsu Chemical Co., Ltd. (Japan)

• Dow (U.S.)

• The Chemours Company (U.S.)

• Momentive (U.S.)

• Saint-Gobain Performance Plastics (France)

• Solvay (Belgium)

• Lanxess (Germany)

• Esterline Technologies Corporation (U.S.)

• 3M (U.S.)

• Holland Shielding Systems BV (Netherlands)

• Jonal Laboratories Inc. (U.S.)

• PolyMod Technologies (U.S.)

• CHT R. Beitlich GmbH | CHT Group (Germany)

• Rogers Corporation (U.S.)

• Seal Science, Inc. (U.S.)

• TransDigm Group, Inc. (U.S.)

• Technetics Group (U.S.)

• Zeon Chemicals L.P. (U.S.)

• Parker Hannifin CORP (U.S.)

Latest Developments in Polymer Filler Market

- In March 2021, Quarzwerke GmbH announced the establishment of a new high-performance filler production facility in Dangjin, South Korea, as part of its strategic expansion across the Asia-Pacific region. The new manufacturing plant was developed to strengthen the company’s production capabilities for advanced mineral-based fillers used in plastics, coatings, and industrial applications. Through this expansion, the company aimed to improve supply chain efficiency, enhance regional customer support, and address rising demand for high-performance filler materials in Asia. The investment also reinforced the growth strategy of Quarzwerke’s HPF division focused on innovative mineral engineering technologies. The development supported increasing adoption of advanced filler solutions across automotive, construction, and industrial polymer manufacturing sectors globally.

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Polymer Filler Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Polymer Filler Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Polymer Filler Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.