Global Polysilicon Market

Market Size in USD Billion

USD

49.94 Billion

USD

113.44 Billion

2025

2033

USD

49.94 Billion

USD

113.44 Billion

2025

2033

| 2026 - 2033 | |

| USD 49.94 Billion | |

| USD 113.44 Billion | |

| % | |

|

Polysilicon Market Overview

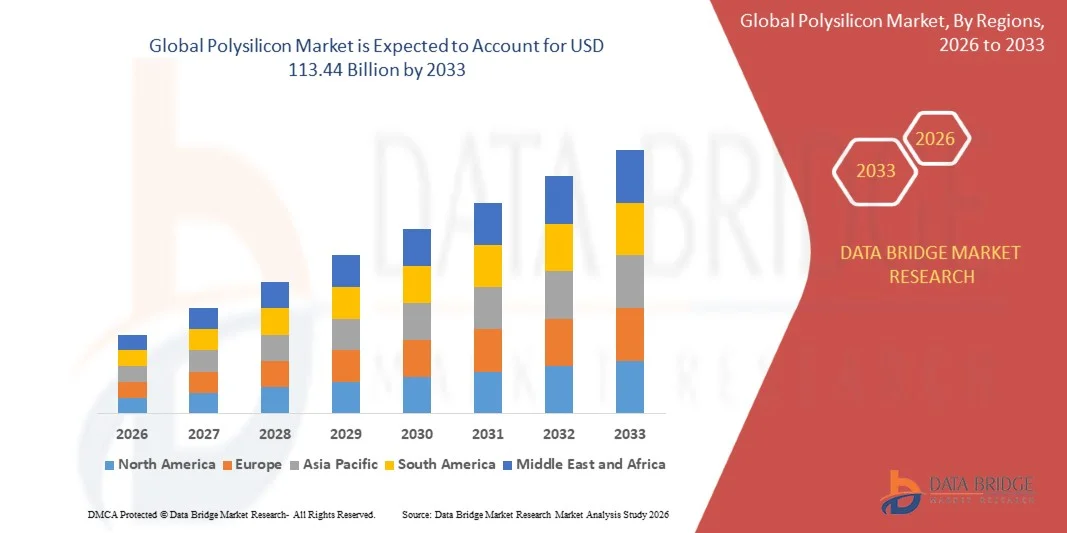

The global polysilicon market was valued at USD 49.94 billion in 2025 and is projected to reach USD 113.44 billion by 2033, growing at a CAGR of 10.80% from 2026 to 2033. The market is witnessing substantial growth driven by increasing demand for solar photovoltaic installations, rising adoption of renewable energy sources, and expanding semiconductor manufacturing activities across the globe. Growing investments in clean energy infrastructure and supportive government initiatives promoting decarbonization are further accelerating market expansion.

The increasing transition toward sustainable power generation, combined with strong demand for high-purity silicon materials in electronics and semiconductor applications, is encouraging manufacturers to expand production capacities and enhance technological capabilities. In addition, rapid urbanization, rising electricity consumption, and continuous advancements in solar cell efficiency are supporting polysilicon adoption in utility-scale and residential solar projects. The market is also benefiting from growing investments in domestic semiconductor manufacturing and the rising need for advanced electronic components across automotive, consumer electronics, and industrial sectors.

Key Market Trends & Insights

- Asia-Pacific dominated the polysilicon market with the largest revenue share in 2025, supported by massive solar photovoltaic manufacturing capacity, rapid expansion of renewable energy infrastructure, and strong semiconductor production activities across China, Japan, South Korea, and India

- North America is expected to be the fastest-growing region, recording a CAGR of from 2026 to 2033. Growth is driven by increasing investments in domestic semiconductor fabrication and solar manufacturing projects.

- The Siemens Process segment held the largest market revenue share of approximately 72.4% in 2025 driven by its ability to produce ultra-high-purity polysilicon required for semiconductor manufacturing and high-efficiency solar photovoltaic applications. The process is widely adopted due to its superior material purity, established industrial infrastructure, and extensive use among leading global manufacturers.

- The Fluidized Bed Reactor (FBR) Process segment is projected to register the fastest growth at a CAGR of 12.1% from 2026 to 2033, driven by rising demand for energy-efficient and lower-cost polysilicon production technologies. Increasing industry focus on reducing operational energy consumption and carbon emissions is accelerating adoption of FBR-based manufacturing systems among solar-grade polysilicon producers.

- The Chunks segment accounted for the largest market revenue share of nearly 58.7% in 2025 owing to its widespread use in photovoltaic wafer manufacturing and conventional solar ingot production processes. Chunks are extensively preferred due to their compatibility with large-scale crystal growth systems and cost-effective handling during manufacturing operations.

- The Granules segment is anticipated to witness the fastest growth at a CAGR of 11.6% from 2026 to 2033 driven by increasing adoption of fluidized bed reactor technologies and rising preference for continuous feeding processes in advanced solar manufacturing facilities. Improved operational efficiency and lower impurity generation are further supporting segment expansion.

- The Solar Photovoltaic segment dominated the market with a revenue share of approximately 86.3% in 2025 due to rapidly increasing global solar panel installations and strong government support for renewable energy infrastructure development. Rising adoption of utility-scale solar projects and expanding residential rooftop solar systems are significantly contributing to segment growth.

- The Electronics segment is expected to register the fastest CAGR of 9.8% from 2026 to 2033 driven by increasing semiconductor fabrication activities, rising demand for AI processors, and growing consumption of consumer electronics and electric vehicles. Expanding investments in domestic chip manufacturing facilities are further accelerating demand for electronic-grade polysilicon.

- The Photovoltaics segment held the largest market revenue share of around 61.9% in 2025 driven by increasing deployment of solar energy systems globally and strong transition toward clean electricity generation. Government incentives, declining solar installation costs, and rising environmental awareness are supporting widespread photovoltaic adoption.

- The Monocrystalline Solar Panel segment is projected to witness the fastest growth at a CAGR of 13.4% from 2026 to 2033 owing to increasing preference for high-efficiency solar modules with superior energy conversion performance. Rapid technological advancements in TOPCon and heterojunction cell technologies are further driving demand for premium-grade polysilicon materials in monocrystalline panel production.

- The Series Connection segment accounted for the largest market revenue share of nearly 67.2% in 2025 due to its widespread adoption in photovoltaic systems requiring higher voltage output and improved energy transmission efficiency. The segment is extensively utilized across utility-scale solar farms and commercial renewable energy installations.

- The Parallel Connection segment is anticipated to register the fastest growth at a CAGR of 10.3% from 2026 to 2033 driven by increasing adoption in small-scale solar applications, distributed energy systems, and advanced electronic configurations requiring stable current distribution. Rising deployment of residential solar systems and backup power applications is further supporting segment expansion.

Market Size & Forecast

- Global Market Value (2025): USD 49.94 Billion

- Expected Market Value (2033): USD 113.44 Billion

- Forecast CAGR (2026–2033): 10.80%

- Leading Region in 2025: Asia-Pacific

- Fastest Growing Region: North America

Report Scope and Polysilicon Market Segmentation

|

Attributes |

Polysilicon Key Market Insights |

|

Segments Covered |

· By Manufacturing Technology: Siemens Process, Fluidized Bed Reactor (FBR) Process, and Upgraded Metallurgical-Grade Silicon Process · By Form: Chunks, Granules, and Rods · By End User Industry: Solar Photovoltaic and Electronics · By Application: Photovoltaics, Monocrystalline Solar Panel, Multicrystalline Solar Panel, Electronics, Civilian Solar Small Equipment, and Others · By Product Type: Series Connection and Parallel Connection |

|

Countries Covered |

North America · U.S. · Canada · Mexico Europe · Germany · France · U.K. · Netherlands · Switzerland · Belgium · Russia · Italy · Spain · Turkey · Rest of Europe Asia-Pacific · China · Japan · India · South Korea · Singapore · Malaysia · Australia · Thailand · Indonesia · Philippines · Rest of Asia-Pacific Middle East and Africa · Saudi Arabia · U.A.E. · South Africa · Egypt · Israel · Rest of Middle East and Africa South America · Brazil · Argentina · Rest of South America |

|

Key Market Players |

|

|

Market Opportunities |

• Expansion Of Renewable Energy Infrastructure |

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include import export analysis, production capacity overview, production consumption analysis, price trend analysis, climate change scenario, supply chain analysis, value chain analysis, raw material/consumables overview, vendor selection criteria, PESTLE Analysis, Porter Analysis, and regulatory framework. |

Global Polysilicon Market Trends

Trend: Rapid Expansion Of Solar Photovoltaic Installations And Domestic Semiconductor Manufacturing

Increasing global focus on renewable energy generation, energy security, and advanced electronics manufacturing is significantly driving demand for high-purity polysilicon across solar photovoltaic and semiconductor industries. Governments worldwide are introducing aggressive carbon neutrality targets and renewable energy deployment programs, encouraging large-scale solar infrastructure investments and expansion of domestic supply chains for critical semiconductor materials.

In the solar industry, manufacturers are increasing installations of monocrystalline solar panels that require ultra-high-purity polysilicon to improve energy conversion efficiency and panel durability. Countries such as China, India, and the U.S. are rapidly expanding solar manufacturing ecosystems to reduce dependence on imports and strengthen local clean energy production. In semiconductor manufacturing, growing demand for AI processors, electric vehicles, and advanced consumer electronics is increasing the requirement for electronic-grade polysilicon with superior purity levels.

The market is also benefiting from large-scale production capacity expansions globally. For instance, China accounted for over 80% of global polysilicon production capacity in 2025, while India announced multiple integrated solar manufacturing projects under production-linked incentive schemes to strengthen domestic solar supply chains. In addition, advanced polysilicon technologies capable of improving wafer efficiency by nearly 2–3% are gaining strong commercial traction among photovoltaic manufacturers

Global Polysilicon Market Dynamics

Key Market Driver: Rising Investments In Renewable Energy And Solar Power Infrastructure

Governments and private energy companies worldwide are significantly increasing investments in solar photovoltaic infrastructure to reduce dependence on fossil fuels and achieve long-term decarbonization goals. Rising electricity demand, supportive policy frameworks, and declining solar installation costs are accelerating the deployment of utility-scale and residential solar power projects, directly driving consumption of solar-grade polysilicon.

Major economies such as China, the U.S., India, and European countries are introducing subsidies, tax incentives, and clean energy transition programs to expand solar energy capacity. Polysilicon manufacturers are correspondingly scaling up production capacities to meet growing demand from photovoltaic module manufacturers. In addition, rapid electrification and grid modernization initiatives are further supporting long-term market expansion.

Large-scale industrial developments are strengthening supply security across the market. For instance, several Chinese manufacturers expanded polysilicon output capacities beyond 1 million metric tons collectively during 2024–2025 to address rising global solar panel demand. Similarly, the U.S. Inflation Reduction Act continues to stimulate investments in domestic solar manufacturing and integrated polysilicon production facilities.

Key Restraint/Challenge: High Energy Consumption And Supply Chain Volatility

Polysilicon production remains highly energy intensive due to the complex purification and chemical vapor deposition processes required to achieve high-purity silicon grades. Fluctuations in electricity prices, raw material availability, and transportation costs significantly impact production economics and profit margins for manufacturers. The industry also faces environmental scrutiny related to carbon emissions and energy usage associated with large-scale polysilicon manufacturing operations.

In addition, supply chain disruptions and trade restrictions between major economies are creating uncertainty in raw material sourcing and global distribution networks. Dependence on limited regional production hubs increases vulnerability to geopolitical tensions and pricing fluctuations, particularly in solar manufacturing supply chains. High capital expenditure requirements for establishing new purification and production facilities further restrict market entry for smaller manufacturers.

Commercial market assessments indicate that electricity expenses account for nearly 30–40% of total polysilicon production costs in conventional manufacturing processes. Furthermore, periodic oversupply conditions in China during 2023–2025 created sharp fluctuations in global polysilicon pricing, impacting profitability across photovoltaic supply chains.

Key Market Opportunity: Growing Adoption In Advanced Semiconductor And Next-Generation Solar Technologies

Rapid advancements in semiconductor technologies, AI computing infrastructure, electric vehicles, and high-efficiency photovoltaic systems are creating strong opportunities for high-purity electronic-grade polysilicon manufacturers. Increasing demand for advanced chips, memory devices, and power semiconductors is accelerating investments in semiconductor fabrication facilities globally, particularly across Asia-Pacific, North America, and Europe.

Solar manufacturers are also increasingly adopting next-generation photovoltaic technologies such as TOPCon and heterojunction solar cells that require higher-quality polysilicon materials for improved energy efficiency and long-term reliability. The expansion of smart grids, battery storage systems, and renewable energy integration projects is further strengthening demand for high-performance solar modules and related raw materials.

In addition, governments are encouraging localized semiconductor and solar supply chains to reduce import dependence and improve strategic technological independence. For instance, semiconductor investments announced in the U.S., India, Japan, and South Korea during 2025 exceeded several billion dollars collectively, directly supporting future demand for ultra-high-purity polysilicon materials. Advanced solar modules utilizing next-generation cell architectures have also demonstrated efficiency improvements exceeding 24–26% under commercial deployment conditions, increasing the requirement for premium polysilicon feedstock.

Global Polysilicon Market Scope

The market is segmented on the basis of manufacturing technology, form, end user industry, application, and product type.

- By Manufacturing Technology

On the basis of manufacturing technology, the polysilicon market is segmented into Siemens Process, Fluidized Bed Reactor (FBR) Process, and Upgraded Metallurgical-Grade Silicon Process. The Siemens Process segment held the largest market revenue share of approximately 72.4% in 2025 driven by its ability to produce ultra-high-purity polysilicon required for semiconductor manufacturing and high-efficiency solar photovoltaic applications. The process is widely adopted due to its superior material purity, established industrial infrastructure, and extensive use among leading global manufacturers.

The Fluidized Bed Reactor (FBR) Process segment is projected to register the fastest growth at a CAGR of 12.1% from 2026 to 2033, driven by rising demand for energy-efficient and lower-cost polysilicon production technologies. Increasing industry focus on reducing operational energy consumption and carbon emissions is accelerating adoption of FBR-based manufacturing systems among solar-grade polysilicon producers.

- By Form

On the basis of form, the polysilicon market is segmented into Chunks, Granules, and Rods. The Chunks segment accounted for the largest market revenue share of nearly 58.7% in 2025 owing to its widespread use in photovoltaic wafer manufacturing and conventional solar ingot production processes. Chunks are extensively preferred due to their compatibility with large-scale crystal growth systems and cost-effective handling during manufacturing operations.

The Granules segment is anticipated to witness the fastest growth at a CAGR of 11.6% from 2026 to 2033 driven by increasing adoption of fluidized bed reactor technologies and rising preference for continuous feeding processes in advanced solar manufacturing facilities. Improved operational efficiency and lower impurity generation are further supporting segment expansion.

- By End User Industry

On the basis of end user industry, the polysilicon market is segmented into Solar Photovoltaic and Electronics. The Solar Photovoltaic segment dominated the market with a revenue share of approximately 86.3% in 2025 due to rapidly increasing global solar panel installations and strong government support for renewable energy infrastructure development. Rising adoption of utility-scale solar projects and expanding residential rooftop solar systems are significantly contributing to segment growth.

The Electronics segment is expected to register the fastest CAGR of 9.8% from 2026 to 2033 driven by increasing semiconductor fabrication activities, rising demand for AI processors, and growing consumption of consumer electronics and electric vehicles. Expanding investments in domestic chip manufacturing facilities are further accelerating demand for electronic-grade polysilicon.

- By Application

On the basis of application, the polysilicon market is segmented into Photovoltaics, Monocrystalline Solar Panel, Multicrystalline Solar Panel, Electronics, Civilian Solar Small Equipment, and Others. The Photovoltaics segment held the largest market revenue share of around 61.9% in 2025 driven by increasing deployment of solar energy systems globally and strong transition toward clean electricity generation. Government incentives, declining solar installation costs, and rising environmental awareness are supporting widespread photovoltaic adoption.

The Monocrystalline Solar Panel segment is projected to witness the fastest growth at a CAGR of 13.4% from 2026 to 2033 owing to increasing preference for high-efficiency solar modules with superior energy conversion performance. Rapid technological advancements in TOPCon and heterojunction cell technologies are further driving demand for premium-grade polysilicon materials in monocrystalline panel production.

- By Product Type

On the basis of product type, the polysilicon market is segmented into Series Connection and Parallel Connection. The Series Connection segment accounted for the largest market revenue share of nearly 67.2% in 2025 due to its widespread adoption in photovoltaic systems requiring higher voltage output and improved energy transmission efficiency. The segment is extensively utilized across utility-scale solar farms and commercial renewable energy installations.

The Parallel Connection segment is anticipated to register the fastest growth at a CAGR of 10.3% from 2026 to 2033 driven by increasing adoption in small-scale solar applications, distributed energy systems, and advanced electronic configurations requiring stable current distribution. Rising deployment of residential solar systems and backup power applications is further supporting segment expansion.

Global Polysilicon Market Regional Analysis

- Asia-Pacific dominated the polysilicon market with the largest revenue share in 2025, driven by massive solar photovoltaic manufacturing capacity, rapid expansion of renewable energy infrastructure, and strong semiconductor production activities across China, Japan, South Korea, and India

- Manufacturers in the region highly value polysilicon due to its critical role in high-efficiency solar panels and semiconductor wafers used in electronics, electric vehicles, and advanced computing technologies

- This widespread adoption is further supported by government incentives for clean energy projects, rising investments in domestic semiconductor manufacturing, and the availability of large-scale low-cost production infrastructure, establishing Asia-Pacific as the global hub for polysilicon production and consumption

China Polysilicon Market Insight

The China polysilicon market captured the largest revenue share in 2025 within Asia-Pacific, fueled by the country’s dominant position in global solar panel manufacturing and large-scale renewable energy deployment. China continues to expand its photovoltaic production ecosystem through major investments in integrated solar manufacturing facilities and advanced wafer technologies. The presence of leading polysilicon manufacturers, combined with favorable government policies supporting clean energy and industrial expansion, is significantly driving market growth. Moreover, rising demand for semiconductors, electric vehicles, and energy storage systems is further contributing to polysilicon consumption across the country.

Japan Polysilicon Market Insight

The Japan polysilicon market is expected to witness strong growth from 2026 to 2033 due to the country’s advanced semiconductor manufacturing capabilities and growing focus on renewable energy transition. Japanese manufacturers are increasingly investing in high-purity electronic-grade polysilicon for AI processors, automotive electronics, and precision devices. In addition, the expansion of high-efficiency solar technologies and rising adoption of energy-efficient infrastructure are supporting market development. The integration of advanced silicon technologies in electronics and photovoltaic applications is expected to continue stimulating industry growth.

North America Polysilicon Market Insight

The North America polysilicon market is expected to witness significant growth from 2026 to 2033, driven by increasing investments in domestic semiconductor fabrication and solar manufacturing projects. Government initiatives promoting supply chain localization and energy independence are accelerating the establishment of new polysilicon production facilities in the U.S. and Canada. The region is also witnessing rising adoption of renewable energy systems and advanced electronic devices requiring high-purity silicon materials. Furthermore, supportive policy frameworks such as clean energy incentives and semiconductor funding programs are strengthening regional market expansion.

U.S. Polysilicon Market Insight

The U.S. polysilicon market is expected to witness significant growth from 2026 to 2033,, attributed to strong investments in solar energy infrastructure, semiconductor manufacturing, and advanced electronics production. The growing emphasis on reducing dependence on imported semiconductor materials is encouraging domestic manufacturing expansion. Increasing deployment of utility-scale solar farms and rising demand for electric vehicles are further supporting market growth. In addition, government funding programs and tax incentives for renewable energy and chip manufacturing are accelerating production capacity expansion across the country.

Europe Polysilicon Market Insight

The Europe polysilicon market is expected to witness the fastest growth rate from 2026 to 2033, primarily driven by ambitious carbon neutrality targets and increasing investments in renewable energy generation. European countries are significantly expanding solar photovoltaic installations and domestic semiconductor production capabilities to strengthen energy security and technological independence. The region is also experiencing increasing demand for sustainable and low-carbon manufacturing materials. Rising adoption of advanced solar technologies and supportive regulatory policies are further contributing to market growth across Europe.

U.K. Polysilicon Market Insight

The U.K. polysilicon market is expected to witness strong growth from 2026 to 2033, driven by increasing investments in renewable energy infrastructure and growing focus on clean electricity generation. Rising deployment of solar projects and energy transition initiatives is encouraging demand for high-quality photovoltaic materials. In addition, the expansion of semiconductor research and electronics manufacturing activities is supporting market development. Government commitments toward achieving net-zero carbon targets are expected to further stimulate polysilicon demand across energy and technology sectors.

Germany Polysilicon Market Insight

The Germany polysilicon market is expected to witness strong growth from 2026 to 2033, fueled by the country’s leadership in renewable energy adoption and advanced industrial manufacturing. Germany’s strong focus on energy transition and sustainable technology development is increasing demand for solar-grade and electronic-grade polysilicon materials. The country is also investing heavily in semiconductor fabrication and energy-efficient electronics manufacturing to strengthen technological competitiveness. Furthermore, rising integration of high-efficiency solar systems in residential and industrial applications is accelerating market expansion across Germany.

Global Polysilicon Market Share

The Polysilicon industry is primarily led by well-established companies, including:

- GCL-Poly Energy Holdings Limited (China)

- Wacker Chemie AG (Germany)

- OCI COMPANY Ltd. (South Korea)

- REC Silicon ASA (Norway)

- Tokuyama Corporation (Japan)

- DAQO NEW ENERGY CO,.LTD. (China)

- Hemlock Semiconductor Operations LLC (U.S.)

- activ solar Schweiz GmbH. (Switzerland)

- GCL-SI (China)

- Wuxi Suntech Power Co., Ltd. (China)

- Renesola (China)

- Yingli Solar (China)

- CSG HOLDING CO., LTD. (China)

- Qatar Solar Technologies (Qatar)

- Mitsubishi Polycrystalline Silicon America Corporation (U.S.)

- Lanco Solar (India)

- Kirloskar (India)

- Generac Power Systems, Inc. (U.S.)

- Caterpillar Inc. (U.S.)

- YANMAR HOLDINGS Co., Ltd. (Japan)

Latest Developments in Global Polysilicon Market

- In December 2025, leading Chinese polysilicon manufacturers, industry consolidation initiative, established a joint acquisition vehicle with registered capital of approximately CNY 3.0 billion to address industry oversupply and stabilize market conditions. The initiative is aimed at acquiring underperforming assets and optimizing production capacities across the polysilicon value chain. It is expected to improve pricing discipline and reduce excessive supply pressure in the global market. The move also strengthens collaboration among major producers and supports long-term operational sustainability. Overall, the development is anticipated to improve market balance and enhance profitability within the polysilicon industry

- In May 2025, United Solar Polysilicon, strategic partnership agreement, collaborated with OQ Alternative Energy to develop a 700 MW photovoltaic project integrating polysilicon feedstock supply with large-scale solar deployment. The partnership is intended to strengthen vertical integration between raw material suppliers and renewable energy developers. It also supports expansion of utility-scale clean energy infrastructure while ensuring stable demand for polysilicon products. The project is expected to improve supply chain efficiency and accelerate renewable energy adoption in the region. Overall, the collaboration reinforces the growing linkage between polysilicon manufacturing and solar power generation markets

- In August 2022, REC Silicon, supply chain partnership development, entered into a memorandum of understanding with Mississippi Silicon to negotiate a raw material supply agreement supporting a low-carbon and fully traceable U.S.-based solar supply chain. The agreement aims to establish integrated domestic production capabilities from raw silicon and polysilicon manufacturing to fully assembled solar modules. The initiative supports the expansion of local clean energy manufacturing infrastructure and reduces reliance on imported materials. It also strengthens transparency and sustainability across the U.S. solar value chain. Overall, the partnership is expected to accelerate domestic solar manufacturing growth and improve long-term supply security

- In April 2022, OCI, long-term supply agreement, signed a memorandum of understanding to supply polysilicon to South Korean solar manufacturer Hanwha Solutions under a contract valued at approximately USD 1.2 billion. The agreement is intended to ensure stable raw material availability for solar module production and strengthen strategic cooperation between the companies. It also supports growing photovoltaic manufacturing activities amid rising global solar panel demand. The partnership enhances OCI’s revenue visibility and strengthens its position in the global solar materials market. Overall, the agreement contributes to improved supply chain stability within the renewable energy sector

- In February 2021, GCL Technology Holdings Limited, long-term commercial supply agreement, finalized strategic deals with Tianjin Zhonghuan Semiconductor and LONGi Green Energy Technology for the long-term supply of polysilicon materials. The agreements are aimed at supporting increasing production requirements for high-efficiency solar wafers and photovoltaic modules in China. The partnerships strengthen GCL’s customer base and improve long-term production planning capabilities. They also support the rapid expansion of China’s integrated solar manufacturing ecosystem. Overall, the development reinforces supply chain stability and strengthens the country’s leadership in global photovoltaic manufacturing

SKU-

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Global Polysilicon Market, Supply Chain Analysis and Ecosystem Framework

To support market growth and help clients navigate the impact of geopolitical shifts, DBMR has integrated in-depth supply chain analysis into its Global Polysilicon Market research reports. This addition empowers clients to respond effectively to global changes affecting their industries. The supply chain analysis section includes detailed insights such as Global Polysilicon Market consumption and production by country, price trend analysis, the impact of tariffs and geopolitical developments, and import and export trends by country and HSN code. It also highlights major suppliers with data on production capacity and company profiles, as well as key importers and exporters. In addition to research, DBMR offers specialized supply chain consulting services backed by over a decade of experience, providing solutions like supplier discovery, supplier risk assessment, price trend analysis, impact evaluation of inflation and trade route changes, and comprehensive market trend analysis.

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.