Global Postmenopausal Vaginal Atrophy Pva Drugs Market

Market Size in USD Billion

CAGR :

%

USD

2.67 Billion

USD

4.76 Billion

2025

2033

USD

2.67 Billion

USD

4.76 Billion

2025

2033

| 2026 –2033 | |

| USD 2.67 Billion | |

| USD 4.76 Billion | |

| % | |

|

Postmenopausal Vaginal Atrophy (PVA) Drugs Market Size

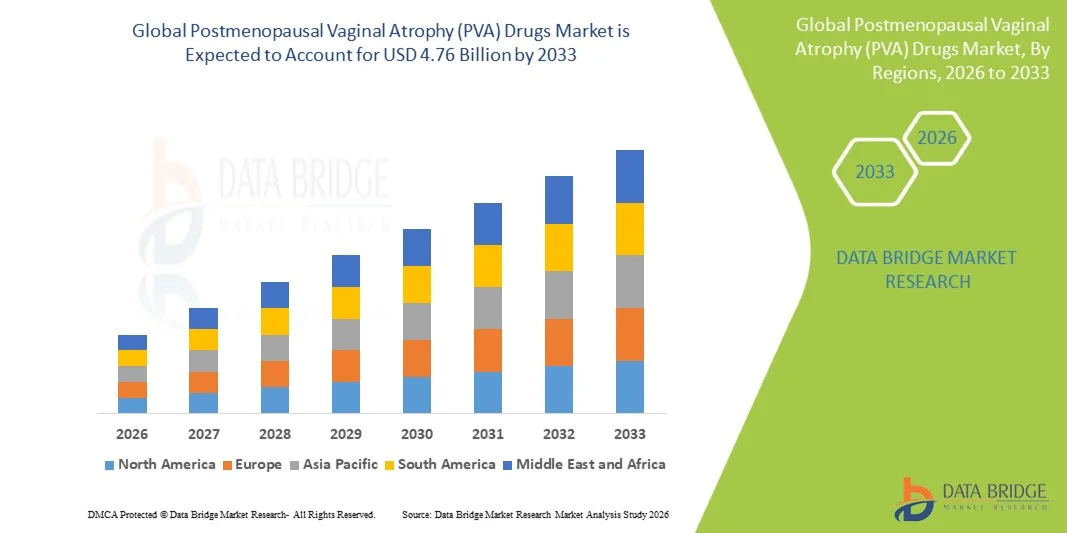

- The global Postmenopausal Vaginal Atrophy (PVA) drugs market size was valued at USD 2.67 billion in 2025 and is expected to reach USD 4.76 billion by 2033, at a CAGR of 7.50% during the forecast period

- The market growth is largely fueled by the increasing prevalence of postmenopausal vaginal atrophy due to the rising aging female population, alongside expanding awareness of genitourinary syndrome of menopause and its treatment options

- Furthermore, the growing adoption of both hormonal and non-hormonal therapeutic solutions, along with advancements in targeted and safer drug delivery systems, is strengthening treatment accessibility and effectiveness

Postmenopausal Vaginal Atrophy (PVA) Drugs Market Analysis

- Postmenopausal Vaginal Atrophy (PVA) drugs market, used for managing symptoms of estrogen deficiency such as vaginal dryness, irritation, and dyspareunia, is increasingly essential in women’s healthcare due to rising awareness of genitourinary syndrome of menopause and the growing focus on improving quality of life among postmenopausal women

- The escalating demand for Postmenopausal Vaginal Atrophy (PVA) drugs market is primarily driven by the rapidly aging female population, increasing diagnosis rates, and growing acceptance of both hormonal (estrogen therapy) and non-hormonal treatment options, supported by expanding awareness campaigns and improved healthcare access

- North America dominated the Postmenopausal Vaginal Atrophy (PVA) drugs market with the largest revenue share of 38.7% in 2025, supported by high diagnosis rates, strong healthcare infrastructure, and early adoption of advanced hormonal therapies, while the U.S. continues to experience significant treatment uptake driven by strong physician awareness and established pharmaceutical offerings

- Asia-Pacific is expected to be the fastest growing region in the Postmenopausal Vaginal Atrophy (PVA) drugs market during the forecast period due to a large aging population, improving women’s healthcare awareness, and increasing access to menopause-related treatments in emerging economies

- Topical Estrogen segment dominated the Postmenopausal Vaginal Atrophy (PVA) drugs market with a significant market share of 62.4% in 2025, owing to its high efficacy in relieving vaginal atrophy symptoms and its long-standing clinical use as the standard treatment option for moderate to severe cases

Report Scope and Postmenopausal Vaginal Atrophy (PVA) Drugs Market Segmentation

|

Attributes |

Postmenopausal Vaginal Atrophy (PVA) Drugs Key Market Insights |

|

Segments Covered |

|

|

Countries Covered |

North America

Europe

Asia-Pacific

Middle East and Africa

South America

|

|

Key Market Players |

|

|

Market Opportunities |

|

|

Value Added Data Infosets |

In addition to the insights on market scenarios such as market value, growth rate, segmentation, geographical coverage, and major players, the market reports curated by the Data Bridge Market Research also include in-depth expert analysis, patient epidemiology, pipeline analysis, pricing analysis, and regulatory framework |

Postmenopausal Vaginal Atrophy (PVA) Drugs Market Trends

“Rising Shift Toward Localized and Non-Hormonal Therapeutics”

- A significant and accelerating trend in the global Postmenopausal Vaginal Atrophy (PVA) drugs market is the growing shift toward localized vaginal therapies and non-hormonal treatment options, driven by safety concerns associated with systemic hormone replacement therapy and increasing patient preference for targeted symptom relief

- For instance, products such as ospemifene-based therapies and prasterone (DHEA) vaginal inserts are increasingly being prescribed as effective alternatives to conventional estrogen-based treatments, offering improved safety profiles for long-term use

- Advancements in drug formulation technologies, including sustained-release vaginal gels, creams, and pessaries, are enhancing drug efficacy and improving patient compliance by reducing dosing frequency and discomfort during application

- The integration of digital women’s health platforms and telemedicine consultations is facilitating faster diagnosis and prescription of PVA drugs, enabling better access to treatment, especially in underserved and rural populations

- Growing pharmaceutical R&D investments in selective estrogen receptor modulators (SERMs) and next-generation non-hormonal molecules are expanding the treatment pipeline and improving long-term therapeutic options for patients

- This trend toward more patient-centric, safer, and easy-to-administer therapies is fundamentally reshaping treatment expectations in women’s health, with companies focusing on innovative, low-dose, and localized drug delivery systems

- The demand for advanced Postmenopausal Vaginal Atrophy (PVA) drugs is growing rapidly across both developed and emerging regions, as awareness of menopause-related conditions and willingness to seek treatment continue to increase

Postmenopausal Vaginal Atrophy (PVA) Drugs Market Dynamics

Driver

“Rising Aging Population and Increasing Women’s Health Awareness”

- The increasing prevalence of postmenopausal vaginal atrophy driven by the rapidly aging global female population, along with growing awareness of women’s health disorders, is a major driver for the expanding demand for Postmenopausal Vaginal Atrophy (PVA) drugs market

- For instance, in 2025, multiple national health programs across developed economies have expanded menopause management initiatives, encouraging early diagnosis and treatment of genitourinary syndrome of menopause through hormone and non-hormone therapies

- As more women actively seek medical attention for symptoms such as vaginal dryness, irritation, and painful intercourse, healthcare providers are increasingly prescribing both estrogen-based and non-hormonal therapies, driving market expansion

- Furthermore, rising accessibility to gynecological care and improved reimbursement coverage for menopause-related treatments are significantly supporting the adoption of PVA drugs in both hospital and retail settings

- Expanding pharmaceutical pipelines focused on women’s health are introducing innovative low-dose and targeted therapies that improve safety and long-term treatment adherence

- Increasing collaboration between healthcare providers and public health organizations is improving early screening rates and boosting diagnosis of menopause-related conditions

- The increasing availability of advanced formulations such as low-dose estrogen creams and selective estrogen receptor modulators is further strengthening treatment adherence and clinical outcomes

- The growing focus on quality of life and active aging among postmenopausal women is further accelerating the uptake of Postmenopausal Vaginal Atrophy (PVA) drugs globally

Restraint/Challenge

“Safety Concerns and Limited Treatment Awareness in Emerging Regions”

- Concerns regarding potential side effects associated with long-term hormonal therapy, including risks of endometrial complications and breast cancer, remain a significant challenge limiting wider adoption of Postmenopausal Vaginal Atrophy (PVA) drugs

- For instance, in several clinical discussions and guideline updates, healthcare professionals continue to recommend cautious use of systemic estrogen therapy, particularly in patients with pre-existing risk factors, impacting overall prescription rates

- Limited awareness of Postmenopausal Vaginal Atrophy as a treatable medical condition among women in developing and rural regions further restricts early diagnosis and timely intervention

- In addition, cultural stigma and reluctance to discuss menopause-related symptoms in certain regions often delay treatment-seeking behavior, reducing market penetration

- Inadequate access to specialized gynecological care and shortage of trained healthcare professionals in rural healthcare systems further limit timely diagnosis and treatment adoption

- While non-hormonal alternatives are emerging, their relatively higher cost compared to traditional therapies can also act as a barrier for price-sensitive populations

- Overcoming these challenges through patient education, improved screening initiatives, and development of safer and affordable treatment options will be critical for sustained market growth

Postmenopausal Vaginal Atrophy (PVA) Drugs Market Scope

The market is segmented on the basis of drugs, product, end-users, and distribution channel.

- By Drugs

On the basis of drugs, the Postmenopausal Vaginal Atrophy (PVA) drugs market is segmented into topical estrogen, oral estrogen, and others. The topical estrogen segment dominated the market with the largest revenue share of 62.4% in 2025, driven by its high efficacy in delivering localized relief with minimal systemic absorption. Topical formulations such as creams, gels, and vaginal rings are widely preferred due to their targeted action on vaginal tissues, reducing symptoms such as dryness and irritation effectively. Physicians often recommend topical estrogen as a first-line therapy for moderate to severe cases due to its favorable safety profile. Increasing patient adherence and ease of administration further support its dominance. Strong clinical acceptance and long-standing therapeutic use also contribute to its leading position in the market. Expanding availability across hospital and retail pharmacies is further strengthening segment growth.

The others segment is expected to witness the fastest growth rate of 9.4% from 2026 to 2033, driven by increasing adoption of non-hormonal therapies such as SERMs, lubricants, and DHEA-based treatments. Rising concerns over hormone-related side effects are encouraging patients to shift toward safer alternatives. For instance, prasterone (DHEA) vaginal inserts are gaining traction as an effective hormone-free option for long-term symptom management. Growing R&D investments in novel drug classes are expanding treatment possibilities beyond conventional estrogen therapy. Increasing awareness of personalized menopause care is further supporting uptake. Expanding physician preference for safer alternatives in high-risk patients is accelerating segment growth globally.

- By Product

On the basis of product, the market is segmented into creams, pessaries, tablets, gels, solutions, inserts, and others. The creams segment dominated the market with a revenue share of 34.8% in 2025, owing to their widespread availability, ease of application, and strong clinical familiarity among healthcare providers. Cream-based estrogen therapies provide effective localized symptom relief and are commonly prescribed for initial treatment of vaginal atrophy. Patients prefer creams due to their flexibility in dosing and quick symptom relief. Their long-established presence in the market further strengthens physician confidence. Strong penetration in hospital and retail pharmacy channels also supports dominance. In addition, affordability compared to advanced delivery systems contributes to their leading position.

The inserts segment is expected to witness the fastest growth rate of 10.2% from 2026 to 2033, driven by rising demand for convenient, low-maintenance, and long-acting drug delivery systems. Vaginal inserts provide sustained release of medication, reducing the need for frequent application. For instance, estradiol vaginal inserts are increasingly prescribed for long-term maintenance therapy in postmenopausal women. Improved patient compliance and discreet usage are key advantages supporting adoption. Growing preference for minimally invasive treatment options is further boosting demand. Expanding innovation in biodegradable and controlled-release inserts is accelerating segment growth.

- By End-Users

On the basis of end-users, the market is segmented into hospitals, homecare, specialty clinics, and others. The hospitals segment dominated the market with a revenue share of 46.3% in 2025, due to high patient inflow, availability of specialized gynecologists, and strong diagnostic capabilities. Hospitals remain the primary point of diagnosis and prescription for moderate to severe cases of postmenopausal vaginal atrophy. Access to advanced hormonal therapies and controlled treatment monitoring further supports dominance. Patients often prefer hospital-based care for accurate diagnosis and safe initiation of hormone therapy. Strong reimbursement support in developed regions also contributes to hospital segment leadership. In addition, integration with women’s health programs strengthens adoption.

The homecare segment is expected to witness the fastest growth rate of 11.1% from 2026 to 2033, driven by increasing preference for self-managed treatment and at-home application of topical therapies. Growing availability of easy-to-use formulations such as creams, gels, and vaginal inserts supports this shift. For instance, patients are increasingly managing mild to moderate symptoms through prescribed home-based estrogen therapies. Rising telemedicine adoption is further enabling remote diagnosis and prescription. Increasing awareness of menopause self-care is boosting acceptance of home-based treatment options. Convenience, privacy, and reduced hospital visits are key growth drivers for this segment.

- By Distribution Channel

On the basis of distribution channel, the market is segmented into hospital pharmacy, retail pharmacy, and online pharmacy. The hospital pharmacy segment dominated the market with a revenue share of 42.9% in 2025, driven by strong linkage with hospital-based prescriptions and direct dispensing of hormonal therapies. Patients diagnosed in hospitals often prefer to purchase medications directly from in-house pharmacies for reliability and authenticity. Availability of specialized PVA drugs under medical supervision further strengthens this channel. Strong physician influence on prescription flow contributes to dominance. Hospital pharmacies also ensure better compliance for controlled hormone therapies. In addition, reimbursement support for hospital dispensed drugs supports segment leadership.

The online pharmacy segment is expected to witness the fastest growth rate of 12.4% from 2026 to 2033, driven by increasing digitalization of healthcare and rising adoption of telemedicine services. Patients prefer online platforms for privacy-sensitive conditions such as menopause-related disorders. For instance, prescription-based delivery of vaginal estrogen creams and non-hormonal therapies is rapidly increasing through e-pharmacy platforms. Growing internet penetration and smartphone usage are further accelerating adoption. Competitive pricing and doorstep delivery convenience are key advantages supporting growth. Expanding regulatory acceptance of online drug sales is further boosting this segment globally.

Postmenopausal Vaginal Atrophy (PVA) Drugs Market Regional Analysis

- North America dominated the Postmenopausal Vaginal Atrophy (PVA) drugs market with the largest revenue share of 38.7% in 2025, supported by high diagnosis rates, strong healthcare infrastructure, and early adoption of advanced hormonal therapies

- Consumers in the region highly value the availability of effective treatment options, strong healthcare infrastructure, and easy access to gynecologists, along with increasing acceptance of estrogen-based and localized vaginal therapies for symptom management

- This widespread adoption is further supported by high healthcare expenditure, strong insurance coverage, and proactive screening programs for menopause-related conditions, establishing PVA drugs as a standard component of women’s healthcare management in both hospital and specialty clinic settings

U.S. Postmenopausal Vaginal Atrophy (PVA) Drugs Market Insight

The U.S. Postmenopausal Vaginal Atrophy (PVA) drugs market captured the largest revenue share of 81% in North America in 2025, driven by high awareness of menopause-related health conditions and strong adoption of advanced hormonal and non-hormonal therapies. Consumers are increasingly prioritizing effective symptom management solutions such as topical estrogen therapies, vaginal inserts, and non-hormonal alternatives for improved quality of life. The growing preference for patient-centric women’s healthcare solutions, combined with strong physician awareness and early diagnosis practices, further propels the PVA drugs market. Moreover, the increasing integration of telemedicine platforms and digital health services is significantly contributing to market expansion.

Europe Postmenopausal Vaginal Atrophy (PVA) Drugs Market Insight

The Europe Postmenopausal Vaginal Atrophy (PVA) drugs market is projected to expand at a substantial CAGR throughout the forecast period, primarily driven by rising aging population, increasing awareness of menopause-related disorders, and strong healthcare systems. The region’s focus on preventive healthcare and early treatment of genitourinary syndrome of menopause is fostering adoption of PVA drugs. European consumers are also increasingly opting for non-hormonal and safer treatment alternatives due to concerns over long-term hormone therapy use. The market is witnessing steady growth across hospitals, specialty clinics, and retail pharmacies, supported by strong regulatory frameworks and reimbursement policies.

U.K. Postmenopausal Vaginal Atrophy (PVA) Drugs Market Insight

The U.K. Postmenopausal Vaginal Atrophy (PVA) drugs market is anticipated to grow at a noteworthy CAGR during the forecast period, driven by increasing awareness of women’s health issues and rising demand for menopause symptom management solutions. In addition, growing acceptance of hormonal and localized estrogen therapies is encouraging treatment adoption among postmenopausal women. The U.K.’s strong healthcare infrastructure and expanding access to gynecological care are expected to continue stimulating market growth. Furthermore, rising telehealth adoption and online pharmacy usage are improving accessibility of PVA drugs across the country.

Germany Postmenopausal Vaginal Atrophy (PVA) Drugs Market Insight

The Germany Postmenopausal Vaginal Atrophy (PVA) drugs market is expected to expand at a considerable CAGR during the forecast period, fueled by increasing awareness of menopausal disorders and demand for advanced, evidence-based therapies. Germany’s strong pharmaceutical research ecosystem and emphasis on high-quality healthcare promote adoption of both hormonal and non-hormonal treatment options. The integration of vaginal estrogen therapies with patient-centric treatment approaches is becoming increasingly prevalent. Moreover, growing preference for safe, localized drug delivery systems aligns with the country’s focus on precision and preventive healthcare solutions.

Asia-Pacific Postmenopausal Vaginal Atrophy (PVA) Drugs Market Insight

The Asia-Pacific Postmenopausal Vaginal Atrophy (PVA) drugs market is poised to grow at the fastest CAGR of 8.2% during the forecast period of 2026 to 2033, driven by a rapidly aging female population, increasing urbanization, and improving awareness of menopause-related conditions. The region’s growing focus on women’s healthcare, supported by expanding healthcare infrastructure, is driving adoption of PVA drugs. Furthermore, rising availability of affordable treatment options and increasing penetration of pharmaceutical companies are expanding market access. Government initiatives promoting women’s health awareness are also supporting market growth across emerging economies.

Japan Postmenopausal Vaginal Atrophy (PVA) Drugs Market Insight

The Japan Postmenopausal Vaginal Atrophy (PVA) drugs market is gaining momentum due to the country’s rapidly aging population, advanced healthcare system, and strong focus on quality of life in elderly care. The market is driven by increasing adoption of hormonal and localized therapies for effective symptom management. Japan’s high level of medical awareness supports early diagnosis and treatment of menopausal conditions. In addition, integration of advanced pharmaceutical formulations and strong clinical acceptance of estrogen-based therapies are fueling market expansion.

India Postmenopausal Vaginal Atrophy (PVA) Drugs Market Insight

The India Postmenopausal Vaginal Atrophy (PVA) drugs market accounted for a significant revenue share in Asia Pacific in 2025, attributed to the country’s large aging population, rising awareness of women’s health, and improving access to gynecological care. India is witnessing increasing adoption of affordable hormonal and non-hormonal therapies across urban and semi-urban regions. The expansion of healthcare infrastructure, along with growing penetration of online pharmacies, is making PVA drugs more accessible. Furthermore, rising focus on preventive healthcare and women’s wellness initiatives is contributing to steady market growth.

Postmenopausal Vaginal Atrophy (PVA) Drugs Market Share

The Postmenopausal Vaginal Atrophy (PVA) Drugs industry is primarily led by well-established companies, including:

- AbbVie Inc. (U.S.)

- Organon & Co. (U.S.)

- Sumitomo Pharma Co., Ltd. (Japan)

- Bayer AG (Germany)

- Pfizer Inc. (U.S.)

- Duchesnay Inc. (Canada)

- Millicent Pharma Limited (Ireland)

- Myovant Sciences, Inc. (U.S.)

- Novo Nordisk A/S (Denmark)

- Astellas Pharma Inc. (Japan)

- Theramex (U.K.)

- Teva Pharmaceutical Industries Ltd. (Israel)

- Endoceutics Inc. (Canada)

- Amgen Inc. (U.S.)

- Novartis AG (Switzerland)

- Eli Lilly and Company (U.S.)

- Viatris Inc. (U.S.)

- Cosette Pharmaceuticals, Inc. (U.S.)

- HRA Pharma (France)

- Ferring Pharmaceuticals (Switzerland)

What are the Recent Developments in Global Postmenopausal Vaginal Atrophy (PVA) Drugs Market?

- In April 2026, Contemporary OB/GYN highlighted ongoing clinical adoption of ospemifene as an FDA-approved oral treatment for dyspareunia associated with PVA, emphasizing its role as a key non-steroidal therapy improving vaginal tissue health and reducing painful intercourse symptoms in postmenopausal women

- In January 2026, MDPI reported continued clinical expansion of non-hormonal and localized therapies for Postmenopausal Vaginal Atrophy (PVA), highlighting growing use of prasterone (DHEA) vaginal suppositories and selective estrogen receptor modulators (SERMs) such as ospemifene as effective FDA-approved treatment alternatives to traditional estrogen therapy

- In January 2025, peer-reviewed pharmacology research on ospemifene emphasized its continued clinical use as an FDA-approved selective estrogen receptor modulator (SERM) for treating moderate to severe dyspareunia associated with Postmenopausal Vaginal Atrophy (PVA), confirming sustained efficacy and safety across long-term studies

- In October 2024, Australian Prescriber published updated clinical guidance on prasterone (Intrarosa), highlighting its approval as an intravaginal DHEA therapy for moderate to severe Postmenopausal Vaginal Atrophy (PVA), reinforcing its role as a non-estrogen alternative with localized action and minimal systemic exposure

- In March 2024, clinical discussions and patient reports highlighted increasing real-world adoption of vaginal estrogen therapies such as estradiol pessaries (e.g., Vagifem) for Postmenopausal Vaginal Atrophy (PVA), with evidence showing strong improvement in vaginal dryness, irritation, and sexual discomfort symptoms, reinforcing its role as a first-line localized hormone treatment option in routine gynecological care

SKU-

Get online access to the report on the World's First Market Intelligence Cloud

- Interactive Data Analysis Dashboard

- Company Analysis Dashboard for high growth potential opportunities

- Research Analyst Access for customization & queries

- Competitor Analysis with Interactive dashboard

- Latest News, Updates & Trend analysis

- Harness the Power of Benchmark Analysis for Comprehensive Competitor Tracking

Research Methodology

Data collection and base year analysis are done using data collection modules with large sample sizes. The stage includes obtaining market information or related data through various sources and strategies. It includes examining and planning all the data acquired from the past in advance. It likewise envelops the examination of information inconsistencies seen across different information sources. The market data is analysed and estimated using market statistical and coherent models. Also, market share analysis and key trend analysis are the major success factors in the market report. To know more, please request an analyst call or drop down your inquiry.

The key research methodology used by DBMR research team is data triangulation which involves data mining, analysis of the impact of data variables on the market and primary (industry expert) validation. Data models include Vendor Positioning Grid, Market Time Line Analysis, Market Overview and Guide, Company Positioning Grid, Patent Analysis, Pricing Analysis, Company Market Share Analysis, Standards of Measurement, Global versus Regional and Vendor Share Analysis. To know more about the research methodology, drop in an inquiry to speak to our industry experts.

Customization Available

Data Bridge Market Research is a leader in advanced formative research. We take pride in servicing our existing and new customers with data and analysis that match and suits their goal. The report can be customized to include price trend analysis of target brands understanding the market for additional countries (ask for the list of countries), clinical trial results data, literature review, refurbished market and product base analysis. Market analysis of target competitors can be analyzed from technology-based analysis to market portfolio strategies. We can add as many competitors that you require data about in the format and data style you are looking for. Our team of analysts can also provide you data in crude raw excel files pivot tables (Fact book) or can assist you in creating presentations from the data sets available in the report.